The age-old question of how much one should spend on rent has many answers. The most popular guideline is the 30% rule, which recommends spending 30% of your gross monthly income on rent. However, this rule has been criticised as outdated and irrelevant, especially in cities with high rent prices, such as New York City or San Francisco. Other guidelines include the 50/30/20 budget, which allocates 50% of your income to needs, 30% to wants, and 20% to savings and debt payments. Ultimately, the proportion of income spent on rent depends on individual circumstances, such as income level, location, and lifestyle choices.

| Characteristics | Values |

|---|---|

| Popular guideline | 30% rule |

| What it means | Spend about 30% of gross income on rent |

| Who uses it | Renters, landlords, mortgage lenders |

| Alternative guideline | 50/30/20 budget |

| 50/30/20 budget breakdown | 50% for needs, 30% for wants, 20% for savings and additional debt payments |

| Average apartment rent | $1,749 |

| Average rent in New York City | Over $3,000 for a one-bedroom apartment |

| Average rent in San Francisco | Over $3,000 for a one-bedroom apartment |

| Reduced costs | Transportation costs |

| Risks of spending 40% on rent | May not be able to save for retirement, student loan payments, etc. |

Explore related products

![]()

The 30% rule

The rule originated in 1969, when public housing regulations capped public housing rent at 25% of a tenant's annual income, which increased to 30% in the early 1980s. While it is a useful guideline, it is not a one-size-fits-all solution. For example, in areas with a high cost of living, such as New York City or San Francisco, sticking to the 30% rule may not be feasible. Similarly, if you live in an affordable area, you may find a good deal on rent that is only 18% of your income, and you should not pass it up just to stick to the 30% rule.

Instead of blindly following the 30% rule, it is recommended to create a realistic budget that is tailored to your specific needs and financial situation. This may involve tracking your monthly expenses and income to determine how much money you can allocate towards rent while still meeting your other financial goals and obligations.

Additionally, sharing the costs of a rental with roommates can help reduce overall housing expenses, allowing individuals to stay within the 30% guideline or allocate more of their budget to other financial priorities.

Eviction in Florida: What Renters Need to Know

You may want to see also

Explore related products

![]()

Location

The location of your rental property is a key factor in determining how much of your income you should spend on rent.

The general rule of thumb is that no more than 30% of your gross monthly income should be spent on rent. However, this rule may not always be feasible depending on the location. For example, in cities like New York, San Francisco, and Toronto, rents are well over $3000 for a one-bedroom apartment, which may exceed the 30% threshold for many individuals.

