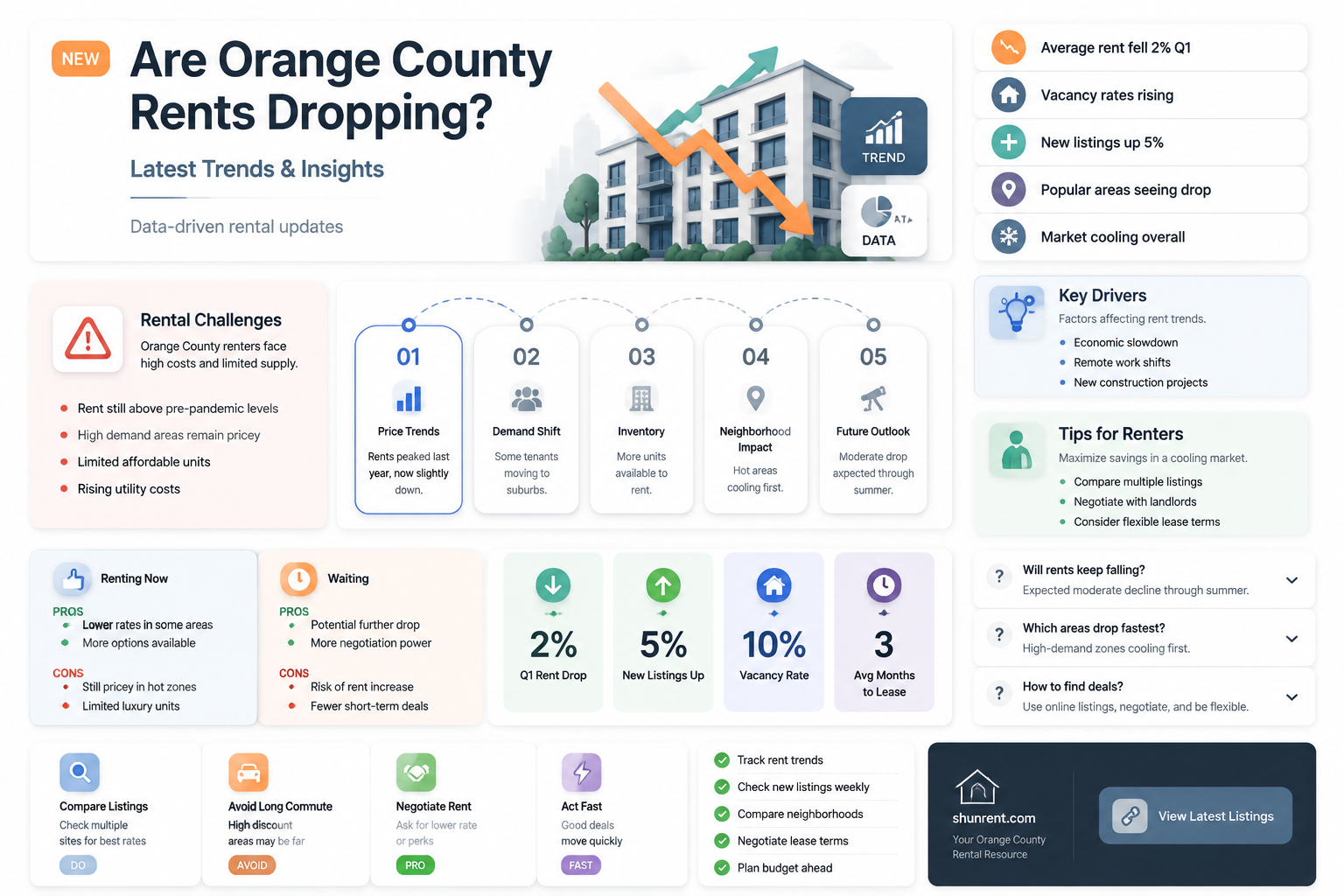

The question of whether rents are going down in Orange County has become a pressing concern for residents, prospective tenants, and real estate observers alike. After years of steep increases driven by high demand, limited inventory, and economic growth, recent data suggests a potential shift in the rental market. Factors such as rising interest rates, a slowdown in job growth, and an increase in new housing developments may be contributing to a cooling trend. While some areas within Orange County are seeing modest declines in rental prices, others remain stable or even slightly elevated, creating a mixed picture. Understanding these dynamics is crucial for renters, landlords, and policymakers as they navigate the evolving housing landscape in one of California’s most sought-after regions.

