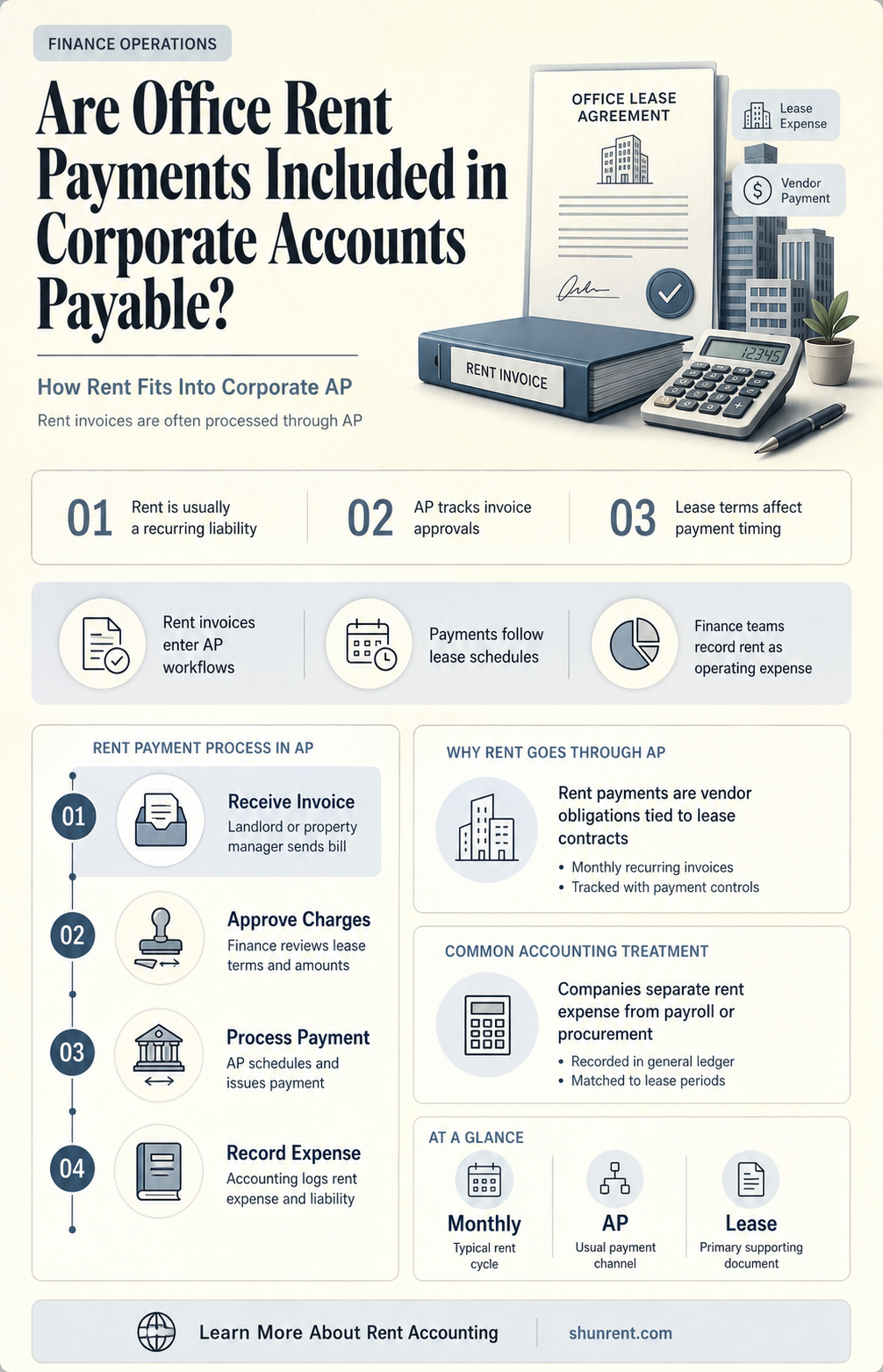

Corporate accounts payable encompass a wide range of financial obligations that a company owes to its creditors, typically arising from the purchase of goods or services on credit. One common question that arises is whether office rent is included in accounts payable. Generally, office rent is considered a short-term liability and is indeed part of a company’s accounts payable, as it represents a recurring expense that must be settled within a specified period, usually monthly or quarterly. This classification ensures that rent payments are accurately tracked and managed alongside other operational expenses, providing a comprehensive view of the company’s financial commitments. However, it’s important to note that the treatment of office rent may vary depending on accounting practices, lease agreements, and the specific policies of the organization.

