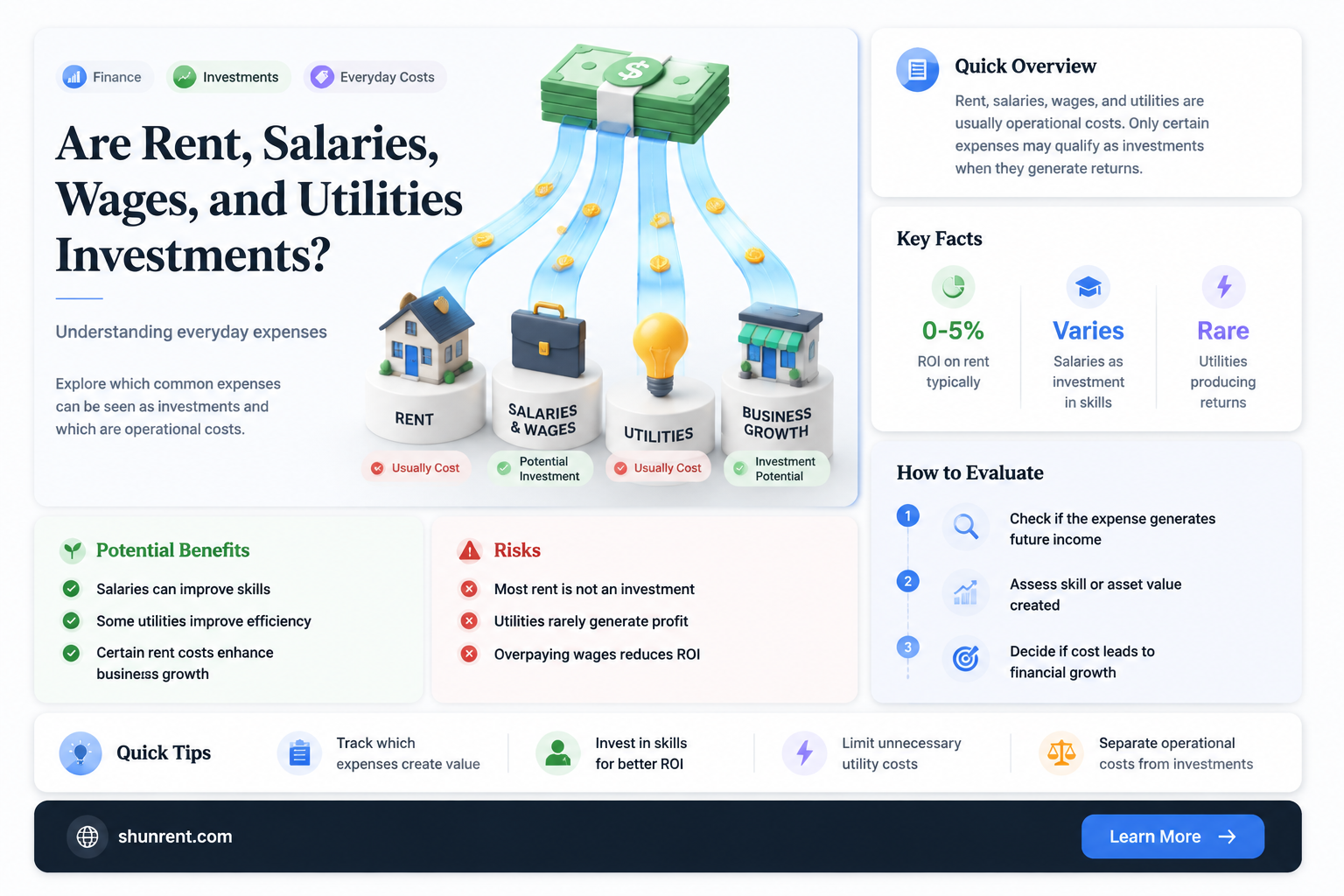

The classification of rent, salaries & wages, and utilities as investments is a nuanced topic that often sparks debate in financial and accounting circles. While these expenses are essential for business operations, they are typically categorized as operational costs rather than investments. Investments generally refer to expenditures made with the expectation of generating future income or appreciating in value, such as purchasing assets or funding projects. Rent, salaries, and utilities, however, are recurring expenses necessary to maintain day-to-day operations and do not inherently yield long-term financial returns. Understanding this distinction is crucial for accurate financial reporting and strategic planning, as misclassifying these expenses could distort a company’s financial health and investment strategy.

