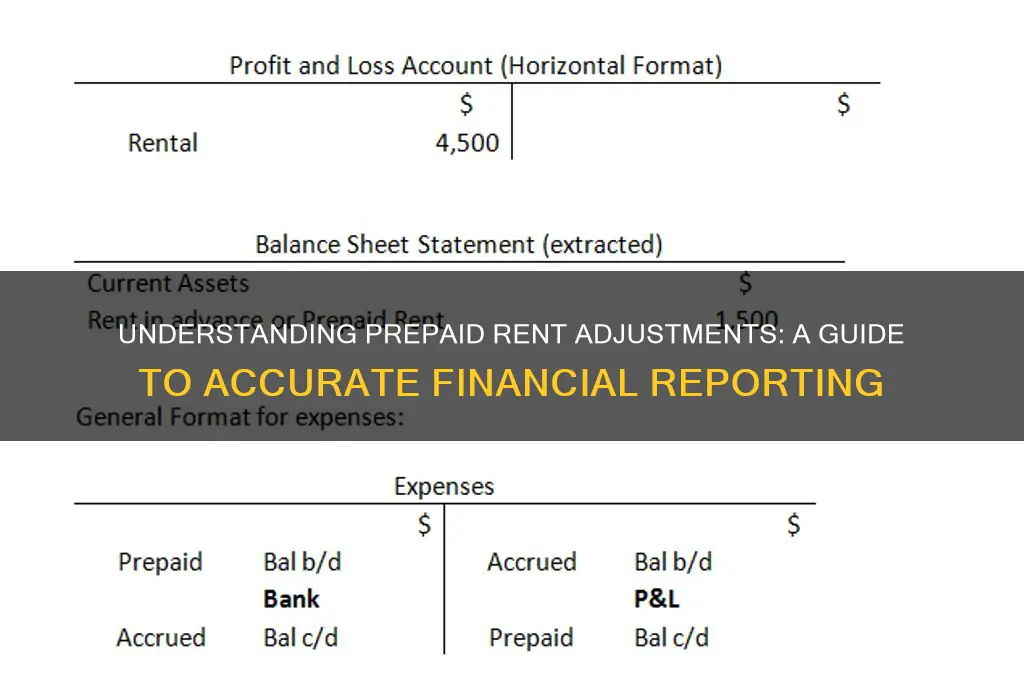

When an adjustment is made for prepaid rent, it reflects the portion of rent paid in advance that pertains to a future accounting period rather than the current one. This adjustment is necessary to ensure that expenses are recognized in the period in which they are incurred, adhering to the matching principle of accounting. Prepaid rent is initially recorded as an asset on the balance sheet, representing the value of rent paid but not yet utilized. At the end of the accounting period, the portion of prepaid rent that corresponds to the current period is recognized as an expense and deducted from the prepaid rent asset, accurately reflecting the financial obligations and resource usage of the business. This process is crucial for maintaining the integrity of financial statements and providing a clear picture of a company’s financial health.

| Characteristics | Values |

|---|---|

| Definition | Adjustment made to recognize the portion of prepaid rent that applies to the current accounting period. |

| Purpose | To match rent expense with the period in which the benefit is received. |

| Accounting Treatment | Prepaid rent is initially recorded as an asset (current asset). |

| Adjustment Entry | Debit Rent Expense, Credit Prepaid Rent (to allocate expense over time). |

| Timing | Adjustment is made at the end of the accounting period. |

| Financial Statement Impact | Reduces Prepaid Rent (asset) and increases Rent Expense on the income statement. |

| Example | If $12,000 is paid for 12 months of rent, $1,000 is expensed monthly. |

| Relevance | Ensures compliance with the accrual accounting principle and GAAP/IFRS. |

| Frequency | Typically adjusted monthly or at the end of each reporting period. |

| Documentation | Supported by lease agreements and payment receipts. |

Explore related products

What You'll Learn

![]()

Journal Entry for Prepaid Rent Adjustment

Prepaid rent adjustments are necessary when a business pays rent in advance for a period that extends beyond the current accounting cycle. This scenario requires a journal entry to accurately reflect the portion of rent expense applicable to the current period, ensuring financial statements remain truthful and reliable.

