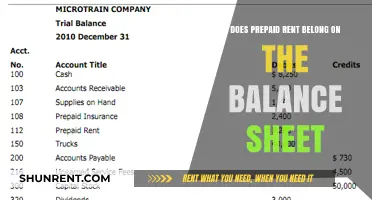

Prepaid rent is a type of account that represents rent paid in advance of the rental period. It is classified as an asset account with a normal debit balance. This is because prepaid rent showcases a future economic benefit to the entity. When a business pays rent in advance, it records this expense in the Prepaid Rent account, increasing its assets. As time passes, the prepaid rent is recognised as an expense, and the business will reduce the Prepaid Rent account by debiting Rent Expense and crediting Prepaid Rent.

| Characteristics | Values |

|---|---|

| Type of account | Asset account |

| Balance type | Debit balance |

| Accounting treatment | Recorded as an asset until the month when the company is actually using the facility to which the rent relates, then charged to expense |

| Example | If a company pays $3,000 for three months of rent in advance, it will record a debit of $3,000 to Prepaid Rent, increasing its assets |

Explore related products

What You'll Learn

![]()

Prepaid rent is an asset account

The normal balance for asset accounts is a debit balance. As time passes, the prepaid rent is recognised as an expense. When the rent period is recognised, the expense is recorded accordingly. Each month, as the rent is used, the company will record an expense by debiting the Rent Expense account and crediting Prepaid Rent, reflecting the consumption of the asset. This way, the company spreads out the cost over time, matching expenses to the months they apply to.

For example, if a company pays $12,000 for a year's lease in advance, it will debit the Prepaid Rent account for that amount, reflecting an asset. Each month, as the rent is "used up", a portion of the prepaid rent is moved from the asset category to the Rent Expense account on the income statement. This is done by debiting the Rent Expense account and crediting Prepaid Rent. By the end of the year, the Rent Expense account will show a total of $12,000 in payments for the year, and the Prepaid Rent account will be depleted to zero.

A concern when recording prepaid rent in this manner is that one might forget to shift the asset into an expense account in the month when rent is consumed. To avoid this, keep track of the contents of the prepaid assets account, and review the list before the end of each month.

RV Rental Guide: Planning Your Road Trip Adventure

You may want to see also

Explore related products

![]()

Prepaid rent is recorded as a debit

Prepaid rent is rent paid prior to the rental period to which it relates. Rent is commonly paid in advance, being due on the first day of the month covered by the rent payment. This presents a problem for the tenant, as the payment would normally appear in its income statement as rent expense in the period in which the invoice was entered in the accounting software. However, since the payment was recorded and the check was cut in the month before the period to which the payment relates, it is actually prepaid rent. Therefore, a tenant should record on its balance sheet the amount of rent paid that has not yet been used.

In accounting, prepaid rent is initially recorded as an asset because it provides future economic benefits to the company. As the benefits of the expenses are realized, the related asset account is decreased, and the expense is recognized. Prepaid rent is amortized over the period to which it relates, confirming that it maintains an asset status until used. This means that as each month passes, the business will reduce the Prepaid Rent account by debiting Rent Expense and crediting Prepaid Rent, ensuring the financial statements accurately represent both the expense incurred and the remaining value of prepaid rent.

When the rent period is recognized, the expense is recorded accordingly. When the time period for the rent expires, the company will then recognize the expense by debiting Rent Expense and crediting Prepaid Rent, thereby reflecting the consumption of the asset. For example, if a company pays $12,000 for a year's lease in advance, it will debit the Prepaid Rent account for that amount, reflecting an increase in assets. As the year progresses, the company will debit Rent Expense and credit Prepaid Rent to recognize the expense.

Asheville Cabin Resort Getaways: Your Private Mountain Escape

You may want to see also

Explore related products

![]()

Prepaid rent is paid in advance

Prepaid rent is classified as an asset account that has a normal debit balance. This account represents payments made in advance for rent, showcasing a future economic benefit. When the rent period is recognised, the expense is recorded accordingly. The account is classified as an asset account on the balance sheet because it represents money that has been paid in advance for rent, providing a future economic benefit to the entity. The normal balance for asset accounts is a debit balance.