| Characteristics | Values |

|---|---|

| Definition | Corporate accounts payable refers to short-term debts owed by a company to suppliers, vendors, or service providers for goods/services received on credit. |

| Inclusion of Office Rent | Office rent is typically not included in corporate accounts payable. |

| Reason for Exclusion | Office rent is usually classified as a lease liability or operating expense, not a trade payable. |

| Accounting Treatment | Rent is recorded under operating expenses in the income statement and as a lease liability on the balance sheet (under ASC 842 or IFRS 16). |

| Accounts Payable Scope | Accounts payable primarily covers trade payables (e.g., supplier invoices, utilities) with short repayment terms (usually 30-90 days). |

| Office Rent Payment Terms | Rent payments are often long-term commitments (e.g., monthly or annually) and are not considered short-term payables. |

| Financial Statement Classification | Office rent: Operating Expenses (Income Statement) and Lease Liability (Balance Sheet). Accounts Payable: Current Liability (Balance Sheet). |

| Example | If a company pays $5,000 monthly rent, it is recorded as rent expense and lease liability, not accounts payable. |

| Exception | If rent is paid in arrears and due within the accounts payable period, it might temporarily appear in accounts payable, but this is rare. |

Explore related products

What You'll Learn

![]()

Definition of Accounts Payable

Accounts Payable (AP) is a fundamental concept in corporate finance, representing a company's short-term obligations to pay off debts to creditors or suppliers. These debts typically arise from the purchase of goods or services on credit, and they are expected to be paid within a specified period, usually within 12 months. Understanding what constitutes Accounts Payable is crucial for accurate financial reporting and effective cash flow management.

In the context of corporate expenses, a common question arises: does office rent fall under Accounts Payable? To answer this, let's dissect the definition further. Accounts Payable specifically refers to liabilities that result from the acquisition of goods or services directly related to the company's operations. Office rent, while an essential operational expense, is typically classified as a long-term liability or a separate line item in financial statements, such as "Rent Payable" or "Operating Lease Liability." This distinction is important because it affects how these expenses are recorded and managed in a company's financial system.

For instance, consider a corporation that leases office space for its operations. The monthly rent payment is a recurring expense, but it is not directly tied to the purchase of goods or services from suppliers. Instead, it is a contractual obligation to the landlord. Therefore, while office rent is a critical component of a company's financial commitments, it is generally not included in the Accounts Payable category. Instead, it is accounted for separately to maintain clarity and accuracy in financial reporting.

From a practical standpoint, segregating office rent from Accounts Payable allows businesses to better track and manage their financial obligations. Accounts Payable often involves multiple vendors and invoices with varying due dates, making it a dynamic and frequently updated account. In contrast, rent payments are usually fixed and predictable, making them more suitable for separate tracking. This separation also aids in financial analysis, enabling stakeholders to assess the company's short-term liquidity and long-term lease commitments independently.

In conclusion, while office rent is a vital corporate expense, it does not typically fall under the definition of Accounts Payable. Accounts Payable is reserved for short-term debts arising from the purchase of goods or services, whereas office rent is generally classified as a separate long-term liability. This distinction is essential for accurate financial reporting, effective cash flow management, and informed decision-making. By understanding and applying this definition, businesses can maintain a clear and organized financial structure, ensuring that all obligations are properly accounted for and managed.

Richmond TX Folding Chair Rentals: Top Spots for Event Seating

You may want to see also

Explore related products

![]()

Office Rent Classification

Office rent is a significant expense for corporations, but its classification in accounts payable can vary depending on accounting practices and industry standards. Typically, office rent is categorized as an operating expense, reflecting its role in maintaining day-to-day business operations. This classification ensures that rent payments are recorded accurately in financial statements, providing a clear picture of a company’s operational costs. For instance, under the Generally Accepted Accounting Principles (GAAP), rent is often recorded as a short-term liability in accounts payable if it is due within a year, while long-term lease obligations may be treated differently.

Analyzing the classification further, it’s crucial to distinguish between prepaid rent and accrued rent. Prepaid rent occurs when a company pays rent in advance, requiring it to be recorded as a current asset until the rental period begins. Conversely, accrued rent arises when rent is owed but not yet paid, appearing as a liability in accounts payable. This distinction ensures compliance with accrual accounting principles, where expenses are matched to the period in which they are incurred, not when they are paid. For example, if a company pays six months of rent upfront, only the portion corresponding to the current accounting period is expensed, while the remainder is treated as a prepaid asset.

