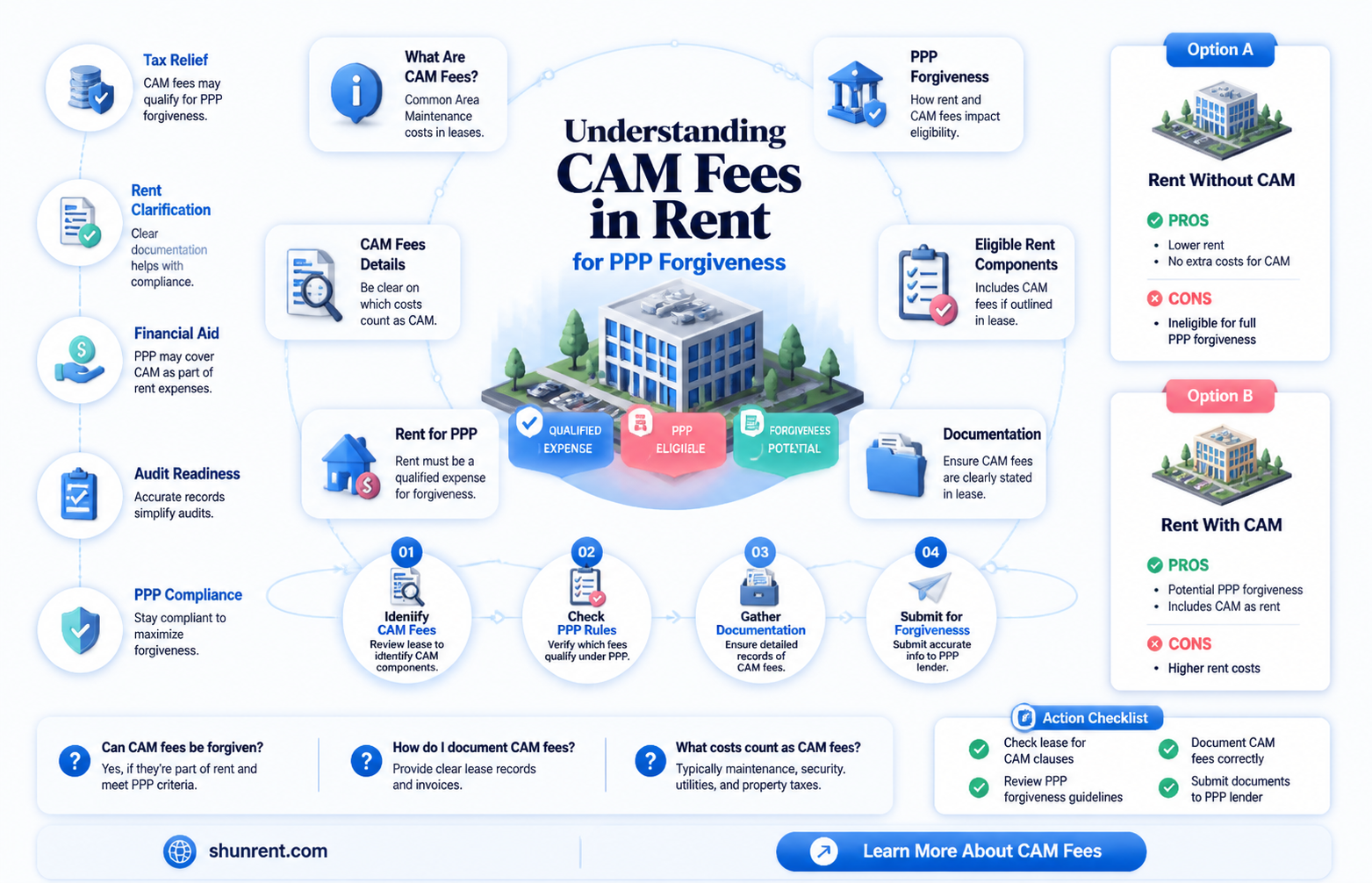

The US Small Business Administration (SBA) has issued guidance on PPP loan forgiveness, answering some key questions. However, there are still open questions, including whether CAM fees are included as part of rent. The SBA's platform for accepting PPP loan forgiveness applications requires no additional documentation, but it is recommended that borrowers keep relevant documents on hand. The SBA also confirmed that payroll incurred and paid during the covered period is eligible for forgiveness.

| Characteristics | Values |

|---|---|

| Are CAM fees part of rent for PPP forgiveness? | No clear answer found. However, CAM charges and rental payments under a lease are forgivable expenses. |

| What are the requirements for PPP loan forgiveness? | The SBA requires borrowers to provide additional documentation upon forgiveness submission. |

| What is the process for applying for PPP loan forgiveness? | Borrowers must submit an application through the SBA direct forgiveness portal or their lender. |

| What are the eligible expenses for PPP loan forgiveness? | Payroll costs, business mortgage interest, business rent or lease payments, business utility payments, covered operations expenditures, transportation expenses, and fuel for business vehicles. |

| What is the timeline for PPP loan forgiveness? | Borrowers have up to 10 months after the last day of the covered period to apply for PPP loan forgiveness; otherwise, loan payments are no longer deferred. |

Explore related products

What You'll Learn

![]()

What are PPP loans?

