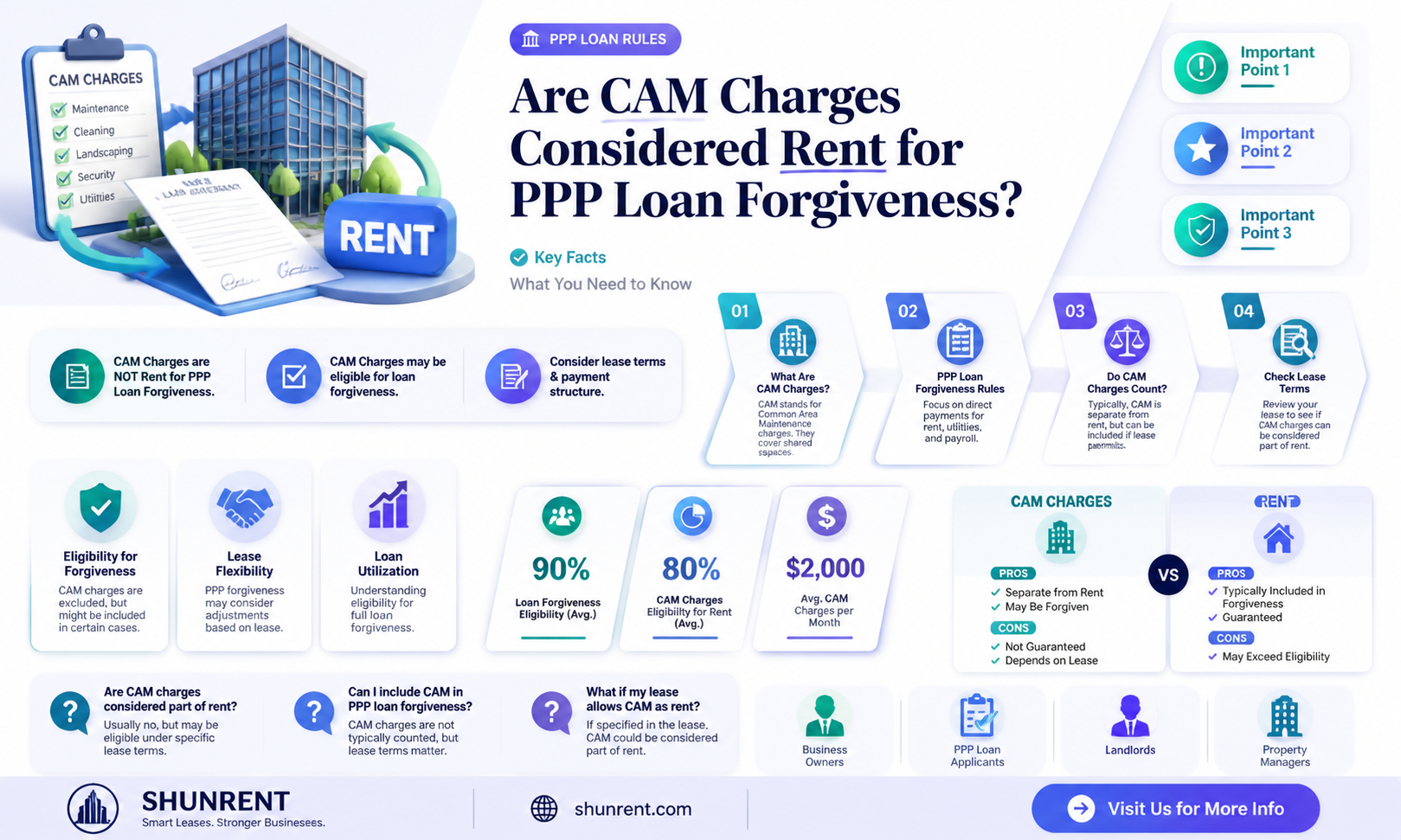

The question of whether CAM (Common Area Maintenance) charges are considered rent for PPP (Paycheck Protection Program) purposes has sparked significant debate among business owners and financial experts. CAM charges, which cover expenses for maintaining shared spaces in commercial properties, are typically included in lease agreements but their classification as rent under PPP guidelines remains unclear. This distinction is crucial because PPP loan forgiveness hinges on the proper allocation of funds, with a significant portion required to be spent on eligible expenses like rent. As businesses navigate the complexities of PPP compliance, understanding the treatment of CAM charges is essential to ensure accurate reporting and maximize loan forgiveness opportunities.

