Reporting prorated rents as a seller involves accurately accounting for the portion of rent that corresponds to the time you owned the property before the sale. When selling a rental property, the buyer typically reimburses you for the rent earned but not yet collected for the period after the closing date. To report this, you must calculate the prorated rent by dividing the monthly rent by the number of days in the month and then multiplying by the number of days you owned the property. This amount is generally reported as rental income on your tax return, usually on Schedule E of Form 1040 in the U.S. It’s essential to document the calculation and ensure both parties agree on the proration terms in the purchase agreement to avoid discrepancies. Consulting a tax professional or real estate attorney can help ensure compliance with local tax laws and regulations.

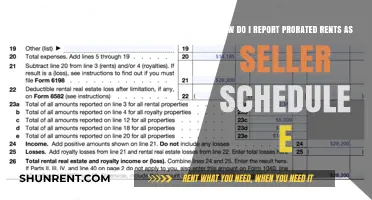

| Characteristics | Values |

|---|---|

| Reporting Method | Prorated rents are typically reported on Schedule D (Capital Gains and Losses) of Form 1040. |

| Calculation | Prorated rent is calculated by dividing the total rent for the period by the number of days in the period, then multiplying by the number of days the seller owned the property. |

| Tax Treatment | Prorated rents are generally considered ordinary income and taxed at the seller's marginal tax rate. |

| Form 1099-S | If the total real estate transaction exceeds $600, the buyer or closing agent must file Form 1099-S with the IRS, which may include prorated rent information. |

| Adjustments | Prorated rents are often adjusted at closing, with the seller receiving a credit for prepaid rent and the buyer receiving a credit for rent paid in advance. |

| Record-Keeping | Sellers should maintain accurate records of prorated rent calculations, lease agreements, and closing statements to support their tax reporting. |

| State-Specific Rules | Some states may have specific rules or requirements for reporting prorated rents, so it's essential to consult state tax laws or a tax professional. |

| Tax Year | Prorated rents are typically reported in the tax year in which the property is sold, regardless of when the rent was actually received. |

| Impact on Basis | Prorated rents do not affect the seller's basis in the property, as they are considered income rather than a recovery of capital. |

| Professional Advice | Given the complexity of tax laws, it's recommended to consult a tax professional or real estate attorney for guidance on reporting prorated rents as a seller. |

Explore related products

What You'll Learn

![]()

Understanding Prorated Rent Calculation

When selling a property, understanding how to handle prorated rents is crucial for both the seller and the buyer. Prorated rent refers to the portion of the rent that corresponds to the number of days the seller occupies the property after the rent is typically due but before the sale is finalized. This ensures that the buyer receives a fair share of the rent for the period they will own the property. To calculate prorated rent, you first need to determine the daily rent amount by dividing the monthly rent by the number of days in the month. For example, if the monthly rent is $1,200, the daily rent would be $1,200 divided by 30, which equals $40 per day.

Once the daily rent is established, the next step is to identify the exact number of days the seller will occupy the property after the rent due date but before the closing date. For instance, if the rent is due on the 1st of the month, the closing date is on the 15th, and the seller occupies the property until the closing, the seller would be responsible for 14 days of rent (from the 2nd to the 15th). Multiply the daily rent by the number of days the seller occupies the property to calculate the prorated rent amount. Using the previous example, the prorated rent would be $40 per day multiplied by 14 days, totaling $560.

Reporting prorated rents as a seller involves clearly documenting this calculation in the closing statement or settlement statement. This ensures transparency and accuracy in the financial transaction. The prorated rent amount is typically credited to the buyer at closing, meaning the seller will either pay this amount directly to the buyer or it will be deducted from the seller’s proceeds. It’s essential to coordinate with the title company, escrow officer, or closing agent to ensure the prorated rent is accurately reflected in the closing documents.

Another important aspect of prorated rent calculation is handling prepaid rents. If the tenant has paid rent in advance for a period extending beyond the closing date, the seller must credit the buyer for the portion of the rent that covers the days after closing. For example, if the tenant has paid $1,200 for the entire month and the closing occurs on the 15th, the buyer is entitled to 16 days of rent (from the 15th to the end of the month). The seller would then credit the buyer for 16 days of rent, calculated at $40 per day, totaling $640.

Lastly, it’s crucial to review the lease agreement to ensure compliance with any specific terms related to rent proration. Some leases may have unique provisions or requirements that need to be addressed during the sale. Additionally, local laws or regulations may dictate how prorated rents should be handled, so consulting with a real estate attorney or professional can provide further guidance. By accurately calculating and reporting prorated rents, sellers can avoid disputes and ensure a smooth transition of ownership.

