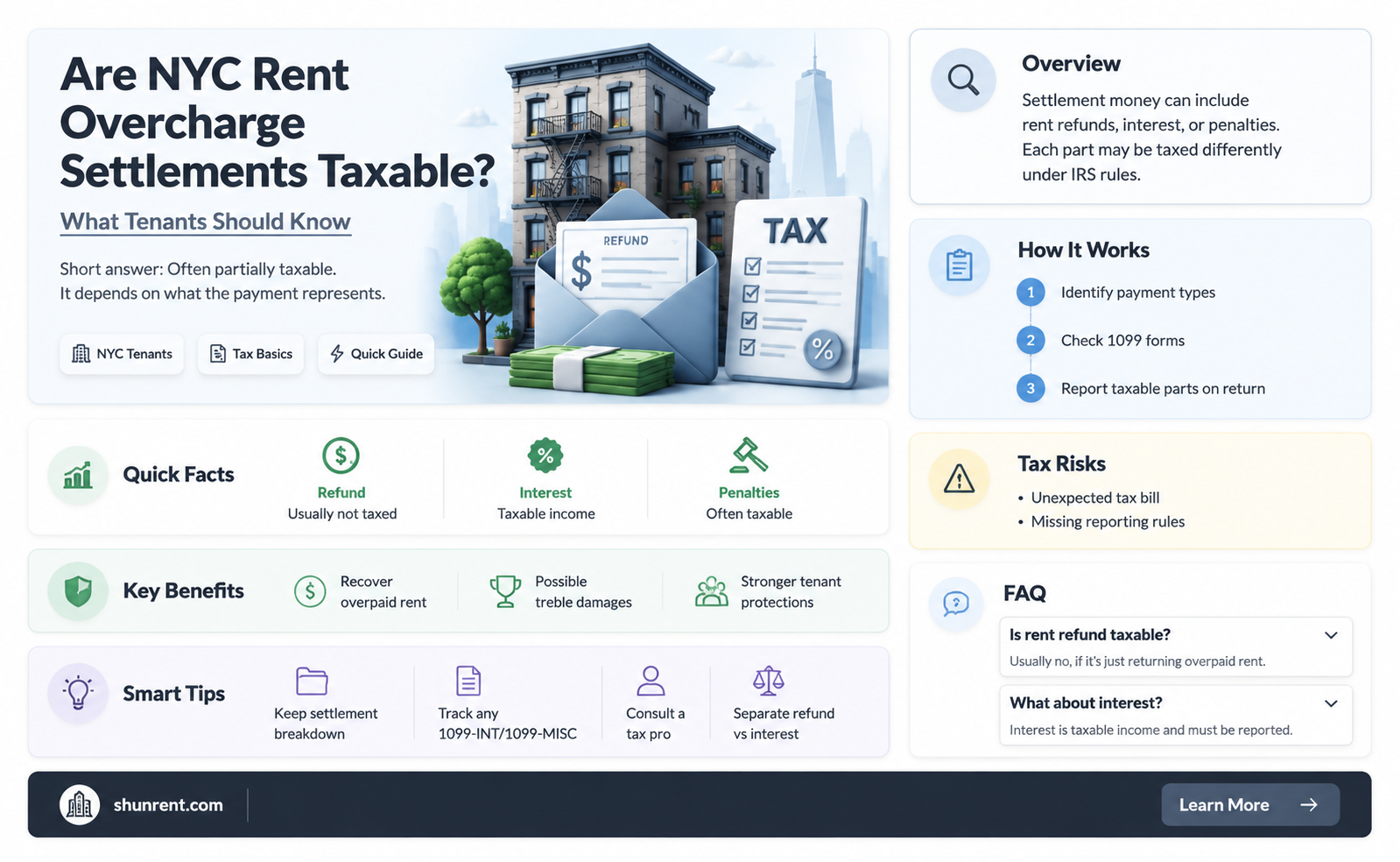

In New York City, the question of whether rent overcharge settlements are taxable is a nuanced issue that intersects landlord-tenant law and tax regulations. When tenants successfully challenge rent overcharges, they may receive settlements from their landlords, which can include refunds for excessive rent paid. However, the tax implications of these settlements are not always clear. Under federal and state tax laws, settlements are generally considered taxable income unless they qualify for specific exemptions, such as restitution for lost property or physical injuries. In the context of rent overcharge settlements, the IRS and New York State Department of Taxation and Finance may treat these payments as taxable income, depending on the nature of the settlement and how it is classified. Tenants and landlords alike must carefully review the terms of the settlement and consult tax professionals to ensure compliance with applicable laws and avoid potential penalties.

