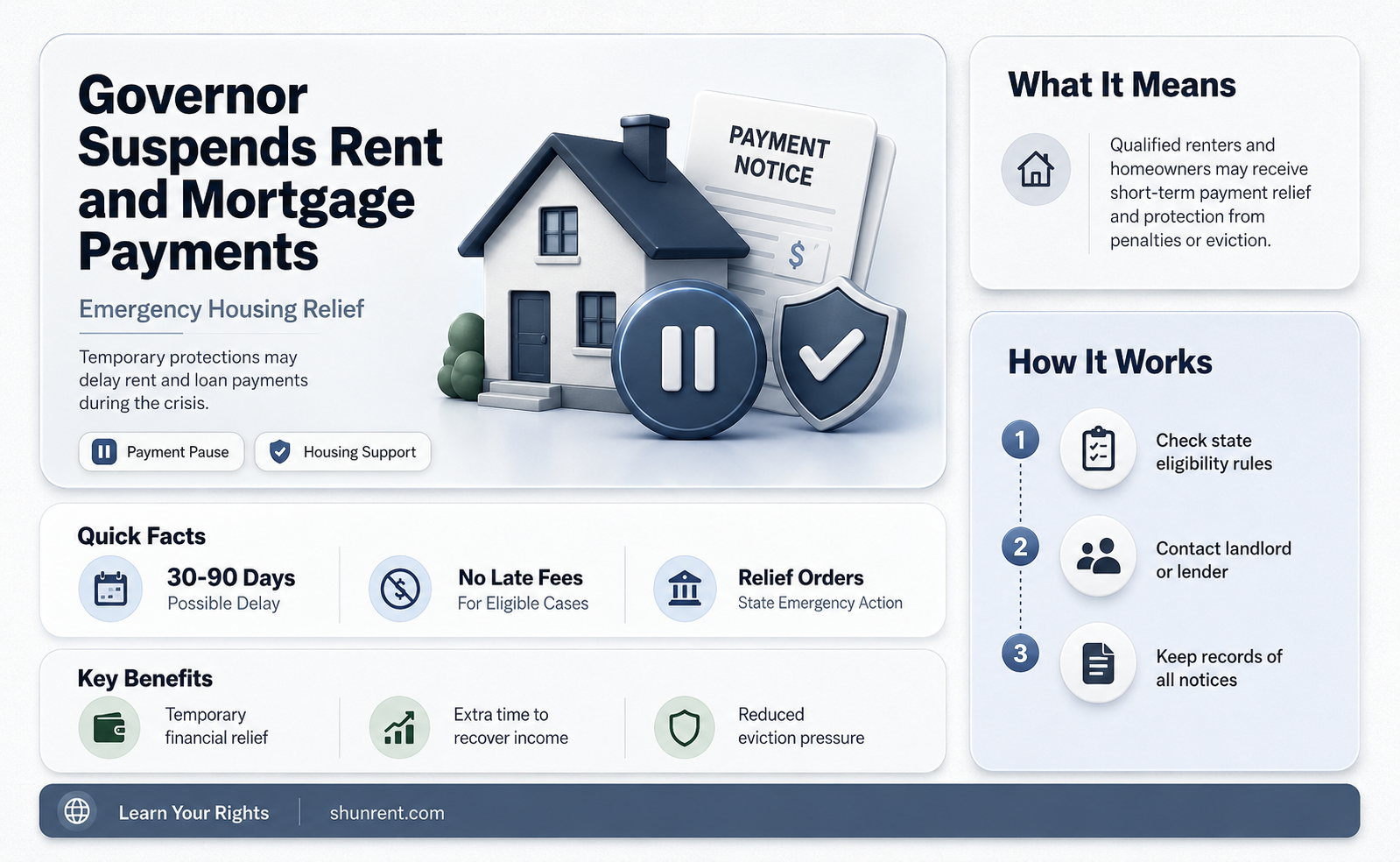

In response to the economic hardships caused by the COVID-19 pandemic, many individuals and families faced significant challenges in meeting their rent and mortgage obligations. As a result, there were widespread calls for government intervention to provide relief. The question of whether the governor suspended rent and mortgage payments became a critical issue, as such measures could offer temporary financial respite to those struggling to make ends meet. While some states and localities implemented moratoriums on evictions and foreclosures, the specifics of rent and mortgage suspensions varied widely, leaving many to wonder about the actions taken by their respective governors to address this pressing concern.

