Rent should be recorded as an expense in the accounting period in which the leased property is used, aligning with the matching principle of accrual accounting. This means that if a business pays rent in advance for multiple months, the expense is not recognized all at once but rather allocated over the period the rent covers. For example, if a company pays $12,000 in January for a year’s rent, $1,000 would be recorded as an expense each month. Conversely, under the cash basis of accounting, rent is recorded as an expense when the payment is made, regardless of the period it covers. Proper timing ensures financial statements accurately reflect the business’s use of resources and financial performance.

| Characteristics | Values |

|---|---|

| Timing of Recognition | Rent should be recorded as an expense in the period it is incurred, following the accrual accounting principle. |

| Matching Principle | Expense is matched to the period in which the rented asset is used, not when payment is made. |

| Prepaid Rent | If rent is paid in advance, it is initially recorded as a prepaid asset and expensed over the rental period. |

| Cash Basis vs. Accrual Basis | Under accrual basis, rent is expensed when incurred; under cash basis, it is expensed when paid. |

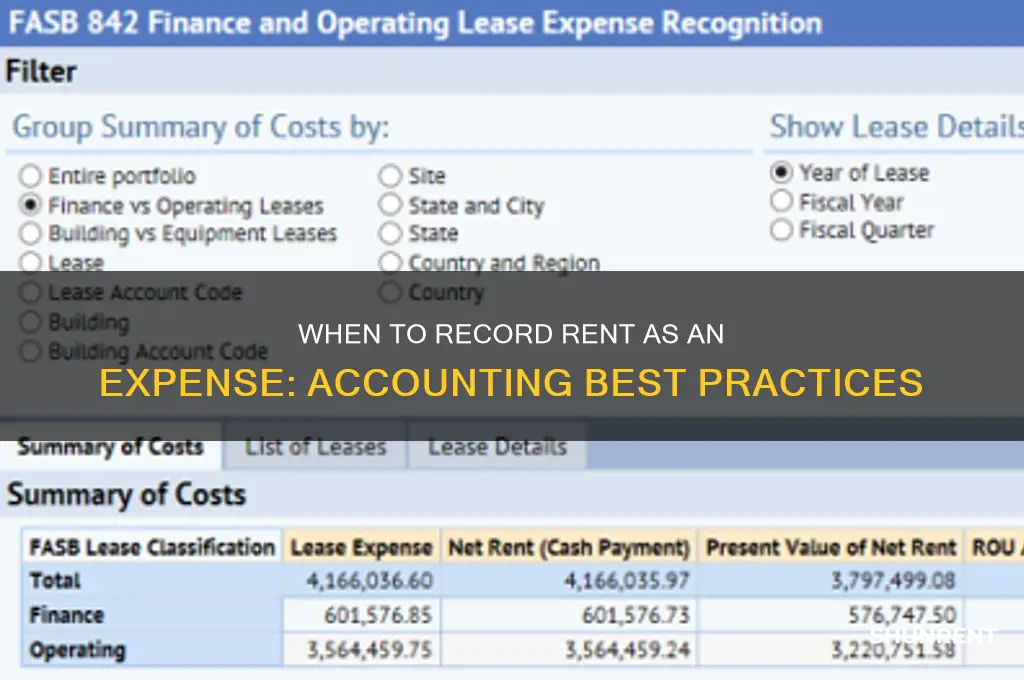

| Lease Classification | For operating leases, rent is expensed monthly; for finance leases, depreciation and interest are expensed separately. |

| Straight-Line Rent Expense | Rent with escalating payments is expensed evenly over the lease term under GAAP (ASC 842). |

| Tax Treatment | Rent is generally deductible in the year paid for tax purposes, but accrual-basis taxpayers follow the matching principle. |

| Short-Term vs. Long-Term Leases | Short-term leases (12 months or less) can be expensed monthly; long-term leases follow specific accounting standards. |

| Initial Direct Costs | Costs like legal fees or broker commissions are capitalized and amortized over the lease term. |

| Lease Incentives | Rent-free periods or incentives reduce rent expense over the lease term. |

| Variable Lease Payments | Payments tied to usage or index are expensed in the period they relate to. |

| Sublease Income | Reduces rent expense proportionally if a portion of the leased space is subleased. |

| Impairment of Right-of-Use Asset | If the right-of-use asset is impaired, rent expense may be adjusted accordingly. |

| International Standards (IFRS 16) | Similar to ASC 842, rent is recognized as a right-of-use asset and lease liability, with expense allocated over the lease term. |

