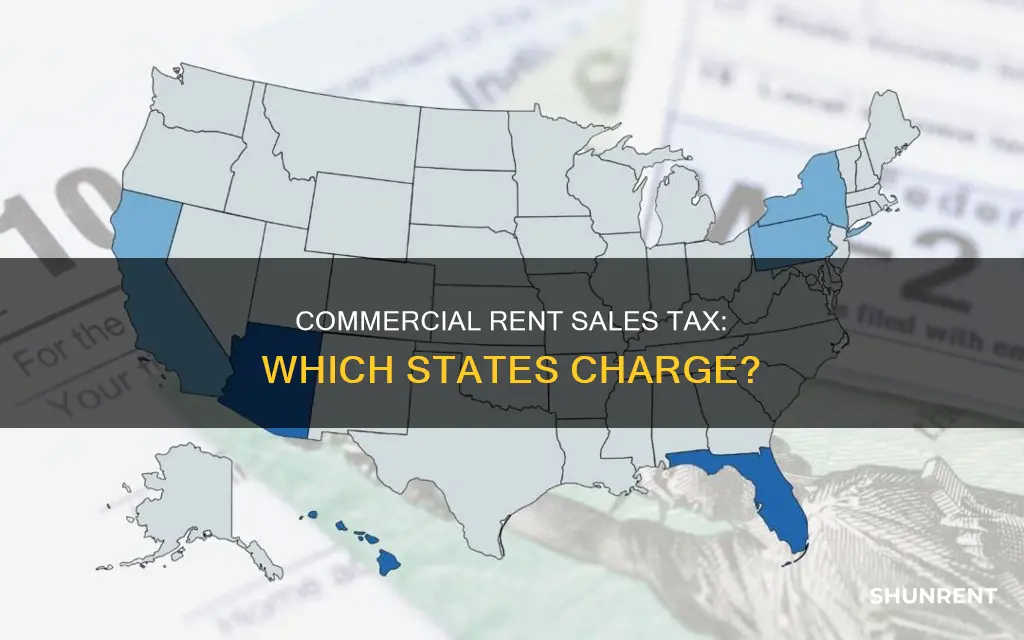

Florida is the only state in the US to charge sales tax on commercial leases. This includes land, buildings, office or retail space, and convention or meeting rooms. The state imposes a 6% sales tax on the total rent paid for any commercial property. However, the sales tax rate on commercial rent has been decreasing over the years, with a reduction to 4.5% in December 2023 and further plans to reduce it to 2% in 2024. While Florida is the only state with a comprehensive sales tax on commercial leases, other states and cities have similar taxes. For example, New York City imposes a 6% tax on commercial real estate leases for companies paying over $250,000 in rent annually.

| Characteristics | Values |

|---|---|

| States that charge sales tax on commercial rent | Florida, New York City, Hawaii, Arizona |

| Florida sales tax rate on commercial rent | 5.5% (previously 6%) |

| Florida sales tax rate on commercial rent from Dec 1, 2023 | 4.5% |

| Florida sales tax rate on commercial rent in mid-2024 | 2% |

| Florida sales tax on commercial rent applies to | Amounts paid as rent by commercial tenants, common area maintenance, parking, janitorial services, real estate taxes, insurance, mortgage payments, ad valorem taxes, subleases |

| Florida sales tax on commercial rent does not apply to | Agricultural rentals, rentals to exempt/nonprofit organizations or government agencies, dwellings, public streets or roads used for transportation |

| Other states' sales tax on commercial rent | Alabama, Arkansas, California |

| Other states' sales tax on commercial rent specifics | New York City imposes a 6% tax on commercial leases for companies paying at least $250,000 in rent annually; Hawaii imposes a 4% general excise tax on income, including rentals; Arizona has 5 cities with a tax on commercial leases; Alabama and Arkansas charge sales tax on rentals of tangible personal property unless specific exemptions apply; California offers lessors a choice to pay sales tax on the initial purchase or collect use tax from lessees |

Explore related products

What You'll Learn

![]()

Florida's unique sales tax on commercial rent

Florida is the only state in the US to impose a sales tax on commercial rent. This tax is levied on the total rent paid for any commercial property, including storefronts, offices, and warehouses. The tax rate has been reduced over the years, with the latest rate standing at 2% as of June 1, 2024. However, individual counties in Florida may impose an additional sales surtax, which can increase the effective tax rate.

