Prepaid rent is a crucial component of a company's financial statements, representing advance payments made for future rental obligations. On a balance sheet, prepaid rent is classified as a current asset, typically listed under the Prepaid Expenses or Other Current Assets section. This categorization reflects its short-term nature, as it represents a benefit that will be consumed within the next 12 months. By recording prepaid rent as an asset, businesses ensure that their financial statements accurately reflect the value of resources paid for but not yet utilized, aligning with the principles of accrual accounting and providing a clear snapshot of the company's financial position.

| Characteristics | Values |

|---|---|

| Classification | Current Asset |

| Location on Balance Sheet | Typically listed under the "Current Assets" section, often near "Cash and Cash Equivalents" or "Accounts Receivable" |

| Nature | Represents rent paid in advance for a future period |

| Recognition | Recorded as an asset when payment is made, then gradually expensed over the rental period |

| Accounting Treatment | Initially debited to Prepaid Rent (asset account) and credited to Cash; subsequently, a portion is debited to Rent Expense and credited to Prepaid Rent each period |

| Reporting Standard | Compliant with GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) |

| Time Frame | Short-term, typically covering a period of one year or less |

| Impact on Financial Statements | Reduces cash balance initially, then impacts income statement as rent expense over time |

| Example | If a company pays $12,000 for a year's rent in advance, $1,000 is expensed monthly, reducing the prepaid rent asset by $1,000 each month |

| Disclosure | May require footnote disclosure if material or part of a significant lease agreement |

Explore related products

What You'll Learn

![]()

Current vs. Long-term Assets

Prepaid rent, a common accounting entry, often sparks confusion regarding its classification on a balance sheet. The distinction between current and long-term assets is crucial here, as it directly impacts a company's financial portrayal and liquidity assessment. This classification hinges on a fundamental principle: the asset's expected conversion into cash or its consumption within one year or the operating cycle, whichever is longer.

Understanding the Time Horizon:

The defining factor for classifying prepaid rent is its time horizon. If the prepaid rent covers a period within the next 12 months, it falls under current assets. This categorization reflects its imminent consumption and contribution to short-term operational needs. Conversely, if the prepaid rent extends beyond this timeframe, it's classified as a long-term asset, indicating a longer-term benefit to the company.

Practical Example:

Imagine a company pays $12,000 annually for rent in advance on January 1st. If the company's fiscal year ends on December 31st, the entire $12,000 would be considered a current asset, as it will be fully consumed within the year. However, if the company pays $24,000 for a two-year lease upfront, $12,000 would be classified as a current asset (covering the first year), while the remaining $12,000 would be a long-term asset, reflecting the rent for the second year.

Implications for Financial Analysis:

This classification significantly impacts financial analysis. Current assets, including the portion of prepaid rent applicable within the year, are crucial for assessing a company's liquidity and ability to meet short-term obligations. Long-term assets, on the other hand, provide insights into a company's long-term financial health and investment in future operations.

Key Takeaway:

Properly classifying prepaid rent as current or long-term is essential for accurate financial reporting and analysis. By understanding the time horizon principle and its practical application, accountants and analysts can ensure a clear and transparent representation of a company's financial position. This distinction allows stakeholders to make informed decisions based on a realistic assessment of the company's short-term and long-term financial commitments.

Jackson Hole Bear Spray Rentals: Your Ultimate Safety Guide

You may want to see also

Explore related products

![]()

Prepaid Rent Classification

Prepaid rent represents a unique accounting challenge, as it embodies both an asset and a future expense. On a balance sheet, it is classified as a current asset, but this placement hinges on a critical temporal distinction. If the prepaid rent covers a period of one year or less, it remains in the current assets section, reflecting its short-term nature. However, if the prepaid rent extends beyond one year, the portion applicable to the period beyond one year is reclassified as a long-term asset. This distinction ensures the balance sheet accurately reflects the liquidity and timing of the asset.

Consider a practical example: a company pays $12,000 for a year’s rent in advance. In this case, the entire $12,000 is recorded as prepaid rent under current assets. However, if the company pays $24,000 for a two-year lease, $12,000 would be classified as a current asset, and the remaining $12,000 would be listed as a long-term asset. This bifurcation aligns with accounting principles like GAAP and IFRS, which emphasize the importance of matching expenses to the periods they benefit.

The classification of prepaid rent also impacts financial ratios and analysis. For instance, a higher current asset balance can improve the current ratio, a key liquidity metric. However, misclassification—such as treating long-term prepaid rent as entirely current—can distort financial health assessments. Auditors and analysts scrutinize this line item to ensure compliance and accuracy, as it directly affects the portrayal of a company’s short-term financial position.

To ensure proper classification, follow these steps: first, identify the lease term and payment structure. Next, allocate the prepaid rent between current and long-term assets based on the one-year threshold. Finally, document the rationale for the classification to support audit trails. Tools like accounting software can automate this process, reducing the risk of errors. For instance, QuickBooks and Xero allow users to set up prepaid expense accounts with automatic amortization schedules, ensuring consistent and accurate reporting.