From a practical standpoint, corporations must carefully review lease agreements to determine the appropriate classification of office rent. Some leases include variable components, such as maintenance fees or property taxes, which may need to be separated from the base rent for accurate reporting. Additionally, the adoption of accounting standards like ASC 842 (for U.S. companies) or IFRS 16 (internationally) has introduced new rules for lease accounting, requiring most leases to be recognized on the balance sheet. Under these standards, office rent is no longer simply an expense but creates both a lease liability and a right-of-use asset, fundamentally changing its classification in accounts payable.

A comparative perspective reveals that small businesses and large corporations may handle office rent classification differently. Small businesses often prioritize simplicity, treating rent as a straightforward operating expense without delving into complex lease accounting. In contrast, larger corporations with multiple lease agreements must adopt more sophisticated methods to ensure compliance with regulatory requirements. For instance, a multinational corporation with offices in various countries must navigate differing tax laws and accounting standards, potentially leading to variations in how office rent is classified across its global operations.

In conclusion, office rent classification in corporate accounts payable is not a one-size-fits-all approach. It requires a nuanced understanding of accounting principles, lease agreements, and regulatory standards. By accurately classifying office rent, companies can maintain financial transparency, comply with reporting requirements, and make informed decisions about their operational costs. Whether treating rent as a short-term liability, a prepaid asset, or a lease obligation, the key is consistency and adherence to established accounting practices.

Negotiating Lower Rent During Property Ownership Transitions: A Tenant's Guide

You may want to see also

Explore related products

$13.85

![]()

Short-Term vs. Long-Term Liabilities

Corporate accounts payable often include office rent, but the classification of this liability depends on its term. Understanding the distinction between short-term and long-term liabilities is crucial for accurate financial reporting and strategic planning. Short-term liabilities, also known as current liabilities, are obligations due within one year or the operating cycle, whichever is longer. Office rent typically falls into this category if the lease agreement spans less than a year or is paid monthly. For instance, a 12-month lease with monthly payments would be recorded as a short-term liability, with the current portion (next month’s rent) listed under accounts payable and the remaining balance under other current liabilities.

In contrast, long-term liabilities extend beyond one year and include obligations like multi-year leases or loans. If a company signs a five-year office lease, the portion of rent due beyond the next 12 months is classified as a long-term liability. This distinction is vital for assessing liquidity and solvency. Short-term liabilities directly impact cash flow and working capital, while long-term liabilities reflect the company’s ability to meet future obligations without disrupting operations. For example, a startup with high short-term liabilities, including office rent, may face liquidity challenges if revenue falls short, whereas a long-term lease provides stability but ties up resources over time.

Analyzing the term of office rent and other liabilities helps stakeholders gauge financial health. Short-term liabilities require immediate attention, as they must be settled with current assets. Companies often prioritize managing these obligations through efficient cash flow management, such as negotiating payment terms with landlords or suppliers. Long-term liabilities, however, allow for strategic planning, enabling businesses to invest in growth while spreading costs over time. For instance, a company might opt for a long-term lease to secure prime office space at a fixed rate, protecting against rent increases but committing to a long-term financial obligation.

Practical tips for managing these liabilities include regularly reviewing lease agreements to identify opportunities for renegotiation or early termination clauses. Companies should also align lease terms with their business cycle to avoid overcommitting resources. For short-term liabilities, maintaining a cash reserve equivalent to 3–6 months of operating expenses, including rent, can provide a buffer during downturns. Conversely, long-term liabilities should be structured to match expected cash flows, ensuring payments remain manageable as the business grows. By carefully classifying and managing office rent and other liabilities, companies can optimize their financial position and support sustainable growth.

Summit Art Space Akron Ohio: Unveiling Current Rent Details

You may want to see also

Explore related products

![]()

Accounting Treatment for Rent

Rent expenses are a fundamental component of corporate accounts payable, particularly for office spaces. The accounting treatment for rent hinges on the timing of payment and the lease agreement’s structure. Under accrual accounting, rent is recognized as an expense in the period it is incurred, not when paid. For example, if a company pays quarterly rent in advance, the expense is spread evenly over the three months, ensuring each month reflects its share of the cost. This method aligns with the matching principle, pairing expenses with the revenues they help generate.

