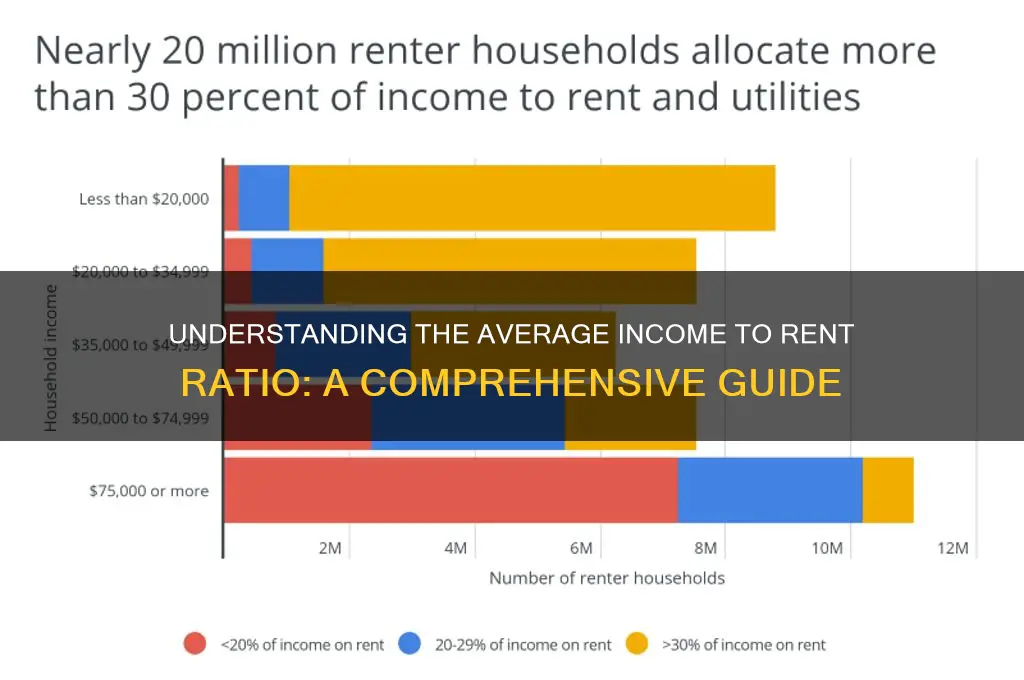

The average income-to-rent ratio is a critical metric used to assess housing affordability, representing the proportion of a household’s income allocated to rent. Typically expressed as a percentage, it is calculated by dividing monthly rent by monthly income, with a widely accepted threshold of 30% or less indicating affordability. For example, if a household earns $5,000 monthly and pays $1,500 in rent, their ratio is 30%, considered manageable. However, in many high-cost urban areas, this ratio often exceeds 50%, straining budgets and limiting financial flexibility. Understanding this ratio helps policymakers, renters, and economists evaluate the balance between earnings and housing costs, highlighting disparities and informing solutions to improve affordability.

Explore related products

What You'll Learn

- Regional Variations: Income-to-rent ratios differ significantly across cities, states, and countries

- Affordability Standards: Commonly, 30% of income is considered the maximum for rent affordability

- Minimum Wage Impact: How minimum wage levels affect the ability to afford average rent

- Housing Market Trends: Rising rents often outpace income growth, skewing the ratio

- Government Policies: Subsidies, rent control, and housing assistance influence income-to-rent dynamics

![]()

Regional Variations: Income-to-rent ratios differ significantly across cities, states, and countries

The income-to-rent ratio, a critical metric for assessing housing affordability, varies dramatically across regions, reflecting disparities in local economies, housing markets, and cost of living. For instance, in San Francisco, where the average rent for a one-bedroom apartment exceeds $3,500, residents often face a ratio of 30% or more of their income going toward rent. In contrast, cities like Indianapolis or Memphis report ratios closer to 15–20%, as median rents hover around $1,000. These differences highlight how regional factors, such as job markets, population density, and housing supply, shape affordability.