In conclusion, prepaid rent classification is not merely a technicality but a critical component of financial transparency. By understanding and applying the rules governing its placement on the balance sheet, businesses can maintain accurate records, comply with accounting standards, and provide stakeholders with a clear picture of their financial health. Whether you’re a CFO, accountant, or business owner, mastering this classification ensures your financial statements reflect both precision and integrity.

Maximize Profits: Renting Your Box Truck for Side Income

You may want to see also

Explore related products

![]()

Balance Sheet Presentation

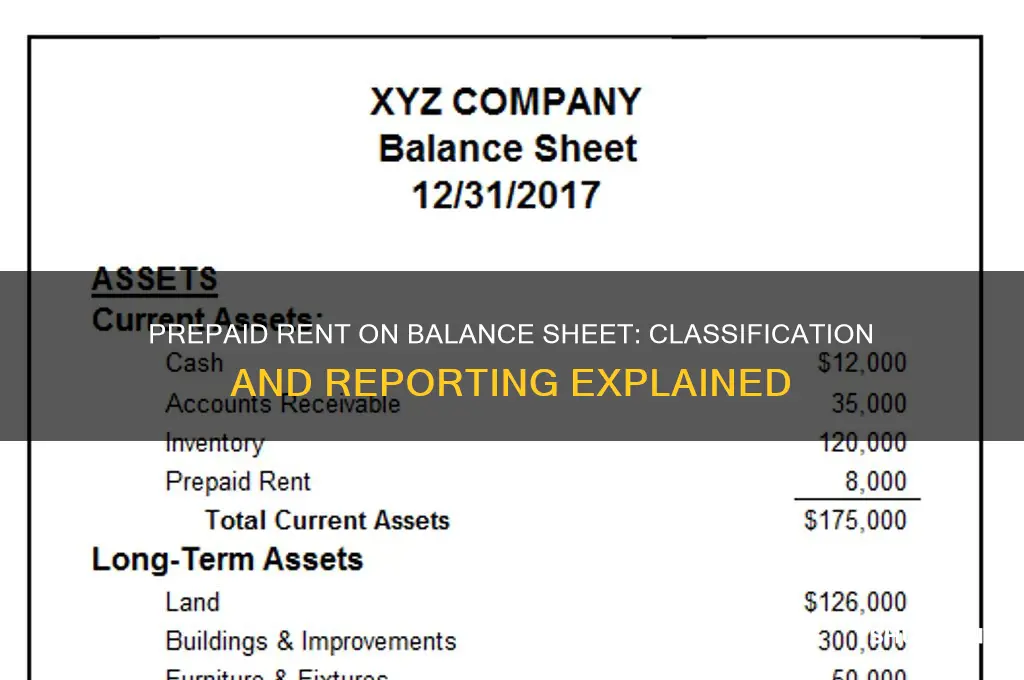

Prepaid rent is classified as a current asset on the balance sheet because it represents a payment made in advance for future benefits, typically within the next 12 months. This categorization aligns with accounting principles that require assets to be reported based on their liquidity and expected conversion into cash. Unlike long-term assets, prepaid rent is short-term in nature, as it covers expenses for a defined period, usually a month or a quarter. For instance, if a company pays $12,000 in January for a year’s rent, $1,000 would be recorded as prepaid rent (a current asset) and amortized monthly as rent expense.

The presentation of prepaid rent on the balance sheet is straightforward but requires precision. It is listed under the "Current Assets" section, often alongside other short-term assets like cash, accounts receivable, and inventory. The amount reported reflects the portion of the prepaid expense that has not yet been consumed. For example, if a company prepays $6,000 for six months of rent, the balance sheet would show $6,000 under prepaid rent until the expense is gradually recognized over the six-month period. This ensures the balance sheet accurately reflects the company’s financial position at a given point in time.

One critical aspect of presenting prepaid rent is the need for consistency and transparency. Companies must adhere to accounting standards, such as GAAP or IFRS, which dictate how prepaid expenses are recorded and disclosed. For instance, GAAP requires prepaid rent to be amortized systematically over the rental period, with the remaining balance clearly stated on the balance sheet. This transparency helps stakeholders, including investors and creditors, understand the company’s liquidity and short-term obligations. Misclassification or omission of prepaid rent could distort financial ratios, such as the current ratio, which assesses a company’s ability to meet short-term liabilities.

To ensure accurate balance sheet presentation, companies should follow a structured approach. First, identify all prepaid expenses, including rent, insurance, and supplies, and verify their amounts and terms. Second, allocate the prepaid rent to the appropriate accounting period using a consistent method, such as the straight-line basis. Third, review the balance sheet to confirm that prepaid rent is correctly classified as a current asset and that the amount aligns with supporting documentation. Finally, disclose any significant prepaid rent balances in the notes to the financial statements, providing additional context for users.