Explore related products

$9.99

What You'll Learn

- Cash Basis Accounting: Record rent expense when payment is made, not when incurred

- Accrual Basis Accounting: Record rent expense when incurred, regardless of payment timing

- Prepaid Rent: Expense is recognized over the rental period, not upfront

- Lease Term: Expense timing depends on lease duration and payment schedule

- Tax Considerations: Timing may differ for tax purposes vs. financial reporting

![]()

Cash Basis Accounting: Record rent expense when payment is made, not when incurred

In cash basis accounting, the timing of recording expenses is straightforward: transactions are recognized only when cash changes hands. For rent, this means the expense is logged the moment payment is made, not when the obligation arises. This approach contrasts sharply with accrual accounting, where rent is recorded as incurred, regardless of payment timing. For small businesses or sole proprietors, this simplicity can be a significant advantage, as it aligns financial records directly with cash flow.

Consider a small retail store that pays $2,000 in rent monthly on the first of each month. Under cash basis accounting, the rent expense is recorded on January 1st, not December 1st, when the rent for January is typically incurred. This method ensures that the business’s financial statements reflect actual cash outflows, providing a clear picture of liquidity. However, it also means that expenses may not align with the period they relate to, potentially skewing short-term profitability assessments.

One practical tip for businesses using cash basis accounting is to maintain a separate calendar or ledger tracking rent due dates and payment dates. This ensures consistency and prevents errors, especially when payments span multiple periods. For instance, if a business pays quarterly rent in advance, the entire payment is recorded as an expense in the month it is paid, not spread across the three months it covers. This adherence to the cash basis principle is critical for compliance and accuracy.

Critics argue that cash basis accounting can misrepresent financial health, particularly for businesses with irregular cash flows. For example, a company paying rent in arrears might appear profitable in one month and loss-making in another, despite consistent operations. To mitigate this, businesses should pair cash basis accounting with regular cash flow forecasts and reconcile rent payments with lease agreements to ensure transparency.

In conclusion, cash basis accounting offers simplicity and clarity for rent expense recording, but it requires discipline and supplementary tools to avoid distortions. By recording rent when paid, businesses align expenses with actual cash movements, though they must remain vigilant to ensure this method serves their financial reporting needs effectively. For those prioritizing ease over complexity, this approach remains a viable and practical choice.

Sutton UK Rents: Affordable Single-Person Flat Options Revealed

You may want to see also

Explore related products

![]()

Accrual Basis Accounting: Record rent expense when incurred, regardless of payment timing

Rent expense under accrual basis accounting hinges on the principle of matching revenues with their associated costs in the period they are incurred, not when payment is made. This means if a business occupies a property in December but pays the rent in January, the expense is recorded in December. This approach ensures financial statements reflect the true financial position and performance of the business during a specific period, aligning with generally accepted accounting principles (GAAP).

For instance, imagine a retail store leasing a storefront. Even if the lease agreement stipulates rent is due on the 1st of each month, the store should recognize the rent expense for December in December’s financial statements, regardless of whether the payment is processed before or after year-end. This method provides a more accurate picture of the store’s profitability for that month.

The key distinction here lies in the timing of recognition. Cash basis accounting, in contrast, records expenses only when payment is made. Accrual basis, however, focuses on the economic substance of the transaction. By recording rent expense when incurred, businesses avoid distortions in financial reporting caused by payment timing discrepancies. This is particularly crucial for companies with significant rental commitments, as it prevents understating expenses in one period and overstating them in another.

