Prepaid rent expense is a type of asset account that represents the portion of rent paid in advance for a future period. It is classified as a current asset on the balance sheet because it provides a benefit that will be realized within one year or the operating cycle, whichever is longer. When a business pays rent upfront for a period that extends beyond the current accounting period, the prepaid amount is initially recorded as an asset. As the rental period progresses, the prepaid rent is gradually recognized as an expense through periodic adjustments, typically on a monthly basis, to reflect the portion of rent that pertains to the current period. This ensures that expenses are matched with the revenues they help generate, adhering to the matching principle in accounting.

| Characteristics | Values |

|---|---|

| Account Type | Asset |

| Classification | Current Asset |

| Nature | Prepaid Expense |

| Timing | Paid in advance for future benefit |

| Recognition | Recorded when payment is made, not when expense is incurred |

| Adjustment | Adjusted monthly through amortization (expense recognition) |

| Financial Statement Impact | Increases assets on the balance sheet; decreases expenses on the income statement over time |

| Example | Paying $12,000 for a year's rent in advance |

| Contra Account | None (not a contra account) |

| Reversal | Expense is recognized monthly, reducing the prepaid rent balance |

Explore related products

What You'll Learn

- Prepaid Rent Classification: Prepaid rent is an asset, not an expense, until amortized over time

- Expense Recognition: Rent expense is recognized monthly, matching the period benefited by the payment

- Balance Sheet Impact: Prepaid rent appears as a current asset on the balance sheet

- Income Statement Role: Rent expense is recorded on the income statement as a periodic cost

- Amortization Process: Prepaid rent is amortized to expense over the rental period systematically

![]()

Prepaid Rent Classification: Prepaid rent is an asset, not an expense, until amortized over time