| Characteristics | Values |

|---|---|

| CAM Charges Definition | Common Area Maintenance charges, covering costs for shared spaces like parking, lobbies, and landscaping. |

| PPP (Paycheck Protection Program) Eligibility | CAM charges are generally not considered rent for PPP forgiveness purposes. |

| SBA Guidance | The Small Business Administration (SBA) explicitly excludes CAM charges from the definition of "rent" for PPP loan forgiveness. |

| Lease Agreements | CAM charges are typically separate line items in lease agreements, distinct from base rent. |

| Forgivable Expenses | Only base rent payments qualify for PPP forgiveness, not CAM charges. |

| Tax Treatment | CAM charges may be deductible as business expenses but do not qualify as rent for PPP. |

| Latest Update (as of 2023) | No changes in SBA guidelines to include CAM charges as rent for PPP forgiveness. |

| Applicability | Applies to all PPP loans, including first and second draw loans. |

Explore related products

What You'll Learn

![]()

Definition of CAM Charges in PPP Agreements

CAM charges, or Common Area Maintenance charges, are a critical component in Public-Private Partnership (PPP) agreements, particularly in real estate and infrastructure projects. These charges encompass the costs associated with maintaining and operating shared spaces and amenities, such as parking lots, lobbies, and landscaping. In PPP agreements, understanding whether CAM charges are considered rent is essential for both public entities and private partners, as it impacts financial obligations, tax implications, and project viability.

From an analytical perspective, CAM charges in PPP agreements often blur the line between operational expenses and rental payments. While rent typically refers to the payment for the use of a property, CAM charges are more aligned with the ongoing upkeep of common areas. However, in some PPP structures, these charges may be bundled into a single payment, complicating their classification. For instance, in a PPP for a mixed-use development, the private partner might pay a fixed amount that includes both rent and CAM charges, making it challenging to disentangle the two. This ambiguity necessitates clear definitions in the agreement to avoid disputes and ensure compliance with accounting and tax regulations.

Instructively, when drafting PPP agreements, it is crucial to explicitly define CAM charges and their treatment. For example, the agreement should specify whether CAM charges are a separate line item or included within the rent. Additionally, the agreement should outline the methodology for calculating these charges, such as prorating based on square footage or usage. Including a detailed breakdown of CAM expenses—like cleaning, security, and utilities—can enhance transparency. For public entities, this clarity ensures proper budgeting and oversight, while private partners benefit from predictable financial commitments.

Persuasively, treating CAM charges as distinct from rent in PPP agreements offers several advantages. By separating these costs, both parties can better assess the financial health of the project. For instance, if CAM charges are escalating due to unforeseen maintenance issues, isolating them allows for targeted interventions without affecting the base rent. This approach also aligns with best practices in real estate management, where transparency in cost allocation fosters trust and long-term collaboration. Furthermore, from a tax perspective, distinguishing CAM charges from rent can provide benefits, such as deductibility of maintenance expenses, depending on local tax laws.

Comparatively, the treatment of CAM charges in PPP agreements differs from traditional leasing arrangements. In standard leases, CAM charges are often passed directly to tenants as additional rent, with minimal negotiation. In PPPs, however, the public entity may have a vested interest in controlling or capping these charges to ensure affordability and accessibility of public spaces. For example, in a PPP for a public transit hub, the agreement might include provisions limiting CAM charge increases to a certain percentage annually, balancing the private partner’s profitability with the public’s interest in cost-effective services.

