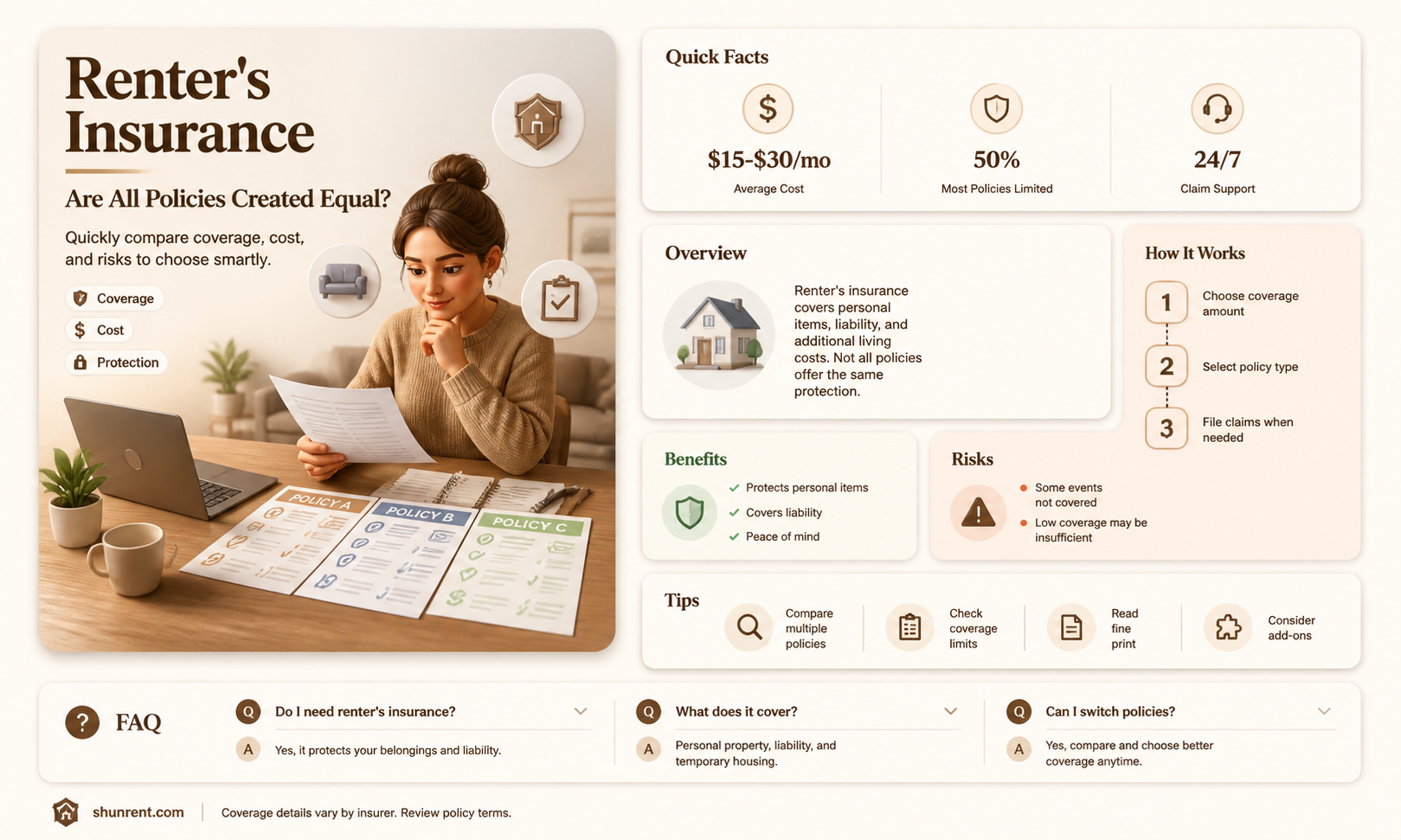

Renter's insurance is an optional insurance policy that tenants can purchase to protect their belongings from theft or damage. While it is not required by law, some landlords may require tenants to have a renter's policy. Basic renter's insurance policies cover a range of items, including electronics, clothing, appliances, and furniture, and can also provide temporary accommodation if the rental property becomes uninhabitable. However, it's important to note that not all renter's insurance policies are the same, and certain types of damage or natural disasters may not be covered. For example, flood insurance is typically not included in a standard policy and must be purchased separately. Additionally, renters may need to purchase extra coverage for high-value items such as jewelry or antiques. Therefore, it is essential for renters to carefully review the terms of their policy and understand what is and isn't covered to ensure they have adequate protection.