For instance, imagine a company pays $12,000 annually for rent in January, covering the entire year. In March, they need to adjust their books to recognize only the rent expense for the first three months ($3,000).

Recording the Adjustment: A Step-by-Step Guide

- Identify the Prepaid Amount: Determine the total prepaid rent amount and the period it covers. In our example, it's $12,000 for 12 months.

- Calculate Monthly Rent: Divide the total prepaid rent by the number of months it covers. Here, $12,000 / 12 = $1,000 per month.

- Determine the Adjustment Period: Identify the months for which an adjustment is needed. In March, we need to adjust for January, February, and March (3 months).

- Debit Rent Expense: Debit the Rent Expense account for the amount applicable to the adjustment period. In this case, debit Rent Expense for $3,000 (3 months x $1,000).

- Credit Prepaid Rent: Credit the Prepaid Rent account for the same amount, reducing the prepaid balance. Credit Prepaid Rent for $3,000.

Potential Pitfalls and Best Practices

A common mistake is forgetting to make prepaid rent adjustments altogether, leading to overstated assets and understated expenses. Regularly reviewing prepaid accounts and establishing a consistent adjustment schedule are crucial. Consider setting reminders or utilizing accounting software with automated features to ensure timely adjustments.

The Impact of Accurate Adjustments

Properly adjusting prepaid rent ensures financial statements accurately reflect the company's financial position. It provides a clearer picture of current liabilities and expenses, aiding in informed decision-making and maintaining compliance with accounting principles.

¿Está la propiedad aún disponible para alquilar en español?

You may want to see also

Explore related products

![]()

Impact on Financial Statements

Adjusting for prepaid rent directly impacts the accuracy of a company’s financial statements by aligning expenses with the period in which they are incurred. When rent is paid in advance, recording the full payment as an expense in the month of payment distorts the income statement, overstating expenses and understating net income. By making an adjustment, the prepaid portion is moved from the expense account to a prepaid asset account on the balance sheet. This ensures that only the portion of rent attributable to the current period is expensed, providing a clearer picture of financial performance.

Consider a scenario where a company pays $12,000 for six months of rent in January. Without adjustment, the income statement would reflect $12,000 in rent expense for January, despite only $2,000 ($12,000 / 6) being used in that month. Adjusting entries allocate $2,000 to rent expense and $10,000 to prepaid rent, a current asset. This adjustment not only corrects the income statement but also ensures the balance sheet accurately reflects the company’s resources, demonstrating the principle of matching expenses to the period in which they are consumed.

The impact of this adjustment extends beyond the income statement and balance sheet to influence key financial ratios. For instance, overstating expenses reduces net income, which in turn lowers profitability ratios like gross profit margin and net profit margin. Similarly, failing to recognize prepaid rent as an asset understates total assets, affecting liquidity ratios such as the current ratio. Accurate adjustments, therefore, are critical for stakeholders relying on these ratios to assess a company’s financial health and operational efficiency.

From a practical standpoint, accounting software often automates these adjustments through recurring journal entries. For example, QuickBooks allows users to set up a monthly journal entry debiting rent expense and crediting prepaid rent for the appropriate amount. However, manual oversight is essential to ensure the prepaid rent account is correctly amortized over the rental period. Small businesses, in particular, should review these entries quarterly to catch any discrepancies, such as changes in lease terms or early terminations, which could alter the adjustment amount.

In conclusion, adjusting for prepaid rent is not merely a compliance requirement but a strategic step in maintaining the integrity of financial statements. It ensures expenses are matched to the periods they benefit, enhances the accuracy of financial ratios, and provides stakeholders with a transparent view of a company’s financial position. By understanding and implementing these adjustments, businesses can avoid misleading representations of their financial performance and make more informed decisions.