| Characteristics | Values |

|---|---|

| Rent Suspension | No statewide rent suspension; varies by local ordinances. |

| Mortgage Suspension | No statewide mortgage suspension; federal programs may apply. |

| Eviction Moratorium | Ended in most states; some local protections remain. |

| Foreclosure Moratorium | Ended in most states; federal programs may offer relief. |

| Rental Assistance Programs | Available in many states; funded by federal Emergency Rental Assistance. |

| Mortgage Relief Programs | Federal programs like forbearance under CARES Act still available. |

| State-Specific Measures | Varies by state; some governors implemented temporary protections. |

| Current Status (as of 2023) | Most pandemic-related suspensions and moratoriums have expired. |

| Local Variations | Cities and counties may have additional protections or programs. |

| Federal Influence | Federal policies (e.g., CARES Act) influenced state and local actions. |

Explore related products

What You'll Learn

- Rent Suspension Orders: Details on which states or regions have issued rent suspension orders

- Mortgage Relief Programs: Overview of available mortgage relief options for homeowners

- Eligibility Criteria: Who qualifies for rent or mortgage suspension during emergencies

- Duration of Relief: How long rent or mortgage suspensions typically last

- Legal Implications: Consequences for landlords or lenders during suspension periods

![]()

Rent Suspension Orders: Details on which states or regions have issued rent suspension orders

During the COVID-19 pandemic, several states and regions implemented rent suspension orders to alleviate financial strain on tenants. These measures varied widely in scope, duration, and enforcement, reflecting the unique economic and political landscapes of each area. For instance, California enacted the Tenant, Homeowner, and Small Landlord Relief and Stabilization Act of 2020, which temporarily halted evictions for non-payment of rent and provided rental assistance programs. Similarly, New York issued an eviction moratorium that protected tenants who could demonstrate pandemic-related hardship, though it did not outright suspend rent obligations.

Analyzing these orders reveals a common thread: they were designed as temporary relief measures, not permanent solutions. Most rent suspension orders were tied to specific timelines, such as the duration of a declared state of emergency or a fixed number of months. For example, Illinois’s eviction moratorium lasted until May 2021, while Washington State’s protections extended through October 2021. These timelines often coincided with federal stimulus efforts, such as the CARES Act, which provided direct payments and enhanced unemployment benefits to help tenants meet their financial obligations.

A comparative look at these policies highlights the tension between tenant protections and landlord viability. States like New Jersey and Massachusetts balanced tenant relief with landlord assistance programs, recognizing that property owners also faced financial challenges. In contrast, regions with stricter rent suspension orders, such as the District of Columbia, faced legal challenges from landlord associations arguing that such measures violated property rights. This underscores the need for comprehensive policies that address both sides of the rental equation.

Practical tips for tenants navigating rent suspension orders include documenting all communications with landlords, understanding the specific terms of local moratoriums, and applying for available rental assistance programs. For instance, tenants in states like Oregon or Minnesota could access emergency rental assistance funds to cover missed payments, reducing the risk of future eviction. Landlords, meanwhile, should explore state-specific relief programs, such as property tax deferrals or low-interest loans, to mitigate financial losses during moratorium periods.

In conclusion, rent suspension orders were a critical tool in stabilizing housing markets during the pandemic, but their effectiveness varied by region. Tenants and landlords alike must stay informed about local policies and available resources to navigate these challenges. As economic conditions evolve, policymakers must continue to strike a balance between protecting vulnerable populations and ensuring the sustainability of the rental housing sector.

Exploring Mimi's Ethnicity in Rent: Hispanic or Not?

You may want to see also

Explore related products

![]()

Mortgage Relief Programs: Overview of available mortgage relief options for homeowners

In the wake of economic uncertainties, homeowners often find themselves grappling with mortgage payments, prompting the question: What relief options are available? While governors may not universally suspend rent and mortgage payments, various mortgage relief programs have been instituted to provide financial breathing room. These programs, often tailored to specific circumstances, can include forbearance plans, loan modifications, and government-backed assistance. Understanding these options is crucial for homeowners seeking to navigate financial hardships without risking foreclosure.

Forbearance programs, for instance, allow homeowners to pause or reduce mortgage payments for a set period, typically 3 to 6 months, with the option to extend. This is not a forgiveness of debt but a temporary reprieve, often requiring a lump-sum payment or repayment plan afterward. Homeowners should contact their lenders immediately to discuss eligibility, as delays can complicate the process. For example, Fannie Mae and Freddie Mac-backed loans offer forbearance plans with no late fees, but terms vary by lender.

Loan modification programs, on the other hand, provide long-term solutions by adjusting the mortgage terms to make payments more manageable. This could involve reducing the interest rate, extending the loan term, or even forgiving a portion of the principal balance. Programs like the Home Affordable Modification Program (HAMP) have helped thousands of homeowners, though eligibility criteria are strict. Applicants must provide proof of income, a hardship letter, and other documentation to qualify.