Explore related products

What You'll Learn

- Rent as Investment: Rent payments can be considered investments in business operations and real estate usage

- Salaries & Wages: Employee compensation is an investment in human capital and operational productivity

- Utilities Expenses: Utilities are operational costs, not investments, as they maintain business functionality

- Investment vs. Expense: Distinguishing between investments and expenses impacts financial reporting and tax treatment

- Return on Investment: Analyzing ROI for salaries, wages, and rent to assess financial efficiency

![]()

Rent as Investment: Rent payments can be considered investments in business operations and real estate usage

Rent payments, often viewed as a necessary expense, can be strategically reframed as investments in business operations and real estate usage. This perspective shifts the narrative from cost to value creation, particularly when rent enables access to prime locations, modern facilities, or scalable spaces that directly support operational efficiency and growth. For instance, a retail business leasing a storefront in a high-traffic area leverages rent to increase foot traffic and sales, effectively turning the payment into a revenue-generating tool. Similarly, a tech startup renting office space in a collaborative hub gains access to networking opportunities and shared resources, amplifying its potential for innovation and expansion.

Analyzing rent as an investment requires a focus on its return on investment (ROI). Businesses should evaluate how rent payments contribute to tangible outcomes such as increased productivity, customer reach, or brand visibility. For example, a manufacturing company renting a warehouse in a logistics-friendly zone reduces transportation costs and delivery times, directly improving profitability. This approach demands a shift from viewing rent as a fixed overhead to recognizing it as a strategic allocation of resources that drives operational excellence and competitive advantage.

To maximize rent as an investment, businesses must adopt a proactive approach. Negotiating lease terms that align with growth projections, such as flexible renewal options or rent escalation caps, ensures long-term affordability and stability. Additionally, investing in leased spaces through customizations or improvements can enhance functionality and asset value, even if the property is not owned. For instance, a restaurant upgrading its leased kitchen equipment not only improves operational efficiency but also positions itself for higher returns in the event of a buyout or expansion.

A comparative analysis highlights the contrast between rent as an expense versus an investment. While salaries and utilities are typically recurring costs with immediate operational benefits, rent uniquely bridges operational needs with long-term strategic goals. Unlike wages, which are directly tied to labor productivity, or utilities, which are essential but offer limited strategic value, rent provides access to assets that can appreciate in value or unlock new opportunities. For example, a company leasing a property in an up-and-coming commercial district may benefit from rising property values and increased market presence over time.

In conclusion, treating rent payments as investments requires a mindset shift and strategic planning. By aligning rent expenditures with business objectives, companies can transform a perceived liability into a powerful asset. Practical steps include conducting thorough cost-benefit analyses, optimizing lease agreements, and leveraging rented spaces to drive innovation and growth. This approach not only enhances financial performance but also positions businesses to thrive in dynamic real estate markets.

Boost Your Credit Score: Reporting Rent Payments to Experian Easily

You may want to see also

Explore related products

![]()

Salaries & Wages: Employee compensation is an investment in human capital and operational productivity

Employee compensation, encompassing salaries and wages, is fundamentally an investment in human capital. Unlike rent or utilities, which are operational expenses with immediate and tangible returns, salaries and wages are strategic outlays aimed at cultivating long-term value. When a company pays its employees, it is not merely covering labor costs but is actively investing in the skills, knowledge, and productivity of its workforce. This investment yields returns in the form of innovation, efficiency, and organizational growth, making it a cornerstone of sustainable business success.

Consider the analytical perspective: studies show that companies investing in competitive compensation packages experience a 20-30% increase in employee retention rates. This retention translates into reduced recruitment costs, minimized knowledge loss, and enhanced team cohesion. For instance, a tech firm that offers salaries 10-15% above industry averages may initially face higher payroll expenses but often sees a 25% boost in project completion rates and a 15% reduction in errors. These metrics underscore the direct correlation between compensation investment and operational productivity, proving that salaries and wages are not just costs but strategic assets.

From an instructive standpoint, businesses must approach employee compensation with a deliberate focus on ROI. Start by benchmarking salaries against industry standards and geographic cost-of-living indices. Implement performance-based incentives, such as profit-sharing or skill development stipends, to align compensation with productivity goals. For example, a manufacturing company could allocate 5% of its annual budget to wage increases tied to productivity metrics, ensuring that every dollar spent on compensation directly contributes to output gains. Regularly audit compensation structures to identify disparities and adjust for inflation, ensuring the investment remains competitive and impactful.

A persuasive argument for viewing salaries and wages as investments lies in their ability to foster employee engagement and loyalty. Research indicates that employees who perceive their compensation as fair are 85% more likely to go above and beyond their job descriptions. This discretionary effort drives innovation and problem-solving, which are critical for staying competitive in dynamic markets. For instance, a retail chain that introduced a 12% wage premium for customer service representatives saw a 40% increase in customer satisfaction scores within six months. Such outcomes demonstrate that investing in compensation is not just about retaining talent but about unlocking its full potential.