| Characteristics | Values |

|---|---|

| Taxability of Rent Overcharge Settlements in NYC | Generally taxable as ordinary income under federal and state tax laws. |

| IRS Classification | Treated as "other income" (Form 1040, Line 21) unless specific exceptions apply. |

| NY State Tax Treatment | Follows federal guidelines; taxable unless exempt under specific provisions. |

| Exceptions | Settlements for emotional distress or physical injuries may be non-taxable. |

| Documentation Required | IRS Form 1099-MISC may be issued if the settlement exceeds $600. |

| Tenant Responsibility | Tenants must report taxable settlements on their tax returns. |

| Landlord Responsibility | Landlords may need to report and withhold taxes if applicable. |

| Legal Advice Recommendation | Consult a tax professional or attorney for case-specific guidance. |

| Relevant Laws | IRS Code, NY Tax Law, and NYC Rent Stabilization Code. |

| Recent Updates | No significant changes as of latest data (October 2023). |

Explore related products

What You'll Learn

![]()

NYC Rent Overcharge Laws

In New York City, rent overcharge claims are governed by the Rent Stabilization Law (RSL) and the Rent Control Law, which protect tenants from excessive rent increases. When a tenant suspects they’ve been overcharged, they can file a complaint with the New York State Division of Housing and Community Renewal (DHCR). If the DHCR finds in the tenant’s favor, the landlord may be required to refund the overcharged amount, often with interest, and adjust the rent to the legal rate. But what happens to these settlements tax-wise? The IRS and New York State Department of Taxation and Finance treat rent overcharge refunds differently depending on their nature. Generally, refunds of rent overpayments are not considered taxable income because they represent a return of money that was never rightfully the landlord’s to keep. However, if the settlement includes additional compensation, such as damages for harassment or legal fees, those amounts may be taxable.

Analyzing the tax implications requires distinguishing between restitution and income. Restitution, which includes rent overcharge refunds, is typically excluded from taxable income under Section 111 of the Internal Revenue Code. This is because the tenant is merely recovering funds they overpaid, not receiving new income. For example, if a tenant receives a $10,000 refund for rent overcharges, this amount would not be taxable. However, if the settlement includes punitive damages or compensation for emotional distress, those portions could be taxable as ordinary income. Tenants should carefully review their settlement agreements and consult a tax professional to determine which parts, if any, need to be reported to the IRS or New York State.

Practical steps for tenants navigating rent overcharge settlements include keeping detailed records of all rent payments, communications with the landlord, and any legal documents related to the claim. When a settlement is reached, tenants should request a breakdown of the payment, specifying which amounts are for rent overcharges, legal fees, or other damages. This documentation is crucial for tax purposes and can help avoid misunderstandings with tax authorities. Additionally, tenants should be aware of the statute of limitations for filing overcharge claims, which is generally four years in New York City, though exceptions may apply.

Comparatively, while rent overcharge refunds are typically non-taxable, other types of tenant settlements may not be. For instance, if a tenant receives a buyout to vacate a rent-stabilized apartment, that payment is often considered taxable income because it is not restitution but rather compensation for relinquishing rights. Similarly, if a tenant receives a settlement for a housing code violation, the tax treatment depends on whether the payment is for restitution (e.g., repair costs) or additional damages. Understanding these distinctions is essential for tenants to comply with tax laws and avoid unexpected liabilities.

In conclusion, NYC rent overcharge settlements are generally not taxable when they represent refunds of overpaid rent. However, tenants must scrutinize their settlement agreements to identify any taxable components, such as damages or legal fees. By staying informed and organized, tenants can navigate both housing and tax regulations effectively, ensuring they retain the full benefit of their rent overcharge refunds without unintended tax consequences.

Renting AWS Servers: A Step-by-Step Guide to Access Setup

You may want to see also

Explore related products

![]()

Tax Implications of Settlements

In New York City, rent overcharge settlements often leave tenants and landlords alike questioning their tax obligations. The Internal Revenue Service (IRS) generally considers settlements as income, but the tax treatment can vary based on the nature of the settlement. For rent overcharge cases, the key lies in distinguishing between restitution and punitive damages. Restitution, which aims to compensate for the overpaid rent, is typically taxable as ordinary income. Punitive damages, however, may be taxed differently, often at a higher rate or under specific rules. Understanding this distinction is crucial for accurately reporting and managing tax liabilities.