A practical tip for implementing this principle is to establish a system for tracking lease agreements and their corresponding payment schedules. This allows for timely recognition of rent expenses in the appropriate accounting period, ensuring compliance with accrual accounting standards.

While accrual basis accounting provides a more accurate financial picture, it requires meticulous record-keeping and a clear understanding of lease terms. Businesses must carefully review lease agreements to identify the rent commencement date and any adjustments for prepaid or deferred rent. By adhering to this principle, companies can ensure their financial statements accurately reflect their rental obligations and provide a transparent view of their financial health.

Renting Redbox Movies for Less: A Promo Code Guide

You may want to see also

Explore related products

![]()

Prepaid Rent: Expense is recognized over the rental period, not upfront

Rent, a significant expense for many businesses, often involves prepaid arrangements where payment is made in advance for future occupancy. This raises the question: when is rent truly an expense? The answer lies in the principle of matching expenses with the period they benefit. Prepaid rent, therefore, is not expensed upfront but recognized gradually over the rental period.

This approach aligns with the accrual accounting method, which aims to reflect a company's financial performance accurately by matching revenues and expenses in the periods they occur.

Consider a scenario where a company pays $12,000 annually for office space, payable in advance. Recording the entire $12,000 as an expense in January would distort the financial picture, implying the company incurred a substantial cost in a single month. Instead, the $12,000 is recorded as a prepaid asset, and $1,000 is recognized as rent expense each month, reflecting the actual usage of the space. This method provides a more accurate representation of the company's financial health and operational costs.

The recognition of prepaid rent as an expense over time is not merely a matter of accounting convention but a reflection of economic reality. The benefit of occupying the rented space is derived over the entire rental period, not just at the time of payment. Therefore, expensing the rent gradually aligns with the principle of prudence, ensuring that expenses are not overstated in any given period.

To implement this approach, businesses should establish a systematic process for recognizing prepaid rent. This involves creating a prepaid rent account to record the initial payment and then systematically transferring a portion of this amount to the rent expense account each period. For instance, if a company prepays $6,000 for six months of rent, it would record $1,000 as rent expense each month, ensuring a consistent and accurate reflection of its rental costs.

In conclusion, the treatment of prepaid rent as an expense recognized over the rental period is a fundamental aspect of accurate financial reporting. By adhering to this principle, businesses can ensure their financial statements provide a true and fair view of their operations, facilitating informed decision-making by stakeholders. This approach not only complies with accounting standards but also reflects the economic substance of rental transactions, reinforcing the integrity of financial information.

When is Rent Due? Understanding Payment Deadlines and Late Fees

You may want to see also

Explore related products

![]()

Lease Term: Expense timing depends on lease duration and payment schedule

The timing of rent expense recognition hinges on the lease term, a critical factor that dictates when and how payments are recorded. Short-term leases, typically defined as those lasting 12 months or less, allow for straightforward expense recognition. Under generally accepted accounting principles (GAAP), rent for such leases is expensed evenly over the lease term, regardless of payment schedule. For instance, a six-month lease with a $6,000 total cost would be recorded as a $1,000 monthly expense, even if the full amount is paid upfront.

Long-term leases, exceeding 12 months, introduce complexity. Here, the payment schedule becomes pivotal. If payments are structured to increase or decrease over time, the expense must be allocated accordingly. For example, a five-year lease with escalating payments requires a more nuanced approach. Instead of recognizing expenses evenly, the straight-line method is often employed. This method spreads the total lease cost uniformly across the lease term, ensuring consistent expense recognition despite varying payment amounts.

Consider a scenario where a company signs a 10-year lease with annual payments starting at $50,000 and increasing by $2,000 each year. The total lease cost is $590,000. Using the straight-line method, the annual rent expense would be $59,000, regardless of the actual payment amount in any given year. The difference between the cash payment and the recognized expense is recorded as a deferred rent liability or asset, adjusting over time to reflect the true expense pattern.