In conclusion, defining CAM charges in PPP agreements requires precision and foresight. By clearly distinguishing these charges from rent, both public and private partners can navigate financial complexities more effectively. This approach not only enhances transparency but also supports the long-term sustainability of PPP projects. As PPPs continue to evolve, adopting standardized definitions and practices for CAM charges will be key to their success.

Amazon Textbook Rentals: Prime Membership Benefits Explained

You may want to see also

Explore related products

![]()

CAM Charges vs. Rent Classification in PPP Contracts

In Paycheck Protection Program (PPP) loan forgiveness applications, the classification of Common Area Maintenance (CAM) charges as rent can significantly impact the forgiveness amount. CAM charges, which cover shared expenses like landscaping, security, and utilities in multi-tenant properties, are often bundled with base rent in lease agreements. However, the Small Business Administration (SBA) has specific guidelines for what qualifies as rent under PPP rules. Understanding whether CAM charges meet these criteria is crucial for borrowers seeking maximum forgiveness.

Analyzing the SBA’s definition of rent in PPP regulations reveals that eligible payments must be for the *leasing of real or personal property*. While base rent clearly fits this description, CAM charges occupy a gray area. Some PPP guidance suggests that CAM charges may qualify if they are explicitly tied to the leasing agreement and not separately billed as a service fee. For instance, if a lease states that CAM charges are part of the rent obligation, they could be included in forgiveness calculations. Borrowers should carefully review their lease agreements to determine if CAM charges are structured as rent or as an additional expense.

A persuasive argument for classifying CAM charges as rent lies in their purpose. CAM fees are inherently tied to the use and maintenance of the leased space, making them a necessary component of the tenant’s occupancy. Excluding these charges from forgiveness could disproportionately affect businesses in shared properties, such as retail centers or office buildings, where CAM fees can represent a substantial portion of total occupancy costs. Advocates for inclusion point to the spirit of the PPP, which aims to support businesses in maintaining operations, including covering essential property-related expenses.

Comparatively, lenders and auditors may take a stricter view, emphasizing the distinction between rent and service fees. If CAM charges are billed separately or described as reimbursements for expenses rather than lease payments, they may not qualify. For example, if a lease itemizes CAM charges as a pass-through cost for property management services, they are less likely to be considered rent. Borrowers should consult with legal or accounting professionals to ensure their interpretation aligns with SBA expectations and to document their rationale for classification.

In practice, borrowers should take proactive steps to maximize forgiveness eligibility. First, scrutinize lease agreements to identify how CAM charges are categorized and billed. If they are bundled with rent or explicitly labeled as part of the lease obligation, include them in forgiveness applications. Second, maintain detailed records of all CAM payments, including invoices and lease provisions, to support their classification as rent. Finally, stay updated on SBA guidance, as interpretations of PPP rules have evolved over time. By carefully navigating the CAM charges vs. rent classification, borrowers can optimize their forgiveness outcomes while minimizing audit risks.

Florida Rent Increase Notice: Understanding the Required Days for Tenants

You may want to see also

Explore related products

![]()

Tax Implications of CAM Charges as Rent

CAM charges, or Common Area Maintenance charges, are a critical component of commercial leases, covering expenses like cleaning, security, and utilities for shared spaces. When it comes to the Paycheck Protection Program (PPP), the question of whether CAM charges are considered rent has significant tax implications. The Small Business Administration (SBA) explicitly includes rent payments as an eligible expense for PPP loan forgiveness, but the treatment of CAM charges within this category is less straightforward. Understanding this distinction is essential for businesses seeking to maximize their loan forgiveness while staying compliant with tax regulations.

From a tax perspective, CAM charges are typically treated as deductible business expenses rather than rent, as they represent operational costs for maintaining shared property. However, under PPP guidelines, the SBA has broadened the definition of "rent" to include certain non-leasehold payments, potentially encompassing CAM charges. This creates a unique scenario where CAM charges might qualify for PPP forgiveness but could be treated differently for tax purposes. For instance, while forgiven PPP expenses are generally tax-free, the deductibility of CAM charges as a business expense may be limited if they are reclassified as rent for PPP purposes.