Where Do Cub Scouts Meet? Exploring Rental Options

You may want to see also

Explore related products

![]()

Documentation Requirements for Reporting

When reporting prorated rents as a seller, maintaining accurate and comprehensive documentation is essential to ensure compliance with tax regulations and to avoid potential disputes. The first critical document is the lease agreement, which outlines the terms of the rental, including the monthly rent amount, lease duration, and any specific clauses related to prorated rent. This document serves as the foundation for calculating the prorated amount and should be readily available for reference. Additionally, the closing statement or settlement statement (often the HUD-1 or ALTA form) must clearly itemize the prorated rent, showing the amount credited to the buyer or debited from the seller. This ensures transparency and provides a formal record of the transaction.

Another key requirement is the rent ledger or payment records, which detail the rent payments made by the tenant up to the closing date. This documentation verifies that the prorated rent calculation is based on actual payments received and not on estimated or assumed figures. If there are any discrepancies or adjustments, such as prepaid rent or outstanding balances, these should be clearly noted in the ledger. Including a proration worksheet or calculation breakdown is also highly recommended. This worksheet should show the daily rent rate, the number of days the seller is responsible for, and the final prorated amount. It provides a step-by-step explanation of the calculation, making it easier to audit and verify.

For sellers, it is crucial to retain communication records with the buyer, tenant, and any involved parties regarding the prorated rent. This includes emails, letters, or messages discussing the proration terms, agreements, or disputes. Such records can serve as evidence of mutual understanding and agreement on the prorated amount. If the tenant vacates the property before closing, documentation of the vacancy date and any related notices (e.g., move-out notices or lease termination agreements) should also be included to justify the proration period.

Lastly, sellers should ensure that all documentation is organized and dated for easy retrieval and reference. This includes keeping both physical and digital copies of all relevant documents, as tax authorities or auditors may request them. Proper documentation not only facilitates accurate reporting but also protects the seller from potential liabilities or disputes arising from prorated rent calculations. By adhering to these documentation requirements, sellers can confidently report prorated rents in compliance with legal and financial standards.

Sixt Atlanta: Renting Cars to 18-Year-Olds?

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Tax Implications of Prorated Rents

When selling a rental property, prorated rents are a common aspect of the transaction, but they also carry specific tax implications that sellers must understand. Prorated rent refers to the allocation of rent payments between the buyer and seller based on the portion of the rental period each party owns the property. For tax purposes, the Internal Revenue Service (IRS) treats prorated rents as income to the seller, as it represents the seller’s share of the rent for the period they owned the property. This means the prorated rent amount must be reported as rental income on the seller’s tax return for the year of the sale. Failure to report this income accurately can result in penalties or audits, so meticulous record-keeping is essential.

The seller must report the prorated rent on Schedule E of Form 1040, which is used for reporting income from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests. The prorated rent is included in the total rental income received during the year, even if the payment is made directly to the seller at closing. Additionally, the seller must also report any associated expenses, such as property taxes or maintenance costs, that were prorated and allocated to their period of ownership. Properly matching income and expenses to the correct tax year ensures compliance with IRS rules and avoids potential issues during tax filings.

Another critical tax consideration is the treatment of security deposits. If the seller retains a portion of the tenant’s security deposit as part of the sale, this amount may also need to be reported as income. However, if the security deposit is transferred to the buyer, it is generally not considered taxable income to the seller. It’s important to clearly document the handling of security deposits in the sales agreement to ensure accurate tax reporting. Misclassification of security deposits can lead to overpayment of taxes or unintended tax liabilities.

Capital gains tax is another area affected by prorated rents. While prorated rents themselves are treated as ordinary income, the sale of the property may trigger capital gains tax if the property has appreciated in value. Sellers should be aware that the prorated rent does not impact the calculation of capital gains, which is based on the difference between the property’s adjusted basis and the sale price. However, accurate reporting of rental income, including prorated rents, is crucial for maintaining a clear financial record that supports the capital gains calculation.

Finally, sellers should consult with a tax professional or accountant to ensure proper handling of prorated rents and related tax implications. State-specific tax laws may also apply, adding another layer of complexity. By staying informed and organized, sellers can navigate the tax implications of prorated rents effectively, minimizing the risk of errors and maximizing compliance with tax regulations. Proper documentation of all transactions, including the closing statement, is key to a smooth tax reporting process.

Finding Your Ground Rent Lease: A Step-by-Step Guide to Locating It

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Disclosing Prorated Rents to Buyers

When selling a property with tenants in place, it’s essential to disclose prorated rents to buyers accurately and transparently. Prorated rent refers to the portion of the rent that corresponds to the time the seller owned the property before closing. As a seller, you must clearly communicate this information to the buyer to ensure a smooth transaction and avoid disputes. Start by calculating the prorated rent based on the number of days the tenant occupied the property before the sale closes. For example, if the tenant paid $1,200 for the month and the seller owned the property for 20 days, the prorated amount would be $800 (20/30 * $1,200). This amount should be credited to the buyer at closing, as they will be responsible for the property for the remaining days of the month.