Legal Steps for Evicting Renters in Minnesota: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Calculation of Rent Expense

Prepaid rent represents a unique challenge in financial accounting, as it requires allocating expenses across multiple periods to accurately reflect the timing of benefits received. When a business pays rent in advance, the entire payment is not immediately expensed; instead, it is recorded as an asset on the balance sheet. The calculation of rent expense, therefore, involves systematically transferring a portion of this prepaid asset to the income statement over the rental period. This process ensures that expenses align with the revenue they help generate, adhering to the matching principle—a cornerstone of accrual accounting.

To calculate rent expense, begin by identifying the total prepaid rent amount and the duration of the rental period. For example, if a company pays $12,000 for a year’s rent in advance, the monthly rent expense would be $1,000 ($12,000 ÷ 12 months). Each month, this amount is debited to rent expense and credited to the prepaid rent account, reducing the asset balance. This method, known as straight-line amortization, is straightforward and widely used due to its simplicity and consistency. However, it assumes uniform usage of the rented space, which may not always reflect reality.

In practice, the calculation can become more nuanced depending on lease terms or seasonal variations. For instance, if a retail business experiences higher sales during the holiday season, allocating a larger portion of rent expense to those months might better match costs with revenues. This approach, while more complex, provides a more accurate financial picture. Accountants must carefully review lease agreements and operational patterns to determine the most appropriate allocation method, balancing precision with practicality.

One critical caution is avoiding the temptation to overcomplicate the calculation unnecessarily. While accuracy is essential, excessive complexity can lead to errors or misinterpretation of financial statements. For small businesses or straightforward leases, the straight-line method often suffices. However, for larger entities or complex leases, consulting accounting standards such as ASC 842 (for U.S. GAAP) or IFRS 16 is advisable to ensure compliance and accuracy.

In conclusion, the calculation of rent expense for prepaid rent is a fundamental yet nuanced task in financial accounting. By systematically allocating prepaid rent over the rental period, businesses can ensure their financial statements accurately reflect the economic reality of their operations. Whether using a simple straight-line approach or a more tailored method, the goal remains the same: to match expenses with the periods in which the related benefits are consumed. Mastery of this process not only enhances financial reporting but also supports informed decision-making.

Is Posting 'For Rent' Ads with Racial Preferences Illegal?

You may want to see also

Explore related products

![]()

Amortization of Prepaid Rent

Prepaid rent represents an advance payment for future occupancy, a common scenario in commercial leases. When a business pays rent upfront for a period extending beyond the current accounting cycle, it creates an asset on the balance sheet. However, this asset isn’t recognized as an expense until the rented period is actually used. This is where amortization comes into play—a systematic process of allocating the prepaid rent expense over the period it benefits. For instance, if a company pays $12,000 for a year’s rent in January, only $1,000 should be expensed monthly, reflecting the monthly usage of the rented space.

While the concept is simple, errors in amortization can lead to significant financial misstatements. Common pitfalls include miscalculating the rental period or failing to adjust for partial months. For instance, if a lease starts mid-month, the first month’s amortization should reflect only the days used. Additionally, businesses must ensure consistency in their amortization method—straight-line is most common, but other methods may apply depending on lease terms. Auditors often scrutinize prepaid rent accounts, making accurate amortization critical for compliance and credibility.

Practical tips for managing prepaid rent amortization include leveraging accounting software to automate calculations and setting reminders for lease renewal or termination dates. Small businesses, in particular, benefit from templates that standardize the process. For example, a spreadsheet with formulas for monthly amortization can reduce manual errors. Regularly reconciling prepaid rent accounts ensures discrepancies are caught early. Finally, documenting the rationale behind amortization decisions—such as lease start dates or prorated periods—provides transparency and simplifies audits.

