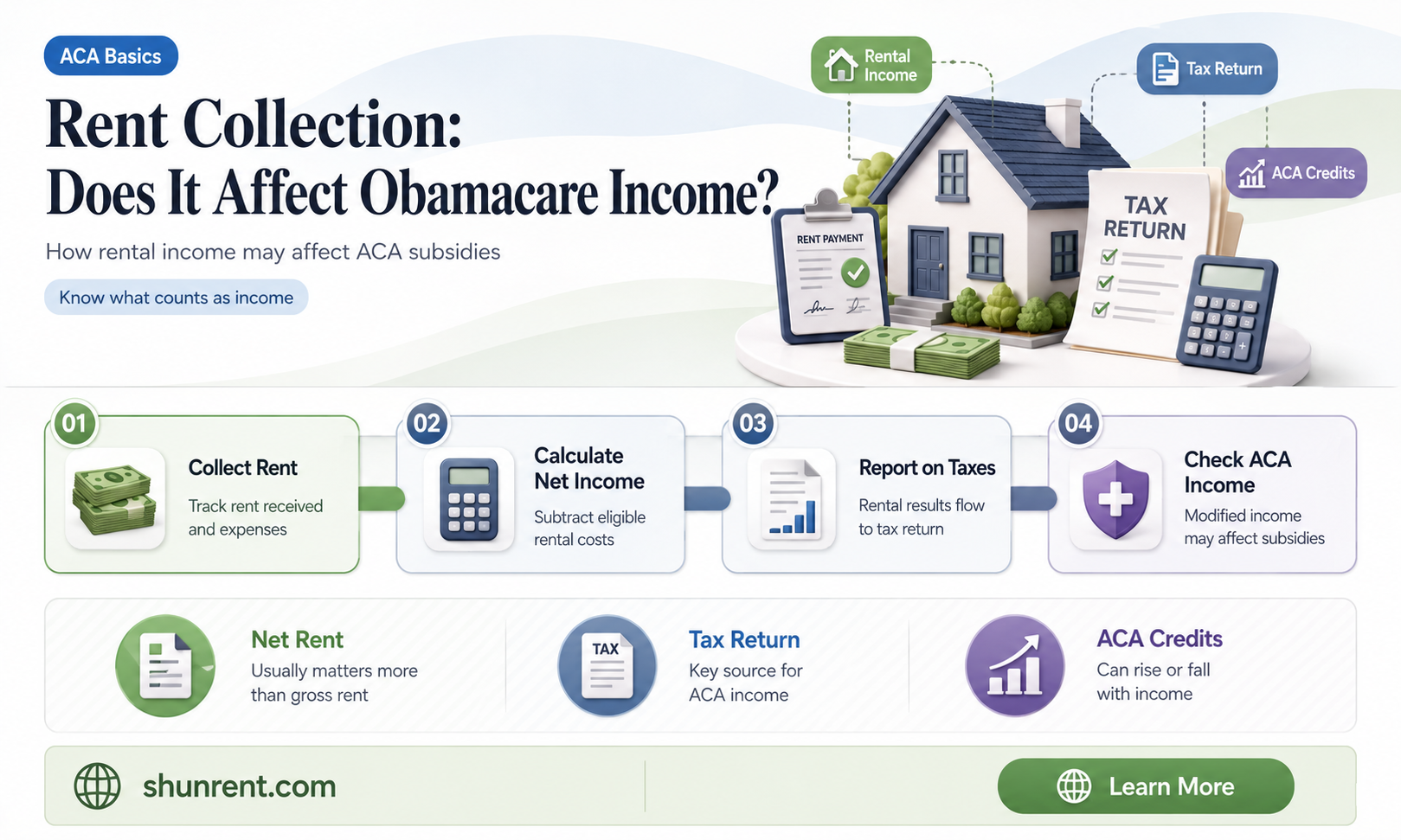

When determining eligibility for Obamacare, the Marketplace counts the estimated income of all household members. This includes net rental and royalty income. However, it's important to note that the MAGI (Modified Adjusted Gross Income) methodology for calculating income differs from previous Medicaid rules, and certain types of income, such as child support, veterans' benefits, and Social Security benefits, may not be included in MAGI. The specific rules and deductions that apply can vary based on individual circumstances and state regulations.