The Paycheck Protection Program (PPP) was established by the CARES Act and is implemented by the Small Business Administration with support from the Department of the Treasury. PPP loans are intended to provide economic relief to small businesses, individuals who are self-employed, independent contractors, and private non-profit organisations that are currently experiencing a temporary loss of revenue as a result of the COVID-19 pandemic. The program provides funds to pay up to 8 weeks of payroll costs, including benefits. The amount of the PPP loan is based on the applicant's payroll costs, including salaries, wages, commissions, cash tips, paid leave, severance pay, and other compensation paid to employees. These costs are limited to $100,000 annualised per employee.

PPP loans are free to apply for and are accepted, approved, and disbursed on a first-come, first-served basis until the funds are depleted. The loan amount is equal to 2.5 times the average monthly payroll costs. Each PPP loan may not exceed $10 million, and no payments are required until the forgiveness amount is remitted to the lender. Interest accrues at 1% from the loan date until any unforgiven amount is paid.

The SBA also provides guidance on calculating loan forgiveness, including the Alternative Payroll Covered Period, which allows borrowers to synchronise their covered period for payroll cost purposes with their biweekly payroll period. Additionally, the SBA has confirmed that gross cash compensation, including bonuses, hazard pay, tips, and commissions, are within the definition of cash compensation, all subject to the $100,000 limit per employee.

While the specific inclusion of CAM fees as part of rent for PPP forgiveness is not explicitly mentioned, the SBA has provided some clarification on eligible expenses. For example, transportation expenses seem to be limited to utility transportation distribution fees and business vehicle fuel. Similarly, leases in place before February 15, 2020, that renew after that date are deemed extensions of the previous lease, and rental payments under that lease are forgivable expenses.

Renting in San Diego: Average Costs Explored

You may want to see also

Explore related products

![]()

What is the process for PPP loan forgiveness?

The Paycheck Protection Program (PPP) was a federal program that provided $793 billion in small business loans during the COVID-19 pandemic. The PPP Act allowed for much of this money to be forgiven, meaning that businesses that received loans would not have to pay them back. The program ended on May 31, 2021, and since then, 10.5 million loans worth $755 billion have been forgiven.

If your business received a PPP loan and you have not yet applied for forgiveness, you can still do so. There are, however, limitations on what expenses can be forgiven, but most companies will be able to write off at least some of their PPP debt. To qualify for full forgiveness, your business must have maintained staffing and compensation levels throughout the covered period, and the loan money must have been spent on eligible expenses. These include:

- Payroll costs: At least 60% of your PPP loan must have been spent on payroll, including wages, commissions, bonuses, insurance payments, and retirement payments made on behalf of your employees.

- Operating costs: This includes mortgage payments, rent, software, and utility bills.

To apply for forgiveness, you can visit the SBA's PPP Direct Forgiveness Portal and fill out SBA Form 3508S if your loan was for $150,000 or less. You don't need to explain how you spent the funds, and if it's your first loan, you don't need to submit any further documentation. If you have a second-draw loan, you'll need to prove that you lost revenue. You can also apply for loan forgiveness via your lender, and if your loan was for more than $150,000, this is the only way to apply. Your lender will be able to inform you about the loan forgiveness application process and any additional documentation that may be required.

It's important to note that if you don't apply for forgiveness within 10 months after the last day of the covered period, PPP loan payments are no longer deferred, and you will need to start making loan payments to your PPP lender.

Renting Smart: How Much of Your Income?

You may want to see also

Explore related products

![Adams Notice to Pay Rent or Vacate, Forms and Instructions [Print and Downloadable] (LF280), White](https://m.media-amazon.com/images/I/81FvibdeL4L._AC_UL320_.jpg)

![]()

What is the timeline for PPP loan forgiveness?

The timeline for PPP loan forgiveness varies depending on the borrower's circumstances and the specific loan in question. Here is a detailed breakdown of the timeline:

Application for Forgiveness

Borrowers can apply for PPP loan forgiveness at any time up to five years from the date the SBA issued the loan number. The application process can be done through the SBA's direct forgiveness portal or directly through the borrower's lender. The application process is expected to take around 15 minutes. It is the borrower's responsibility to provide accurate calculations of the loan forgiveness amount, and lenders are expected to review these calculations and supporting documents.

