Unearned rent revenue is a type of liability account that represents rent payments received by a landlord or property owner in advance, before the rental period has actually been completed. This occurs when tenants pay rent upfront for a future period, such as a month or several months, creating an obligation for the landlord to provide the rental space or services in the future. As a liability, unearned rent revenue reflects the landlord's responsibility to fulfill the rental agreement, and it is gradually recognized as earned revenue over the rental period through periodic adjustments, typically in accordance with the matching principle of accounting.

| Characteristics | Values |

|---|---|

| Account Type | Liability Account |

| Classification | Current Liability |

| Nature | Unearned Revenue (Prepaid Income) |

| Recognition | Recognized when payment is received but service (rent) is not yet provided |

| Balancing Side | Credit side of the ledger |

| Financial Statement | Reported on the Balance Sheet under Current Liabilities |

| Matching Principle | Follows the matching principle by deferring revenue recognition |

| Time Frame | Short-term (typically within one year) |

| Example | Tenant pays $1,200 in advance for the next month's rent |

| Adjustment | Adjusted monthly as the rental period progresses |

| Reversal | Reversed by recognizing revenue in the income statement over time |

Explore related products

What You'll Learn

![]()

Unearned Rent Revenue Definition

Unearned rent revenue is a liability account that reflects payments received in advance for rental services not yet provided. This concept is rooted in the accrual accounting method, where revenue is recognized when earned, not when cash is received. For instance, if a tenant pays $1,200 in January for rent covering February, the landlord records $1,200 as unearned rent revenue. As February progresses, the landlord gradually recognizes this amount as rental income, reducing the liability balance. This ensures financial statements accurately represent the period’s economic activity, aligning with accounting principles like GAAP and IFRS.

Consider a commercial property owner who receives a $24,000 annual payment from a tenant in January. Instead of recording the entire amount as revenue immediately, the owner books $24,000 as unearned rent revenue. Each month, $2,000 is transferred from the liability account to rental income, reflecting the service provided. This method prevents revenue overstatement in the initial period and ensures consistency across financial reporting. For small businesses, this practice is critical for tax planning and cash flow management, as it avoids premature tax liabilities on unearned income.

From a comparative perspective, unearned rent revenue contrasts with prepaid expenses, another accrual accounting concept. While unearned rent revenue is a liability (money owed to provide future services), prepaid expenses are assets (payments made for future benefits). For example, a tenant’s prepaid rent is an asset on their books but a liability on the landlord’s. This duality highlights the importance of proper account classification to maintain balance sheet accuracy. Misclassification could distort financial ratios, such as current liabilities, misleading stakeholders about a company’s short-term obligations.

To implement unearned rent revenue correctly, follow these steps: first, record the advance payment as a credit to the unearned rent revenue account and a debit to cash. Second, create a schedule to allocate the liability over the rental period. For example, a $6,000 six-month prepayment would be recognized at $1,000 per month. Third, adjust journal entries monthly to transfer the earned portion to rental income. Caution: avoid manual errors by using accounting software with automated accrual features. Regularly reconcile the unearned rent account to ensure it matches lease agreements and payment schedules.

In practice, unearned rent revenue serves as a safeguard against revenue manipulation. For instance, a landlord cannot inflate quarterly earnings by recording a full year’s rent upfront. This transparency builds trust with investors and lenders, who rely on accurate financial statements. Additionally, it aids in cash flow analysis by distinguishing between cash received and services delivered. For landlords managing multiple properties, tracking unearned rent ensures each tenant’s payments are applied correctly, reducing disputes and improving tenant relations. Mastery of this concept is essential for anyone handling rental property accounting.

Renting Wheelchairs in North Austin: A Simple Guide

You may want to see also

Explore related products

![]()

Accounting Treatment for Unearned Rent

Unearned rent revenue is classified as a liability account in accounting, reflecting amounts received in advance for services not yet rendered. This treatment aligns with the accrual accounting principle, which recognizes revenues and expenses when they are earned or incurred, not when cash exchanges hands. For landlords or property managers, unearned rent represents a future obligation to provide rental services, making it a critical component of financial reporting and management.