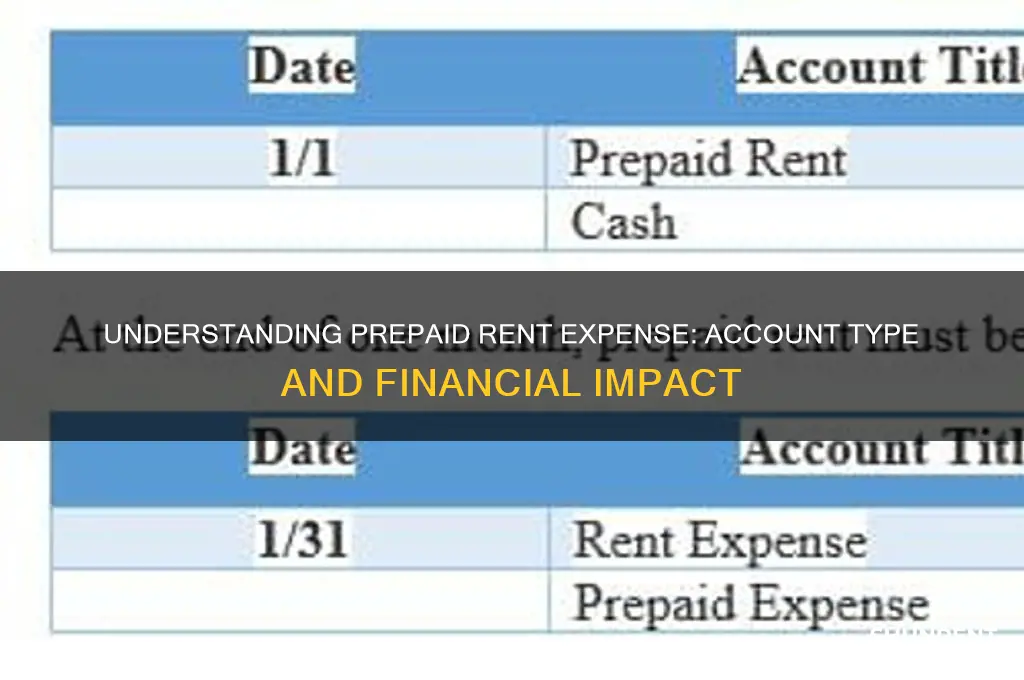

Prepaid rent often confuses those new to accounting because its name suggests an expense, but its treatment on the balance sheet tells a different story. Unlike immediate expenses such as office supplies or utilities, prepaid rent represents a payment made in advance for future use of a property. This distinction is critical: the payment itself is not an expense but an asset, reflecting the value of the rental period yet to be consumed. For instance, if a business pays $12,000 upfront for a year’s rent, that $12,000 is recorded as a prepaid rent asset, not as an expense, until the rental period begins.

The classification of prepaid rent as an asset aligns with the matching principle in accounting, which requires expenses to be recognized in the same period as the revenue they help generate. If prepaid rent were expensed immediately, it would distort financial statements by overstating expenses in the payment period and understating them in subsequent periods. Instead, the asset is systematically reduced through amortization, typically on a straight-line basis. For example, a $12,000 annual rent payment would be amortized as a $1,000 monthly expense, ensuring expenses are matched with the corresponding benefits over time.

Amortization is the process that transforms prepaid rent from an asset into an expense. This process requires careful tracking and journal entries to reflect the gradual consumption of the prepaid amount. Each month, an adjusting entry is made to debit rent expense and credit prepaid rent, reducing the asset account while increasing the expense account. For businesses, this ensures financial statements accurately represent the economic reality of the rental agreement. Failure to amortize prepaid rent properly can lead to misstated financial reports, potentially misleading stakeholders about the company’s financial health.

Practical application of prepaid rent classification varies by industry and scale. Small businesses might handle this manually, while larger enterprises use accounting software to automate amortization schedules. For example, a retail store leasing a storefront would record the prepaid rent as an asset and then amortize it monthly, aligning the expense with the store’s operational use of the space. Similarly, a tech startup with a multi-year office lease would spread the prepaid rent expense over the lease term, ensuring consistency in financial reporting. Understanding this process is essential for accurate bookkeeping and compliance with accounting standards.

In conclusion, prepaid rent is not an expense at the time of payment but an asset that becomes an expense over time through amortization. This classification ensures adherence to accounting principles and provides a clear financial picture of a company’s obligations and resources. By recognizing prepaid rent as an asset and systematically amortizing it, businesses maintain transparency and accuracy in their financial statements, fostering trust among investors, creditors, and other stakeholders.

Rent vs. Lease: Understanding Storefront Agreements for Your Business

You may want to see also

Explore related products

![]()

Expense Recognition: Rent expense is recognized monthly, matching the period benefited by the payment

Prepaid rent expense is an asset account that represents the amount of rent paid in advance for a future period. This concept is crucial in accounting because it ensures that expenses are recognized in the period they benefit, aligning with the matching principle. For instance, if a company pays $12,000 for a year’s rent in January, only $1,000 is recognized as rent expense each month, reflecting the monthly benefit received. This approach prevents distortion in financial statements by avoiding the recognition of a large expense in a single month.

The process of recognizing rent expense monthly involves a systematic adjustment. At the end of each month, an adjusting journal entry is made to transfer a portion of the prepaid rent from the asset account to the rent expense account. For example, the entry would debit rent expense for $1,000 and credit prepaid rent for the same amount. This method ensures that the income statement accurately reflects the cost of occupying the rented space during the reporting period, while the balance sheet shows the remaining prepaid amount as an asset.

From a practical standpoint, this practice is essential for businesses to maintain accurate financial records and comply with accounting standards like GAAP or IFRS. Misrecognition of rent expense can lead to overstated profits in the prepaid month and understated profits in subsequent months. For small businesses, this could impact cash flow projections and decision-making. Larger corporations, on the other hand, might face regulatory scrutiny if expenses are not matched correctly. Thus, monthly recognition is not just a procedural step but a critical component of financial integrity.

