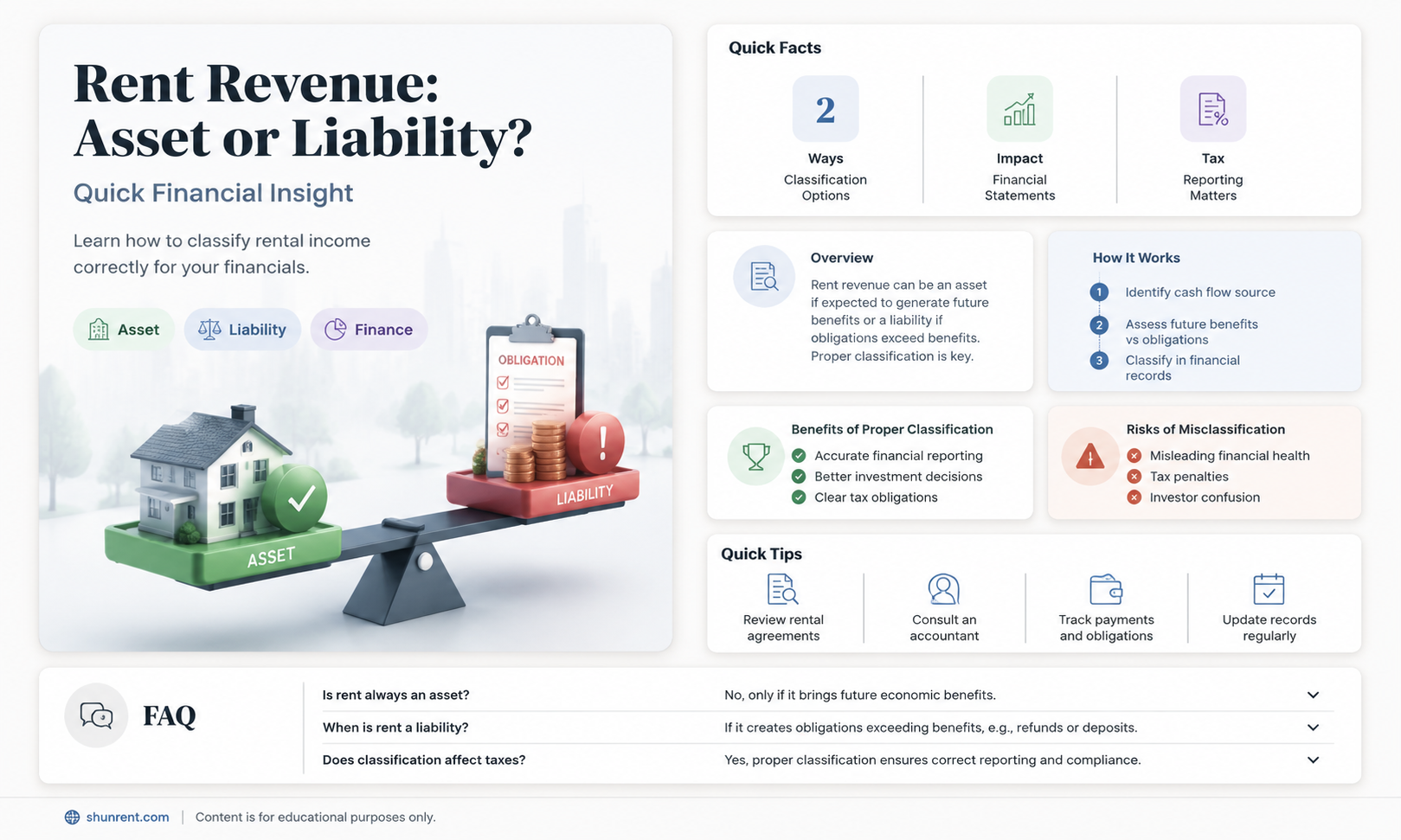

The classification of rent revenue as either an asset or a liability is a fundamental question in accounting and financial reporting. Rent revenue, which represents the income generated from leasing property, is typically considered an asset when it is earned but not yet received, often recorded as rent receivable. However, once the rent is collected, it is recognized as revenue on the income statement, reducing the asset balance. Conversely, if a company has prepaid rent or owes rent for future periods, it may be classified as a liability, such as rent payable or a prepaid expense. Understanding this distinction is crucial for accurately reflecting a company's financial position and ensuring compliance with accounting standards.

