Prepaid rent refers to rent payments made in advance of the rental period. For example, if a tenant pays January's rent in December, this is considered prepaid rent. Prepaid rent is recorded as an asset on a balance sheet, not as income, as it is money received for a service that has not yet been provided. This is important for maintaining accurate financial records and reporting. Prepaid rent is a common issue for landlords and tenants, and it can make monthly income look uneven. It is also a concern for companies that rent commercial spaces.

| Characteristics | Values |

|---|---|

| Definition | Prepaid rent refers to rent payments received before the rental period begins. |

| Accounting Treatment | Prepaid rent is recorded as a current asset, not income, when it's first received. |

| Impact on Income Statement | Prepaid rent can make monthly income look uneven. |

| Cash Flow Statement | Prepaid rent is reflected when cash is received, not when it's earned, increasing cash flow. |

| Income Tax Treatment | The IRS treats prepaid rent as taxable income in the year it's received, especially under cash-basis accounting. |

| ASC 842 Treatment | Under ASC 842, prepaid rent is included as a right-of-use (ROU) asset and a lease liability on the balance sheet. |

| Accrual Accounting Treatment | In accrual accounting, prepaid rent is a future benefit and is recorded as an asset until it is drawn down as an expense. |

| Cash Basis Accounting Treatment | Under cash basis accounting, prepaid rent would be recorded as an expense when paid. |

Explore related products

What You'll Learn

![]()

Prepaid rent is a current asset

Prepaid rent is a common occurrence in the rental market, with tenants often paying rent for the upcoming month at the end of the preceding month. This situation raises a critical accounting question: does prepaid rent count as a current asset on the balance sheet?