Finally, a comparative analysis highlights the distinction between salaries and wages as investments versus rent and utilities as expenses. While rent and utilities are necessary for operational continuity, they do not inherently generate value beyond their immediate use. In contrast, compensation investments compound over time, enhancing employee skills, morale, and productivity. For example, a software company that invests $50,000 annually in employee training and competitive wages may see a $150,000 increase in annual revenue through improved product quality and faster delivery times. This comparison reinforces the idea that salaries and wages are not just costs but strategic investments in a company’s most valuable asset: its people.

Understanding Rent Rebate Income Limits: Eligibility and Application Guide

You may want to see also

Explore related products

![]()

Utilities Expenses: Utilities are operational costs, not investments, as they maintain business functionality

Utilities expenses, such as electricity, water, and gas, are essential for keeping a business operational. These costs are not discretionary; they are necessary to maintain day-to-day functionality. For instance, a retail store requires lighting to display products, HVAC systems to ensure customer comfort, and internet connectivity for transactions. Without these utilities, the business would grind to a halt. This fundamental necessity categorizes utilities as operational costs rather than investments. Investments, by contrast, are expenditures made with the expectation of generating future returns, such as purchasing equipment or expanding marketing efforts. Utilities, however, are recurring expenses that do not directly contribute to revenue growth but are indispensable for sustaining operations.

To illustrate, consider a small café. The monthly electricity bill ensures the coffee machines, refrigerators, and lighting operate smoothly. While these utilities are critical for serving customers, they do not inherently increase the café’s earning potential. Instead, they enable the business to function at its current capacity. This distinction is crucial for financial planning. Misclassifying utilities as investments could lead to inaccurate budgeting, as investments typically involve a long-term strategy for growth, whereas utilities are immediate, ongoing expenses. Recognizing this difference helps business owners allocate resources more effectively, ensuring that operational needs are met without diverting funds from true growth opportunities.

From a financial management perspective, treating utilities as operational costs allows for better cost control and forecasting. Businesses can analyze utility bills to identify inefficiencies, such as excessive energy consumption, and implement measures to reduce waste. For example, switching to energy-efficient lighting or installing smart thermostats can lower costs without compromising functionality. These actions are operational improvements, not investments, as they focus on optimizing existing expenses rather than generating new revenue streams. By categorizing utilities correctly, businesses can prioritize spending on areas that directly impact growth, such as product development or employee training, while maintaining a lean operational budget.

A persuasive argument for this classification lies in the nature of business sustainability. Utilities are akin to the lifeblood of a company, ensuring it remains functional and compliant with health and safety standards. For instance, a manufacturing plant cannot operate without power, and a tech startup needs internet access to develop and deliver its services. While these expenses are recurring and necessary, they do not offer a return on investment in the traditional sense. Instead, they provide the foundation upon which investments can be made. By acknowledging utilities as operational costs, businesses can focus their investment strategies on initiatives that drive innovation, expand market reach, or enhance customer experience, thereby fostering long-term success.

In conclusion, utilities expenses are operational costs that maintain business functionality, not investments. This distinction is vital for accurate financial planning and resource allocation. By understanding the role of utilities, businesses can optimize their spending, ensure operational efficiency, and direct investments toward initiatives that genuinely contribute to growth. Practical steps, such as auditing utility usage and implementing cost-saving measures, can further enhance financial health. Ultimately, recognizing the true nature of utilities expenses empowers businesses to build a sustainable foundation while strategically pursuing opportunities for expansion and innovation.

Filing Rental Income in Your Tax Return: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Investment vs. Expense: Distinguishing between investments and expenses impacts financial reporting and tax treatment

In the realm of financial management, distinguishing between investments and expenses is crucial for accurate reporting and tax optimization. Rent, salaries, wages, and utilities are often categorized as expenses, but understanding their potential as investments can reshape financial strategies. For instance, rent paid for commercial property can be seen as an investment if it directly contributes to revenue generation, such as a retail store’s lease enabling sales. Similarly, salaries and wages invested in skilled employees can yield long-term returns through increased productivity and innovation. Utilities, while typically operational expenses, can be reframed as investments if they support energy-efficient systems that reduce future costs. This nuanced perspective highlights the importance of evaluating how expenditures align with long-term value creation.

Analyzing the tax implications further underscores the need for clear categorization. Expenses like utilities and wages are generally tax-deductible in the year they are incurred, providing immediate financial relief. Investments, however, may offer deferred tax benefits or depreciation allowances, depending on jurisdiction and asset type. For example, a business investing in renewable energy systems (initially classified as utilities) may qualify for tax credits or accelerated depreciation, turning a routine expense into a strategic financial move. Misclassification can lead to missed opportunities or compliance issues, emphasizing the need for meticulous assessment.