Explore related products

What You'll Learn

- Rent Revenue Classification: Is rent revenue considered an asset or liability in accounting

- Asset vs. Liability: Understanding the nature of rent revenue in financial statements

- Accounting Treatment: How rent revenue is recorded and reported in books

- Cash Flow Impact: Rent revenue’s role in operating cash flow analysis

- Balance Sheet Placement: Where rent revenue appears on the balance sheet, if at all

![]()

Rent Revenue Classification: Is rent revenue considered an asset or liability in accounting?

Rent revenue, a fundamental component of many businesses, particularly in the real estate sector, often sparks confusion regarding its classification in accounting. The question arises: Is rent revenue an asset or a liability? To unravel this, let's delve into the accounting principles that govern such classifications.

Understanding the Basics

In accounting, assets are resources owned by a company that provide future economic benefits, while liabilities are obligations that require future settlement. Revenue, on the other hand, represents the income generated from business activities. Rent revenue, specifically, is the income earned from leasing property. At first glance, it might seem like revenue should align with assets, as it increases a company’s financial health. However, revenue is not classified as either an asset or a liability. Instead, it is recorded in the income statement, which tracks earnings over a period. When rent is collected in advance, it is treated as a liability (deferred revenue) until the service period is fulfilled, at which point it is recognized as revenue.

Analyzing the Timing Factor

The classification of rent revenue hinges on timing. If a tenant pays rent upfront for a future period, the landlord records it as a liability (unearned rent revenue). This is because the landlord has an obligation to provide the rental service in the future. As each month passes and the service is delivered, the liability is reduced, and the corresponding amount is recognized as revenue. For example, if a tenant pays $12,000 annually in advance, the landlord would record $1,000 as revenue each month and reduce the liability by the same amount. This ensures that revenue is recognized in the period it is earned, adhering to the accrual accounting principle.

Practical Implications for Businesses

For businesses, understanding this classification is crucial for accurate financial reporting. Misclassifying rent revenue can distort financial statements, leading to incorrect assessments of profitability and financial health. For instance, recording advanced rent payments as revenue immediately would inflate current earnings, misrepresenting the company’s performance. Conversely, failing to recognize earned revenue would understate income. Accountants must meticulously track the timing of rent payments and the corresponding service periods to ensure compliance with accounting standards like GAAP or IFRS.

Comparative Perspective

To illustrate, consider two scenarios: a landlord receiving monthly rent payments and another receiving a year’s rent in advance. In the first case, each payment is directly recorded as revenue in the month it is received. In the second case, the entire payment is initially recorded as a liability, with revenue recognized monthly as the service is provided. This distinction highlights the importance of aligning revenue recognition with the delivery of services, a core principle in accounting.

Rent revenue itself is neither an asset nor a liability; it is a component of the income statement. However, advanced rent payments create a liability (deferred revenue) until the service is rendered. This classification ensures that financial statements accurately reflect a company’s economic reality. For businesses, the key takeaway is to carefully manage the timing of revenue recognition, avoiding pitfalls that could compromise financial integrity. By adhering to these principles, companies can maintain transparency and trust in their financial reporting.

Renting from a Private Owner? Essential Tips for a Smooth Experience

You may want to see also

Explore related products

![]()

Asset vs. Liability: Understanding the nature of rent revenue in financial statements

Rent revenue, a cornerstone of many businesses, particularly in real estate, often sparks confusion in financial categorization. Is it an asset, bolstering a company's financial health, or a liability, representing an obligation? The answer lies in understanding the timing and nature of this revenue stream.

When rent is received upfront, it's initially recorded as a liability, specifically a deferred revenue or unearned revenue account. This reflects the obligation to provide the rented space or service in the future. As time passes and the rental period elapses, the liability is gradually recognized as revenue, shifting from the liability section to the asset side of the balance sheet. This transformation highlights the dynamic nature of rent revenue, evolving from a future obligation to a realized asset.

Consider a landlord receiving a year's rent in advance. This lump sum isn't immediately considered income. Instead, it's a liability, a promise to provide housing for the next twelve months. Each month, a portion of this liability is recognized as revenue, reflecting the service provided. This method, known as accrual accounting, ensures a more accurate representation of a company's financial position by matching revenue with the period it's earned.