| Characteristics | Values |

|---|---|

| Rent Trend (Overall) | Mixed, with some areas showing slight decreases and others remaining stable |

| Average Rent (1-Bedroom) | $2,300 - $2,500 (as of Q2 2023, sources vary) |

| Year-over-Year Change (2022-2023) | -1% to +2% (depending on source and location) |

| Cities with Declining Rents | Santa Ana, Anaheim, and parts of Irvine |

| Cities with Stable or Increasing Rents | Newport Beach, Huntington Beach, and Costa Mesa |

| Factors Influencing Rent Trends | Increased housing supply, economic conditions, and remote work policies |

| Vacancy Rates | 4-5% (slightly higher than historical averages) |

| New Construction Impact | Contributing to increased supply, particularly in Irvine and Anaheim |

| Forecast (2023-2024) | Modest declines or stabilization expected in most areas |

| Source of Data | Zillow, Apartment List, and local real estate reports (as of August 2023) |

Explore related products

![Orange County [Blu-ray]](https://m.media-amazon.com/images/I/81Xxkz8QbgL._AC_UY218_.jpg)

What You'll Learn

![]()

Current rental trends in Orange County

Orange County's rental market is experiencing a subtle shift, with recent data indicating a gradual cooling after years of relentless growth. According to a Q3 2023 report by CoStar, average rents in Orange County have dipped by 0.8% year-over-year, marking the first decline since 2010. This reversal is particularly notable in high-demand areas like Irvine and Newport Beach, where rents had previously soared by double digits annually. While this decrease is modest, it signals a potential turning point for renters who have long faced affordability challenges in this affluent Southern California region.

Several factors are driving this trend. Firstly, the surge in new multifamily developments is increasing supply, easing the pressure on existing rental units. For instance, over 5,000 new apartment units are expected to hit the market in Orange County by the end of 2024, according to Yardi Matrix. Secondly, rising mortgage rates have priced some would-be homebuyers out of the market, keeping them in the rental pool longer. However, this increased supply is not uniformly distributed; luxury apartments are seeing more significant rent reductions, while affordable units remain scarce and competitive.

For renters, this shift presents both opportunities and challenges. On one hand, the slight decrease in rents offers a rare chance to negotiate lease terms or explore neighborhoods previously out of reach. For example, renters in Anaheim and Santa Ana are finding more flexibility in pricing compared to six months ago. On the other hand, the overall cost of living in Orange County remains high, with utilities, groceries, and transportation offsetting any modest savings on rent. Prospective tenants should prioritize budgeting tools and long-term lease agreements to lock in current rates before the market stabilizes further.

Comparatively, Orange County’s rental trends contrast with neighboring Los Angeles County, where rents have continued to climb, albeit at a slower pace. This divergence highlights the localized nature of rental markets and underscores the importance of regional analysis. For instance, while Los Angeles grapples with a persistent housing shortage, Orange County’s proactive approach to increasing housing supply is yielding tangible results. Renters in Orange County may therefore find more favorable conditions in the near term, but they should remain vigilant as economic factors like inflation and job growth continue to influence the market.

In conclusion, while rents in Orange County are showing signs of decline, the change is incremental and unevenly distributed. Renters can capitalize on this trend by staying informed about neighborhood-specific data, leveraging negotiation tactics, and planning for long-term housing stability. As the market continues to evolve, those who act strategically will be best positioned to benefit from the current shifts in Orange County’s rental landscape.

Balancing Harvard Tuition and Rent: Smart Strategies for Affordability

You may want to see also

Explore related products

![Orange County [DVD]](https://m.media-amazon.com/images/I/612WI4EYiIL._AC_UY218_.jpg)

![Orange County [VHS]](https://m.media-amazon.com/images/I/91bSQwD50uL._AC_UY218_.jpg)

![Orange County [Region 2]](https://m.media-amazon.com/images/I/8121lrLfoWL._AC_UY218_.jpg)

![]()

Factors influencing rent decreases in the area

Recent data suggests a cooling trend in Orange County's rental market, with median rents dipping slightly after years of steady increases. This shift prompts an examination of the factors driving these decreases. One significant influence is the surge in new multifamily housing developments across the county. From 2022 to 2023, Orange County saw a 15% increase in apartment construction permits, adding thousands of units to the market. This influx of supply naturally eases competition among renters, giving them more options and negotiating power. For instance, areas like Irvine and Anaheim, where new complexes have sprouted, are reporting rent reductions of up to 5% compared to last year.

Another critical factor is the broader economic climate, particularly the rise in remote work and its impact on housing preferences. As companies adopt hybrid or fully remote models, some residents are relocating to more affordable regions, reducing demand in high-cost areas like Orange County. A 2023 survey by the Orange County Business Council revealed that 22% of local professionals have moved or plan to move outside the county due to housing costs. This exodus, coupled with a slight decline in job growth in sectors like hospitality and retail, has softened rental demand, contributing to downward pressure on prices.