The uniqueness of Florida's commercial rent sales tax lies in its comprehensive nature. While other states and municipalities have similar taxes, none of them are as broad in scope as Florida's. For example, New York City imposes a 6% tax on commercial real estate leases, but only on companies that pay at least $250,000 in annual rent. Similarly, Hawaii has a 4% general excise tax on income, which can include rental income, while Arizona has five cities that impose a tax on commercial real estate leases despite having no state-level tax on rent.

Florida's commercial rent sales tax applies to a wide range of commercial properties, including office spaces, retail stores, warehouses, and even licenses for vending, amusement, or newspaper machines. The tax is due on the rental stream, which refers to the periodic rental payments made by the lessee to the lessor. This tax can be a significant expense for businesses operating in Florida, and both landlords and tenants must be aware of their obligations to avoid costly mistakes and ensure smooth operations.

The state's sales tax on commercial rent has been a topic of discussion and proposed changes. For instance, in his 2017-18 recommended budget, Governor Rick Scott proposed reducing the tax on commercial leases by 25%, which was expected to cut off $454 million in state sales tax revenue. Additionally, Governor DeSantis signed House Bill 7063 in 2023, which reduced the sales tax rate on commercial leases of real property from 5.5% to 4.5%.

Chapel Hickory Hills Apts: Available to Rent Now

You may want to see also

Explore related products

![]()

New York City's CRT tax

Florida is the only state in the US to levy a sales tax on all commercial leases. However, some other states and municipalities have similar taxes, though none are as comprehensive as Florida's. For example, New York City imposes a 6% tax on commercial real estate leases, but only on companies that pay at least $250,000 in rent annually.

The Commercial Rent Tax (CRT) in New York City is a tax levied on businesses that rent commercial real estate. The CRT rate is currently 3.9%. However, businesses with a total income of less than $5,000,000 in the preceding tax year and paying less than $500,000 in annual base rent are exempt from CRT liability. They will receive a full tax credit, effectively reducing their tax burden.

For businesses with total incomes between $5,000,000 and $10,000,000 and annual base rents between $500,000 and $550,000, a partial tax credit is available on a sliding scale. The tax credit phases out at $10,000,000 in total income and $550,000 in annual base rent. The credit is calculated by multiplying the tax amount by the "income factor" and the "rent factor".

For example, a business with a total income of $7,500,000 and an annual base rent of $525,000 will receive a credit on their CRT equal to one quarter of their tax owed:

Tax = $525,000 * 3.9% = $20,475

Credit = $20,475 * ($2,500,000/$5,000,000) * ($25,000/$50,000)

Credit = $20,475 * 50% * 50%

Credit = $5,119

The CRT amendment specifically targets small businesses, and those that have been historically non-compliant for CRT purposes may be eligible for a Voluntary Disclosure Agreement, which offers a waiver of penalties and a limited look-back period of three to six years.

Boat Rentals: What You Need to Know

You may want to see also

Explore related products

![]()

Alabama's rental tax

Alabama generally charges a privilege or license tax (rental tax) on the rental or lease of tangible personal property unless a specific exemption applies. The gross receipts, including any rental tax invoiced, from the rental or leasing of tangible personal property are subject to the state rental tax. This tax is due on true leases, in which the title to the property is retained by the lessor at the end of the lease agreement or when the lessee has an option to purchase the item at the end of the lease agreement for the fair market value of the item.

Rental tax returns and remittances are due on or before the 20th day of the month for the previous month’s rentals. However, you may request quarterly filing status if you have a tax liability of less than $2,400 for the preceding calendar year. You may request semi-annual filing if your tax liability for the preceding calendar year is less than $1,200. You may also request annual filing status if your tax liability for the entire preceding calendar year is less than $600. Changes to the filing status can only be requested each year before February 20 to file quarterly, semi-annually, or annually for that calendar year.

Rental facilitators are required to collect and remit rental tax for leases made to Alabama customers or comply with the notice and reporting requirements. Rental facilitators must apply for a special rental tax account with the Alabama Department of Revenue (ALDOR) to comply with remittance or reporting requirements. If the rental facilitator chooses to comply with the notice and reporting requirements instead of collecting and remitting rental tax, an annual informational reporting requirement with ALDOR is necessary, along with an annual transaction summary notice provided to each third-party owner/lessor.

