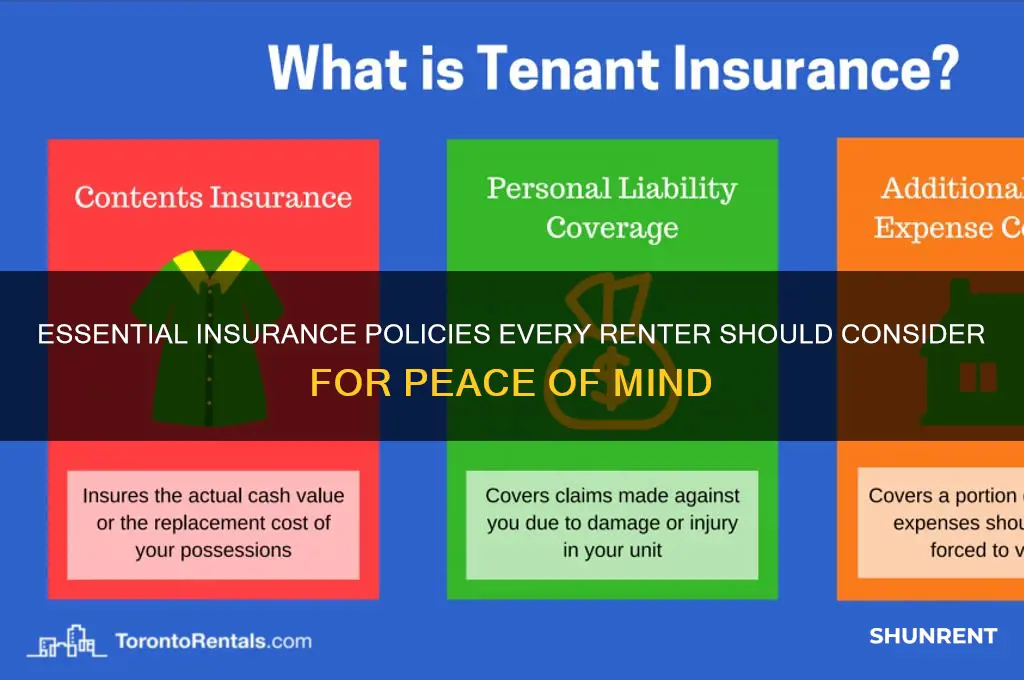

When renting a property, it’s essential for both landlords and tenants to understand the importance of having the right insurance coverage to protect their interests. Landlords should consider landlord insurance, which typically covers property damage, liability claims, and loss of rental income, while renters should invest in renters insurance to safeguard their personal belongings, provide liability coverage, and offer additional living expenses if the rental becomes uninhabitable. Clear communication between both parties about insurance requirements and responsibilities can prevent misunderstandings and ensure adequate protection for all involved.

| Characteristics | Values |

|---|---|

| Type of Insurance | Renter's Insurance |

| Coverage for Personal Property | Protects belongings (furniture, electronics, clothing) from theft, fire, or damage |

| Liability Coverage | Covers legal expenses if someone is injured in the rental unit |

| Additional Living Expenses (ALE) | Pays for temporary housing if the rental becomes uninhabitable due to a covered event |

| Cost | Typically $15–$30 per month (varies by location, coverage, and deductible) |

| Policy Limits | Usually $10,000–$100,000 for personal property; liability limits often $100,000–$500,000 |

| Deductible | Typically $500–$2,000 (higher deductibles lower premiums) |

| Coverage for High-Value Items | Requires additional riders for expensive items like jewelry or art |

| Natural Disaster Coverage | Covers damage from fire, wind, or vandalism but excludes floods (separate flood insurance needed) |

| Roommate Coverage | Policies may or may not cover roommates; clarify with insurer |

| Landlord Requirements | Some landlords require renters insurance as part of the lease |

| Credit Score Impact | Filing a claim may affect premiums but not credit score |

| Bundling Discounts | Discounts available when bundling with auto or other insurance policies |

| Policy Duration | Typically 6–12 months, renewable annually |

| Exclusions | Damage from floods, earthquakes, or intentional acts not covered |

| Portability | Coverage moves with the renter, not tied to a specific rental unit |