A comparative approach reveals the contrasting treatment of these items in financial statements. Expenses reduce net income on the income statement, reflecting immediate costs of operations. Investments, on the other hand, appear on the balance sheet as assets, signaling future economic benefits. For instance, a company’s decision to lease equipment (rent) rather than purchase it may be recorded as an expense, but if the lease improves operational efficiency, it could be argued as an investment in productivity. This duality demands a case-by-case evaluation, considering both the nature of the expenditure and its intended purpose.

To navigate this distinction effectively, businesses should adopt a structured approach. First, assess the long-term impact of each expenditure: Does it generate future revenue, enhance asset value, or improve operational efficiency? Second, consult tax regulations to identify potential benefits or pitfalls of classification. Third, maintain detailed documentation to support categorization decisions during audits. For example, a company could track how employee training (wages) correlates with increased sales, justifying it as an investment rather than a mere expense. This proactive methodology ensures financial accuracy and strategic alignment.

In conclusion, the line between investment and expense is not always clear-cut, particularly for items like rent, salaries, wages, and utilities. By scrutinizing their purpose, potential returns, and tax treatment, businesses can optimize financial reporting and resource allocation. This distinction is not merely semantic but a strategic imperative that influences profitability, compliance, and long-term growth.

Finding Rental Housing with a Felony: Strategies for Success

You may want to see also

Explore related products

![]()

Return on Investment: Analyzing ROI for salaries, wages, and rent to assess financial efficiency

Salaries, wages, and rent are often categorized as expenses rather than investments, but this perspective overlooks their potential to generate returns. Treating these costs as investments shifts the focus from mere expenditure to value creation. For instance, an employee’s salary can be viewed as an investment in productivity, innovation, and revenue generation. Similarly, rent for office space or equipment can be seen as an investment in operational efficiency and business scalability. To assess their financial efficiency, applying Return on Investment (ROI) analysis is critical. ROI in this context measures how effectively these expenditures contribute to measurable financial gains, such as increased revenue, cost savings, or improved profitability.

To calculate ROI for salaries and wages, start by identifying the direct and indirect returns generated by employees. Direct returns include revenue attributable to their work, while indirect returns encompass cost savings, process improvements, or enhanced customer satisfaction. For example, a sales team’s wages can be evaluated by comparing their total compensation to the revenue they generate. A simple formula is: (Net Profit from Employee’s Work / Total Compensation) × 100. If a salesperson earns $60,000 annually and generates $300,000 in net profit, their ROI is 400%. This metric helps businesses identify high-performing employees and optimize workforce allocation.

Rent ROI analysis requires a different approach, as its returns are often less direct. For commercial spaces, evaluate how the location and functionality of the property contribute to business performance. For instance, a retail store’s rent can be assessed by comparing foot traffic, sales per square foot, and customer retention rates to the rental cost. A formula like (Additional Revenue from Location / Annual Rent) × 100 can provide insight. If a store pays $50,000 in annual rent and attributes $200,000 in additional revenue to its prime location, the ROI is 300%. This analysis helps businesses determine whether their rental investments are justified or if alternatives like remote work or smaller spaces could yield better returns.

A cautionary note: ROI analysis for salaries, wages, and rent must account for qualitative factors that quantitative metrics may overlook. For example, employee morale, company culture, and long-term strategic value are difficult to quantify but significantly impact financial efficiency. Similarly, rent ROI should consider factors like lease flexibility, market trends, and future growth potential. Overlooking these elements can lead to short-sighted decisions that undermine long-term profitability. To mitigate this, complement ROI calculations with scenario planning and stakeholder feedback.

In conclusion, treating salaries, wages, and rent as investments and applying ROI analysis provides a framework for assessing their financial efficiency. By quantifying returns and considering qualitative factors, businesses can make informed decisions about resource allocation, workforce management, and real estate strategies. This approach not only optimizes current expenditures but also positions organizations for sustainable growth. Practical tips include regularly updating ROI calculations, benchmarking against industry standards, and aligning investment decisions with broader business objectives.

Top Food Warmer Rental Options in Fresno, CA: Your Guide

You may want to see also

Frequently asked questions

No, rent, salaries & wages, and utilities are typically classified as operating expenses rather than investments. They represent ongoing costs necessary to maintain business operations, not assets expected to generate future returns.

Yes, rent, salaries & wages, and utilities are generally tax-deductible as ordinary business expenses, as they are directly related to the operation and maintenance of a business.

Rent, salaries & wages, and utilities are recurring costs for day-to-day operations, while investment expenditures involve spending on assets (e.g., equipment, property) expected to provide long-term value or income.