In practice, the presentation of prepaid rent can vary slightly depending on industry norms and company size. For example, small businesses may combine prepaid rent with other prepaid expenses under a single line item, while larger corporations might break it out separately for clarity. Regardless of the approach, the goal remains the same: to provide a clear and accurate snapshot of the company’s financial health. By properly presenting prepaid rent, businesses enhance the reliability of their financial statements and build trust with stakeholders.

Renting a Tiller in Odessa, TX: Top Local Options

You may want to see also

Explore related products

$19.15 $24.95

![]()

Impact on Financial Ratios

Prepaid rent, classified as a current asset on the balance sheet, directly influences liquidity ratios like the current ratio and quick ratio. By increasing current assets without affecting current liabilities, prepaid rent artificially inflates these ratios. For instance, a company with $100,000 in current assets and $50,000 in current liabilities has a current ratio of 2:1. Adding $10,000 in prepaid rent boosts the current ratio to 2.2:1, potentially misleading stakeholders about short-term liquidity. Analysts must scrutinize this component to avoid overestimating a company’s ability to meet immediate obligations.

The impact of prepaid rent on profitability ratios, such as return on assets (ROA), is more nuanced. Since prepaid rent ties up funds that could otherwise be invested in revenue-generating activities, it reduces the efficiency of asset utilization. For example, if a company’s total assets are $500,000 and net income is $50,000, the ROA is 10%. However, if $20,000 of those assets are prepaid rent, the effective asset base for generating income is lower, distorting the true profitability picture. Adjusting for non-operational assets like prepaid rent provides a clearer view of operational efficiency.

Debt-to-equity and other leverage ratios remain largely unaffected by prepaid rent, as it does not alter liabilities or equity. However, its presence can indirectly influence borrowing decisions. Lenders often rely on liquidity ratios to assess creditworthiness, and inflated ratios due to prepaid rent might lead to over-lending. Conversely, if prepaid rent is substantial, it could signal a conservative approach to cash management, which lenders may view positively. Understanding this dynamic is crucial for both borrowers and lenders in evaluating financial health.

Practical tip: When analyzing financial ratios, isolate prepaid rent from other current assets to assess its impact. For instance, recalculate the quick ratio (excluding inventory and prepaid expenses) to gauge immediate liquidity more accurately. Additionally, compare prepaid rent to total current assets; if it exceeds 10%, investigate whether it reflects prudent planning or inefficient cash management. This granular approach ensures ratios reflect operational reality rather than accounting nuances.

Eviction Process Timeline: How Long Until a Renter Must Vacate?

You may want to see also

Explore related products

![]()

Adjustment Journal Entries

Prepaid rent represents a unique accounting challenge, requiring careful treatment to ensure financial statements accurately reflect a company's financial position. Adjustment journal entries are the mechanism used to achieve this accuracy, specifically when dealing with prepaid expenses like rent.

Here's a breakdown of how these entries work in the context of prepaid rent:

Understanding the Need for Adjustment: Imagine a company pays $12,000 in rent for the upcoming year in December. Recording this as a full expense in December would distort the financial picture, as the benefit of the rent extends into the next year. Adjustment journal entries rectify this by allocating the expense over the period it benefits.

In this case, only $1,000 (representing December's rent) should be expensed, with the remaining $11,000 recorded as a prepaid asset on the balance sheet.

The Adjustment Entry: The adjustment journal entry for prepaid rent typically involves debiting the Prepaid Rent account (an asset account) and crediting the Rent Expense account (an expense account). The amount debited to Prepaid Rent reflects the portion of the rent payment that hasn't yet been used. For our example, the entry would be:

- Debit: Prepaid Rent - $11,000

- Credit: Rent Expense - $1,000

Impact on Financial Statements: This adjustment has a direct impact on both the income statement and the balance sheet. On the income statement, only the portion of rent expense incurred in the current period is reflected, providing a more accurate picture of profitability. On the balance sheet, the Prepaid Rent account increases, representing the future economic benefit the company holds.

Best Practices: Consistency is key. Establish a clear policy for recognizing prepaid rent and apply it consistently across all periods. Regularly review prepaid rent balances to ensure they accurately reflect the remaining benefit. Consider using accounting software that automates the adjustment process to minimize errors.

Bergen County NJ Office Space Rental Rates: What to Expect

You may want to see also

Frequently asked questions

Prepaid rent is recorded as a current asset on the balance sheet under the "Prepaid Expenses" or "Other Current Assets" section.

Prepaid rent is considered an asset because it represents a payment made in advance for future benefits.

Prepaid rent is initially recorded as an asset and then gradually expensed over the rental period through adjusting entries.

Yes, prepaid rent affects the income statement as it is expensed over time, reducing the reported rental expense in the periods it benefits.

Once prepaid rent is fully expensed, it is removed from the balance sheet, as the asset has been fully utilized.