Comparatively, prepaid rent differs from other prepaid expenses like insurance or supplies, as rent often involves larger sums and longer periods. While the principle of expense recognition remains the same, the impact of misapplication is more pronounced with rent due to its size. For example, a $10,000 annual insurance premium might be less noticeable if misrecognized, but a $120,000 annual rent payment could significantly skew financial results. This highlights the need for meticulous tracking and adjustment of prepaid rent.

In conclusion, recognizing rent expense monthly is a fundamental practice that ensures financial statements reflect the economic reality of a business’s operations. By matching the expense to the period benefited, companies maintain transparency and accuracy in their reporting. Whether for a small startup or a multinational corporation, this approach is indispensable for reliable financial management and compliance with accounting principles.

Renting a One-Week Timeshare in Hilton Head: A Quick Guide

You may want to see also

Explore related products

![]()

Balance Sheet Impact: Prepaid rent appears as a current asset on the balance sheet

Prepaid rent is classified as a current asset on the balance sheet, reflecting payments made in advance for future rental periods. This categorization stems from its liquidity and short-term nature, as it represents a resource expected to be consumed within one year or the operating cycle, whichever is longer. Unlike long-term assets, prepaid rent does not require depreciation and is fully expensed over the rental period, aligning with the matching principle of accounting.

Consider a small business that pays $12,000 annually for office space in January, covering rent from January to December. On the balance sheet, $12,000 is initially recorded as prepaid rent under current assets. Each month, $1,000 is recognized as rent expense, reducing the prepaid rent balance by the same amount. By year-end, the prepaid rent account is depleted, and the full $12,000 has been expensed, accurately reflecting the consumption of the prepaid resource.

The placement of prepaid rent as a current asset is critical for financial analysis. It enhances liquidity ratios, such as the current ratio, by increasing the numerator (current assets) without affecting liabilities. However, investors and creditors must interpret this asset cautiously, as it does not represent cash or inventory but rather a prepaid expense. Misinterpretation could lead to overestimating a company’s operational liquidity or short-term financial health.

To ensure accurate reporting, businesses should maintain detailed records of prepaid rent agreements, including payment terms, rental periods, and amortization schedules. For instance, if a company prepays $6,000 for six months of rent, it should systematically recognize $1,000 monthly as rent expense. Accounting software can automate this process, reducing the risk of errors and ensuring compliance with accounting standards like GAAP or IFRS.

In summary, prepaid rent’s classification as a current asset on the balance sheet serves both accounting and analytical purposes. It adheres to the matching principle while providing insights into a company’s short-term financial position. By understanding its mechanics and implications, stakeholders can better assess liquidity and operational efficiency, making informed decisions based on accurate financial data.

Is $1000 Monthly Rent Reasonable? A Comprehensive Financial Analysis

You may want to see also

Explore related products

![]()

Income Statement Role: Rent expense is recorded on the income statement as a periodic cost

Rent expense, a critical component of a company's financial health, is meticulously recorded on the income statement as a periodic cost. This classification is not arbitrary; it reflects the matching principle in accounting, which dictates that expenses should be recognized in the same period as the revenues they help generate. For instance, if a retail store pays rent for a storefront, that cost is allocated over the months the store operates, aligning with the sales it facilitates. This approach ensures that financial statements provide a clear, accurate snapshot of a company's profitability during a specific period.

Consider the practical implications of this recording method. Suppose a business prepays $12,000 for a year’s rent in January. Instead of expensing the entire amount immediately, it is spread evenly across 12 months, with $1,000 recorded each month as rent expense. This treatment prevents distortion in the income statement, avoiding an artificially low profit in January and inflated profits in subsequent months. For small businesses or startups, this practice is particularly vital, as it helps maintain a realistic view of cash flow and operational efficiency.