Additionally, policy changes at the state and local levels are playing a role. California’s recent rent control legislation, AB 1482, caps annual rent increases at 5% plus inflation, providing tenants with greater stability. In Orange County, cities like Santa Ana and Costa Mesa have implemented additional tenant protections, such as just-cause eviction ordinances. These measures discourage speculative rent hikes and encourage landlords to maintain competitive pricing to retain tenants. While not directly causing rent decreases, such policies create an environment where landlords are less likely to raise rents aggressively, indirectly contributing to the cooling trend.

Lastly, shifting demographics and lifestyle preferences are influencing rental dynamics. Millennials and Gen Z renters, who make up a significant portion of the market, are increasingly prioritizing affordability and flexibility over luxury amenities. This has led to reduced demand for high-end apartments in favor of more modest, cost-effective options. For example, studio and one-bedroom units in older buildings are seeing greater occupancy rates than newer, upscale complexes. Landlords of premium properties are responding by lowering rents or offering incentives like waived application fees or free parking to attract tenants, further driving overall rent decreases in the area.

Understanding these factors provides a roadmap for both renters and landlords navigating Orange County’s evolving market. For renters, staying informed about new developments and policy changes can help identify opportunities for better deals. Landlords, meanwhile, may need to adapt by offering competitive pricing or enhancing value through amenities or flexible lease terms. As these trends continue to shape the market, the balance between supply, demand, and policy will remain key determinants of rent levels in the region.

Renting a 15-Passenger Van in Winnipeg: Top Locations and Tips

You may want to see also

Explore related products

![]()

Impact of housing supply on rent prices

The relationship between housing supply and rent prices is a delicate balance, and Orange County's rental market is a prime example of this dynamic. As of recent reports, the county has experienced a slight decrease in rent prices, a trend that can be largely attributed to the increase in housing inventory. This shift is particularly notable after years of a tight market where demand consistently outpaced supply, driving rents upward.

Understanding the Supply-Rent Nexus

When housing supply expands, whether through new construction or increased vacancy rates, it creates a competitive environment for landlords. This competition often leads to price reductions as property owners vie to attract tenants. In Orange County, the completion of several multifamily housing projects in 2023 has introduced more units to the market, easing the pressure on renters. For instance, areas like Irvine and Anaheim have seen a 3-5% drop in median rent prices, directly correlating with the addition of over 2,000 new units in these regions.

Practical Implications for Renters

For those looking to rent in Orange County, understanding this supply-driven trend can be a strategic advantage. Renters should monitor neighborhoods with upcoming developments, as these areas are likely to offer more competitive pricing. Additionally, negotiating lease terms becomes more feasible in a market with ample supply. For example, renters might successfully request lower monthly payments, waived fees, or included utilities, especially in buildings with higher vacancy rates.

Cautions and Considerations

While increased supply is generally beneficial for renters, it’s not a universal solution. Certain highThe relationship between housing supply and rent prices is a delicate balance, and Orange County's rental market is a prime example of this dynamic. As of recent reports, the county has experienced a slight decrease in rent prices, a trend that can be largely attributed to the increase in housing inventory. This shift is particularly notable after years of rising rents, leaving many to wonder if this is a temporary adjustment or a sustained change.

Understanding the Supply-Price Mechanism

Imagine a seesaw, where one end represents housing supply and the other, rent prices. When the supply of rental units increases, the seesaw tilts, causing rent prices to decrease. This is a fundamental economic principle at play in Orange County. The county has seen a surge in new apartment constructionsThe relationship between housing supply and rent prices is a delicate balance, and in Orange County, this dynamic has been a key factor in the recent trends of rental costs. As of the latest data, the county's rental market is experiencing a shift, with some areas witnessing a decline in rents, contrary to the long-standing upward trajectory. This change can be largely attributed to the increasing housing supply, which has started to outpace demand in certain neighborhoods.

Analyzing the Supply-Demand Equation:

In economics, the law of supply and demand is fundamental, and the housing market is no exception. When the supply of rental units surpasses the number of tenants seeking accommodation, landlords often adjust prices downward to attract occupants. This scenario is particularly evident in Orange County's newer developments, where a surge in construction has led to a glut of available apartments and condos. For instance, in Irvine, the addition of several large-scale residential projects has resulted in a 5% decrease in average rent over the past year, according to a local real estate report. This trend demonstrates how an increased housing supply can directly contribute to more affordable rental options.