"Conditional sales leases" in Alabama are subject to sales tax. These are leases in which the title of the property is transferred to the lessee at the end of the lease agreement or when the lessee has the option to purchase the item for a nominal amount, with no option to return the leased item without purchasing. When equipment is under the control of and operated by an employee of the lessor, the transaction is considered a service rendered and is not subject to rental tax. Local rental tax is levied in the same manner as the state rental tax, and these rates vary.

The rental tax rate for most tangible personal property in Alabama is 4% of the gross proceeds of the business. However, a 2% rate applies to the gross proceeds from the leasing or rental of linens and garments, while a 1.5% rate applies to the gross proceeds from the leasing or rental of automotive vehicles, truck trailers, semi-trailers, and house trailers.

Renting a Lamborghini for a Day: The Ultimate Guide

You may want to see also

Explore related products

![]()

Arkansas's sales tax on rentals

In Arkansas, sales tax is imposed on the lease or rental of tangible personal property. The state's sales tax rate is 6.5% of the gross receipts from the sale of tangible personal property and selected services. However, food sales are taxed at 2%, and alcoholic beverages are subject to additional taxes. Local governments in Arkansas are also allowed to impose additional local sales and use taxes.

The definition of "sale" in Arkansas includes the lease or rental of tangible personal property. The tax is paid based on the rental or lease payments made to the lessor. A rental vehicle tax is imposed on the gross receipts from rentals of licensed motor vehicles leased for 30 days or less. This tax does not apply to diesel trucks rented or leased for commercial shipping or farm machinery. It also does not apply to trucks rented or leased for residential moving or shipping.

In addition to the state sales tax, local sales taxes may be levied by each city or county in Arkansas. Businesses may apply for a refund of local taxes from the Arkansas Department of Finance and Administration. The state collects these taxes and distributes them to the cities and counties monthly.

It's important to note that ancillary charges such as finance, insurance, and maintenance play a role in determining the overall tax liability for rental properties. If these charges are included in the rental agreement, they are typically subject to sales tax. However, if they are separately stated, they may be exempt.

Excavator Rentals: License Requirements and Rules

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![]()

California's sales tax on rentals

California typically taxes rentals and leases, but there are specific sales tax implications that lessors must be aware of, such as how and when the tax is paid. Lessees should also be aware of these details to ensure they are paying the right amount of tax.

In California, the rental or lease of tangible personal property comes with specific sales tax implications. Lessors are given a choice: they can decide to pay sales or use tax based on the initial purchase price of the property, or they can opt to collect and remit use tax from the lessee with each lease payment. It is important to note that selecting both is not allowed.

Additionally, if the rental period is less than 30 days, the tax is due regardless of whether the lessor paid sales or use tax at the time of the original purchase of the property.

If a dealer of mobile transportation equipment makes the sale and delivery within California, the transaction is subject to sales tax unless the lessor makes a timely election to report their tax liability measured by the fair rental value. On the other hand, if the sale and delivery occur outside California and the property is purchased for use in California, use tax will apply measured by the purchase price unless the equipment enters the state in interstate commerce and is used continuously thereafter in interstate commerce, or the lessor makes a timely election to report use tax liability measured by the fair rental value.

It is worth noting that Florida is the only state that levies a standard statewide sales tax on commercial real estate leases, although other states and municipalities have similar taxes that are not as comprehensive as Florida's.

Finding a Community with Affordable Lot Rent

You may want to see also

Frequently asked questions

Florida is the only state that charges sales tax on commercial rent.

The sales tax rate on commercial rent in Florida is 5.5%. However, it is expected to reduce to 4.5% in December 2023 and 2% in mid-2024.

Yes, there may be additional discretionary county surcharges.

Yes, New York City imposes a 6% tax on commercial real estate leases for companies that pay at least $250,000 in rent annually. Hawaii has a 4% general excise tax on income, which includes rental income. Arizona has five cities that impose a tax on commercial real estate leases.

Yes, in 45 states, there is either no sales tax or state law applies only to tangible personal property. Alabama and Arkansas are two states that generally charge sales tax on the rental or lease of tangible personal property unless specific exemptions are met.

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)