In conclusion, amortization of prepaid rent is a vital adjustment that ensures financial accuracy and adherence to accounting principles. By systematically allocating rent expenses over the leased period, businesses maintain a realistic view of their financial health. Whether through manual calculations or automated tools, precision in this process is non-negotiable. Mastering this adjustment not only enhances financial reporting but also builds trust with stakeholders, from investors to tax authorities.

Essential Steps to Take Before Renting in Montgomery County, MD

You may want to see also

Explore related products

![TracFone Motorola Moto g 5G (2024) [Activation Promotion] Locked Prepaid Smartphone, 128GB, Gray - Includes $20 Unlimited Talk, Text, & 4GB Data 30-Day Plan](https://m.media-amazon.com/images/I/71y7mfjjN1L._AC_UY218_.jpg)

![]()

Year-End Adjustment Process

Prepaid rent adjustments are a critical component of the year-end closing process, ensuring financial statements accurately reflect the current financial position of a business. This process involves reclassifying rent payments made in advance from an asset to an expense, aligning with the matching principle of accounting. For instance, if a company pays $12,000 in January for a year’s rent, only $1,000 should be expensed each month, with the remaining balance classified as a prepaid asset. At year-end, an adjusting entry is required to reallocate the unexpired portion of the prepaid rent to the following year, maintaining accuracy in financial reporting.

The year-end adjustment process for prepaid rent begins with a review of the general ledger to identify the prepaid rent account balance. Next, calculate the portion of rent that pertains to the current year versus the next. Using the previous example, if $6,000 of the $12,000 prepaid rent has been consumed by year-end, the adjusting entry would debit Rent Expense for $6,000 and credit Prepaid Rent for the same amount. This ensures the income statement reflects the correct rent expense for the period, while the balance sheet accurately shows the remaining prepaid asset.

A common pitfall in this process is overlooking partial periods or misinterpreting lease terms. For example, if a lease begins mid-year, the prepaid rent calculation must account for the exact number of months covered. Additionally, businesses should verify lease agreements for any escalations, discounts, or unusual payment terms that could affect the adjustment. Automated accounting systems can streamline this process, but manual checks remain essential to catch discrepancies, especially in complex lease structures or multi-year agreements.

From a strategic perspective, proper year-end adjustments for prepaid rent enhance financial transparency and compliance with accounting standards like GAAP or IFRS. Accurate reporting builds trust with stakeholders, including investors and auditors, who rely on precise financial data to assess a company’s health. Moreover, this process supports tax planning by ensuring deductible expenses are correctly timed, potentially reducing taxable income for the year. For small businesses, this might mean the difference between a profitable and unprofitable tax year, underscoring the practical significance of meticulous adjustments.

In conclusion, the year-end adjustment process for prepaid rent is a blend of technical precision and strategic foresight. By systematically reviewing prepaid balances, calculating accurate allocations, and avoiding common errors, businesses can maintain financial integrity and support informed decision-making. Whether leveraging software tools or manual checks, the goal remains the same: to ensure financial statements are a true reflection of the company’s financial reality at year-end.

Locate Your Rent Paid Certificate: A Step-by-Step Guide for Tenants

You may want to see also

Frequently asked questions

Prepaid rent refers to the payment made by a tenant to a landlord for rent in advance of the actual rental period. This often occurs when a tenant pays for multiple months of rent upfront.

An adjustment is made for prepaid rent at the end of an accounting period, typically monthly or annually, to recognize the portion of the prepaid rent that has been used or expired during that period.

The adjustment is recorded by debiting the rent expense account and crediting the prepaid rent asset account. This reduces the prepaid rent asset and recognizes the rent expense for the period.

The journal entry is: Debit Rent Expense (for the amount of rent used in the period) and Credit Prepaid Rent (for the same amount). For example, if $1,200 of prepaid rent is used in a month, the entry would be: Debit Rent Expense $1,200, Credit Prepaid Rent $1,200.

It is important to make an adjustment for prepaid rent to ensure that the financial statements accurately reflect the expenses incurred during the accounting period, adhering to the matching principle of accounting, which matches expenses with the revenues they help generate.