For example, if a company pays $3,000 for three months of rent in advance, it will record a debit of $3,000 to Prepaid Rent, increasing its assets. Each month, as the rent is used, the company will record an expense by debiting Rent Expense and crediting Prepaid Rent. This ensures that the financial statements accurately represent both the expense incurred and the remaining value of prepaid rent.

Prepaid expenses are first recorded in the prepaid asset account on the balance sheet. Once expenses are incurred, the prepaid asset account is reduced and an entry is made to the expense account on the income statement. Prepaid expenses are not included in the income statement per generally accepted accounting principles (GAAP). Prepaid expenses are considered assets because they represent money that the company has not yet spent.

Roll-Off Container Rental: Size Matters

You may want to see also

Explore related products

![]()

Prepaid rent is adjusted monthly

Prepaid rent is a payment made in advance for the rental of property or equipment. It is classified as an asset account with a normal debit balance. This is because prepaid rent represents a future economic benefit to the entity. When a business pays rent ahead of time, it records this expense in the Prepaid Rent account. This account is listed as an asset on the balance sheet.

The normal balance for asset accounts is a debit balance. So, if a company pays rent for the upcoming month or year in advance, it records this payment as a debit to the Prepaid Rent account, indicating an increase in assets. As each month passes, the business will reduce the Prepaid Rent account by debiting Rent Expense and crediting Prepaid Rent, as the actual benefit of the lease is consumed. This ensures that the financial statements accurately represent both the expense incurred and the remaining value of prepaid rent.

For example, if a company pays $12,000 for a year’s lease in advance, it will debit the Prepaid Rent account for that amount, reflecting an increase in assets. At the end of the first month, the company has used up one month's worth of rent, so the prepaid rent must be adjusted. The adjusting journal entry for a prepaid expense affects both a company’s income statement and balance sheet.

It is important to keep track of the contents of the prepaid assets account and review the list prior to the end of each month. This is to avoid forgetting to shift the asset into an expense account when the rent is consumed, which would result in under-reporting the expense and over-reporting the asset. Prepaid rent can also impact monthly income, as it may result in a large sum being received all at once. However, only a portion of that should count as income in the month it is received, with the rest being recorded in the following months as it is earned.

Jonathan Larson's Pre-Rent Creation: Tick, Tick... Boom!

You may want to see also

Explore related products

![]()

Prepaid rent is a future economic benefit

When a business pays rent ahead of time, it records this expense in the prepaid rent account. Since this account holds value that the business will benefit from in the future, it is listed as an asset on the balance sheet. For example, if a company pays $12,000 for a year's lease in advance, it will debit the prepaid rent account for that amount, reflecting an increase in assets. As time passes, the prepaid rent is recognised as an expense. When the rent period is recognised, the expense is recorded accordingly.

For tenants, prepaid rent can be advantageous as it demonstrates their commitment and responsibility, building trust with the landlord. It also ensures financial security and efficiency for both landlords and tenants. Additionally, tenants can benefit from negotiating better rates and possible discounts for paying early. From the landlord's perspective, prepaid rent arrangements provide stable financial support, enabling them to enhance property maintenance and plan for future investments.

However, it is important to note that prepaid rent can be a concern for businesses if they forget to shift the asset into an expense account when the rent is consumed. This can lead to under-reporting of expenses and over-reporting of assets in financial statements. Therefore, proper tracking of prepaid expenses is crucial for taxes and financial reporting. According to generally accepted accounting principles (GAAP), prepaid expenses are amortised over the period they relate to, confirming their asset status until they are used.

Airbnb Legalities: Business Licenses in Charleston, SC

You may want to see also

Frequently asked questions

Prepaid rent is rent paid prior to the rental period. It is commonly paid in advance, at the beginning of the month covered by the rent payment.

Prepaid rent is first recorded as an asset account on the balance sheet. It is recorded as a debit, indicating an increase in assets.

Prepaid rent is recognised as an expense when the rent period is recognised. The expense is recorded by debiting rent expense and crediting prepaid rent, reflecting the consumption of the asset.

Accrued expenses are the opposite of prepaid expenses. Accrued expenses are costs of goods or services that a company consumes before paying for them, while prepaid expenses are payments made in advance.

Prepaid rent is classified as an asset account, and the normal balance for asset accounts is a debit balance. This is because prepaid rent represents payments made in advance, providing a future economic benefit.