| Characteristics | Values |

|---|---|

| What counts as income for Obamacare? | The Marketplace counts the estimated income of all household members. |

| What is included in the income calculation? | Net rental and royalty income, most IRA and 401k withdrawals, interest and dividends earned on investments, and income from business after expenses. |

| What is MAGI? | MAGI is adjusted gross income (AGI) plus tax-exempt interest, certain non-taxable Social Security benefits, and excluded foreign income. |

| What is included in MAGI? | Tax-exempt interest, non-taxable Social Security benefits, and certain forms of income that are non-taxable or partially taxable. |

| What is not included in MAGI? | Pre-tax deductions such as health insurance premiums, retirement plan contributions, or flexible spending accounts. Child support received, veterans' benefits, workers' compensation, gifts and inheritances, and certain American Indian and Alaska Native income. |

| How is income calculated for dependents? | If a dependent has a tax-filing requirement, their MAGI is included in household income. If their income is below a certain threshold, they are not required to file. |

Explore related products

What You'll Learn

![]()

Rental income is counted as income for Obamacare

When it comes to determining eligibility for Obamacare, officially known as the Affordable Care Act (ACA), rental income is indeed considered part of an individual's or household's income. This income is specifically referred to as "net rental income".

The ACA uses the Modified Adjusted Gross Income (MAGI) methodology to calculate household income. MAGI is calculated by taking the gross income (income from any source that is not exempt from tax) and adding tax-exempt interest and certain tax-exempt Social Security benefits. Net rental income is included in this calculation.

It is important to note that MAGI does not include all forms of income. For example, child support received, veterans' benefits, workers' compensation, gifts and inheritances, and certain assistance payments are not counted in MAGI. Additionally, pre-tax deductions, such as health insurance premiums and retirement plan contributions, are not included in MAGI as they are not taxed.

When applying for health insurance through the ACA Marketplace, individuals or households must report their current income. This includes rental income. However, the Marketplace allows for certain deductions to be subtracted from the total income. It is essential to report any income changes as they occur to avoid missing out on savings or owing money when filing tax returns.

Sunbed Rentals: Nammos' Exclusive Beach Experience

You may want to see also

Explore related products

![]()

MAGI is used to calculate household income

When determining eligibility for health insurance coverage under the Affordable Care Act (also known as Obamacare), Marketplace and Medicaid agencies use Modified Adjusted Gross Income (MAGI) to calculate household income. MAGI is a specific calculation that differs from previous Medicaid rules and includes certain items that may not be included in a household's tax return.

MAGI is calculated by taking the adjusted gross income (AGI) and adding tax-exempt interest, certain Social Security benefits, and excluded foreign income. AGI is derived by subtracting deductions for certain expenses from an individual's gross income, which includes income from any source that is not exempt from tax.

For households with dependents, the MAGI calculation includes any dependent's income that meets the tax-filing threshold. If a dependent has earned or unearned income above a certain threshold, they are required to file taxes, and their income is included in the household's MAGI. However, if a dependent does not meet the filing requirement but chooses to file anyway, their income is not included in the household's MAGI.

MAGI also includes certain forms of non-taxable or partially taxable income, such as tax-exempt interest from specific investments like state and municipal bonds. Additionally, non-taxable Social Security benefits are included in MAGI, especially for individuals who rely solely on these benefits as their source of income.

It is important to note that MAGI does not include all sources of income. For example, pre-tax deductions such as health insurance premiums, retirement plan contributions, or flexible spending accounts are not included in MAGI calculations. Furthermore, under MAGI rules, certain types of income that were previously considered part of household income for Medicaid eligibility, such as child support, veterans' benefits, and workers' compensation, are no longer counted.

Appraisal Rent Schedules: What's Included in a 1025?

You may want to see also

Explore related products

![]()

Tax-exempt interest is included in MAGI

When it comes to healthcare, the Marketplace counts the estimated income of all household members. This includes net rental and royalty income, as well as interest and dividends earned on investments.