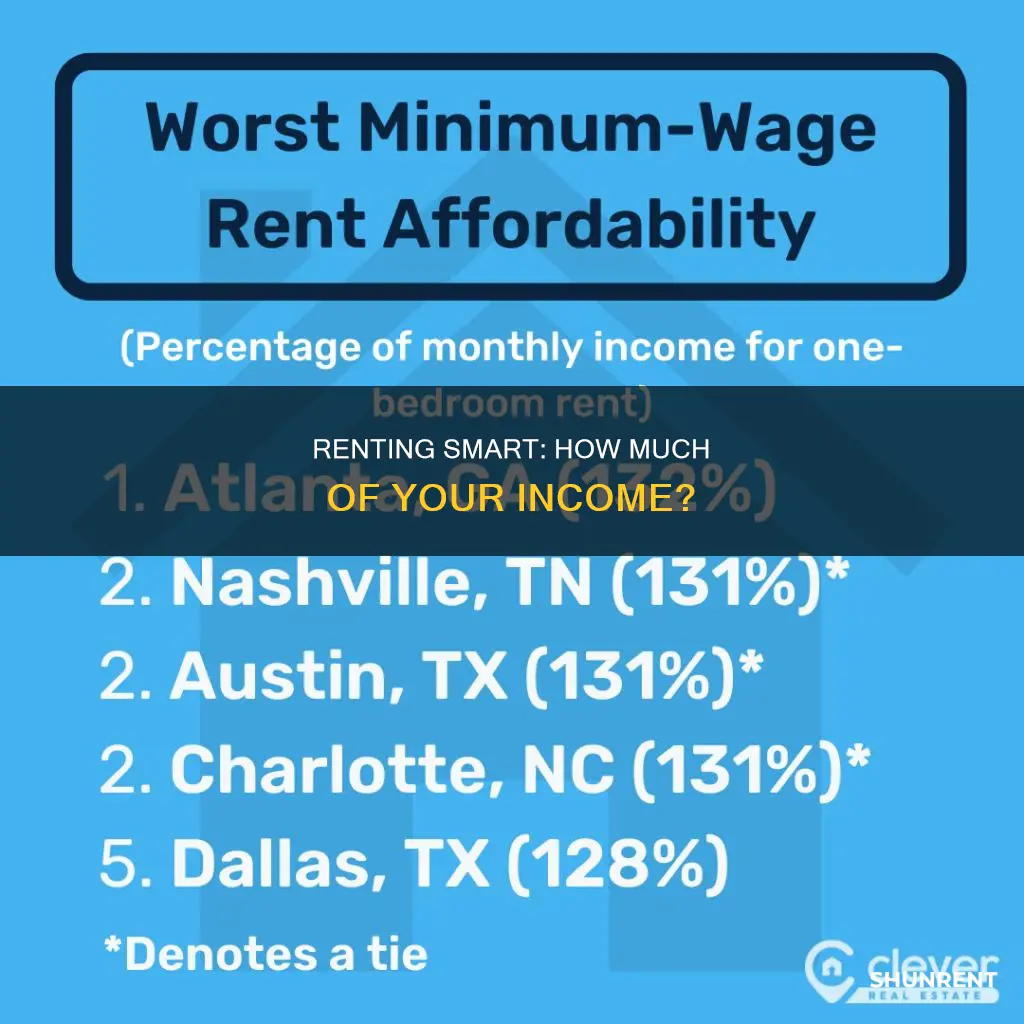

In high-cost cities, the rent-to-income ratio can be significantly higher than 30%. For instance, in Miami, renters may spend more than 54.9% of their income on rent. On the other hand, in more affordable locations, such as Knoxville, renters may only spend around 8.2% of their income on rent.

Your personal circumstances and financial goals should also be considered when deciding on a rental property. If you prioritize a safer neighbourhood, a convenient location, or unique amenities, you may be willing to spend a higher proportion of your income on rent.

Additionally, it's important to consider other expenses and goals when determining your budget. The 50/30/20 budget is a popular alternative guideline, where 50% of your income is allocated to needs (including rent, utilities, and groceries), 30% to wants, and 20% to savings and debt repayment.

In summary, while the 30% rule is a widely accepted guideline, the ideal rent-to-income ratio varies depending on the location and your individual circumstances. It's crucial to carefully weigh your financial situation, outstanding debts, lifestyle needs, and other factors to make informed decisions about your rental budget.

Rent-to-Own Homes: Understanding the Process in Colorado

You may want to see also

Explore related products

![]()

Lifestyle

When it comes to lifestyle, there are several factors to consider when deciding how much of your income to allocate to rent.

Firstly, your lifestyle choices and personal preferences will play a significant role in determining your rental budget. If you prioritize having a large apartment or house, you may be comfortable spending more on rent, even if it means cutting back on other expenses such as dining out, entertainment, or travel. On the other hand, if you prefer to spend more on leisure activities, you may opt for a smaller or less expensive rental to free up funds for these pursuits.

Secondly, your location will impact your rental costs. If you live in an area with a high cost of living, such as a city centre, you may need to allocate a larger portion of your income to rent. For example, in places like New York City or San Francisco, rents can exceed $3,000 per month for a one-bedroom apartment, making it challenging to adhere to the 30% rule. Conversely, if you live in an affordable area, you may find rentals that fit comfortably within a lower percentage of your income, such as 18%.