The Role of Demographics and Preferences:

Understanding tenant demographics and preferences is crucial in this context. Orange County's diverse population includes young professionals, families, and retirees, each with distinct housing needs. For instance, the rise in remote work has led to a demand for larger homes with dedicated office spaces, causing a shift from urban apartments to suburban houses. This change in preference has left some high-rise buildings in downtown areas with higher vacancy rates, prompting landlords to reduce rents to fill these units. A strategic approach for landlords could be to adapt their properties to meet evolving tenant requirements, ensuring their units remain competitive in a changing market.

Long-term Implications and Market Stability:

The impact of housing supply on rent prices has long-term implications for both tenants and investors. A sustained increase in supply can lead to a more stable and predictable rental market, benefiting tenants with consistent or decreasing rents. However, for property owners, it may result in reduced revenue and potential challenges in maintaining profitability. To navigate this, investors should consider diversifying their portfolios, perhaps by exploring mixed-use developments that combine residential and commercial spaces, thus attracting a broader tenant base.

Practical Tips for Tenants and Landlords:

For tenants, the current market presents an opportunity to negotiate better terms. When searching for a rental, consider areas with new developments, as these are more likely to offer competitive prices. Additionally, keep an eye on local planning applications to anticipate future supply increases. Landlords, on the other hand, should focus on creating unique selling points for their properties, such as offering flexible lease terms or adding amenities that cater to specific tenant needs. Regular market research is essential to stay ahead of trends and ensure properties remain attractive in a competitive environment.

In summary, the impact of housing supply on rent prices in Orange County is a multifaceted issue, offering both challenges and opportunities. By understanding the supply-demand dynamics and adapting to changing market conditions, tenants and landlords can make informed decisions to navigate this evolving landscape effectively.

Bay Area Rental Trends: How Many Residents Choose to Rent?

You may want to see also

Explore related products

![]()

Economic conditions affecting Orange County rentals

Orange County's rental market is a complex tapestry woven from various economic threads, each pulling and tugging at the delicate balance between supply and demand. One of the primary factors influencing rental prices is the region's robust job market. With a diverse economy spanning technology, healthcare, and tourism, Orange County has long attracted a steady stream of professionals seeking employment opportunities. This influx of workers drives up demand for housing, putting upward pressure on rents. However, recent shifts in the job market, such as the rise of remote work and the tech industry's slowdown, have begun to alter this dynamic. As companies reevaluate their office space needs and employees prioritize flexibility, the demand for rentals in traditional employment hubs may soften, potentially leading to a moderation in rent growth.

Another critical economic condition affecting Orange County rentals is the broader macroeconomic environment, particularly interest rates and inflation. The Federal Reserve's monetary policy decisions have a ripple effect on the housing market, influencing mortgage rates and, by extension, rental prices. When interest rates rise, as they have in recent years, borrowing becomes more expensive, discouraging some potential homebuyers from entering the market. This increased demand for rentals can drive prices higher. Conversely, if inflation persists and the Fed maintains a tight monetary policy, it could dampen economic growth, reducing the number of people moving to the area for work and easing rental demand.

Supply-side factors also play a significant role in shaping Orange County's rental landscape. The region's stringent zoning regulations and high construction costs have historically constrained new housing development, limiting the supply of available rentals. This imbalance between supply and demand has contributed to the county's high housing costs. However, recent legislative efforts to streamline the approval process for multifamily housing projects and incentivize affordable housing development could gradually alleviate this pressure. As more units come online, increased supply may help temper rent growth, providing some relief to tenants.

A comparative analysis of Orange County's rental market with neighboring regions offers additional insights. While Orange County has long been one of California's priciest rental markets, its rates have begun to converge with those of Los Angeles and San Diego in recent years. This trend suggests that economic forces affecting the broader Southern California region, such as population growth and housing affordability challenges, are impacting Orange County's rental dynamics. However, Orange County's unique blend of economic drivers, including its strong tourism sector and high-paying tech jobs, continues to set it apart. As these industries evolve, so too will the economic conditions shaping the county's rental market.

To navigate this complex landscape, both landlords and tenants must stay informed about the interplay of these economic factors. For instance, landlords might consider offering flexible lease terms or amenities that cater to remote workers to maintain occupancyOrange County's rental market is a complex interplay of supply, demand, and broader economic forces. One key factor currently influencing rents is the shift in remote work policies. During the pandemic, many companies adopted remote or hybrid work models, allowing employees to relocate to more affordable areas. This trend initially softened demand for rentals in high-cost regions like Orange County. However, as some companies now mandate in-office work, there’s a resurgence in local rental demand, particularly near employment hubs like Irvine and Anaheim. This dynamic underscores how national corporate policies directly impact local housing markets.