For tenants receiving rent overcharge settlements, the IRS treats the recovered amount as income in the year it is received. This means the settlement must be reported on your federal tax return, typically on Line 21 of Form 1040 as "Other Income." In NYC, the state and local tax treatment may align with federal rules, but it’s essential to verify with the New York State Department of Taxation and Finance. Tenants should retain detailed records of the settlement agreement, including the breakdown of restitution and any punitive damages, to ensure accurate reporting. Failing to report the settlement could result in penalties or audits, so proactive compliance is advised.

Landlords, on the other hand, may face different tax implications. If a landlord pays a settlement for rent overcharges, the amount paid may be deductible as a business expense, provided it qualifies as an ordinary and necessary expense under IRS guidelines. However, if the settlement includes penalties or fines, these amounts are generally not deductible. Landlords should consult a tax professional to determine the appropriate treatment of the settlement payment, especially when navigating the complexities of NYC’s rent stabilization laws and their interplay with tax regulations.

A practical tip for both parties is to consult a tax advisor or attorney specializing in real estate and tax law. They can provide tailored guidance based on the specifics of the settlement, such as whether the overcharge was due to a clerical error or intentional misconduct. Additionally, tenants and landlords should consider the timing of the settlement. If the overcharge spans multiple years, the IRS may require the income to be allocated across those years, potentially affecting tax brackets and liabilities. Proactive planning and documentation are key to minimizing tax surprises and ensuring compliance with both federal and state tax laws.

In conclusion, rent overcharge settlements in NYC carry significant tax implications that demand careful attention. Tenants must report restitution as income, while landlords may deduct settlement payments under certain conditions. The distinction between restitution and punitive damages, coupled with the need for precise record-keeping, underscores the importance of professional advice. By understanding these nuances, both parties can navigate the tax landscape effectively, avoiding pitfalls and ensuring financial clarity in the aftermath of a rent overcharge settlement.

Average Rent in Scottdale, GA: What to Expect in 2023

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![]()

Reporting Settlement Income

In New York City, rent overcharge settlements often result in tenants receiving substantial sums, but the tax implications of this income can be complex. The Internal Revenue Service (IRS) generally considers settlement proceeds as taxable income unless they are specifically excluded by law. For rent overcharge settlements, the key question is whether the payment compensates for lost rent or represents a return of overpaid rent. If the latter, it may be treated as a refund of previously taxed rent, potentially reducing its taxable nature. However, without clear guidance, tenants must carefully analyze the settlement terms to determine their reporting obligations.

To report settlement income accurately, tenants should first request a detailed breakdown of the settlement amount from their attorney or the housing court. This breakdown should distinguish between any interest, penalties, or other components included in the payment. For instance, interest accrued on the overcharged rent is typically taxable as ordinary income, while the principal amount might be offset against previously deducted rent expenses. Tenants should use IRS Form 1040 to report taxable portions and consult Schedule 1 if the settlement includes interest or penalties. Keeping thorough records of all rent payments and deductions is essential for substantiating any offsets claimed.

A common mistake tenants make is assuming the entire settlement is tax-free because it arises from a housing dispute. However, the IRS focuses on the nature of the payment, not the source. For example, if a tenant deducted rent expenses in prior years, a settlement refunding those overpayments may not be fully taxable, as it effectively corrects a previous deduction. Conversely, if the tenant did not itemize deductions, the entire settlement could be taxable income. This distinction highlights the importance of understanding one’s tax history and consulting a tax professional to navigate these nuances.

Practical tips for reporting settlement income include filing an amended return if the settlement corrects a prior tax year’s deduction and retaining all court documents and settlement agreements for at least seven years. Tenants should also be aware of New York State tax rules, which may differ from federal guidelines. For instance, New York State may exclude certain portions of rent overcharge settlements from taxable income under specific circumstances. Proactive communication with both legal and tax advisors ensures compliance and minimizes the risk of audits or penalties.

Renting to Selling: Unforeseen Consequences and Legal Pitfalls to Avoid

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![]()

Exemptions for Rent Overcharges

In New York City, rent overcharge settlements can be a financial lifeline for tenants who have been paying excessive rent. However, the tax implications of these settlements are often misunderstood. While the general rule is that such settlements are taxable as income, certain exemptions can apply, reducing or eliminating the tax burden. Understanding these exemptions is crucial for tenants navigating the complexities of rent overcharge cases.

One key exemption arises from the nature of the settlement itself. If the overcharge settlement is deemed a refund of rent paid, rather than additional income, it may not be taxable. The IRS and New York State tax authorities distinguish between income and refunds, with refunds generally not subject to taxation. For example, if a tenant paid $2,000 in excess rent over two years and receives a $4,000 settlement, this could be treated as a refund of the overpaid amount rather than taxable income. Tenants should consult tax professionals to ensure proper classification, as documentation and the specific terms of the settlement agreement play a critical role in this determination.