Analyzing these variations reveals a pattern: coastal cities and global hubs tend to have higher income-to-rent ratios due to soaring demand and limited housing stock. In New York City, for example, households earning the median income of $70,000 often spend 40–50% on rent, far exceeding the recommended 30% threshold. Meanwhile, in Midwestern or Southern cities, where housing is more abundant and wages align with local costs, residents enjoy greater financial flexibility. This disparity underscores the need for localized housing policies that account for regional economic conditions.

To navigate these regional differences, consider a comparative approach. For instance, in Berlin, Germany, rent control policies have kept the income-to-rent ratio around 20%, even in a major European capital. Conversely, in Sydney, Australia, where rents consume 35–40% of income, the government has introduced incentives for affordable housing development. These examples illustrate how policy interventions can mitigate regional disparities, offering a roadmap for cities struggling with affordability.

Practical tips for individuals include researching regional ratios before relocating and budgeting accordingly. For example, if moving to a high-ratio city like Los Angeles, where rents average $2,500, ensure your income supports a 30–40% allocation to housing. Alternatively, consider cities like Austin, Texas, where a tech boom has increased rents but still maintains a ratio of 25–30%. Pairing this research with tools like rent calculators or affordability indexes can provide a clearer financial picture.

Ultimately, understanding regional income-to-rent ratios empowers both policymakers and individuals to make informed decisions. For governments, it emphasizes the need for tailored solutions, such as increasing housing supply in high-demand areas or implementing rent stabilization measures. For renters, it serves as a reminder to balance lifestyle preferences with financial sustainability, ensuring housing costs don’t compromise other essential expenses. By acknowledging these variations, we can work toward more equitable housing outcomes across diverse regions.

Understanding the 30 Percent Rule for Rent: A Budgeting Guide

You may want to see also

Explore related products

![]()

Affordability Standards: Commonly, 30% of income is considered the maximum for rent affordability

The 30% rule, a cornerstone of financial planning, suggests that households should allocate no more than 30% of their gross income to housing costs, primarily rent. This guideline, established by the U.S. Department of Housing and Urban Development (HUD), aims to ensure that individuals and families maintain a balanced budget, covering essentials like food, transportation, and healthcare without strain. For instance, a household earning $5,000 monthly should ideally spend no more than $1,500 on rent. However, this standard often clashes with reality, especially in high-cost urban areas where rent can easily surpass this threshold.

Analyzing the feasibility of the 30% rule reveals its limitations in today’s housing market. In cities like San Francisco, New York, or Los Angeles, median rents frequently exceed $2,500 per month, while median incomes struggle to keep pace. For a family earning $60,000 annually, the 30% rule allows $1,500 monthly for rent, yet many face rents closer to $2,000 or more. This disparity forces households to either compromise on living standards, relocate to less desirable areas, or allocate a larger portion of their income to housing, often at the expense of savings or other necessities.

To navigate this challenge, individuals can adopt practical strategies. First, consider shared housing or roommate arrangements to split costs. Second, explore government assistance programs like Section 8 vouchers or local rent subsidies. Third, negotiate lease terms with landlords, such as longer-term contracts in exchange for reduced rent. Additionally, budgeting tools and apps can help track expenses and identify areas to cut back, freeing up funds for housing. For those in high-cost areas, relocating to more affordable neighborhoods or cities may be the most sustainable solution.

Despite its widespread use, the 30% rule is not one-size-fits-all. Factors like family size, debt obligations, and regional cost of living variations necessitate flexibility. A single professional with no debt may comfortably exceed the 30% threshold, while a family with student loans and childcare expenses may need to stay well below it. Tailoring this guideline to individual circumstances ensures a more realistic and sustainable approach to housing affordability.

In conclusion, while the 30% rule serves as a valuable benchmark, it requires adaptation to address the complexities of modern housing markets. By combining strategic planning, resourcefulness, and a willingness to adjust expectations, households can achieve a balance between housing costs and overall financial health. This approach not only mitigates the risk of financial strain but also fosters long-term stability and peace of mind.

Locate Rent-to-Own Serial Numbers with Splice: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Minimum Wage Impact: How minimum wage levels affect the ability to afford average rent

The average income-to-rent ratio in the U.S. hovers around 30%, meaning households should ideally spend no more than 30% of their pre-tax income on housing. However, for minimum wage workers, this benchmark is often unattainable. At the federal minimum wage of $7.25 per hour, a full-time worker earns approximately $1,257 monthly before taxes. In contrast, the national average rent for a one-bedroom apartment exceeds $1,200. This disparity forces many low-wage earners to allocate closer to 95% of their income to rent alone, leaving little for other essentials like food, healthcare, and transportation.

