Determining an appropriate wage to afford rent is a critical financial consideration, as housing costs typically represent a significant portion of one’s income. To ensure financial stability, it’s essential to calculate a wage that not only covers rent but also leaves room for other essential expenses like utilities, groceries, transportation, and savings. A common rule of thumb is the 30% rule, which suggests that rent should not exceed 30% of your gross monthly income. However, this may vary based on location, cost of living, and personal financial goals. Factors such as local minimum wage laws, industry standards, and negotiating power also play a role in determining a fair wage. By carefully assessing your budget, researching local housing costs, and aligning your income with your expenses, you can establish a wage that allows you to afford rent while maintaining a balanced and sustainable lifestyle.

Explore related products

What You'll Learn

- Local Cost of Living: Research area-specific expenses to determine necessary income for rent and basics

- /30/20 Budget Rule: Allocate 50% of income to needs, including rent, for stability

- Rent-to-Income Ratio: Aim for rent under 30% of gross monthly income

- Hidden Housing Costs: Factor in utilities, maintenance, and parking when calculating affordability

- Negotiating Rent: Understand local laws and market trends to secure fair rental terms

![]()

Local Cost of Living: Research area-specific expenses to determine necessary income for rent and basics

The cost of living varies dramatically by location, making it essential to research area-specific expenses before determining the income needed to afford rent and basics. For instance, a studio apartment in San Francisco averages $2,800 monthly, while a similar unit in Tulsa, Oklahoma, costs around $700. This disparity highlights why a one-size-fits-all wage calculation falls short. To avoid financial strain, tailor your income expectations to the local economy.

Begin by identifying key expenses beyond rent, such as groceries, transportation, and utilities, which fluctuate by region. In New York City, monthly groceries for one person average $400, whereas in rural Iowa, the same basket might cost $250. Use tools like the Economic Policy Institute’s Family Budget Calculator or Numbeo’s Cost of Living Index to compare expenses across cities. These resources provide data-driven insights into how far your income will stretch in a specific area.

Next, calculate the income required to cover these costs comfortably. A common rule of thumb is the 30% rule, where rent should not exceed 30% of your gross income. However, in high-cost areas, this may be unrealistic. For example, in Los Angeles, where median rent is $2,500, you’d need a monthly income of $8,333 to meet this threshold. Adjust your expectations by prioritizing needs over wants and considering shared housing or remote work opportunities to bridge the gap.

Finally, factor in local taxes and healthcare costs, which can significantly impact your take-home pay. States like Texas have no income tax, while California’s top rate reaches 13.3%. Health insurance premiums vary by state and employer, so research average costs in your area. By accounting for these nuances, you’ll arrive at a more accurate wage target that ensures financial stability in your chosen location.

Simplify Rent Payments: A Step-by-Step Guide to Setting Up Payment in Rent Track

You may want to see also

Explore related products

![]()

50/30/20 Budget Rule: Allocate 50% of income to needs, including rent, for stability

Determining a wage that comfortably covers rent often leads to the 50/30/20 budget rule, a framework that divides income into needs, wants, and savings. This rule suggests allocating 50% of your after-tax income to necessities, including rent, utilities, groceries, and transportation. For renters, this means your housing costs should ideally not exceed half of your take-home pay. For example, if your monthly income is $4,000, rent should cap at $2,000 to maintain stability. This approach ensures you’re not overextended financially while still having room for other essentials.

Analyzing the 50/30/20 rule reveals its practicality for renters. By capping rent at 50% of income, you avoid the pitfalls of being "house poor," where housing consumes most of your earnings, leaving little for emergencies or leisure. For instance, a $3,500 monthly income would allow for $1,750 in rent, leaving $1,050 for other needs and $1,050 for wants and savings. This balance fosters financial resilience, especially in high-cost-of-living areas where rent often competes with other priorities. However, it’s crucial to adjust this rule based on local living costs and personal circumstances.

To implement this rule effectively, start by calculating your after-tax income and dividing it into the 50/30/20 categories. Use budgeting tools or apps to track spending and ensure rent stays within the 50% threshold. If your rent exceeds this limit, consider downsizing, finding a roommate, or negotiating with your landlord. For younger renters or those in entry-level jobs, this rule may require prioritizing affordability over amenities. Conversely, higher earners might allocate less than 50% to needs, freeing up funds for savings or investments.

A persuasive argument for the 50/30/20 rule is its ability to prevent financial stress. Renters who adhere to this guideline are less likely to rely on credit cards or loans to cover living expenses. For example, a $50,000 annual salary translates to roughly $3,100 monthly after taxes, allowing for $1,550 in rent. This leaves $1,550 for other needs and $930 for discretionary spending and savings. By sticking to this structure, you build a safety net while enjoying financial flexibility, making it a sustainable approach for long-term stability.