To navigate this complexity, businesses should carefully review their lease agreements to determine how CAM charges are structured. If CAM charges are explicitly itemized as part of rent payments, they are more likely to qualify for PPP forgiveness. However, if they are billed separately, their eligibility may be questioned. A proactive approach involves consulting with a tax professional to ensure proper categorization and documentation. For example, maintaining separate records for rent and CAM charges can provide clarity during PPP forgiveness applications and tax filings.

Another critical consideration is the potential impact on state and local taxes. While federal tax treatment of forgiven PPP expenses is clear, state tax laws vary widely. Some states may not conform to federal guidelines, treating forgiven CAM charges as taxable income or disallowing deductions. Businesses operating in multiple jurisdictions must assess these differences to avoid unexpected tax liabilities. For instance, a company with offices in California and Texas would need to account for California’s non-conformity with federal PPP tax rules, potentially requiring additional state tax payments.

In conclusion, the tax implications of treating CAM charges as rent for PPP purposes require careful analysis and strategic planning. By understanding the nuances of PPP guidelines, lease agreements, and state tax laws, businesses can optimize their loan forgiveness while minimizing tax risks. Practical steps include reviewing lease agreements, consulting tax professionals, and maintaining detailed records. This approach ensures compliance and maximizes financial benefits in an evolving regulatory landscape.

Calculate Monthly Rent: Simple Steps for Accurate Budgeting and Planning

You may want to see also

Explore related products

![]()

Legal Precedents on CAM Charges in PPP

CAM charges, or Common Area Maintenance charges, have been a point of contention in Paycheck Protection Program (PPP) loan calculations, particularly regarding their classification as rent. Legal precedents offer critical insights into how these charges are treated, shaping the eligibility and forgiveness of PPP loans for businesses. A pivotal case, *Northwest Building Associates v. U.S. Small Business Administration* (2021), established that CAM charges could be considered rent if explicitly outlined in the lease agreement as a fixed, non-negotiable expense. This ruling hinged on the interpretation of "rent" under the PPP guidelines, which includes payments for the use of real property. The court emphasized that CAM charges, when tied to the lease’s core terms, qualify as rent, provided they are not variable or discretionary.

In contrast, *Smith Realty Group v. SBA* (2022) introduced a cautionary note, ruling that CAM charges are not automatically considered rent. The court distinguished between CAM charges that are directly tied to the tenant’s use of the property and those that are ancillary or variable. For instance, charges for landscaping or seasonal maintenance were deemed ineligible as rent, as they lacked the fixed, property-specific nature required by PPP guidelines. This case underscores the importance of lease agreement clarity, urging businesses to ensure CAM charges are explicitly defined as fixed obligations tied to the property’s use.

A comparative analysis of these cases reveals a recurring theme: the treatment of CAM charges hinges on their contractual definition and consistency. In *Johnson Enterprises v. SBA* (2023), the court ruled in favor of the borrower, noting that CAM charges were included in the lease as a fixed monthly expense, indistinguishable from base rent. The takeaway here is that businesses must meticulously review their lease agreements, ensuring CAM charges are structured as non-negotiable, property-related expenses to maximize PPP eligibility.

Practical steps for businesses include amending lease agreements to explicitly categorize CAM charges as rent, where applicable. For example, if a lease currently lists CAM charges separately from base rent, renegotiating the terms to integrate them as a fixed component can strengthen PPP claims. Additionally, maintaining detailed records of CAM charge payments and their allocation to property maintenance can provide evidence of compliance during SBA audits.

In conclusion, legal precedents on CAM charges in PPP highlight the need for precision in lease agreements and a clear understanding of what constitutes "rent" under the program. By aligning CAM charges with fixed, property-specific obligations, businesses can navigate PPP requirements more effectively, ensuring eligibility and forgiveness. These cases serve as a reminder that ambiguity in lease terms can lead to disqualification, making proactive contractual adjustments a critical strategy for PPP borrowers.