Practical implementation requires careful documentation and adherence to accounting standards. For businesses, understanding the lease term and payment structure is essential for accurate financial reporting. Misalignment between expense recognition and payment schedules can distort financial statements, misleading stakeholders. For instance, failing to use the straight-line method for long-term leases with variable payments can result in overstated or understated expenses in certain periods.

In summary, the lease term and payment schedule are pivotal in determining when rent is recorded as an expense. Short-term leases allow for simple, even expense recognition, while long-term leases demand more sophisticated methods like the straight-line approach. By aligning expense timing with lease specifics, businesses ensure compliance and financial transparency, fostering trust among investors and regulators alike.

Scooter Rentals: Disney World's Documentation Requirements

You may want to see also

Explore related products

![Receipt Organizer Envelopes. 3-Way Organizers that Store Receipts, Track Expenses & Let You Find Receipts Fast. Includes an Expense Ledger + Mileage Log. 12 Pack. [6.5x9.5"] Made in USA.](https://m.media-amazon.com/images/I/811AGIXv7PL._AC_UY218_.jpg)

![]()

Tax Considerations: Timing may differ for tax purposes vs. financial reporting

Rent expense recognition can diverge sharply between tax and financial reporting frameworks, creating a compliance minefield for businesses. Under Generally Accepted Accounting Principles (GAAP), rent is typically expensed on a straight-line basis over the lease term, even if payments vary. For example, a 5-year lease with escalating payments of $10,000 (Year 1), $12,000 (Year 2), and $14,000 (Years 3-5) would be recorded as a consistent $12,000 annual expense for financial reporting. However, the IRS often requires taxpayers to deduct rent in the period paid, particularly for cash-basis taxpayers or when lease agreements specify variable payment structures tied to performance metrics.

This timing discrepancy necessitates meticulous record-keeping and dual-tracking systems. Consider a retail tenant whose rent includes a base amount plus 5% of annual sales exceeding $1 million. For tax purposes, the variable component would only be deductible in the year the sales threshold is met and the payment is made. Conversely, financial statements might recognize the expected variable expense ratably throughout the year based on sales projections. Failure to reconcile these differences could trigger audit flags or distort financial ratios like operating margins.

Strategic tax planning can exploit these timing differences, particularly around year-end transactions. A company with a December 31 fiscal year-end might prepay January rent in December to accelerate a tax deduction, even though financial reporting would defer the expense to the following period. However, such maneuvers require careful documentation to withstand IRS scrutiny, especially under Section 467 rules governing deferred payment arrangements. Small businesses with annual revenues under $25 million may qualify for simplified cash-method accounting, but should weigh the trade-offs between administrative simplicity and tax optimization.

To navigate these complexities, businesses should implement three-pronged controls: (1) maintain separate schedules reconciling book vs. tax rent expenses; (2) review lease agreements for ambiguous payment terms that could trigger IRS recharacterization; and (3) consult tax advisors when structuring leases with deferred or contingent payment features. For instance, a lease requiring $50,000 in tenant improvements before rent commences might capitalize these costs under GAAP but could deduct them immediately under certain tax safe harbors. Proactive management of these timing differences not only ensures compliance but also preserves cash flow through optimized tax liability management.

Understanding Colfax County's Average Cash Rent for Farmland in 2023

You may want to see also

Frequently asked questions

Rent should be recorded as an expense in the period it is incurred, regardless of when the payment is made. For example, if rent for December is paid in November, it should still be recorded as an expense in December under accrual accounting.

No, in cash-basis accounting, rent is recorded as an expense only when the payment is actually made. For instance, if rent is paid in January for the upcoming month, it is expensed in January, not in the month the rent covers.

Prepaid rent is initially recorded as an asset on the balance sheet. It is then expensed over the period it covers. For example, if six months of rent is prepaid, it is expensed evenly each month over those six months, not all at once.