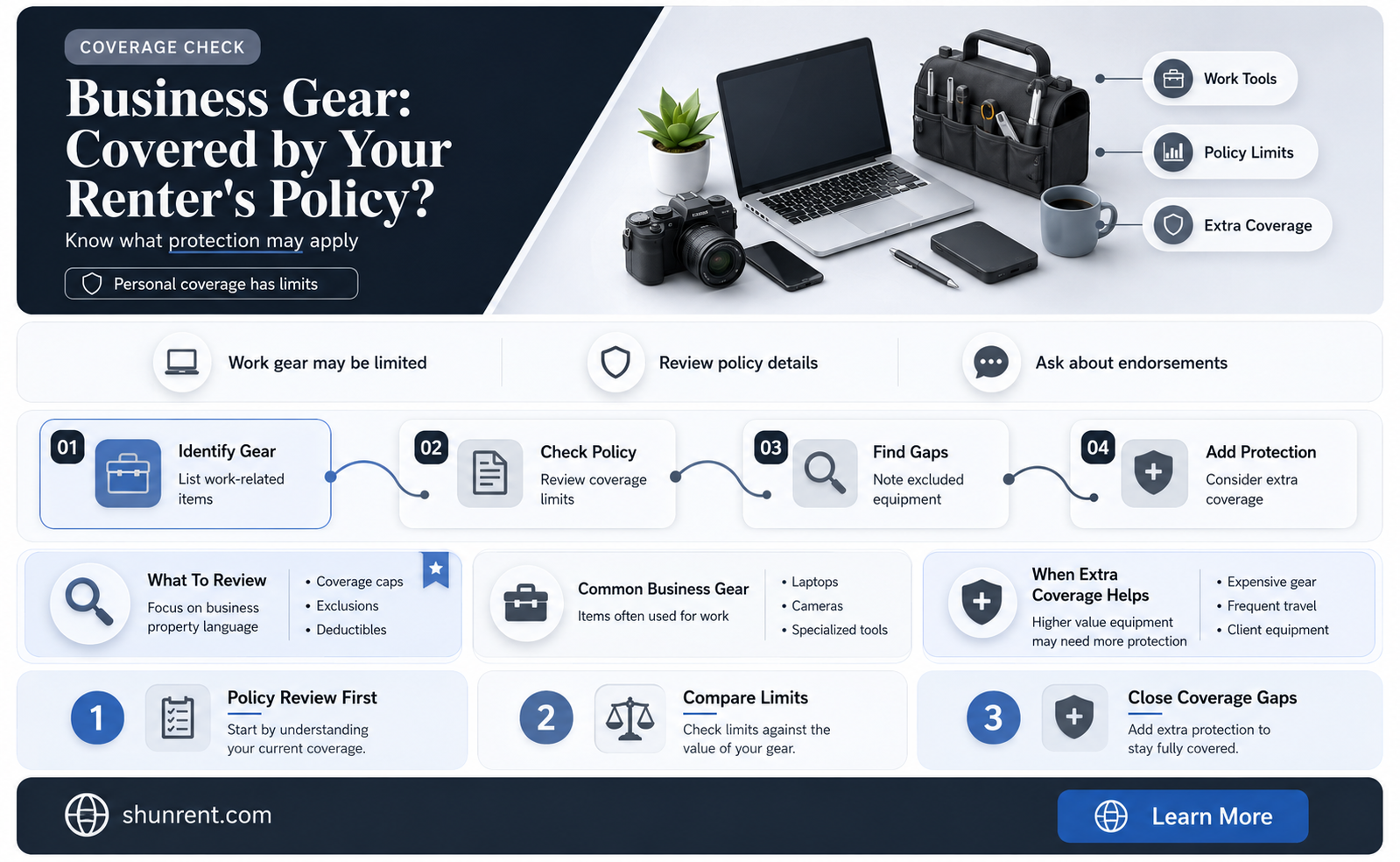

If you run a business from a rented property, it's important to understand what insurance coverage you need. A renter's policy may not cover business operations, and you might need to purchase additional insurance to protect your business. This is because a renter's policy is designed to cover the contents of a rented property and may not extend to business activities. Landlords may require tenants to have liability insurance to protect themselves from the cost of accidents or injuries. Small business owners can purchase business renter's insurance, which combines general liability insurance, commercial property insurance, and business interruption insurance. This type of insurance helps protect the property, team, and operations of a business. The cost of business renter's insurance varies depending on factors such as business size, equipment, number of employees, and location. It's important to carefully review the terms of any insurance policy to understand what is covered and what additional coverage may be needed.

| Characteristics | Values |

|---|---|

| Who needs business renters insurance? | Businesses that rent property for their operations, such as offices, storefronts, or warehouses. |

| What does business renters insurance cover? | Business renters insurance can include general liability insurance, commercial property insurance, and business interruption insurance. Commercial property insurance covers owned or rented buildings, office spaces, and equipment. |

| What is not covered by business renters insurance? | Business renters insurance does not typically cover flood or earthquake damage, sewer and drain backups, or business merchandise. |

| What are the benefits of business renters insurance? | Business renters insurance can help protect your property, team, and operations. It can also provide liability coverage for medical and legal costs if someone is injured on your property. |

| How much does business renters insurance cost? | The cost of business renters insurance varies depending on business size, equipment, number of employees, and location. A Business Owner's Policy (BOP) combining multiple types of insurance typically costs around $1,200 annually. |

Explore related products

What You'll Learn

![]()

Commercial property insurance

The cost of commercial property insurance can vary depending on several factors, such as the location of your business, the construction materials used, occupancy rates, and the presence of safety features. Businesses located in high-crime areas or those with higher occupancy rates may pay higher insurance costs. Installing safety features like smoke detectors and burglar alarms can help lower your insurance rates.