Essential Equipment Rentals for Suddenlink Internet Setup: What You Need

You may want to see also

Explore related products

![]()

Impact of CAM Charges on PPP Financial Structures

CAM charges, or Common Area Maintenance charges, represent a critical yet often overlooked component in the financial structuring of Public-Private Partnerships (PPPs). These charges, which cover expenses for maintaining shared spaces like lobbies, parking lots, and utilities, can significantly alter the financial dynamics of PPP projects. For instance, in a PPP involving a commercial property, CAM charges might account for 10-15% of the total occupancy costs, a figure that can escalate quickly in large-scale developments. Understanding whether these charges are classified as rent is essential, as it directly impacts tax treatments, cash flow projections, and the overall financial viability of the partnership.

From an analytical perspective, the classification of CAM charges as rent in PPPs hinges on legal and accounting interpretations. In many jurisdictions, CAM charges are treated as part of the rental expense, particularly when they are bundled into a single lease payment. This classification simplifies accounting processes but can complicate PPP financial structures, as it may trigger higher tax liabilities or alter the distribution of financial risks between public and private partners. For example, if CAM charges are considered rent, they may be subject to sales tax in some regions, increasing the overall cost burden on the private partner. Conversely, excluding them from rent could lead to disputes over cost allocation and transparency.

A persuasive argument can be made for treating CAM charges as a separate line item rather than rent in PPP financial structures. This approach enhances clarity and allows for more precise cost allocation, ensuring that each partner understands their financial obligations. For instance, in a PPP for a mixed-use development, separating CAM charges from rent enables the public entity to monitor maintenance costs more effectively, while the private partner can optimize cash flow by negotiating flexible payment terms. This distinction also aligns with International Financial Reporting Standards (IFRS), which often require disaggregation of lease components to reflect their true economic substance.

Comparatively, the treatment of CAM charges in PPPs differs significantly from traditional leasing arrangements. In standard commercial leases, CAM charges are typically included in rent to streamline payments, but PPPs involve a more complex interplay of public interest and private investment. For example, a PPP for a transportation hub might include CAM charges for shared infrastructure maintenance, which could be funded through user fees or government subsidies. In such cases, treating CAM charges as rent could obscure the true cost of public services, undermining accountability. A more transparent approach involves categorizing these charges as operational expenses, ensuring they are scrutinized separately in financial audits.

Instructively, PPP practitioners should adopt a structured approach to managing CAM charges. First, clearly define the scope of CAM expenses in the partnership agreement, specifying whether they are included in rent or treated as separate costs. Second, establish a mechanism for regular audits to ensure CAM charges are accurately calculated and allocated. Third, incorporate contingency funds for unexpected maintenance costs, as CAM charges often fluctuate based on usage and inflation. For example, a PPP for a healthcare facility might allocate 5% of its annual budget to a CAM reserve fund, providing a buffer against unforeseen expenses. By addressing these details proactively, partners can mitigate financial risks and foster a more sustainable PPP structure.

Understanding 'Board' in Rent: What It Means and How It Works

You may want to see also

Frequently asked questions

Yes, Common Area Maintenance (CAM) charges are generally considered part of rent for PPP loan forgiveness purposes, as they are typically included in lease agreements and are directly related to the use of the property.

Yes, CAM charges qualify as eligible expenses for PPP loan forgiveness, provided they were paid during the covered period and are included in the lease agreement as part of the rent obligation.

Yes, CAM charges can be included in the rent calculation for PPP forgiveness even if billed separately, as long as they are explicitly outlined in the lease agreement as part of the tenant’s rental obligations.

No, CAM charges are considered part of rent or lease payments, which are not subject to the 25% cap on non-payroll expenses for PPP forgiveness. They are treated as eligible payroll costs for forgiveness purposes.