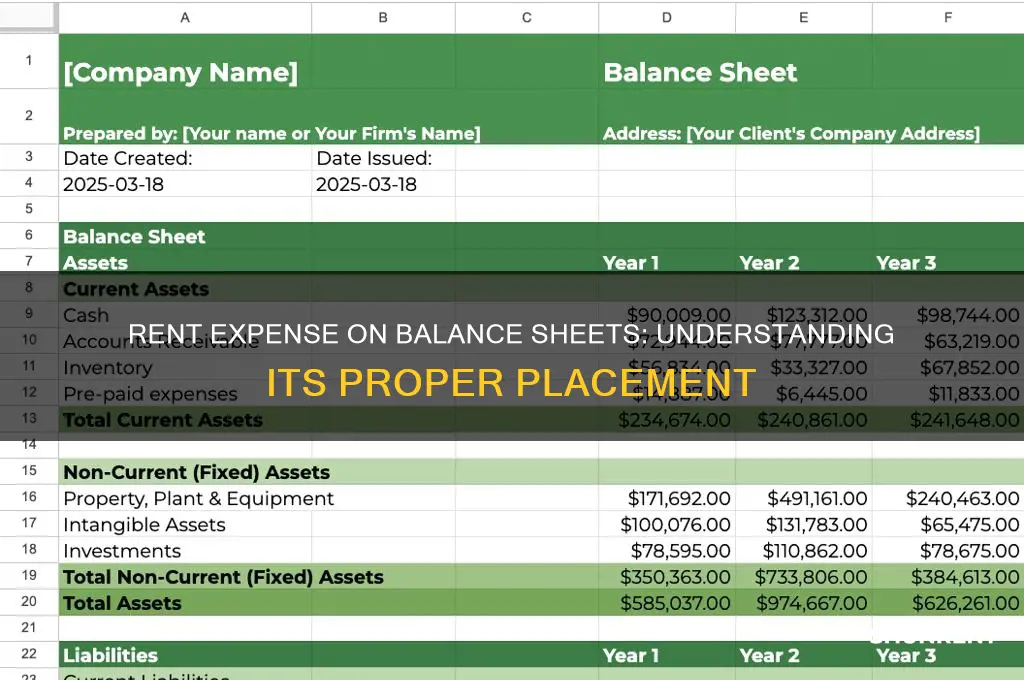

Rent expense is typically not directly recorded on a balance sheet, as it is considered an operational cost that affects the income statement. Instead, rent expense is recognized in the income statement under operating expenses, reducing the company's net income for the period. However, any prepaid rent or rent payable may appear on the balance sheet. Prepaid rent, which represents rent paid in advance, is recorded as a current asset, while rent payable, the amount owed for rent but not yet paid, is listed as a current liability. These entries ensure that the balance sheet accurately reflects the company's financial obligations and assets related to rent.

Explore related products

What You'll Learn

- Rent Expense Classification: Identify if rent is an operating or financing expense

- Income Statement Impact: Rent expense reduces net income on the income statement

- Prepaid Rent: Unexpired rent is recorded as a current asset on the balance sheet

- Accrued Rent: Unpaid rent is shown as a current liability on the balance sheet

- Lease Accounting: Capital leases affect assets and liabilities, while operating leases impact expenses

![]()

Rent Expense Classification: Identify if rent is an operating or financing expense

Rent expense is a critical component of a company's financial statements, but its classification can be a point of confusion. The question of whether rent is an operating or financing expense hinges on the nature of the lease and its impact on the business's core operations. In accounting, operating expenses are those directly tied to the day-to-day activities of a business, while financing expenses relate to the cost of raising capital or servicing debt. For most businesses, rent is an operating expense because it is essential for maintaining operations, such as leasing office space or retail locations. However, the classification can shift under specific circumstances, particularly with the adoption of accounting standards like ASC 842 or IFRS 16, which require leases to be capitalized on the balance sheet.