| Characteristics | Values |

|---|---|

| Cost | Renter's insurance is usually inexpensive, with the average policy in Texas costing about $20 a month. |

| Coverage | Basic renter's insurance policies cover a range of items, including electronics, clothing, appliances, and furniture. They may also cover additional living expenses and personal liability. |

| Exclusions | Renter's insurance does not cover every type of damage. For example, it may not cover electrical failure or certain natural disasters like hurricanes or floods. |

| Necessity | Renter's insurance is generally optional and not required by law. However, some landlords may require tenants to have a renter's policy. |

| Landlord's Insurance | A landlord's insurance policy does not cover a tenant's personal belongings. |

| Additional Coverage | Tenants can purchase additional coverage for high-value items or specific hazards like earthquakes or floods. |

Explore related products

$41.14 $44.95

$42.35 $55

$44.95 $42.99

What You'll Learn

![]()

Renters insurance is not a requirement by law

While renters insurance can provide valuable protection for tenants and their belongings, it is not a legal requirement. This means that tenants are not legally obligated to obtain renters insurance when renting a property.

However, it is worth noting that while not legally required, renters insurance can offer important financial protection in the event of damage, loss, or liability claims. For example, if a tenant negligently causes property damage or personal injury, their renters insurance could cover the resulting expenses, potentially saving them from significant out-of-pocket costs. Similarly, in the case of theft, fire, smoke damage, or certain types of water damage, renters insurance can provide financial reimbursement for lost or damaged belongings, giving tenants peace of mind.

Additionally, renters insurance can benefit landlords as well. By requiring tenants to have renters insurance as a condition of the lease, landlords can reduce their own liability risks. This is because a tenant's renters insurance policy can cover damages caused by the tenant's negligence, such as kitchen fires or water damage, protecting the landlord from bearing the full financial burden of repairs.

Although renters insurance is not mandated by law, some landlords may require tenants to purchase it as part of the lease agreement. This is a way for landlords to encourage tenants to protect their belongings and minimize potential liabilities. Ultimately, the decision of how much renters insurance to purchase, or whether to purchase it at all, rests with the tenant. However, it is always a good idea to carefully review the terms of a lease agreement and consider the benefits of renters insurance before deciding.

Guarantors: A Must-Have for Renting a Flat?

You may want to see also

Explore related products

![]()

Landlord insurance does not cover your belongings

While every insurance policy is different, landlord insurance generally offers protection for three types of losses. However, it is important to note that landlord insurance does not cover a tenant's personal belongings. This means that if a fire, water damage, or another incident damages or destroys your belongings, you will not be reimbursed unless you have renters insurance.

Landlord insurance is designed to protect the property owner's investment and liability interests. It typically covers the physical structure of the dwelling, any outbuildings, and the landlord's personal property. For example, most policies will cover damage to a garage, shed, or the landlord's appliances provided for the tenant. Landlord insurance may also provide liability coverage if someone is injured on the property. This can help cover legal and medical costs if the landlord is found to be at fault.

On the other hand, renters insurance is designed to protect a tenant's personal belongings. It covers personal property against perils such as fire, theft, or natural disasters. It also offers personal liability protection, which can help cover costs if the tenant is found legally responsible for injury or damage to someone else. Before purchasing renters insurance, it is important to conduct a complete inventory of your belongings and calculate the replacement costs to ensure you have adequate coverage.

While landlord insurance does not cover a tenant's belongings, there may be exceptions. For instance, if the landlord was aware of a hazardous condition, failed to correct it within a reasonable time frame, and as a result, the tenant's property was damaged, the landlord's insurance may cover the tenant's losses. Additionally, in some cases, a landlord may require a tenant to purchase renters insurance as a condition of the lease.

In summary, landlord insurance and renters insurance serve distinct purposes. Landlord insurance protects the property owner's investment and liability, while renters insurance safeguards a tenant's personal possessions. By understanding the scope and limitations of each type of insurance, tenants can ensure they have the necessary coverage to protect their belongings.

How Much is Three Times the Rent?