Explore related products

What You'll Learn

- Liability coverage for accidents or damages caused by the renter to others

- Personal property insurance to protect the renter’s belongings from theft or damage

- Renters insurance for additional living expenses if the property becomes uninhabitable

- Landlord’s insurance to cover the property structure and potential liability claims

- Umbrella insurance for extra liability protection beyond standard policy limits

![]()

Liability coverage for accidents or damages caused by the renter to others

Renters insurance often focuses on protecting personal belongings, but liability coverage is equally critical. This component shields your renter from financial ruin if they accidentally cause harm to others or damage someone else’s property. For instance, if a guest slips on a spilled drink in their apartment and sues for medical bills, or if their pet damages a neighbor’s expensive furniture, liability coverage steps in to cover the costs. Without it, your renter could face lawsuits, wage garnishments, or even bankruptcy.

Consider this scenario: a renter’s faulty space heater starts a fire that spreads to adjacent units, causing $50,000 in damages. Liability coverage would pay for repairs and legal fees, up to the policy limit (typically $100,000 to $500,000). Most policies also include "no-fault medical coverage," which pays for minor injuries (e.g., a guest’s broken arm) without requiring a lawsuit, often up to $1,000–$5,000. This not only protects your renter but also fosters goodwill with neighbors and guests.

When advising your renter, emphasize that liability coverage extends beyond their home. If their dog bites someone at the park, or if they accidentally knock over a priceless vase at a friend’s house, this coverage follows them. It’s a portable safety net, typically costing just $10–$20 per month for $300,000 in coverage. Encourage them to assess their risk factors—do they own pets, host frequently, or have valuable visitors? Higher limits may be warranted.

A common misconception is that landlords’ insurance will cover renter-caused damages. In reality, landlords’ policies rarely extend to tenants’ liability, leaving your renter exposed. To bridge this gap, suggest they pair renters insurance with an umbrella policy if their assets exceed their liability limit. For example, a renter with $500,000 in liability coverage and $1 million in assets should consider an umbrella policy to cover the difference.

Finally, remind your renter that liability claims can arise from unexpected sources. A defamatory social media post, a child’s playground accident, or even a guest’s food poisoning after a dinner party could trigger a lawsuit. Liability coverage isn’t just for physical damages—it often includes personal injury claims like libel or slander. By framing this coverage as essential, not optional, you’ll help your renter avoid catastrophic financial consequences from everyday mishaps.

Where Did Rent-a-Girlfriend Anime End? Chapter Breakdown

You may want to see also

Explore related products

![]()

Personal property insurance to protect the renter’s belongings from theft or damage

Renters often overlook the value of their personal belongings until it’s too late. A laptop, furniture, clothing, and electronics can add up to tens of thousands of dollars, yet many assume their landlord’s insurance will cover losses. This is a critical mistake. Landlord policies typically protect only the structure, not the tenant’s possessions. Personal property insurance steps in to fill this gap, offering coverage for theft, fire, water damage, and other perils. Without it, replacing stolen or damaged items falls entirely on the renter’s shoulders.

Consider this scenario: a fire breaks out in the apartment below yours, and smoke and water damage ruin your furniture and electronics. Without personal property insurance, you’re left to fund replacements out of pocket. Policies typically cover the actual cash value (ACV) or replacement cost of items. ACV accounts for depreciation, while replacement cost pays to buy new items at current prices. For example, a 5-year-old laptop might receive $200 under ACV but $1,000 under replacement cost coverage. Choosing the right option depends on your budget and the value of your belongings.

To determine how much coverage you need, conduct a home inventory. List all possessions, including electronics, clothing, furniture, and jewelry, along with their estimated value. Apps like Sortly or simple spreadsheets can streamline this process. Most insurers recommend coverage limits between $10,000 and $100,000, depending on your assets. For high-value items like engagement rings or art, consider scheduling them separately to ensure full coverage, as standard policies often cap payouts for specific categories like jewelry.

While personal property insurance is essential, it’s not without limitations. Policies typically exclude damage from floods, earthquakes, and intentional acts. Renters in flood-prone areas should purchase separate flood insurance through the National Flood Insurance Program. Additionally, some policies require proof of loss, such as receipts or photos, to process claims. Keep detailed records and store them digitally for easy access. Finally, compare deductibles—the amount you pay before insurance kicks in—to find a balance between affordability and coverage.