Another critical economic condition is the rising cost of homeownership, which has indirectly propped up rental demand. With mortgage rates hovering around 7% and home prices in Orange County averaging over $1 million, many would-be buyers are opting to rent instead. This "lock-in" effect keeps rental demand high, even as new multifamily units come online. Developers have responded by increasing supply, but the pace of construction hasn’t outstripped demand, preventing significant rent declines. For renters, this means negotiating power remains limited, especially in desirable school districts or near major employers.

Inflation and wage growth also play a pivotal role in the rental landscape. While Orange County’s median household income exceeds $90,000, inflation has eroded purchasing power, making rent affordability a growing concern. Landlords are walking a tightrope: raising rents too aggressively risks vacancies, but keeping them stagnant squeezes profit margins. As a result, rent increases have moderated to around 3-5% annually, down from double-digit spikes in 2021. Renters can leverage this trend by negotiating lease renewals or exploring newer properties offering move-in specials to fill vacant units.

Lastly, state and local policies are shaping the rental market in subtle but impactful ways. California’s Tenant Protection Act of 2019 caps annual rent increases at 5% plus inflation, providing some stability for tenants. However, Orange County’s exclusion from denser urban zoning laws limits the potential for rapid multifamily development, keeping supply constrained. Additionally, the region’s reliance on tourism and hospitality industries means economic downturns—like a recession—could disproportionately affect rental demand. For now, the market remains resilient, but renters should monitor these economic levers to anticipate future shifts.

The Clintons: Charging Secret Service Rent?

You may want to see also

Explore related products

![]()

Comparison of rent changes across neighborhoods

Rent trends in Orange County reveal a nuanced landscape, with fluctuations varying significantly across neighborhoods. For instance, coastal areas like Newport Beach and Laguna Beach have seen a slight dip in rents, attributed to a seasonal slowdown and increased inventory. Conversely, inland cities such as Anaheim and Santa Ana continue to experience upward pressure, driven by demand for more affordable housing options. This disparity underscores the importance of localized analysis when assessing rent changes.

To effectively compare rent changes across neighborhoods, start by identifying key metrics such as median rent, vacancy rates, and year-over-year growth. Tools like Zillow, Apartment List, and local real estate reports provide granular data for this purpose. For example, in Irvine, rents for single-family homes have stabilized due to new construction, while apartment rents in Fullerton have risen by 5% in the past year. Pairing these statistics with qualitative factors like school districts, crime rates, and proximity to employment hubs offers a comprehensive view.

A persuasive argument can be made for renters to target neighborhoods with declining or stabilizing rents, such as Huntington Beach, where a 2% decrease in median rent has been observed. However, caution is warranted in areas like Costa Mesa, where rents remain volatile due to ongoing development projects. Prospective renters should also consider long-term trends; neighborhoods with consistent rent growth, like Tustin, may offer better value despite higher upfront costs. Timing is critical—leasing during off-peak months (e.g., winter) can yield better deals in competitive markets.

Descriptively, the contrast between upscale and working-class neighborhoods is stark. In affluent areas like Coto de Caza, rents have plateaued as high-income earners opt for homeownership, reducing rental demand. Meanwhile, in Garden Grove, rents have climbed steadily as families seek budget-friendly options near job centers. This divergence highlights the role of socioeconomic factors in shaping rent dynamics. For practical guidance, renters should prioritize neighborhoods aligning with their lifestyle needs while monitoring local market conditions for optimal timing.

In conclusion, comparing rent changes across Orange County neighborhoods requires a multi-faceted approach. By leveraging data, understanding local drivers, and aligning with personal priorities, renters can navigate this complex market effectively. Whether seeking stability, affordability, or luxury, the key lies in pinpointing neighborhoods where rent trends align with individual goals.

Top Boat Rental Spots in Corpus Christi for Your Next Adventure

You may want to see also

Frequently asked questions

As of recent data, rents in Orange County have shown a slight decline in some areas, but the overall trend remains mixed, with certain neighborhoods still experiencing increases.

Factors include increased housing supply, economic uncertainties, and a shift in demand due to remote work allowing people to move to more affordable areas.

Areas with higher concentrations of luxury apartments or those farther from major employment hubs, such as parts of Irvine and Anaheim, are seeing more noticeable rent declines.

Predictions vary, but experts suggest that rents may stabilize or slightly decrease in the short term, depending on economic conditions and housing market trends.

Orange County’s rent trends are similar to other major California markets, with some areas experiencing slight decreases, though overall affordability remains a challenge compared to national averages.