Key Takeaway: Rent revenue's classification as an asset or liability hinges on timing. Upfront payments create a liability, while revenue recognition over the rental period transforms it into an asset.

This distinction is crucial for financial analysis. Investors and creditors scrutinize a company's assets and liabilities to gauge its financial stability and risk profile. Misclassification of rent revenue can distort these perceptions. For instance, a company with significant deferred rent revenue might appear more indebted than it truly is, potentially deterring investors. Conversely, prematurely recognizing rent as revenue could inflate a company's financial health, leading to misguided investment decisions.

Practical Tip: Businesses should clearly disclose their rent revenue recognition policies in financial statements to ensure transparency and allow for accurate analysis.

Understanding the asset-liability duality of rent revenue is essential for both financial professionals and business owners. It ensures accurate financial reporting, informed decision-making, and a clearer picture of a company's true financial standing. By grasping this concept, stakeholders can navigate the complexities of financial statements with greater confidence and precision.

Rent Game of Thrones Season 5: Top Streaming Platforms Guide

You may want to see also

Explore related products

![]()

Accounting Treatment: How rent revenue is recorded and reported in books

Rent revenue is classified as neither an asset nor a liability; instead, it is recognized as income on the income statement. This distinction is crucial for accurate financial reporting. When a landlord receives rent, it represents earnings from the use of a property, not an obligation or a resource owned. Therefore, it falls under revenue, which reflects the inflow of economic benefits during a specific period.

Recording rent revenue follows the accrual accounting principle, meaning it is recognized when earned, not when payment is received. For example, if a tenant pays $1,200 in advance for six months of rent, the landlord records $200 as revenue each month, not $1,200 upfront. This method ensures financial statements reflect the economic reality of the transaction. To implement this, use journal entries: debit cash (asset) for the amount received and credit unearned rent revenue (liability) for the prepaid portion. As each month passes, adjust by debiting unearned rent revenue and crediting rent revenue (income).

The reporting of rent revenue also involves disclosure in financial statements. On the income statement, it appears under operating income, contributing to the entity’s total revenue. In the notes to the financial statements, details such as lease terms, payment schedules, and any contingent rents may be disclosed for transparency. For instance, if a lease includes variable rent based on sales, this should be clearly explained to avoid misleading stakeholders.

A common pitfall is misclassifying rent revenue as an asset or liability due to confusion with prepaid rent or security deposits. Prepaid rent, paid by a tenant, is an asset for the tenant and a liability for the landlord until earned. Security deposits, however, are liabilities for the landlord until returned or applied to damages. To avoid errors, maintain separate accounts for rent revenue, prepaid rent, and security deposits, ensuring each transaction is recorded accurately.

In summary, rent revenue is treated as income, recorded using accrual accounting, and reported on the income statement. Proper classification and disclosure are essential for compliance with accounting standards and providing a clear financial picture. By following these steps and avoiding common mistakes, entities can ensure their financial statements accurately reflect their rental activities.

Renting a Conan Exiles Server: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Cash Flow Impact: Rent revenue’s role in operating cash flow analysis

Rent revenue is classified as neither an asset nor a liability on a balance sheet; instead, it is recognized as income on the income statement. However, its impact on cash flow analysis is profound, particularly within operating activities. When tenants pay rent, it directly increases cash inflows, bolstering liquidity and operational sustainability. For instance, a commercial property owner receiving $50,000 monthly in rent sees this amount reflected in operating cash flow, enhancing the ability to cover expenses like maintenance, taxes, and debt servicing. This predictable, recurring nature of rent revenue makes it a cornerstone of cash flow stability for real estate businesses.

Analyzing rent revenue’s role in operating cash flow requires distinguishing it from non-operating or financing activities. Unlike proceeds from selling a property (an investing activity) or issuing bonds (a financing activity), rent revenue is purely operational. It’s essential to scrutinize the timing and consistency of these inflows. For example, a 10% vacancy rate in a multifamily property reduces expected rent revenue, directly impacting cash flow. Investors and analysts must assess lease terms, tenant creditworthiness, and market demand to forecast rent revenue accurately and avoid overestimating cash flow resilience.