Modified Adjusted Gross Income, or MAGI, is an important tax term to understand. MAGI is your Adjusted Gross Income (AGI) plus a few additional items, such as tax-exempt interest and the tax-free portion of Social Security benefits. This is used by the Internal Revenue Service (IRS) to determine eligibility for certain tax deductions, credits, and retirement savings plans.

MAGI can vary depending on the specific tax benefit in question. For example, when determining eligibility for Roth IRA contributions, the income limits for a Roth retirement account are based on your MAGI.

To calculate MAGI for a Traditional IRA deduction, you add your AGI plus any deductions or foreign earned income, foreign housing, tax-exempt interest, and the tax-free portion of Social Security benefits.

It is important to note that MAGI calculations can vary, and some items may be treated differently. For instance, while most calculations include excluded foreign earned income, not all include excludable savings bond interest and excludable adoption benefits.

Essential Documents: Renting a Hotel Room

You may want to see also

![]()

Social Security benefits are counted in MAGI

When it comes to determining eligibility for health insurance coverage, the Marketplace uses a figure known as Modified Adjusted Gross Income (MAGI) to assess whether an individual qualifies for savings or financial assistance. This calculation takes into account various sources of income, including Social Security benefits.

Social Security benefits are generally considered taxable income and are, therefore, included in the calculation of MAGI. This applies to Social Security retirement benefits, survivor benefits, and disability payments (SSDI). If an individual is receiving these benefits, they are required to include the full amount before any deductions in their MAGI calculation. This is true even for non-taxable Social Security income—it still counts toward MAGI.

However, there are certain exceptions to this rule. Supplemental Security Income (SSI) is not considered a Social Security benefit but rather a supplemental income program for those with little to no income. SSI is always excluded from MAGI-based income calculations. Additionally, for children and tax dependents, Social Security income is only factored into the total household income if the individual is required to file a federal income tax return.

It's important to note that the inclusion of Social Security benefits in MAGI can have implications for eligibility for programs like Medicaid and Marketplace financial assistance. In some cases, individuals who are not required to file taxes may be denied Medicaid due to their Social Security income pushing their MAGI above the eligibility threshold. Therefore, accurately reporting and understanding the treatment of Social Security benefits in MAGI calculations is crucial for individuals seeking healthcare coverage.

Umbrellas on Myrtle Beach: Rent or Buy?

You may want to see also

![]()

Dependents' income may be included in household income

When applying for health insurance through the Marketplace, you will need to estimate your household income for the year. This is because Marketplace savings are based on your expected household income for the year you want coverage. The Marketplace counts the estimated income of all household members, including the income of any dependents.

If you are claimed as a tax dependent by someone else, you are counted as part of their household, and your income will be included in their household income. If you are the one claiming someone else as a dependent, their income will be included in your household income. However, it is important to note that a dependent's income is only included if they are required to file taxes. If they are not required to file a federal income tax return for the year you want coverage, their income will not be included in your household income.

The Marketplace uses a measure called modified adjusted gross income (MAGI) to determine eligibility for savings and tax credits. MAGI is adjusted gross income (AGI) plus tax-exempt interest, certain foreign income, and Social Security benefits not included in gross income. When calculating MAGI, any foreign income excluded under Section 911 of the Internal Revenue Code must be added back.

It is important to report any income changes as soon as possible after enrolling in Marketplace health insurance. Failing to do so could result in missing out on savings or owing money back when filing your federal tax return.

Rent Write-Offs: State or Federal?

You may want to see also

Frequently asked questions

Yes, collected rent is considered taxable income under the Affordable Care Act.

MAGI stands for Modified Adjusted Gross Income. It is used to determine a household's income for Medicaid and premium tax credit eligibility. MAGI includes tax-exempt interest, Social Security benefits, and some forms of non-taxable income.

Yes, rental income is generally considered passive income and is taxable as net investment income. However, if you qualify as a Real Estate Professional and actively participate in rental activities, you may be able to exclude rental income from your MAGI.

Passive income is income derived from investments or activities in which you are not actively involved, such as rental income. Active income is earned from activities in which you actively participate, like a job or business.

Yes, certain deductions can be applied to your MAGI calculation. These include pre-tax deductions like health insurance premiums, retirement plan contributions, and flexible spending accounts. Additionally, if you qualify for Medicaid based on age, disability, or other factors, different rules for counting income may apply.