Government-backed relief programs, such as those offered by the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), cater to specific demographics. FHA’s Special Forbearance program assists homeowners with FHA-insured loans facing long-term financial hardships, while the VA offers repayment plans and loan modifications for veterans. State-specific programs, like California’s Homeowner Assistance Fund, provide grants to cover past-due mortgage payments, property taxes, and insurance.

Practical tips for homeowners include maintaining open communication with lenders, exploring all available options, and seeking advice from HUD-approved housing counselors. These counselors offer free guidance on navigating relief programs and avoiding scams. Additionally, homeowners should review their financial situations regularly to determine the most suitable relief option. While mortgage relief programs may not be as sweeping as a gubernatorial suspension of payments, they provide targeted support to help homeowners weather financial storms.

CHR in Enfield, CT: Rent Assistance Available?

You may want to see also

Explore related products

![]()

Eligibility Criteria: Who qualifies for rent or mortgage suspension during emergencies

During emergencies, the suspension of rent or mortgage payments is often a temporary relief measure aimed at helping those most affected by unforeseen circumstances such as natural disasters, pandemics, or economic downturns. Eligibility criteria for such suspensions vary widely depending on the jurisdiction, the nature of the emergency, and the specific policies enacted by the governor or relevant authorities. Typically, these criteria are designed to target individuals and households facing immediate financial hardship, ensuring that relief reaches those who need it most. Understanding these criteria is crucial for anyone seeking assistance during a crisis.

One common eligibility factor is proof of income loss directly related to the emergency. For instance, during the COVID-19 pandemic, many states required applicants to demonstrate a significant reduction in income due to job loss, reduced work hours, or business closures. Documentation such as pay stubs, unemployment benefits statements, or business income records might be necessary to qualify. In some cases, eligibility extends to essential workers who incurred additional expenses, such as childcare, due to their roles during the crisis. This criterion ensures that relief is directed toward those whose financial stability has been most severely impacted.

Another key factor is the type of housing and the terms of the lease or mortgage. Renters and homeowners may face different eligibility requirements. For example, renters might need to provide proof of tenancy, such as a lease agreement, while homeowners may need to show that their mortgage is their primary residence. Additionally, some programs exclude properties owned by large corporations or investment firms, focusing instead on individual homeowners and small landlords. This distinction aims to prevent misuse of funds and prioritize relief for those who rely on the property for personal housing.

Geographic location often plays a role in eligibility, as certain areas within a state may be more severely affected by the emergency. For instance, after a hurricane, residents in declared disaster zones might automatically qualify for rent or mortgage suspension, while those in less-affected regions may not. This targeted approach ensures that resources are allocated efficiently to the hardest-hit communities. It also underscores the importance of staying informed about local declarations and updates from government agencies.

Finally, eligibility criteria often include a time-bound component, reflecting the temporary nature of the relief. For example, a governor might suspend rent or mortgage payments for a specific period, such as 60 or 90 days, with the possibility of extension based on ongoing assessments of the emergency. Applicants may need to reapply or provide updated documentation to continue receiving assistance. This structure balances immediate relief with long-term sustainability, encouraging individuals to seek permanent solutions as conditions improve.

In summary, eligibility for rent or mortgage suspension during emergencies hinges on a combination of income loss, housing type, geographic impact, and the duration of the crisis. By understanding these criteria, individuals can better navigate the application process and access the support they need during challenging times. Always consult official government resources or legal advisors for the most accurate and up-to-date information specific to your situation.

When Does Rent-A-Center Involve Police for Unpaid Rentals?

You may want to see also

Explore related products

![]()

Duration of Relief: How long rent or mortgage suspensions typically last

The duration of rent or mortgage suspensions varies widely depending on the jurisdiction, the severity of the crisis prompting the relief, and the specific terms set by the governor or legislative body. Typically, such measures are temporary, designed to provide immediate financial breathing room during emergencies like natural disasters, pandemics, or economic downturns. For instance, during the COVID-19 pandemic, some states implemented moratoriums lasting 3 to 12 months, with extensions based on ongoing assessments of public need. Understanding these timelines is crucial for both tenants and homeowners to plan their finances effectively.

Analyzing historical examples reveals patterns in how these suspensions are structured. In California, Governor Gavin Newsom’s executive order in 2020 initially suspended evictions for non-payment of rent for a 60-day period, later extended through legislative action until September 2021. Similarly, New York’s eviction moratorium lasted over a year, with phased rollbacks tied to federal relief fund distribution. These cases highlight how initial short-term measures often evolve into longer-term policies as crises persist, emphasizing the need for flexibility in policy design.