To determine if rent is an operating or financing expense, examine the lease agreement and its purpose. If the lease is for property or equipment used in daily operations, it is typically classified as an operating expense. For example, a retail store renting a storefront would categorize this rent as an operating expense because it directly supports sales activities. Conversely, if the lease is for a long-term asset that provides financing benefits, such as a lease-to-own agreement, it may be treated as a financing expense. However, this is less common and usually applies to specialized scenarios like leveraged leases in real estate or equipment financing.

The introduction of lease accounting standards has further complicated this classification. Under ASC 842 and IFRS 16, most leases are now recognized as right-of-use assets and lease liabilities on the balance sheet, effectively treating them as financing arrangements. However, the income statement still separates lease payments into interest (financing) and amortization of the right-of-use asset (operating). This distinction is crucial for financial analysis, as it affects metrics like operating cash flow and leverage ratios. For instance, separating the interest portion of a lease payment helps investors and analysts assess a company’s ability to generate cash from operations without the distortion of financing costs.

Practical tips for classifying rent expense include reviewing the lease term, payment structure, and the asset’s role in operations. Short-term leases or those with low-value assets may qualify for simplified accounting treatments, allowing them to be expensed directly as operating costs. Additionally, companies should disclose their lease accounting policies in financial statements to ensure transparency. For example, a technology firm leasing servers might classify this as an operating expense if the servers are essential for daily operations, even if the lease is capitalized under ASC 842.

In conclusion, rent expense is typically an operating expense but can be influenced by lease accounting standards and the nature of the lease. Understanding this classification is vital for accurate financial reporting and analysis. By focusing on the lease’s purpose, term, and accounting treatment, businesses can ensure compliance with standards and provide a clear financial picture to stakeholders. Whether operating or financing, proper classification of rent expense enhances the reliability and comparability of financial statements.

Renting a Suit: An Unnecessary Expense

You may want to see also

Explore related products

![]()

Income Statement Impact: Rent expense reduces net income on the income statement

Rent expense is a critical component of a company's financial health, and its impact on the income statement is both direct and measurable. When a business incurs rent expense, it is recorded as a deduction from revenue, thereby reducing the net income for the period. This reduction is not merely an accounting formality; it reflects the real cost of occupying space necessary for operations. For instance, a retail store paying $10,000 monthly in rent sees this amount subtracted from its gross profit, lowering the bottom line by the same figure. This straightforward relationship underscores the importance of managing rent costs to maintain profitability.

Analyzing the income statement reveals how rent expense fits into the broader financial picture. It is typically categorized under operating expenses, alongside items like utilities and salaries. Unlike capital expenditures, which are investments in long-term assets, rent is an ongoing operational cost. For example, a tech startup with a $5,000 monthly rent payment would list this under "Selling, General, and Administrative Expenses" (SG&A). Over time, if rent increases—say, from $5,000 to $7,000—the income statement will show a corresponding decrease in net income, assuming all other factors remain constant. This highlights the need for businesses to monitor rent trends and negotiate favorable lease terms.

From a strategic perspective, understanding the income statement impact of rent expense enables better decision-making. Companies may opt to sublease excess space or relocate to lower-cost areas to mitigate this expense. For instance, a small business paying 20% of its revenue in rent could explore shared office spaces, potentially reducing this ratio to 10%. Such actions not only preserve net income but also improve cash flow, which is vital for reinvestment and growth. Conversely, ignoring rent expense trends can lead to financial strain, particularly in industries with thin profit margins.

A comparative analysis of rent expense across industries further illustrates its significance. In sectors like retail and hospitality, rent often constitutes a larger share of operating expenses compared to manufacturing or technology. A restaurant, for example, might allocate 15-20% of its revenue to rent, while a software company may spend less than 5%. This disparity emphasizes the need for industry-specific financial strategies. Businesses in high-rent industries should focus on optimizing space utilization or adopting hybrid work models to reduce reliance on physical locations.

In conclusion, rent expense’s role in reducing net income on the income statement is a tangible and actionable financial metric. By tracking and managing this cost, businesses can enhance profitability and adaptability. Practical steps include regular lease reviews, exploring alternative workspace arrangements, and benchmarking rent-to-revenue ratios against industry standards. Ultimately, treating rent expense as a strategic variable rather than a fixed cost empowers companies to navigate financial challenges more effectively.