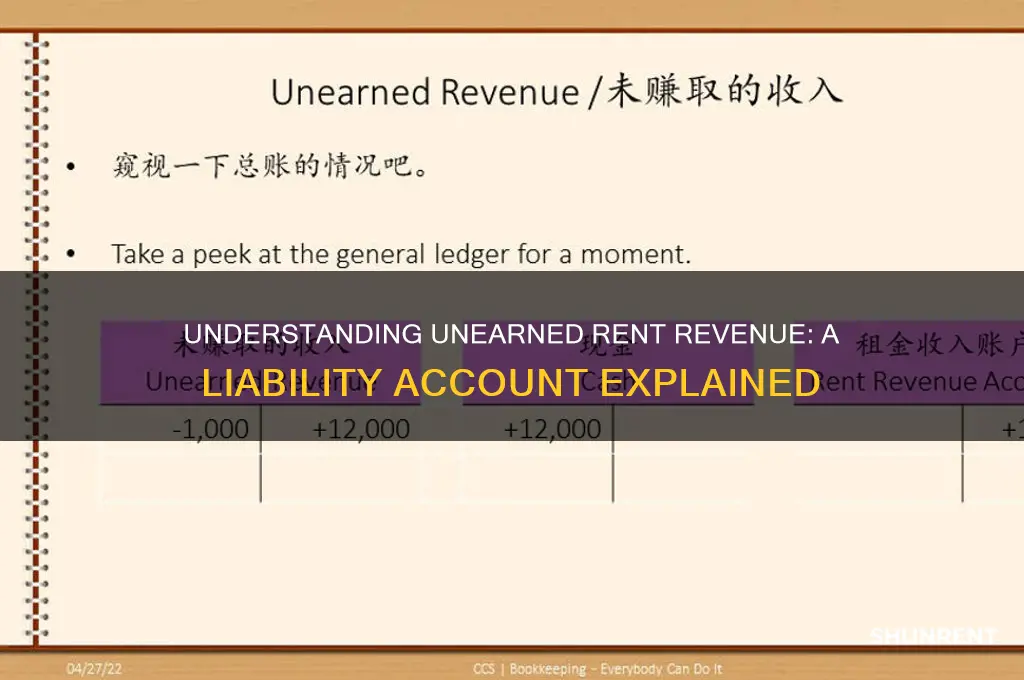

Consider a scenario where a tenant pays $12,000 upfront for a year’s rent. At the time of receipt, the landlord does not recognize this as revenue. Instead, the full amount is recorded as a liability under unearned rent revenue. As each month passes, the landlord systematically transfers a portion (e.g., $1,000 monthly) from the liability account to rental income, reflecting the earned revenue for services provided. This method ensures that financial statements accurately represent the economic reality of the transaction over time.

The accounting treatment involves two key journal entries. First, when the advance payment is received, the entry debits cash (asset) and credits unearned rent revenue (liability). For instance:

Debit: Cash – $12,000

Credit: Unearned Rent Revenue – $12,000

Second, at the end of each rental period, an adjusting entry is made to recognize earned revenue. For example, monthly:

Debit: Unearned Rent Revenue – $1,000

Credit: Rental Income – $1,000

This process maintains the balance sheet and income statement in accordance with the matching principle, pairing revenues with their corresponding expenses.

A critical caution lies in misclassifying unearned rent as revenue prematurely, which can distort financial statements and mislead stakeholders. For instance, if the entire $12,000 were recorded as revenue upfront, it would overstate current income and understate future liabilities. Small businesses, in particular, must adhere to this treatment to avoid compliance issues with accounting standards like GAAP or IFRS. Regular reconciliation of the unearned rent account is also essential to track obligations accurately.