When considering commercial property insurance, it is essential to assess your business's needs and risks. Determine the assets you want to protect, including buildings, equipment, inventory, and other physical property. Identify potential risks, including industry-specific hazards and weather events common in your area. Commercial property insurance does not cover all incidents, excluding claims involving earthquakes, hurricanes, and floods.

Rent Expense: What's the Ideal Percentage of Your Income?

You may want to see also

Explore related products

![]()

Business interruption insurance

The national average cost of business interruption insurance is $1200 per year, and it is essential for landlords to understand the terms, exclusions, and restoration period of their policy. Endorsements may be necessary for specific circumstances, such as the COVID-19 pandemic, which led to special endorsements or exclusions related to civil authority orders. Business interruption insurance can be a standalone policy or an add-on to a casualty policy, and it often requires a "suspension" of business "operations" resulting in a "rental value" loss to trigger coverage.

While business interruption insurance is primarily discussed in the context of landlords and rental properties, it is worth noting that business owners may also benefit from this type of insurance. Business interruption insurance can help business owners manage their liability and financial exposure, especially when renting or borrowing equipment. For example, a tree care company renting equipment may rely on their Commercial General Liability coverage to pay for injuries or damage caused while using rented equipment. Additionally, their Inland Marine/Contractor's Equipment policy may provide some coverage for rented equipment, typically around $25,000.

When considering business interruption insurance, it is important to review the specific terms and conditions of the policy. Understand the obligations of any rental contracts, including the requirement to replace rented equipment with a new, similar make and model. Additionally, be mindful of reporting conditions that may require disclosing the total amount spent on leased or borrowed contractor's equipment within a specified timeframe. By carefully reviewing the policy details and seeking clarification from insurance agents, individuals can make informed decisions about their coverage needs.

Rent the Runway: Shipping Speed and Efficiency

You may want to see also

Explore related products

![]()

Business income insurance

The coverage period for business income insurance typically includes a waiting period or a monetary deductible, and it may be extended beyond the completion of repairs for a specified number of days. It's important to carefully review the terms and conditions of the policy, as well as any endorsements or additional protections that can be added.

In addition to business income insurance, it's worth noting that renters' insurance typically does not cover business equipment or property used for business purposes. If you work from home or run a business from a rented property, you may need to add endorsements to your renters' insurance policy to extend coverage for business-related equipment and liabilities. However, it's always recommended to consult with an insurance professional to understand the specific terms and limitations of your policy.

Renter's Insurance: Texas Townhome Necessity?

You may want to see also

Explore related products

![]()

General liability insurance

While general liability insurance is not legally required, it is often requested by clients before signing a contract. Certain industries may also require it if you work with clients or have contract agreements. Additionally, some states may require general liability insurance for professional licenses or specific jobs. For instance, general contractors and other construction professionals often need general commercial liability insurance.

The cost of general liability insurance varies depending on specific business features, such as profession, business size, number of employees, location, and risk exposure. It is typically more expensive for larger businesses with higher risk exposure. Small and medium-sized businesses may benefit from additional protections found in a Business Owner's Policy (BOP), which combines general liability insurance with commercial property insurance and business interruption insurance.

It is important to note that general liability insurance does not cover all claims. It typically excludes commercial auto accidents, employee injuries or illnesses, damage to business property, professional mistakes, purposeful wrongdoing, and illegal acts. To ensure adequate coverage, business owners should carefully review their policies and consider additional types of insurance to address specific risks.

Security Deposits: Rent Expense or Not?

You may want to see also

Explore related products

$9.34 $9.95

$38.41 $64.99

![]()

Commercial flood insurance

Most business insurance policies do not cover losses resulting from floods. Commercial flood insurance can be purchased separately to cover damage to the building, its contents, or both. This insurance can also cover damage from mould and mildew resulting from flooding, although pre-existing mould and mildew conditions are not covered. Commercial flood insurance typically provides up to $500,000 of coverage for the building and its contents. Businesses can also purchase excess insurance coverage to rebuild properties valued above the National Flood Insurance Program (NFIP) limits, which includes protection against business interruption.

The NFIP, established by Congress in 1968, provides flood insurance to property owners, renters, and businesses. It is managed by the Federal Emergency Management Agency (FEMA) and delivered through a network of over 50 insurance companies. The NFIP works with communities to adopt and enforce floodplain management regulations that help reduce flood risks. Flood insurance rates are determined by factors such as the type of construction, age, and location of the property, as well as the area's flood risk level as assessed by FEMA.

Businesses located in high-risk flood areas with mortgages from federally-regulated or insured lenders are typically required to have flood insurance. Even if your business is in a low- to moderate-risk area, it is still wise to consider investing in flood insurance, as it can provide a high level of protection at a lower cost. There is usually a 30-day waiting period for an NFIP policy to go into effect, so it is important to plan ahead and purchase coverage before a flood occurs.

In addition to the NFIP, there are private market options for commercial flood insurance, such as FloodFlash, which offers fast, flexible, and affordable coverage for businesses, public entities, and residential properties at higher risk of flooding. FloodFlash uses a data and smart sensor approach to provide coverage for financial losses arising from flooding, including business interruption.

Late Fees and Rental Taxes: Arizona's Guide

You may want to see also

Frequently asked questions

Business renters insurance is a type of insurance policy that combines general liability insurance, commercial property insurance, and business interruption insurance. It helps protect your property, team, and operations.

Business renters insurance covers losses to business property due to theft, fire, or other covered losses. It also includes liability coverage for medical and legal costs if someone gets hurt on the property.

If you rent property for your business, your landlord may require you to have business renters insurance. It is also important to note that a property insurance policy does not cover every type of damage, so additional coverage may be necessary depending on your business's specific needs.