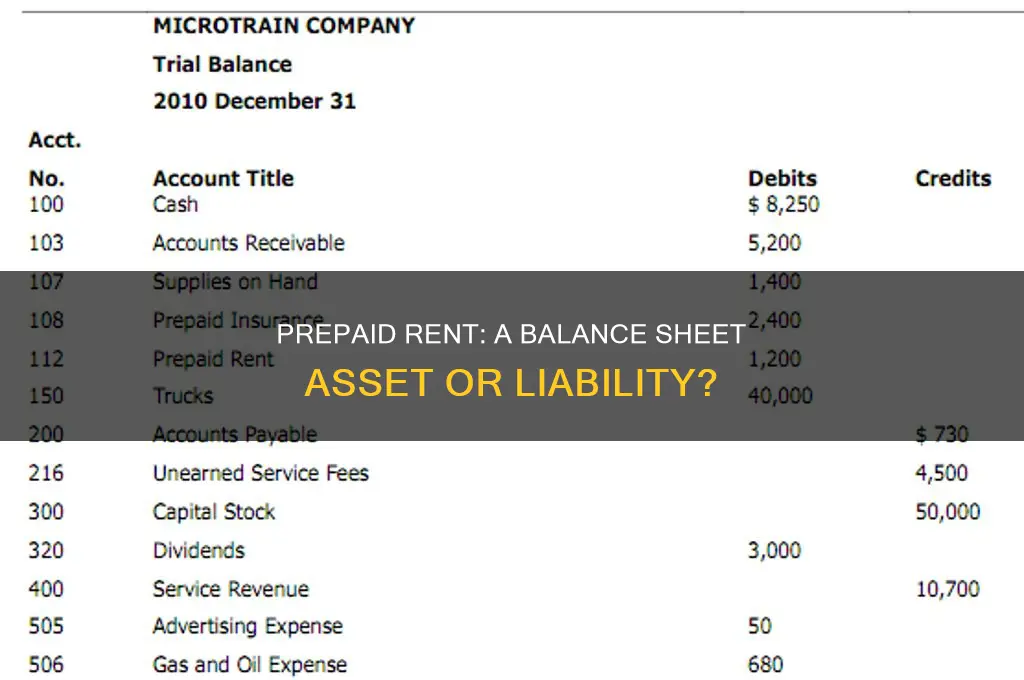

The answer is yes; prepaid rent is considered a current asset in accounting. Prepaid rent refers to rent payments made before the rental period begins. For example, if a tenant pays January's rent in December, that payment is classified as prepaid rent. While the landlord has received the money, they haven't earned it yet, as the tenant has not occupied the property during the period the rent covers. Therefore, when first received, prepaid rent is recorded as a current asset, not income. It is essential to note that the treatment of prepaid rent in accounting has evolved over time. Under the previous accounting standard, ASC 840, prepaid rent was recognised as a current asset on the balance sheet. However, with the introduction of ASC 842, there is a subtle distinction to be made. Prepaid rent is no longer classified as a current asset but is instead included as a right-of-use (ROU) asset for operating and finance leases. This change in classification does not diminish the fact that prepaid rent is still considered an asset.

The distinction between prepaid rent and income is crucial for accurate financial reporting. When a tenant prepays rent, it represents an obligation that the landlord must fulfil in the future. By recording prepaid rent as an asset, landlords can accurately track their financial position and ensure that their income reporting aligns with the reality of their cash flow. This approach helps avoid an "income dip" during months when no new rent is collected, even though cash has been received earlier. Properly accounting for prepaid rent as an asset also assists in maintaining compliance with accounting standards and accurately depicting the financial position of a company or individual.

Furthermore, the treatment of prepaid rent as an asset aligns with the GAAP matching principle, which requires accrual accounting. This principle stipulates that revenue and expenses must be reported in the period when the spending occurs, rather than when cash is exchanged. As a result, prepaid rent is initially recorded as a prepaid asset, and only when the rental period commences, it is removed from the asset section and posted as rental income. This process ensures that income is recognised in the period when it is earned, providing a more accurate representation of financial performance.

In conclusion, prepaid rent is indeed a current asset on the balance sheet. By recording it as an asset, landlords and tenants can maintain accurate financial records, align their income reporting with reality, and comply with accounting standards. Properly managing prepaid rent ensures that financial statements provide a transparent and truthful depiction of an entity's financial position.

Appraisal Rent: Actual vs Market Value

You may want to see also

Explore related products

![]()

It's recorded differently under ASC 842

Prepaid rent is a common occurrence in lease agreements, where a lessee pays rent for a period that has not yet occurred. Under ASC 842, the concept of prepaid rent does not exist in the same way as other accounting standards. This means that prepaid rent is not recognised as a separate account on the balance sheet. Instead, it is incorporated into the right-of-use (ROU) asset and impacts the lease liability.

This shift from the previous ASC 840 standard, where prepaid rent was treated as a separate asset, marked a significant change in lease accounting. It necessitates adjustments to financial reporting practices, requiring careful tracking of lease payments and their effects on financial statements. The transition to the new lease accounting standard results in financial statements that more accurately reflect an organisation's leasing activity, ensuring transparency and compliance.

Under ASC 842, prepaid rent is accounted for as part of the ROU asset, and the lease liability is determined by calculating the present value of future lease payments. The ROU asset amortisation is then calculated, ensuring that the ROU asset is fully amortised over the lease term. This process involves debiting the ROU asset and crediting the prepaid rent account, ensuring these transactions are recorded properly for accurate financial reporting.

The treatment of prepaid rent under ASC 842 is particularly important for organisations managing multiple leases, as it impacts their balance sheets and financial ratios. It is beneficial for these organisations to adopt lease accounting software to handle the complexities of lease accounting and ensure compliance with the new standard.

The Ultimate Guide to Hammock Camping: Rent or Not?

You may want to see also

Explore related products

![]()

It impacts income reporting

Prepaid rent is a common occurrence in the rental market, but it can have an impact on income reporting, especially if you are a landlord or a tenant keeping financial records. Prepaid rent is when rent is paid in advance of the rental period. For example, if a tenant pays January's rent in December, that is considered prepaid rent.

When it comes to accounting, prepaid rent is initially recorded as a prepaid asset on the balance sheet. It is not considered income until the rental period begins. This is because it is money received for a service that has not yet been provided. This is important for accurate financial reporting and maintaining a clear cash flow. It also ensures that reported income is aligned with each rental period.