A persuasive argument for prioritizing rent revenue in cash flow analysis lies in its ability to signal financial health. Consistent rent collections indicate strong tenant relationships and market positioning, while declining revenue may foreshadow operational or economic challenges. Consider a retail landlord experiencing a 20% drop in rent payments due to e-commerce competition—this would immediately strain operating cash flow, potentially jeopardizing debt obligations. By monitoring rent revenue trends, stakeholders can proactively adjust strategies, such as renegotiating leases or diversifying tenant types, to safeguard cash flow.

Comparatively, rent revenue’s impact on cash flow differs across industries. For real estate investment trusts (REITs), it constitutes the primary operating cash flow source, often exceeding 80% of total inflows. In contrast, manufacturing firms may derive less than 5% of cash flow from rent if they lease excess warehouse space. This disparity underscores the need for industry-specific analysis. A REIT with declining rent revenue faces immediate cash flow risks, whereas a manufacturer might absorb such losses through core business operations. Tailoring cash flow models to account for rent revenue’s proportional significance ensures more accurate financial assessments.

Practically, optimizing rent revenue’s contribution to cash flow involves strategic lease structuring and expense management. For instance, escalating rent clauses tied to inflation or market rates can future-proof cash inflows. Additionally, minimizing operating expenses—such as energy-efficient upgrades reducing utility costs—amplifies net cash flow from rent. A case study of a Class A office building in New York City illustrates this: by implementing smart building technology, the owner reduced operational expenses by 15%, effectively increasing net cash flow from rent by $250,000 annually. Such proactive measures ensure rent revenue not only sustains but enhances operating cash flow over time.

How to Calculate Affordable Rent Based on Your Income

You may want to see also

Explore related products

![]()

Balance Sheet Placement: Where rent revenue appears on the balance sheet, if at all

Rent revenue, a cornerstone of many businesses, particularly real estate and leasing operations, does not appear directly on the balance sheet. This might seem counterintuitive, given its significance to cash flow and profitability. However, understanding why requires a dive into the fundamental principles of accounting and the distinct roles of the income statement and balance sheet.

The balance sheet, a snapshot of a company's financial position at a given moment, categorizes items into assets, liabilities, and equity. Assets represent what a company owns, liabilities what it owes, and equity the residual interest of owners. Rent revenue, being income earned from leasing property, falls under the realm of the income statement, which tracks revenues and expenses over a specific period. It’s a flow, not a stock, and thus doesn’t fit the static nature of the balance sheet.

To illustrate, imagine a landlord collecting $10,000 in rent for the month. This $10,000 is revenue, but it doesn’t become an asset until it’s received and held as cash. Until then, it’s merely an earned amount, recognized on the income statement. Once received, the cash increases the asset side of the balance sheet, while the corresponding revenue is recorded on the income statement, impacting net income and ultimately equity.

A common misconception arises from confusing rent revenue with prepaid rent or security deposits. Prepaid rent, where a tenant pays rent in advance, is indeed an asset for the tenant and a liability for the landlord until the rent period begins. Similarly, security deposits are liabilities for the landlord until they’re either refunded or applied to damages. These items appear on the balance sheet because they represent obligations or claims, not earned income.

In summary, rent revenue’s absence from the balance sheet is a reflection of its nature as a flow of income rather than a static asset or liability. Its proper place is on the income statement, where it contributes to the calculation of net income and, indirectly, to changes in equity. Understanding this distinction is crucial for accurately interpreting financial statements and assessing a company’s financial health.

Mastering the Art of Playing Trailers for Sale or Rent

You may want to see also

Frequently asked questions

Yes, rent revenue is considered an asset when it is earned but not yet received. It is recorded as accounts receivable on the balance sheet until the payment is collected.

No, rent revenue itself is not a liability. However, if rent is received in advance, it is recorded as a deferred revenue liability until the service period is fulfilled.

If rent is paid in advance, it is initially recorded as a prepaid rent asset by the payer and as a deferred revenue liability by the receiver. It is recognized as revenue over the rental period.

Rent revenue impacts both. It is recorded as revenue on the income statement when earned and may appear as accounts receivable (asset) or deferred revenue (liability) on the balance sheet, depending on the timing of payment.