Covered Period

The covered period refers to the time during which PPP loan recipients can spend the funds. For loans made on or after June 5, the covered period is 24 weeks. Borrowers who received loans before June 5 can choose an eight-week covered period.

Deferment of Payments

No payments on PPP loans are required until the forgiveness amount is remitted to the lender by the SBA, assuming the application is filed within 10 months of the completion of the covered period. If borrowers do not apply for forgiveness within this 10-month period, PPP loan payments are no longer deferred, and borrowers must begin making loan payments.

Early Application

PPP recipients can apply for loan forgiveness early, but doing so may have financial implications. Early applicants forfeit a safe-harbor provision that allows them to restore salaries or wages by December 31 and avoid reductions in loan forgiveness.

Salvation Army Rent Assistance: How to Apply

You may want to see also

Explore related products

![]()

What are CAM charges?

CAM, or Common Area Maintenance, refers to the fees incurred by tenants on top of their base rent. These fees are paid to the landlord of a commercial property and are used to cover routine charges to maintain the shared spaces of a given property. In other words, they are the maintenance expenses incurred for work on the common area of a property. For example, in an office park, tenants will pay CAM for gardening services.

CAM charges can be either fixed or variable. They can be influenced by the type of lease signed between the landlord and the tenant. For instance, gross leases are typically considered 'all-inclusive', meaning the property owner is responsible for almost everything, and the tenant does not pay CAM fees. On the other hand, triple net (NNN) leases place responsibility for almost all costs with the tenant, meaning they will pay their full share of CAM charges. Double net (NN) leases are somewhere in the middle, meaning the tenant will likely pay some CAM fees but not as much as a triple net lease tenant.

CAM charges can be broken down into two subcategories: controllable and uncontrollable. Uncontrollable CAM charges include taxes, security costs, utilities, and snow removal expenses—these are outside the property owner's control and unpredictable. Controllable charges are those that the property owner has direct influence over, such as administrative costs and staff payroll. In certain leases, CAM charges may also include administrative and management fees.

The calculation of CAM charges is based on the amount of space occupied by the tenant, with larger spaces incurring higher CAM charges. Each tenant pays their pro rata share of a property's total CAM charges, which is the percentage of the tenant's rented square footage of the total rentable square footage of the property.

CAM charges are subject to variations and may increase by a specific amount each year. However, there is often a price cap to protect tenants from excessive increases, and this cap is negotiated between the tenant and landlord.

Renting a Wheelchair: Daily Options

You may want to see also

Explore related products

![]()

What expenses are forgivable?

The US Small Business Administration (SBA) has provided some guidance on forgivable expenses for PPP loan forgiveness. Firstly, it is important to note that if borrowers do not apply for forgiveness within 10 months of the completion of the covered period, PPP loan payments will no longer be deferred, and borrowers will have to start making loan payments.

Regarding specific expenses, the SBA has outlined that forgivable transportation expenses include utility transportation distribution fees assessed by state and local governments, as well as fuel for business vehicles. For business mortgage interest payments to be forgiven, borrowers must provide a copy of the lender amortization schedule, along with receipts or lender account statements verifying payments. Business rent or lease payments may be forgiven, and borrowers will need to provide a copy of the current lease agreement and receipts, cancelled checks, or other verification of eligible payments. There is some ambiguity regarding leases that include CAM charges; it is unclear whether these qualify for forgiveness.

Additionally, eligible business utility payments, covered operations expenditures, and employer contributions to employee health insurance and retirement plans may be forgiven. To qualify, borrowers must provide copies of invoices, receipts, cancelled checks, or account statements. When calculating cash compensation, the SBA has confirmed that the gross amount is utilized, and compensation such as bonuses, hazard pay, tips, and commissions are included, up to $100,000 per employee annually. The definition of eligible owner compensation varies depending on the type of business entity.

The SBA also provides an EZ loan forgiveness application for sole proprietors, the self-employed, and independent contractor borrowers without employees. This streamlined process does not require additional documentation upon submission, although borrowers may be asked to provide relevant documentation during the loan review or audit processes.

The Wage-Rent Conundrum: Why Are They So Mismatched?

You may want to see also

Frequently asked questions

PPP loan forgiveness refers to the U.S. Small Business Administration's Paycheck Protection Program, which allows eligible borrowers to apply for loan forgiveness.

The process for PPP loan forgiveness involves submitting a loan forgiveness application, providing relevant documentation, and meeting certain conditions and deadlines.

It is not entirely clear if CAM fees are included, as this is an open question. However, rent or lease payments are forgivable expenses under PPP loan forgiveness.

Expenses covered include payroll, business mortgage interest, business rent or lease payments, business utility payments, and covered operations expenditures.

Borrowers must apply for forgiveness within 10 months after the last day of the covered period. The SBA then has up to 5 months to remit the forgiveness amount to the lender.