Prepaid rent, a common scenario in corporate leases, requires careful handling. When a company pays rent upfront for a future period, it is recorded as a current asset on the balance sheet. As the rental period progresses, the asset is gradually expensed. For instance, a $12,000 annual rent payment made in January would be recorded as a $1,000 monthly expense, reducing the prepaid rent asset by the same amount each month. This approach ensures financial statements accurately reflect the company’s financial position and performance.

The treatment of rent also varies based on lease classification under accounting standards like ASC 842 or IFRS 16. Operating leases, where the lessor retains ownership, result in straight-line rent expense recognition. Finance leases, however, require the lessee to recognize a right-of-use asset and a lease liability. For example, a 5-year office lease with annual payments of $50,000 would create a $250,000 liability and a corresponding asset, with the expense amortized over the lease term. This distinction is critical for compliance and financial reporting accuracy.

Practical tips for managing rent accounting include maintaining a rent schedule to track payment due dates, lease terms, and escalation clauses. Automating expense allocation through accounting software can reduce errors and save time. Additionally, regularly reviewing lease agreements for variable payments, such as common area maintenance (CAM) charges, ensures all rent-related expenses are captured. Proper documentation and reconciliation of rent payments to lease agreements are essential for audit purposes and financial transparency.

In conclusion, the accounting treatment for rent in corporate accounts payable demands precision and adherence to accounting standards. By understanding the nuances of accrual accounting, prepaid rent, and lease classifications, companies can ensure their financial statements accurately reflect their obligations and expenses. Effective management of rent accounting not only supports compliance but also provides valuable insights into cash flow and operational costs.

Affordable NYC Living: Tips to Rent Under $1000 Monthly

You may want to see also

Explore related products

![]()

Impact on Financial Statements

Office rent is a quintessential example of a liability that falls under corporate accounts payable, and its treatment has a profound impact on financial statements. When a company leases office space, the rent expense is typically recorded as a short-term liability until it is paid. This classification directly affects the balance sheet, increasing total liabilities and, consequently, reducing working capital. For instance, if a company has a monthly rent of $10,000, this amount appears as a current liability until the payment is made, reflecting the company’s obligation to the landlord.

Analyzing the income statement reveals another layer of impact. Rent expense is recognized in the period it is incurred, reducing net income. This treatment aligns with the accrual accounting principle, ensuring expenses are matched with the revenues they help generate. For example, a tech startup with annual rent of $120,000 would report $10,000 monthly as an operating expense, lowering profitability but providing a realistic view of operational costs. Investors and stakeholders scrutinize this line item to assess cost management and operational efficiency.

The cash flow statement also reflects the dynamics of office rent payments. When rent is paid, it is recorded as a cash outflow from operating activities, reducing net cash flow. However, the timing of payment versus recognition creates a distinction between accrual and cash-based reporting. For instance, if rent is paid quarterly but accrued monthly, the cash flow statement will show a lump-sum outflow, while the income statement spreads the expense evenly. This discrepancy highlights the importance of reconciling accrual-based financials with actual cash movements.

A comparative analysis of companies with varying rent structures can reveal strategic financial decisions. Companies opting for long-term leases may capitalize a portion of rent as a prepaid asset, deferring expense recognition. Conversely, short-term leases are fully expensed, impacting immediate profitability. For example, a company with a 10-year lease might capitalize $50,000 annually as a right-of-use asset, while expensing the remaining $70,000. This approach smooths income statement volatility but complicates balance sheet interpretation, requiring careful scrutiny by financial analysts.

In conclusion, office rent as part of corporate accounts payable significantly influences financial statements through its treatment as a liability, expense, and cash outflow. Proper classification and recognition are critical for accurate financial reporting and stakeholder analysis. Companies must balance compliance with accounting standards and strategic presentation to reflect their financial health accurately. For practitioners, understanding these nuances ensures transparency and aids in making informed decisions.

Essential Requirements for Renting a Motel 6 Room: A Quick Guide

You may want to see also

Frequently asked questions

Yes, corporate accounts payable typically include office rent as it is a recurring expense that a company owes to its landlord or property management.

Office rent is usually considered a short-term liability in accounts payable, as it is often paid monthly or quarterly and does not extend beyond a year.

Office rent is recorded as an expense in the income statement and as a liability in the balance sheet until it is paid, typically under the accounts payable or accrued expenses section.

No, prepaid office rent is not included in accounts payable. It is recorded as a prepaid asset on the balance sheet since the payment has already been made for future rent periods.