Consider the state-level variations in minimum wage and their impact on affordability. In states like California, where the minimum wage is $15.50 per hour, a full-time worker earns about $2,600 monthly. While still tight, this income allows for a more manageable rent burden, especially in areas with lower housing costs. Conversely, in states like Georgia, where the minimum wage remains at the federal level, workers face a starker reality. For instance, Atlanta’s average one-bedroom rent of $1,500 consumes nearly 120% of a minimum wage earner’s monthly income, making it mathematically impossible to afford housing without additional support or multiple jobs.

To bridge this gap, policymakers and advocates often propose raising minimum wages to a "living wage" level. A living wage is calculated based on the actual cost of living in a specific area, including housing, food, and other necessities. For example, MIT’s Living Wage Calculator estimates that a single adult in Los Angeles needs to earn at least $18.66 per hour to cover basic expenses, while in rural Mississippi, the figure drops to $13.22. Implementing such wages would significantly reduce the income-to-rent ratio for low-wage workers, making housing more accessible.

However, simply raising wages is not a silver bullet. Landlords and developers often respond to higher wages by increasing rents, a phenomenon known as "rent capture." For instance, in Seattle, where the minimum wage rose to $15 per hour, some studies found that rents in low-wage neighborhoods increased at a faster rate than in other areas. To counteract this, policies like rent control, inclusionary zoning, and increased investment in affordable housing must accompany wage increases. Without such measures, the benefits of higher wages risk being eroded by rising housing costs.

For individuals navigating this challenge, practical strategies can help mitigate the impact. First, consider shared housing arrangements, which can reduce rent burdens significantly. Second, explore government assistance programs like Section 8 vouchers or local rental subsidies. Third, advocate for policy changes at the local and state levels, such as higher minimum wages and stronger tenant protections. While systemic solutions are essential, proactive steps can provide immediate relief in the face of daunting income-to-rent ratios.

Rental Agreements: What to Know Beforehand

You may want to see also

Explore related products

![]()

Housing Market Trends: Rising rents often outpace income growth, skewing the ratio

The average income-to-rent ratio, a key metric for housing affordability, is traditionally considered healthy at 30%—meaning renters should spend no more than 30% of their monthly income on housing. However, recent trends reveal a disturbing shift: rents are rising faster than incomes, pushing this ratio far beyond sustainable levels. In cities like San Francisco, Los Angeles, and New York, renters now allocate closer to 50% or more of their earnings to housing, leaving little for other essentials like food, healthcare, and savings. This disparity isn’t confined to coastal metros; even in mid-sized cities like Phoenix and Nashville, rent growth has outstripped wage increases by double-digit percentages over the past five years.

To illustrate, consider a renter earning the median U.S. income of $55,000 annually. At the recommended 30% ratio, their monthly rent should cap at $1,375. Yet, in 2023, the average U.S. rent reached $1,702, requiring an income of $68,080 to meet the 30% threshold. This mismatch forces households to make untenable trade-offs, such as living in substandard conditions, moving farther from job centers, or accumulating debt. For low-income earners, the situation is dire: those making $30,000 annually would need to spend 68% of their income to afford the average rent, a figure that defies financial logic.

Several factors drive this trend. First, housing supply has failed to keep pace with demand, particularly in high-growth regions. Zoning restrictions, construction costs, and NIMBYism (Not In My Backyard) limit new development, while investors prioritize luxury units over affordable housing. Simultaneously, wage growth remains sluggish, with the average hourly earnings rising just 4.4% in 2023 compared to rent increases of 7-10% in many markets. Inflation compounds the issue, eroding purchasing power even as nominal incomes rise. The result? A widening affordability gap that disproportionately affects younger workers, families, and marginalized communities.

Policymakers and advocates propose solutions, but implementation remains uneven. Rent control, while popular, often backfires by reducing supply and incentivizing landlords to convert rentals into condos. Increasing the housing stock through streamlined permitting and density incentives shows promise, as seen in Minneapolis’s 2040 Plan, which eliminated single-family zoning. Another approach is expanding housing vouchers and tax credits, though these programs face chronic underfunding. Employers can also play a role by offering housing stipends or remote work options, reducing the need to live in high-cost areas.