Understanding Rent-to-Own Takeover Payments: A Comprehensive Guide for Buyers

You may want to see also

Explore related products

![]()

Prepaid Rent: Unexpired rent is recorded as a current asset on the balance sheet

Rent expense, a fundamental component of a company's financial obligations, is typically recorded on the income statement, reflecting the cost of occupying a property over a specific period. However, when rent is paid in advance, it introduces a unique accounting treatment that shifts the focus to the balance sheet. This is where the concept of prepaid rent comes into play, offering a nuanced perspective on how unexpired rent is managed in financial reporting.

In the realm of accounting, prepaid rent represents a situation where a tenant pays rent for a period that extends beyond the current accounting period. Instead of immediately expensing the entire payment, the unexpired portion is recognized as a current asset on the balance sheet. This approach adheres to the matching principle, ensuring that expenses are aligned with the revenues they help generate. For instance, if a company pays $12,000 for a year’s rent in January, only $1,000 is expensed monthly, while the remaining $11,000 is classified as prepaid rent, a current asset.

The classification of prepaid rent as a current asset is strategic, as it reflects the company’s right to use the property for the unexpired period. This asset is gradually reduced each month as the rent expense is recognized, ensuring that the financial statements accurately represent the company’s financial position. For example, a retail business leasing a storefront might prepay six months of rent. During this period, the prepaid rent account is amortized monthly, with the corresponding amount moved to the rent expense account on the income statement.

From a practical standpoint, managing prepaid rent requires meticulous record-keeping and periodic adjustments. Accountants must ensure that the prepaid rent account is accurately adjusted each month to reflect the portion of rent that has been consumed. This process not only maintains the integrity of the financial statements but also provides stakeholders with a clear picture of the company’s short-term assets and liabilities. For small businesses, using accounting software can streamline this process, automating the amortization of prepaid rent and reducing the risk of errors.

In conclusion, prepaid rent serves as a critical bridge between the income statement and the balance sheet, ensuring that rent expenses are recognized in the periods they pertain to. By recording unexpired rent as a current asset, companies adhere to accounting principles while providing transparency into their financial health. This treatment underscores the importance of understanding the nuances of rent accounting, particularly for businesses with significant lease obligations. Whether a seasoned accountant or a business owner, mastering this concept is essential for accurate financial reporting and informed decision-making.

Pre-Foreclosure Rent-to-Own: A Guide to Buying Homes at Risk

You may want to see also

Explore related products

![]()

Accrued Rent: Unpaid rent is shown as a current liability on the balance sheet

Rent expense, a fundamental component of a company's financial obligations, is typically recorded in the income statement, reflecting the cost of leasing property over a specific period. However, when rent remains unpaid at the end of an accounting period, it transforms into a distinct accounting concept known as accrued rent. This unpaid rent is not merely forgotten or overlooked; instead, it is meticulously documented as a current liability on the balance sheet. This treatment ensures that the company's financial statements accurately represent its outstanding obligations, providing a clear picture of its short-term financial responsibilities.

From an analytical perspective, accrued rent serves as a critical indicator of a company's liquidity and cash flow management. By recording unpaid rent as a current liability, businesses acknowledge their immediate financial commitments, which are expected to be settled within the next 12 months. This classification aligns with the principles of accrual accounting, where expenses are recognized when incurred, not when paid. For instance, if a company occupies a property in December but pays the rent in January, the rent expense for December is still recognized in that year’s financial statements, with the unpaid amount reflected as accrued rent on the balance sheet.

Instructively, accounting for accrued rent involves a straightforward yet essential journal entry. At the end of the accounting period, the company debits Rent Expense (an income statement account) and credits Accrued Rent Payable (a balance sheet liability account). This entry ensures that the expense is recognized in the appropriate period while simultaneously capturing the unpaid obligation. For example, if a company has $5,000 in unpaid rent at year-end, the entry would be: *Debit Rent Expense $5,000, Credit Accrued Rent Payable $5,000*. Once the rent is paid, the liability account is debited, and cash is credited, removing the obligation from the balance sheet.