In conclusion, the accounting treatment for unearned rent revenue is straightforward yet vital for financial accuracy. By classifying it as a liability and systematically recognizing revenue as services are provided, businesses ensure transparency and compliance. This approach not only aligns with accounting principles but also provides a clear picture of financial health, enabling better decision-making for landlords and investors alike.

Understanding Rent-to-Own Homes in Oklahoma: A Comprehensive Guide

You may want to see also

Explore related products

$21.99 $34.99

![]()

Liability vs. Revenue Classification

Unearned rent revenue sits at the crossroads of liability and revenue classification, a nuanced distinction with significant implications for financial reporting. At first glance, it might seem counterintuitive to label a payment received as anything but revenue. However, the timing of the transaction and the obligation it creates are critical factors in determining its proper classification. When a landlord receives rent in advance, the payment represents a promise to deliver future services—the use of the property. Until those services are rendered, the landlord has a liability, not revenue. This is because the business has an obligation to fulfill, and until that obligation is met, the funds cannot be considered earned.

To illustrate, consider a tenant who pays $12,000 for a year’s rent upfront in January. While the landlord receives the cash immediately, only $1,000 per month can be recognized as revenue as each month passes. The remaining $11,000 is classified as unearned rent revenue, a liability account, because the landlord owes the tenant 11 months of occupancy. This classification ensures that revenue is recognized in the period it is earned, aligning with the matching principle of accounting. Misclassifying unearned rent as revenue would overstate income and distort financial statements, misleading stakeholders about the company’s financial health.

The distinction between liability and revenue is not merely semantic; it has practical consequences for businesses. For instance, a small property management firm might face cash flow challenges if it fails to differentiate between earned and unearned revenue. By properly classifying unearned rent as a liability, the firm can accurately track its obligations and plan for future expenses. Additionally, this classification aids in tax planning, as unearned revenue is typically not taxable until it is recognized as income. For example, if a landlord receives $24,000 in unearned rent, only the portion recognized as revenue in the current tax year would be subject to taxation.

From a persuasive standpoint, proper classification of unearned rent revenue is essential for maintaining transparency and trust with investors and creditors. Financial statements that accurately reflect liabilities and revenues provide a clearer picture of a company’s financial position. For instance, a real estate investment trust (REIT) with significant unearned rent liabilities might appear less profitable in the short term but more stable in the long term, as it has secured future cash flows. This transparency can enhance credibility and attract long-term investors who value consistency and reliability.

In conclusion, the classification of unearned rent revenue as a liability rather than revenue hinges on the timing of service delivery and the obligation it creates. This distinction is not just an accounting technicality but a critical component of accurate financial reporting. By understanding and applying this principle, businesses can ensure compliance with accounting standards, improve financial planning, and build trust with stakeholders. Whether you’re a landlord, property manager, or investor, recognizing the difference between liability and revenue in this context is key to making informed financial decisions.

Rent in Collections: Consequences and Steps to Resolve the Issue

You may want to see also

Explore related products

$13.37 $14.99

![]()

Journal Entry for Unearned Rent

Unearned rent revenue is a liability account, representing advance payments received for rental services not yet rendered. This classification is crucial for accurate financial reporting, ensuring that revenue recognition aligns with the matching principle. When a landlord collects rent upfront, it’s not immediately considered income because the obligation to provide the rental period still exists. Thus, the journal entry for unearned rent serves as a bridge between the receipt of cash and the fulfillment of the rental agreement.

To record unearned rent, the journal entry involves debiting Cash (an asset account) and crediting Unearned Rent Revenue (a liability account). For example, if a tenant pays $1,200 for six months of rent in advance, the entry would be:

Debit: Cash | $1,200

Credit: Unearned Rent Revenue | $1,200

This entry reflects the increase in cash and the corresponding liability, acknowledging the obligation to provide future rental services.