For individuals navigating this landscape, practical strategies are essential. First, prioritize budgeting tools that account for higher rent burdens, such as cutting discretionary spending or seeking roommates. Second, explore lesser-known markets with better income-to-rent ratios; cities like Pittsburgh, Indianapolis, and Memphis offer rents below $1,200 with median incomes sufficient to meet the 30% threshold. Finally, advocate for systemic change by supporting policies that address both supply and demand, from affordable housing mandates to wage increases. Without collective action, the skewed income-to-rent ratio will continue to undermine financial stability for millions.

Are Rent Receipts Mandatory for Tenants in California? Know Your Rights

You may want to see also

Explore related products

![]()

Government Policies: Subsidies, rent control, and housing assistance influence income-to-rent dynamics

The average income-to-rent ratio in the U.S. hovers around 30%, meaning households ideally spend no more than 30% of their income on rent. However, government policies like subsidies, rent control, and housing assistance significantly alter this dynamic, creating both opportunities and challenges for renters and policymakers alike.

Subsidies, such as the Housing Choice Voucher Program (Section 8), directly reduce the income-to-rent ratio for eligible low-income households by covering a portion of their rent. For example, a family earning $30,000 annually might face a market rent of $1,200, pushing their ratio to 48%. With a subsidy covering 70% of the rent, their effective rent drops to $360, lowering the ratio to a manageable 14.4%. This not only improves affordability but also frees up income for other essentials like healthcare and education. However, the limited availability of vouchers—only one in four eligible households receive them—highlights the program’s constraints.

Rent control, while intended to stabilize housing costs, often produces unintended consequences. In cities like San Francisco, rent-controlled units can have income-to-rent ratios as low as 20% for long-term tenants. Yet, this policy can discourage new construction and reduce rental supply, driving up market rents for uncontrolled units. For instance, a 2019 study by the American Economic Review found that rent control in San Francisco led to a 15% reduction in available rental units, exacerbating affordability issues for new renters. Policymakers must balance tenant protection with incentives for developers to avoid such paradoxes.

Housing assistance programs, including Low-Income Housing Tax Credits (LIHTC) and public housing, target specific demographics to address affordability gaps. LIHTC properties, for instance, often cap rents at 30% of the area median income, ensuring that a family earning $40,000 in a high-cost area pays no more than $1,000 monthly. Public housing, though underfunded, provides deeply subsidized units with income-to-rent ratios as low as 10% for the poorest households. However, long waitlists—sometimes exceeding five years—limit their impact. Expanding these programs and streamlining access could significantly reduce housing insecurity nationwide.

To maximize the effectiveness of these policies, governments should adopt a multi-pronged approach. First, increase funding for subsidies and housing assistance to reach more eligible households. Second, pair rent control with pro-development policies, such as density bonuses or expedited permitting, to mitigate supply shortages. Finally, evaluate programs regularly to ensure they meet evolving needs, such as adjusting income limits to reflect local cost-of-living increases. By addressing both supply and demand, policymakers can create a more equitable income-to-rent landscape.

Renting a Washer: Aaron's Appliance Options

You may want to see also

Frequently asked questions

The average income to rent ratio is a measure of housing affordability, typically calculated by dividing annual household income by annual rent. A common benchmark is the 30% rule, where rent should not exceed 30% of gross income.

The income to rent ratio is calculated by dividing the annual household income by the annual rent. For example, if a household earns $60,000 per year and pays $18,000 in rent, the ratio is 3.33 ($60,000 / $18,000).

A healthy income to rent ratio is generally considered to be around 3 or higher, meaning rent should not exceed 33% of gross income. However, the widely accepted standard is that rent should not surpass 30% of income.

The income to rent ratio is important because it helps determine housing affordability and financial stability. A high ratio indicates that rent is manageable relative to income, while a low ratio suggests potential financial strain.

The average income to rent ratio varies significantly by location due to differences in cost of living, housing markets, and local incomes. Urban areas with high housing costs often have lower ratios, while rural areas tend to have higher ratios.