For those seeking relief, it’s essential to monitor not just the start date of a suspension but also its expiration and any conditions for renewal. Some states require tenants to declare financial hardship or provide proof of pandemic-related income loss to qualify for extended protection. Homeowners, meanwhile, may face differing timelines for mortgage forbearance, often ranging from 3 to 18 months, depending on federal programs like those offered by the CARES Act. Proactive communication with landlords or lenders is key to navigating these deadlines.

Comparatively, international examples offer additional insights. In countries like Germany and Canada, rent freezes or moratoriums were often shorter, lasting 3 to 6 months, but were paired with robust financial aid programs to ensure long-term stability. This contrasts with U.S. policies, which sometimes relied on extended moratoriums without sufficient accompanying support. Such comparisons underscore the importance of balancing immediate relief with sustainable solutions to prevent future financial strain.

In conclusion, while the typical duration of rent or mortgage suspensions ranges from a few months to over a year, the specifics depend heavily on local policies and the nature of the crisis. Tenants and homeowners should stay informed about both the initial terms and potential extensions, leveraging available resources to prepare for the eventual resumption of payments. By understanding these timelines, individuals can better manage their financial obligations during uncertain times.

Rent a 12-Passenger Van in Phoenix, AZ: Top Locations

You may want to see also

Explore related products

![]()

Legal Implications: Consequences for landlords or lenders during suspension periods

During rent and mortgage suspension periods, landlords and lenders face immediate cash flow disruptions, but the legal implications extend far beyond temporary financial strain. For landlords, eviction moratoriums often prohibit removing non-paying tenants, creating a paradox where property owners must maintain services (e.g., utilities, maintenance) without income. Lenders, meanwhile, confront deferred mortgage payments, which can disrupt securitization agreements and trigger technical defaults in loan portfolios. Both parties must navigate these constraints while ensuring compliance with rapidly evolving state and federal regulations, or risk legal penalties.

Consider the analytical perspective: suspension policies often shift risk asymmetrically. Landlords, particularly small-scale owners, bear the brunt of uncollected rent, while lenders may offset losses through federal relief programs or loan forbearance terms. However, lenders face long-term risks if deferred payments accrue interest or balloon, potentially increasing borrower defaults post-suspension. This imbalance underscores the need for landlords to document all communications with tenants and for lenders to restructure loans proactively, ensuring transparency in repayment terms to avoid litigation.

From a practical standpoint, landlords should prioritize negotiating partial payment plans with tenants during suspension periods, as courts may later consider good-faith efforts in eviction proceedings. For instance, offering a 30% rent reduction in exchange for consistent partial payments can mitigate losses while demonstrating flexibility. Lenders, on the other hand, should audit loan portfolios to identify high-risk borrowers and proactively offer forbearance agreements with clear end dates and repayment terms. Both parties must ensure all agreements are in writing and comply with state-specific laws, such as California’s requirement for landlords to provide written notices before pursuing unpaid rent post-moratorium.

A comparative analysis reveals that jurisdictions with robust tenant protections, like New York’s COVID-19 Emergency Eviction and Foreclosure Prevention Act, impose stricter obligations on landlords, including mandatory mediation before eviction filings. In contrast, states with weaker tenant laws may leave landlords more vulnerable to prolonged occupancy without recourse. Lenders in these regions must balance foreclosure actions with reputational risks, as aggressive tactics during suspension periods can invite regulatory scrutiny or public backlash.

In conclusion, suspension periods demand strategic adaptability from landlords and lenders. Landlords should focus on preserving tenant relationships while documenting all efforts to collect rent, positioning themselves favorably in potential legal disputes. Lenders must balance short-term liquidity concerns with long-term portfolio health, leveraging federal programs like the CARES Act to restructure loans without triggering defaults. By proactively addressing these legal implications, both parties can minimize financial and legal exposure during and after suspension periods.

Renting vs. Leasing in Mexico: Key Differences Explained

You may want to see also

Frequently asked questions

It depends on the state and specific executive orders. Some governors issued temporary eviction moratoriums or rent relief programs, but rent suspension was rare.

No, governors do not have the authority to suspend mortgage payments. However, federal programs like CARES Act forbearance or lender-specific relief options may apply.

Some governors implemented temporary eviction moratoriums during emergencies, but these protections vary by state and have expiration dates.

No, gubernatorial orders typically delayed payments or evictions temporarily but did not forgive rent or mortgage debt. Tenants and homeowners remain responsible for repayment.