Another exemption to consider is the treatment of attorney’s fees associated with rent overcharge cases. Under the Tax Cuts and Jobs Act (TCJA), attorney’s fees are no longer deductible as miscellaneous itemized deductions for most taxpayers. However, if the attorney’s fees are paid out of the settlement proceeds and are directly tied to the recovery of rent overcharges, they may reduce the taxable portion of the settlement. For instance, if a tenant receives a $10,000 settlement and $3,000 goes to attorney’s fees, only $7,000 may be taxable, provided the fees are properly allocated in the settlement agreement.

Practical steps can help tenants maximize these exemptions. First, ensure the settlement agreement explicitly states that the payment is a refund of overpaid rent, not additional compensation. Second, document all rent payments and overcharges to support the refund classification. Third, work with a tax advisor to properly allocate attorney’s fees and other expenses within the settlement. Finally, be aware of state-specific rules; New York State may have additional exemptions or requirements that differ from federal guidelines.

In conclusion, while rent overcharge settlements in NYC are generally taxable, exemptions exist that can significantly reduce the tax liability. By understanding the distinction between refunds and income, properly allocating attorney’s fees, and taking proactive steps to document the settlement, tenants can navigate the tax implications more effectively. This knowledge not only ensures compliance with tax laws but also maximizes the financial benefit of rent overcharge recoveries.

Is Advanced Rent Revenue a Current Liability? Understanding Accounting Basics

You may want to see also

Explore related products

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![]()

IRS vs. NYS Tax Rules

The IRS and New York State (NYS) tax rules diverge significantly when it comes to the taxability of rent overcharge settlements in NYC, creating a complex landscape for tenants and landlords alike. While the IRS generally treats such settlements as taxable income, NYS offers a more tenant-friendly approach, often exempting these amounts from state taxation. This discrepancy stems from differing interpretations of what constitutes taxable income and the purpose of rent overcharge settlements.

From the IRS’s perspective, rent overcharge settlements are considered reparations for excess rent paid, which fall under the category of “other income” as per IRS Publication 525. This means that unless the settlement qualifies for a specific exclusion (such as for physical injury or sickness), it is taxable at the federal level. For instance, if a tenant receives a $10,000 settlement for rent overcharges, the IRS would require this amount to be reported on Form 1040, potentially increasing the taxpayer’s federal tax liability. Landlords, on the other hand, may be able to deduct the settlement amount as a business expense if it relates to their rental activity, but this does not alleviate the tenant’s tax burden.

In contrast, NYS takes a more nuanced approach. Under New York State tax law, rent overcharge settlements are often exempt from taxation if they are awarded under the state’s rent stabilization laws. The NYS Department of Taxation and Finance considers these settlements as restitution for overpaid rent rather than taxable income. For example, if the same $10,000 settlement mentioned earlier is received by a tenant in NYC, it would likely be excluded from NYS taxable income, provided it meets the criteria outlined in the Rent Stabilization Law (RSL) or Rent Control regulations.

This divergence in tax treatment highlights the importance of understanding both federal and state tax rules when dealing with rent overcharge settlements. Tenants should consult tax professionals to ensure compliance with IRS regulations while taking advantage of NYS exemptions. Landlords, too, must carefully document settlements to support potential deductions and avoid double taxation issues. Practical tips include retaining all settlement documents, including court orders or agreements, and clearly identifying the nature of the settlement in tax filings to avoid audits or penalties.

In conclusion, while the IRS broadly taxes rent overcharge settlements, NYS provides a tax-exempt haven for tenants under specific conditions. Navigating this dual tax landscape requires careful attention to detail and, often, professional guidance to ensure both federal and state tax obligations are met without overpaying.

Paris, KY Land Rental Rates: What to Expect in 2023

You may want to see also

Frequently asked questions

Yes, rent overcharge settlements in NYC are generally considered taxable income by the IRS and New York State, as they are treated as compensation for damages or lost rent.

Report the settlement amount as "Other Income" on your federal tax return (Form 1040, Line 8) and follow New York State guidelines for state tax reporting, typically on Form IT-201.

Yes, if you itemize deductions, you may be able to deduct legal fees related to the settlement as a miscellaneous itemized deduction, subject to certain limitations.

There are no specific exceptions for rent overcharge settlements. However, if a portion of the settlement is designated as reimbursement for specific expenses (e.g., moving costs), that portion may not be taxable. Consult a tax professional for clarity.

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)