As each rental period is completed, the unearned rent is gradually recognized as revenue. The adjusting entry involves debiting Unearned Rent Revenue and crediting Rent Revenue (an income account). For instance, if one month of the $1,200 advance has been fulfilled, the entry would be:

Debit: Unearned Rent Revenue | $200

Credit: Rent Revenue | $200

This reduces the liability and recognizes the earned income, aligning revenue with the period in which the service is provided.

A common mistake is treating unearned rent as immediate revenue, which distorts financial statements by overstating income. Proper journal entries ensure compliance with accounting standards like GAAP or IFRS, maintaining transparency and accuracy. For landlords or property managers, tracking these entries monthly or quarterly is essential, especially when managing multiple tenants with varying lease terms.

In summary, the journal entry for unearned rent is a two-step process: recording the advance payment as a liability and then recognizing revenue as the rental period progresses. This method not only adheres to accounting principles but also provides a clear financial picture of obligations and earnings. By mastering this entry, businesses can avoid misstatements and better manage cash flow tied to rental agreements.

Struggling to Pay Rent? Here’s How to Navigate the Crisis

You may want to see also

Explore related products

![]()

Recognition of Earned Rent Revenue

Unearned rent revenue is a liability account, representing advance payments received for services not yet rendered. This contrasts with earned rent revenue, which is recognized when the rental period has elapsed and the landlord has fulfilled their obligation. The recognition of earned rent revenue is a critical aspect of financial reporting, ensuring accuracy and compliance with accounting principles.

Example and Analysis:

Imagine a tenant pays $12,000 upfront for a year's rent. Initially, the landlord records this as unearned rent revenue. As each month passes, the landlord recognizes $1,000 as earned rent revenue, systematically reducing the unearned rent liability. This method, known as the straight-line approach, aligns revenue recognition with the period in which the service is provided. For instance, under the accrual accounting method, if a tenant pays rent on January 1 for the entire year, the landlord would recognize 1/12 of the total rent as earned revenue each month.

Steps for Proper Recognition:

- Identify the Rental Period: Determine the duration for which rent is being paid in advance.

- Calculate Monthly Revenue: Divide the total unearned rent by the number of months covered.

- Record Monthly Entries: At the end of each month, debit unearned rent revenue and credit earned rent revenue for the calculated amount.

- Monitor Liability Balance: Ensure the unearned rent account decreases monthly, reflecting the shift to earned revenue.

Cautions and Considerations:

Avoid recognizing the entire advance payment as revenue immediately, as this violates the matching principle. For example, if a tenant prepays $6,000 for six months, recognizing $1,000 monthly ensures revenue aligns with the period benefited. Additionally, landlords must adjust for lease incentives or variable payments, which may require prorated recognition. For instance, if a tenant receives one month free in a 12-month lease, the total rent should be recognized evenly over 11 months.

Practical Tips:

- Use Accounting Software: Automate revenue recognition to minimize errors and ensure consistency.

- Review Lease Agreements: Clarify payment terms and conditions to accurately determine recognition periods.

- Reconcile Regularly: Monthly reconciliation of unearned and earned rent accounts helps maintain financial integrity.

By meticulously recognizing earned rent revenue, landlords uphold transparency, comply with accounting standards, and provide a clear financial picture of their operations. This practice not only ensures accurate reporting but also builds trust with stakeholders.

Average Rent in Columbia, Maryland: What to Expect in 2023

You may want to see also

Frequently asked questions

Unearned rent revenue is a liability account. It represents rent payments received in advance that have not yet been earned by the landlord or property owner.

Unearned rent revenue is classified as a liability because it represents an obligation to provide future services (renting out the property) for which payment has already been received.

Unearned rent revenue is recorded as a credit to the unearned rent revenue account (liability) and a debit to cash or the appropriate revenue account when the payment is received. As the rent is earned over time, the liability is reduced, and revenue is recognized.