In conclusion, the 50/30/20 rule offers a clear, actionable strategy for renters to align their wages with housing costs. It’s not a one-size-fits-all solution but a starting point for tailoring your budget to your lifestyle. Whether you’re a recent graduate or a seasoned professional, this rule encourages mindful spending and prioritization. By keeping rent within 50% of your income, you create a foundation for financial security, ensuring that your wage not only covers rent but also supports your overall well-being.

Understanding Section 8 Rental Rates: What Tenants Need to Know

You may want to see also

Explore related products

![]()

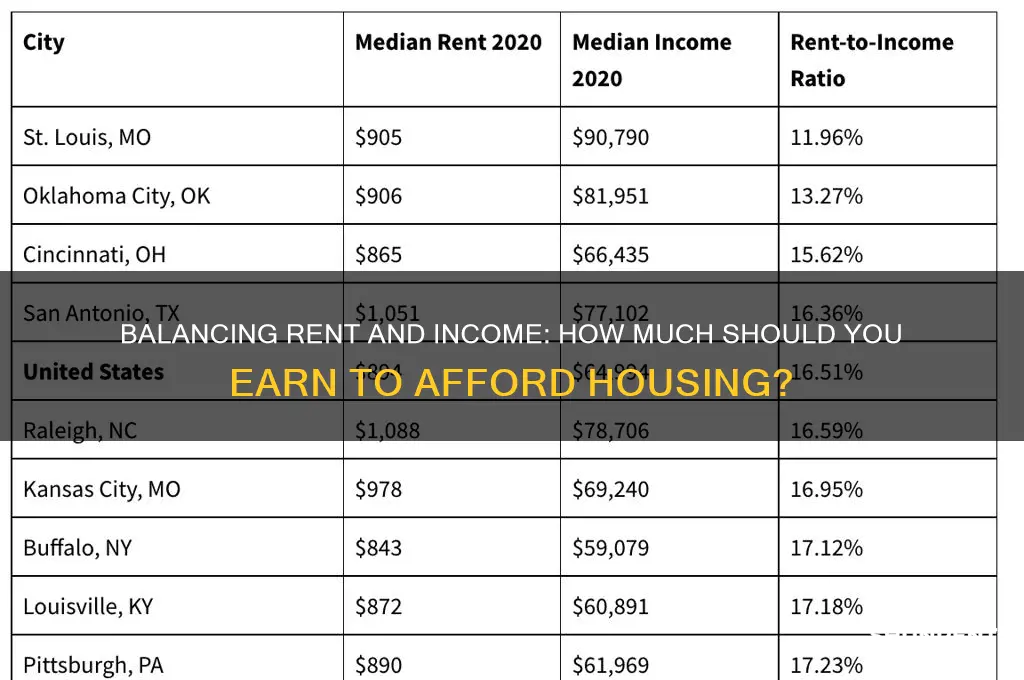

Rent-to-Income Ratio: Aim for rent under 30% of gross monthly income

A common rule of thumb in personal finance is the 30% rent-to-income ratio, which suggests that your monthly rent should not exceed 30% of your gross monthly income. This guideline helps ensure that you have enough income left over to cover other essential expenses, savings, and discretionary spending. For example, if your gross monthly income is $4,000, your rent should ideally be no more than $1,200. This simple calculation provides a baseline for budgeting and can help you avoid financial strain.

To apply this rule effectively, start by calculating your gross monthly income, which is your total earnings before taxes and deductions. If you’re paid bi-weekly, multiply your paycheck by 26 (the number of pay periods in a year) and then divide by 12 to get your monthly income. Next, multiply this figure by 0.30 to determine your maximum affordable rent. Keep in mind that this ratio is a starting point, not a rigid rule. Factors like high cost-of-living areas, student loans, or other financial obligations may require you to adjust this percentage downward to maintain a balanced budget.

Critics of the 30% rule argue that it may not reflect the realities of renters in expensive cities like New York or San Francisco, where housing costs can easily surpass 50% of income. However, this ratio remains a useful benchmark for most individuals and families. To make it work in high-cost areas, consider strategies like finding a roommate to split rent, negotiating lease terms, or exploring government housing assistance programs. Additionally, if you’re consistently spending more than 30% on rent, prioritize increasing your income or reducing other expenses to regain financial stability.

A practical tip for adhering to this ratio is to reverse-engineer your ideal rent based on your income. For instance, if you want to spend no more than $1,500 on rent, you’d need a gross monthly income of at least $5,000. This approach can guide career decisions, such as negotiating a higher salary or pursuing side gigs to meet your housing goals. Remember, the 30% rule isn’t just about affordability—it’s about creating a sustainable financial foundation that allows you to save for emergencies, invest in your future, and enjoy your lifestyle without being burdened by rent.

RV Rentals: Do You Need a Business License?

You may want to see also

Explore related products

![]()

Hidden Housing Costs: Factor in utilities, maintenance, and parking when calculating affordability

Rent often dominates the affordability conversation, but it’s merely the tip of the housing expense iceberg. Beneath the surface lurk utilities, maintenance, and parking costs—hidden fees that can sink your budget if overlooked. For instance, a $1,200 monthly rent might seem manageable on a $40,000 salary, but add $200 for electricity, $100 for water, and $50 for internet, and suddenly you’re at $1,550—38% of your gross income, edging dangerously close to the 30% affordability threshold. This example underscores why a holistic view of housing costs is essential.