The treatment of prepaid rent as an asset is also important for tax purposes. In some cases, the IRS treats prepaid rent as taxable income in the year it is received, especially if using cash-basis accounting. This means that if a tenant pays rent for January 2025 in December 2024, it counts as income for 2024, even though it is for the following year.

The treatment of prepaid rent as an asset also has implications for expense reporting. As the rent expense is incurred over time, the prepaid rent asset is gradually reduced and recognised as an expense, which is then reflected on the income statement. This process ensures that expenses are accurately matched with the period in which they are incurred, providing a clear picture of financial performance.

Overall, understanding the treatment of prepaid rent as an asset and its impact on income reporting is crucial for maintaining accurate financial records, tax compliance, and making informed financial decisions.

How Rent Impacts Your Tax Return

You may want to see also

Explore related products

![]()

It can make monthly income look uneven

Prepaid rent can make monthly income look uneven. This is because prepaid rent is recorded as a current asset, not income, when it is first received. It is considered an asset because it represents the future use of the rented space. However, it is not yet considered income as it has not been "earned". The rent is only earned when the tenant officially occupies the property during the rental period.

For example, if a tenant pays rent for October and November in September, the landlord will receive a large sum all at once. However, only a portion of that should count as income in September. The rest needs to be recorded in the following months as it becomes "earned". This approach keeps financial reporting aligned with reality, showing not just the cash on hand but also the portion that still represents an unearned obligation.

This timing difference is important to understand, especially if reports are used to make monthly financial decisions. It can result in an "income dip" during months when no new rent is collected, even though the money came in earlier. This can be further complicated by the fact that the IRS typically treats prepaid rent as taxable income in the year it is received, especially if using cash-basis accounting.

To avoid this issue, it is important to keep track of the contents of the prepaid assets account and review the list prior to the end of each month. This will help ensure that expenses are not under-reported and assets are not over-reported.

Renting: First Floor vs. Third Floor Units

You may want to see also

Explore related products

![]()

It's taxable income in the year it's received

Prepaid rent is typically recorded as a current asset on a balance sheet, not as income. However, when it comes to taxes, the Internal Revenue Service (IRS) treats prepaid rent as taxable income in the year it is received, regardless of the period covered or the accounting method used. This is true even if the rent covers multiple years in the future.

For example, if a tenant pays January's rent in December, it counts as income for the current year, even though it is for the following year. This is because, for tax purposes, rental income includes any payment received for the use or occupation of property. It is considered constructive receipt of income when it is made available to you, such as by being credited to your bank account.

The IRS allows deductions for rental expenses in the year they are paid. These expenses may include repairs, utilities, and other deductible items. However, if the expenses cover a period of more than one year, only the portion applicable to the current year can be deducted.

Prepaid rent can impact your tax bill significantly. By accepting prepaid rent, you may be reporting a higher amount of rental income for the current year, potentially pushing your income into a higher tax bracket or making a larger portion of your rental income taxable. Therefore, it is essential to understand the tax implications of prepaid rent and consult with a tax professional or accountant to ensure accurate reporting and compliance with tax regulations.

Listing Rats: What Rental Applications Need

You may want to see also

Frequently asked questions

Prepaid rent refers to rent payments received by the landlord before the rental period begins. For example, if a tenant pays January rent in December, that payment is considered prepaid rent.

Prepaid rent is recorded as a current asset, not income, when it's first received. It is considered an asset because it represents future use of the rented space.

Prepaid rent can make monthly income look uneven. For example, if a tenant pays rent for October and November in September, you will receive a large sum all at once. However, only a portion of that should count as income in September, with the rest recorded in the following months as it becomes earned.

It is important to keep track of the contents of the prepaid assets account and review the list before closing the books at the end of each month. Once the rental period arrives, the prepaid amount is removed from the asset section and posted as rental income.

Prepaid rent occurs when rent is paid in advance before the lease period begins, while accrued rent refers to rent expenses that have been incurred but not yet paid. Prepaid rent is included as a right-of-use (ROU) asset on the balance sheet, while accrued rent decreases the ROU asset as the expense has been recognized.