Comparatively, accrued rent differs from prepaid rent, another common rent-related account. While accrued rent represents an unpaid obligation, prepaid rent reflects advance payments made for future rental periods. Prepaid rent is recorded as a current asset on the balance sheet, as it represents a right to future benefits. This distinction highlights the importance of accurately classifying rent-related transactions to maintain the integrity of financial statements. For example, if a company pays $12,000 in January for a year’s rent, $10,000 would be recorded as prepaid rent (asset) at year-end, with $2,000 recognized as rent expense.

Practically, understanding accrued rent is vital for stakeholders, including investors, creditors, and management. For investors, it provides insight into a company’s short-term financial health and its ability to meet immediate obligations. Creditors use this information to assess the risk of extending credit, while management relies on it for budgeting and cash flow planning. For small businesses or startups, managing accrued rent effectively can prevent cash flow shortages and maintain positive relationships with landlords. A practical tip is to regularly reconcile rent payments with lease agreements to ensure accurate accruals and avoid discrepancies.

In conclusion, accrued rent is more than just an accounting entry; it is a reflection of a company’s financial discipline and transparency. By recording unpaid rent as a current liability on the balance sheet, businesses adhere to accounting standards while providing a comprehensive view of their financial position. Whether you’re a business owner, accountant, or financial analyst, mastering this concept ensures accurate reporting and informed decision-making.

Simplify Rent Payments: Setting Up Autopay with Chase Bank

You may want to see also

Explore related products

![]()

Lease Accounting: Capital leases affect assets and liabilities, while operating leases impact expenses

Rent expense, a common line item in income statements, doesn't directly appear on a balance sheet. This is because it represents a cost incurred during a specific period, not an asset or liability held by the company. However, the treatment of leases, which often underlie rent agreements, significantly impacts a company's balance sheet.

Distinguishing Between Lease Types: The key distinction lies in the nature of the lease. Capital leases, also known as finance leases, are essentially purchases disguised as rentals. The lessee gains substantial control over the asset, often with the option to purchase it at a discounted price at the end of the lease term. This treatment reflects economic reality: the company effectively owns the asset. Consequently, capital leases are capitalized on the balance sheet. The present value of future lease payments is recorded as an asset (right-of-use asset) and a corresponding liability (lease liability).

Operating leases, on the other hand, are more akin to traditional rentals. The lessee doesn't gain significant control over the asset and doesn't expect to own it at the end of the lease term. These leases are treated as operating expenses. Rent payments are expensed directly on the income statement, bypassing the balance sheet entirely.

Impact on Financial Ratios: The classification of leases has a ripple effect on financial ratios. Capitalizing leases increases both assets and liabilities, potentially affecting metrics like debt-to-equity ratio and return on assets. Operating leases, by keeping liabilities off the balance sheet, can artificially inflate these ratios, making a company appear less leveraged than it truly is.

Disclosure Requirements: Accounting standards mandate clear disclosure of lease arrangements in financial statements. This includes details about lease terms, future lease payments, and the rationale behind lease classification. This transparency allows investors and analysts to accurately assess a company's financial health and obligations.

Understanding the distinction between capital and operating leases is crucial for interpreting financial statements accurately. While rent expense itself doesn't appear on the balance sheet, the underlying lease structure can significantly impact a company's asset and liability composition, ultimately shaping its financial portrait.

Penske Rental Auto Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Rent expense does not appear directly on the balance sheet. It is recorded on the income statement as an operating expense, reducing net income.

Rent expense itself is not a liability. However, prepaid rent or rent payable (if owed) may appear as a current liability or current asset on the balance sheet.

Prepaid rent is recorded as a current asset on the balance sheet until the rent period is used, at which point it is expensed on the income statement.

Yes, rent expense indirectly affects the balance sheet by reducing retained earnings (part of equity) when net income is decreased on the income statement.

Rent-related information, such as prepaid rent or rent payable, can be found under current assets or current liabilities, respectively, on the balance sheet.