The income statement’s role in capturing rent expense periodically also aids stakeholders in making informed decisions. Investors, for example, rely on consistent expense reporting to assess a company’s ability to manage costs and generate sustainable earnings. Similarly, lenders scrutinize these figures to evaluate creditworthiness. A lumpy or inconsistent recording of rent expense could mislead these parties, potentially leading to misguided investments or loan terms. Thus, periodic recognition is not just an accounting formality but a cornerstone of financial transparency.

However, this method is not without challenges. Companies must maintain rigorous records to ensure accurate allocation of prepaid rent. Errors in calculation or timing can lead to misstated financial results, triggering audits or regulatory scrutiny. For instance, a miscalculation that overstates rent expense in one period could understate it in another, skewing profitability metrics. To mitigate this, businesses often use accounting software or consult professionals to ensure compliance with GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards).

In conclusion, the income statement’s treatment of rent expense as a periodic cost is a strategic accounting practice that balances accuracy with practicality. It supports the matching principle, aids stakeholder analysis, and fosters financial integrity. While it demands meticulous record-keeping, the benefits far outweigh the effort, making it an indispensable tool in modern financial reporting.

Is Alligator Alley Rent Per Person or Total? A Clear Breakdown

You may want to see also

Explore related products

$13.37 $14.99

![]()

Amortization Process: Prepaid rent is amortized to expense over the rental period systematically

Prepaid rent is an asset account, not an expense, until the rental period it covers begins. This distinction is crucial because it reflects the timing of when the expense is recognized in financial statements. When a business pays rent in advance, it records the payment as a prepaid expense, a current asset on the balance sheet. However, as the rental period progresses, the asset is systematically reduced, and the corresponding expense is recognized on the income statement. This process is known as amortization, and it ensures that expenses align with the period in which they are incurred, adhering to the matching principle in accounting.

The amortization process for prepaid rent is straightforward but requires consistency and accuracy. For example, if a company pays $12,000 for a year’s rent in January, it would initially record this as a prepaid rent asset. Each month, $1,000 ($12,000 ÷ 12 months) is amortized, reducing the prepaid rent asset and increasing the rent expense. This systematic allocation ensures that the financial statements reflect the actual use of the rented space over time. Failure to amortize prepaid rent properly can distort financial results, overstating assets and understating expenses in the early periods of the rental agreement.

One practical tip for managing prepaid rent amortization is to use accounting software that automates the process. Most ERP systems allow businesses to set up recurring journal entries, ensuring that the amortization occurs consistently each period. For smaller businesses or those without advanced software, a simple spreadsheet can be used to track prepaid rent and manually record the monthly amortization entries. Regardless of the method, maintaining a clear audit trail is essential for compliance and financial transparency.

A comparative analysis highlights the importance of amortization in different industries. For instance, retail businesses often prepay rent for prime locations to secure long-term leases. Without proper amortization, their financial statements might show inflated profits in the initial months, misleading investors and stakeholders. In contrast, startups with limited cash flow may prepay rent to negotiate discounts, making accurate amortization critical to reflect their true financial health. This underscores the universal relevance of the amortization process across diverse business contexts.

In conclusion, the amortization of prepaid rent is a fundamental accounting practice that bridges the gap between asset recognition and expense allocation. By systematically expensing prepaid rent over the rental period, businesses ensure compliance with accounting principles and provide a more accurate financial picture. Whether through automated systems or manual tracking, the key lies in consistency and attention to detail. Mastering this process not only enhances financial reporting but also supports informed decision-making and strategic planning.

Understanding Market Rent-Tied Lease Structures for Optimal Property Agreements

You may want to see also

Frequently asked questions

Prepaid rent expense is an asset account.

It is classified as an asset because it represents a payment made in advance for future rent, providing a future benefit to the business.

Regular rent expense is recorded when rent is due or paid for the current period, while prepaid rent expense is recorded when rent is paid in advance for future periods.

Prepaid rent expense is reported under the current assets section of the balance sheet.

Prepaid rent expense is a temporary account, as it is adjusted over time to reflect the portion of rent used in each accounting period.