Utilities are the silent budget drainers, varying wildly by location and lifestyle. In Phoenix, summer AC bills can soar to $400 monthly, while in Seattle, heating costs spike in winter. To avoid surprises, research average utility costs in your area and factor in your usage habits. For example, a single person working from home will consume more electricity than someone in an office. Pro tip: Use online calculators like the U.S. Energy Department’s Home Energy Score to estimate costs based on property size and efficiency.

Maintenance is another overlooked expense, especially for renters who assume landlords cover everything. While major repairs are typically the landlord’s responsibility, tenants often pay for minor fixes, pest control, or appliance replacements. Set aside 1–2% of your rent monthly for these costs. For a $1,200 rent, that’s $12–24 per month—a small price for peace of mind. Additionally, renters insurance, averaging $15–$30 monthly, protects your belongings from theft or damage, a cost often forgotten until disaster strikes.

Parking, though seemingly trivial, can be a budget buster in urban areas. In cities like San Francisco, monthly parking permits cost upwards of $300, while suburban renters might pay $50–$100 for a garage or reserved spot. If parking isn’t included in your rent, factor it into your calculations. Alternatively, consider living in transit-friendly neighborhoods where you can forgo a car, saving on parking, gas, and insurance.

The takeaway? Rent affordability isn’t just about the monthly payment—it’s about the total housing cost. To ensure financial stability, calculate your all-in expenses, including utilities, maintenance, and parking. Aim to keep these combined costs below 40% of your gross income. By accounting for these hidden fees, you’ll avoid the trap of overcommitting and build a budget that’s as sturdy as the roof over your head.

Renting 'Ballad of Songbirds & Snakes': A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Negotiating Rent: Understand local laws and market trends to secure fair rental terms

Rent negotiation is a skill, and like any skill, it requires knowledge and strategy. Before entering into any rental agreement, understanding the legal framework that governs tenant-landlord relationships in your area is crucial. Local laws often dictate the maximum allowable rent increase, security deposit limits, and the conditions under which a landlord can terminate a tenancy. For instance, in some cities, rent control laws cap annual rent increases, providing tenants with long-term affordability. Knowing these regulations empowers you to negotiate from a position of strength, ensuring you're not overpaying or agreeing to unfair terms.

Market trends are the other piece of this puzzle. Researching local rental market dynamics can reveal whether you're in a tenant's or landlord's market. In a tenant's market, where vacancy rates are high, landlords may be more open to negotiations, offering concessions like lower rent, waived fees, or even rent-free periods. Conversely, in a tight market with low vacancy rates, your negotiating power diminishes. Utilize online tools and local real estate reports to gather data on average rents, vacancy rates, and popular amenities in your desired neighborhood. This information will help you make a compelling case for your proposed rental terms.

Here's a step-by-step approach to negotiating rent effectively: First, determine your budget and the maximum rent you can afford, considering the 30% rule, which suggests that rent should not exceed 30% of your gross income. Then, research comparable properties to understand the market rate for your desired location and amenities. When negotiating, lead with confidence and provide data to support your proposed rent. For example, if similar units in the area are renting for less, present this information to the landlord. Be prepared to negotiate other terms, such as lease duration or included utilities, if the landlord is firm on the rent.

A common misconception is that rent negotiation is solely about haggling over price. However, it's a nuanced process that involves understanding the landlord's perspective and finding a mutually beneficial agreement. Landlords often prefer long-term, reliable tenants, so highlighting your stability and commitment can be a powerful negotiating tool. Additionally, offering to sign a longer lease or providing excellent references can make your application stand out and give you leverage in rent negotiations.

In the context of 'what should my wage be to afford rent,' negotiating rent is a proactive way to ensure your housing costs align with your income. By understanding local laws and market trends, you can secure a fair deal, potentially saving hundreds or even thousands of dollars annually. This approach empowers renters to take control of their housing expenses, making it a vital strategy for anyone looking to manage their budget effectively. Remember, knowledge is power, and in the rental market, it can translate into significant savings.

Red Roof Inn's Policy: Renting to 18-Year-Olds?

You may want to see also

Frequently asked questions

To determine your ideal wage, calculate 30% of your monthly gross income, which is the recommended maximum for rent. For example, if your rent is $1,500, your monthly income should be at least $5,000.

Financial experts recommend spending no more than 30% of your gross monthly income on rent to maintain a balanced budget and avoid financial strain.

If your wage is lower, consider finding a roommate, moving to a more affordable area, or increasing your income through side jobs or negotiations with your employer.

Rent costs vary significantly by location. High-cost areas like cities may require a higher wage to afford rent, while rural areas may allow for a lower income to cover housing expenses.