Thirdly, consider the trade-off between rental costs and other expenses. Choosing a more expensive apartment that is closer to work or school can reduce commuting costs and save time. Opting for a safer neighbourhood or one with better amenities may be worth the extra money for your peace of mind and overall quality of life. Additionally, if you live in an area with good public transportation, you may be able to allocate more of your budget to rent and less to transportation costs.

Lastly, it's important to weigh your current financial situation and goals. If you have outstanding debts, you may want to prioritize paying those off before committing a larger portion of your income to rent. Additionally, consider your savings goals and retirement plans. While the 30% rule is a common guideline, it may not be feasible for everyone, and you may need to adjust it based on your unique circumstances.

In conclusion, when deciding how much of your income to spend on rent, carefully consider your lifestyle choices, location, financial situation, and goals. Remember that the 30% rule is just a starting point, and you may need to adapt it to fit your individual needs and preferences. Finding the right balance between rental costs and other expenses will help you achieve a comfortable and fulfilling lifestyle.

Chapel Hickory Hills Apts: Available to Rent Now

You may want to see also

Explore related products

![]()

Additional housing costs

When deciding how much of your income should go towards rent, it is important to consider additional housing costs. These costs can include utilities, groceries, insurance, transportation, and debt payments.

One way to account for these additional costs is to use the 50/30/20 budget rule. This rule suggests allocating 50% of your take-home pay (after taxes) to needs, which can include rent, utilities, groceries, insurance, and minimum debt payments. The remaining 30% is for wants, and the final 20% is for savings and additional debt payments.

For example, if you earn $4,000 per month after taxes, you would allocate $2,000 for needs. However, if your rent is $1,120 per month, this leaves only $880 for other needs, which may not be enough. In this case, you may need to consider alternative housing options or look for ways to increase your income.

Another option is to use a rent affordability calculator, which can help you determine how much rent you can afford based on your income and other expenses. These calculators allow you to input your gross monthly income and the percentage you want to spend on housing, and they will provide a suggested budget.

Additionally, sharing the costs of a rental with roommates can help reduce overall housing expenses. This option may be especially beneficial if you are willing to compromise on space or location to save money.

It is also important to consider your location and lifestyle when budgeting for additional housing costs. For example, if you live in a city with good public transportation, you may be able to reduce your transportation costs. Alternatively, if you live in an expensive market, you may need to allocate a larger portion of your income to housing.

In conclusion, when determining how much of your income should be spent on rent, it is crucial to consider additional housing costs and your unique circumstances. This may include using budget rules, rent calculators, or sharing costs with roommates to ensure your housing needs are met within your financial capabilities.

Excavator Rentals: License Requirements and Rules

You may want to see also

Explore related products

![]()

The 50/30/20 rule

For example, if your monthly take-home pay is $4,000, you would allocate $2,000 for essential living expenses and minimum debt payments. This includes rent, utilities, groceries, insurance, and other needs. The 30%, or $1,200, is for your "wants", such as clothing, dining out, and entertainment. The final 20%, or $800, is for savings and additional debt payments.

Additionally, the location of your rental property can impact the feasibility of the 50/30/20 rule. In expensive cities like New York or San Francisco, where rents are well over $3,000 for a one-bedroom apartment, sticking to the 30% guideline may not be realistic. In such cases, you may need to consider alternative options, such as finding roommates to share the costs or choosing a less expensive neighbourhood.

It's important to remember that budgets are guidelines rather than strict rules. Your specific circumstances, such as income, cost of living, and other financial goals, will determine the best approach for allocating your income towards rent and other expenses.

Renting Near USC: A Guide to 9-Month Leases

You may want to see also

Frequently asked questions

The 30% rule is a popular guideline that states that no more than 30% of your gross monthly income should be spent on rent. However, this rule may not work for everyone.

The 30% rule is an antiquated benchmark with a one-size-fits-all approach. It does not take into account other expenses such as student loans, retirement savings, debt, child care, etc. It may also not be feasible in expensive cities.

One alternative is the 50/30/20 rule, which allocates 50% of your income to needs (rent, utilities, etc.), 30% to wants, and 20% to savings and debt payments. Another alternative is to create a realistic budget that's specific to your needs and consider alternative housing options.