Persuading renters to prioritize personal property insurance requires highlighting its affordability and peace of mind. Premiums average $15–$30 per month, a small price for protecting thousands of dollars’ worth of belongings. Imagine losing everything in a burglary or fire—this coverage ensures you can rebuild without financial strain. For landlords, encouraging tenants to purchase this insurance reduces disputes over liability and demonstrates a commitment to their well-being. It’s not just a policy; it’s a safeguard for the life you’ve built.

Solano County Rent-to-Income Ratio: Understanding Affordability in the Housing Market

You may want to see also

Explore related products

![]()

Renters insurance for additional living expenses if the property becomes uninhabitable

Renters insurance often includes a critical but overlooked component: coverage for additional living expenses (ALE) if your rental property becomes uninhabitable due to a covered peril, such as fire, water damage, or natural disaster. This provision ensures you’re not left stranded financially while your home is being repaired or replaced. For instance, if a kitchen fire forces you to relocate temporarily, ALE coverage can pay for hotel stays, restaurant meals, and even laundry services, typically up to 20–30% of your policy’s personal property limit. Without this, the sudden costs of displacement could quickly overwhelm your budget.

Analyzing the specifics, ALE coverage typically kicks in when the damage is severe enough to make the property unsafe or unlivable. It’s not just for major disasters; even a burst pipe causing extensive water damage could qualify. However, there are limits. Most policies cap ALE coverage at a specific time frame, often 12–24 months, or until the property is restored, whichever comes first. Additionally, insurers may require documentation, such as receipts for expenses, to reimburse you fully. Understanding these parameters ensures you’re not caught off guard when filing a claim.

Persuasively, ALE coverage is a non-negotiable for renters, especially in areas prone to natural disasters or older buildings with higher maintenance risks. Consider this: the average hotel stay costs $150–$200 per night, and eating out triples your daily food expenses. Without ALE, a month-long displacement could cost $6,000–$9,000 out of pocket. For a policy that adds just $10–$20 monthly to your premium, it’s a small price for significant peace of mind. Landlords’ insurance rarely covers tenant displacement, so relying on them is a risky gamble.

Comparatively, ALE coverage in renters insurance is more comprehensive than what you might assume. Unlike basic liability or personal property coverage, it addresses the immediate, practical challenges of displacement. For example, while your landlord’s insurance might cover structural repairs, it won’t pay for your temporary housing or increased living costs. Renters insurance with ALE bridges this gap, ensuring you maintain your standard of living during a crisis. It’s a proactive measure that turns a potential financial disaster into a manageable situation.

Practically, to maximize ALE benefits, keep detailed records of all displacement-related expenses. Save receipts for hotels, meals, transportation, and even pet boarding if necessary. Notify your insurer promptly after the incident to understand their specific requirements and timelines. Additionally, review your policy annually to ensure your coverage limits align with your current living costs. For renters in high-risk areas, consider increasing your ALE limit beyond the standard 20–30% of personal property coverage. This small step could make a world of difference when you need it most.

Basement Rentals: Do You Need a Permit?

You may want to see also

Explore related products

![]()

Landlord’s insurance to cover the property structure and potential liability claims

Landlords insurance is a critical safeguard for property owners, designed to protect both the physical structure of the rental property and the landlord from potential liability claims. Unlike renters insurance, which tenants should carry to protect their personal belongings and liability, landlords insurance focuses on the building itself and the risks associated with owning and renting out real estate. This dual protection ensures that landlords are not left financially vulnerable in the event of damage to the property or lawsuits arising from accidents on the premises.

One of the primary components of landlords insurance is dwelling coverage, which protects the physical structure of the rental property. This includes the walls, roof, floors, and built-in appliances. For example, if a fire damages the property, dwelling coverage would pay for repairs or rebuilding costs, up to the policy limit. Landlords should ensure their policy reflects the property’s replacement cost, not just its market value, to avoid being underinsured. Additionally, policies often include coverage for other structures, such as detached garages or fences, which are typically covered at a percentage of the dwelling limit.