You may want to see also

Explore related products

![]()

Basic renters insurance covers electronics, clothing, appliances, and furniture

Basic renters insurance covers personal property, including electronics, clothing, appliances, and furniture, in the event of theft, damage, or destruction. It is important to note that a landlord's insurance policy does not cover a tenant's personal belongings. Therefore, renters insurance is essential to protect one's possessions.

While the specifics of renters insurance policies may vary, they generally provide financial reimbursement for covered losses to personal belongings. For example, if a laptop purchased for $1,300 two years ago is now worth $500, a basic renters insurance policy would reimburse the current value of $500 if the laptop was destroyed. This principle applies to other items such as appliances, clothing, and furniture.

Renters insurance typically includes personal liability coverage, which protects against legal and financial consequences if someone is injured on the insured property or if the insured accidentally damages someone else's property. It may also cover additional living expenses, such as temporary housing and groceries, if the insured property becomes uninhabitable due to a covered loss.

It is important to note that renters insurance does not cover damage to the structure of the rented property, as that falls under the landlord's insurance policy. Additionally, certain items with high values, such as jewelry, artwork, and collectibles, may require additional coverage beyond the basic policy.

When considering renters insurance, it is advisable to conduct a comprehensive inventory of personal belongings, including their current values, to ensure adequate coverage. Renters insurance provides peace of mind and financial protection in the event of unforeseen circumstances.

Renting: Ensure You Earn 3x the Asking Price

You may want to see also

Explore related products

$8

![]()

Renters insurance covers personal liability

While renters' insurance policies differ in their coverage, they all typically include personal liability insurance. This type of insurance covers bodily injury to others and damage to others' property. For example, if a visitor trips and falls in your apartment, breaking their wrist, your renters' insurance will likely cover their medical expenses. It is important to note that personal liability insurance does not cover injuries to yourself or damage to your property. Instead, it is designed to protect you from the costs of liability claims made against you. Most personal liability insurance for renters provides a minimum of $100,000 in coverage, and you can often pay a higher premium to increase your coverage limits.

Renters' insurance also typically includes personal property coverage, which protects your belongings from theft or damage. This coverage includes items stolen from your car or while you are travelling. However, it is important to note that there may be limits on payments for certain types of property, such as cash, jewellery, and watches. You may be able to purchase additional coverage for high-value items to ensure they are fully protected.

In addition to personal liability and personal property coverage, renters' insurance may also include additional living expense coverage. This type of coverage pays for extra costs, such as food and rental, if you need to move out of your home temporarily due to covered damages. It is important to note that renters' insurance does not typically cover losses due to floods, and you may need to purchase separate flood insurance to protect against this type of damage.

While renters' insurance is not required by law, some landlords may require tenants to have a policy in place. It is important to carefully review the terms of your renters' insurance policy to understand what is covered and what may be excluded or limited. Conducting a complete inventory of your personal belongings and understanding the replacement costs can help ensure that you have adequate coverage in the event of a loss.

Rent Heavy-Duty Equipment: Construction Solutions at A-1 Rent-Alls

You may want to see also

Explore related products

![]()

Additional coverage for high-value items, floods, and earthquakes

While renters insurance offers essential protection for personal belongings, standard policies do not cover flood damage, earthquakes, or high-value items. As a result, renters may need to purchase additional coverage for these perils.

Floods

Floods are not typically covered by renters insurance and require a separate policy. If you live in an area prone to flooding, consider purchasing flood insurance to protect your belongings from water damage caused by floods.

Earthquakes

Earthquakes are generally excluded from renters insurance policies. If you live in an area prone to earthquakes, you may need to buy additional earthquake insurance to cover the cost of resulting damage. Earthquake insurance can be purchased from insurance companies that are members of the California Earthquake Authority (CEA), which provides most earthquake insurance in California. It's important to note that earthquake insurance does not cover damage to your vehicles or landscaping, pools, fences, or separate buildings.

High-value items

Expensive items such as jewellery, artwork, electronics, and collectibles are typically not fully covered by standard renters insurance policies. To ensure adequate coverage for high-value items, you may need to add a rider or endorsement to your policy. This will increase the limit of coverage for these items and provide peace of mind in the event of a loss.

It's important to carefully review the exclusions and limitations of any renters insurance policy before purchasing. By understanding what is and isn't covered, you can make informed decisions about additional coverage options to ensure your belongings are fully protected.

Exploring the Minimum Age Requirements for Renting with Turo

You may want to see also