To disclose prorated rents effectively, include this information in the settlement statement or closing disclosure documents. Work with your title company or closing attorney to ensure the prorated rent is clearly itemized and reflects the agreed-upon calculations. Provide the buyer with a copy of the lease agreement or rental records to verify the rent amount and payment schedule. Transparency in this process builds trust and ensures both parties understand their financial obligations. Additionally, if there are any prepaid rents or security deposits, these should also be disclosed and transferred to the buyer, as they will assume responsibility for managing the tenancy.

It’s crucial to follow local real estate laws and regulations when disclosing prorated rents. Some states or jurisdictions may have specific requirements for handling tenant-occupied properties during a sale. Consult with a real estate attorney or agent to ensure compliance with these rules. For instance, certain areas may require written notice to tenants about the sale or specific documentation regarding the transfer of security deposits. Being proactive in understanding and adhering to these requirements protects both the seller and the buyer from potential legal issues.

Communication with the buyer is key throughout this process. Clearly explain how the prorated rent was calculated and provide supporting documentation, such as rent receipts or bank statements. If there are multiple tenants or complex rental agreements, create a detailed breakdown for each unit or tenant. Address any questions or concerns the buyer may have promptly and professionally. This level of clarity helps prevent misunderstandings and ensures a fair transaction for all parties involved.

Finally, consider including a clause in the purchase agreement that explicitly addresses prorated rents. This clause should outline the method of calculation, the responsibilities of both parties, and how any discrepancies will be resolved. By formalizing this aspect of the sale in writing, you minimize the risk of disputes after closing. Properly disclosing prorated rents not only fulfills your legal and ethical obligations as a seller but also contributes to a positive and transparent real estate transaction.

Men's Wearhouse: Suit Rentals for Kids?

You may want to see also

Explore related products

$13.9 $25

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![]()

Handling Disputes Over Prorated Amounts

When handling disputes over prorated rent amounts as a seller, it's essential to first understand the basis of the disagreement. Prorated rent is calculated by dividing the total monthly rent by the number of days in the month and then multiplying by the number of days the buyer occupies the property. Disputes often arise due to miscalculations, differing interpretations of the lease agreement, or discrepancies in the move-in or move-out dates. To address this, start by reviewing the purchase agreement and any relevant documents that outline how prorated rent should be calculated. Ensure both parties are using the same methodology and dates to avoid confusion.

Clear communication is key in resolving disputes over prorated amounts. If the buyer or their agent disputes the calculated amount, request a detailed explanation of their position and the figures they believe are correct. Provide your own calculations and supporting documentation, such as the lease agreement, closing statement, and any correspondence regarding move-in dates. If the dispute stems from a disagreement over the move-in date, refer to the closing disclosure or any written agreements that specify when the buyer takes possession of the property. Maintaining a professional and transparent dialogue can often lead to a mutual resolution without escalation.

If the dispute persists, consider involving a neutral third party, such as a real estate attorney or mediator, to help resolve the issue. A legal professional can review the contracts and calculations to provide an unbiased opinion. In some cases, the title company or escrow agent may also assist in mediating the dispute, as they often handle prorated rent calculations during the closing process. Be prepared to provide all relevant documentation to support your position, and remain open to compromise if a reasonable solution is proposed.

To prevent future disputes, ensure that the prorated rent calculation is clearly outlined in the purchase agreement and that all parties understand the terms before closing. Double-check the accuracy of the dates and figures used in the calculation, and consider including a clause that specifies how disputes over prorated amounts will be handled. For example, you might agree to resolve disagreements through mediation or arbitration rather than litigation. Taking proactive steps to clarify expectations can minimize the risk of conflicts arising after the sale.

Finally, if the dispute cannot be resolved amicably and involves a significant amount of money, consult with a real estate attorney to explore your legal options. While litigation should be a last resort due to its cost and time-consuming nature, it may be necessary to protect your financial interests. Keep detailed records of all communications, calculations, and agreements related to the prorated rent to strengthen your case if legal action becomes unavoidable. Handling disputes professionally and methodically not only helps resolve the current issue but also preserves your reputation as a seller in future transactions.

Why You Need an Agent to Rent

You may want to see also

Frequently asked questions

Prorated rents should be reported as rental income on your tax return, typically on Schedule E (Form 1040) in the U.S. Allocate the rent based on the number of days you owned the property during the rental period.

Keep records of the closing statement, lease agreement, and any calculations showing how the rent was prorated. These documents will help verify the accuracy of your reporting in case of an audit.

Yes, even if the tenant hasn’t paid the prorated rent, it should still be reported as income. The buyer typically credits you for the prorated rent at closing, and this amount is considered taxable income.

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)