Liability coverage is another essential aspect of landlords insurance, shielding property owners from financial loss if someone is injured on the rental property and sues for damages. For instance, if a tenant’s guest slips on a wet floor and sustains injuries, the landlord could be held responsible. Liability coverage would help pay for medical bills, legal fees, and any settlements or judgments up to the policy limit. Landlords should consider higher liability limits, especially if the property has features that increase risk, such as a swimming pool or uneven landscaping.

Beyond these core protections, landlords insurance often includes loss of rental income coverage. This provision compensates landlords for lost rental income if the property becomes uninhabitable due to a covered peril, such as a fire or storm. For example, if repairs take three months, the policy would reimburse the landlord for the rent they would have collected during that period. This feature is particularly valuable for landlords who rely on rental income to cover mortgage payments or other expenses.

When selecting a landlords insurance policy, it’s crucial to review exclusions and additional coverage options. For instance, standard policies typically exclude damage from floods or earthquakes, requiring separate policies for these perils. Landlords should also consider adding umbrella insurance for extra liability protection beyond the limits of their primary policy. Practical tips include bundling landlords insurance with other policies, such as auto insurance, to save on premiums, and regularly updating the policy to reflect renovations or changes in property value. By carefully tailoring their coverage, landlords can ensure comprehensive protection for their investment and peace of mind.

Consequences of Not Deducting TDS on Rent: What You Need to Know

You may want to see also

Explore related products

![]()

Umbrella insurance for extra liability protection beyond standard policy limits

Standard renter's insurance policies typically cap liability coverage at $100,000 to $300,000. While sufficient for minor incidents, this limit can leave you vulnerable if your renter causes significant property damage or bodily injury. For instance, if your renter’s negligence results in a fire that displaces neighbors or causes severe injuries, the costs could easily surpass your policy’s liability limit. This is where umbrella insurance steps in, offering an additional $1 million or more in coverage to bridge the gap.

Consider umbrella insurance as a safety net for high-risk scenarios. It activates once your primary renter’s insurance liability limit is exhausted, covering legal fees, medical bills, and settlements. For example, if your renter is sued for $1.2 million after a guest slips and suffers a debilitating injury, your renter’s policy might cover $300,000, but the remaining $900,000 could fall on you without umbrella coverage. By adding this layer, you protect your assets—savings, investments, and future earnings—from being seized in a lawsuit.

Requiring your renter to carry umbrella insurance isn’t just about protecting them; it’s about safeguarding your interests as a landlord. If your renter’s actions lead to a lawsuit, plaintiffs may target you as the property owner, especially if the renter lacks sufficient assets. By mandating umbrella coverage, you ensure there’s adequate funds to settle claims without exposing yourself to financial risk. Include this requirement in your lease agreement, specifying the minimum coverage amount (e.g., $1 million) and verifying proof of policy annually.

Umbrella insurance is surprisingly affordable, typically costing $150 to $300 annually for $1 million in coverage. Encourage your renter to shop around, as many insurers offer discounts when bundling umbrella policies with auto or renter’s insurance. Remind them that umbrella coverage is portable, meaning it follows them beyond your property, providing protection for accidents they cause anywhere, such as a car collision or pet-related injury. This added value can make it an easier sell when discussing lease terms.

Finally, treat umbrella insurance as a non-negotiable for high-risk renters, such as those with pets, frequent guests, or a history of claims. Even for low-risk renters, it’s a prudent precaution. Share real-life examples of lawsuits exceeding standard policy limits to illustrate the stakes. By prioritizing this extra layer of protection, you foster a safer rental environment and minimize the likelihood of financial catastrophe for both parties.

Mastering Rent-to-Own: A Step-by-Step Guide to Crafting Your Contract

You may want to see also

Frequently asked questions

As a renter, you should have renter’s insurance, which covers your personal belongings, liability, and additional living expenses if your rental becomes uninhabitable due to a covered event.

No, your landlord’s insurance typically covers the building structure, not your personal property. Renter’s insurance is necessary to protect your belongings.

Renter’s insurance covers personal property (e.g., furniture, electronics), liability (if someone is injured in your rental), and additional living expenses (e.g., hotel costs) if you’re temporarily displaced.

Renter’s insurance is not required by law in most places, but some landlords may require it as part of your lease agreement.

Renter’s insurance is affordable, typically costing $15–$30 per month. Choose a policy based on coverage limits for personal property and liability, and consider additional endorsements for high-value items if needed.

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)