Enterprise Rent-to-Own is a flexible financing option that allows individuals to acquire furniture, appliances, electronics, or other household items without the need for traditional credit. Under this arrangement, customers lease the item for a set period, typically with weekly or monthly payments, while having the option to purchase it outright at any time during or at the end of the lease term. The total cost of ownership is often higher than buying outright due to added fees and interest, but it provides immediate access to essential items with no long-term commitment. If the customer chooses not to purchase, they can return the item without penalty, though they forfeit any payments made. This model is particularly appealing to those with limited credit history or financial flexibility, offering a pathway to ownership while maintaining affordability and convenience.

Explore related products

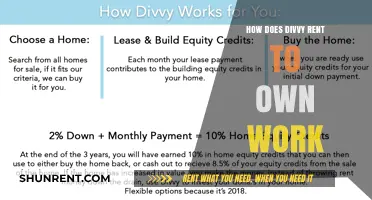

What You'll Learn

- Eligibility Requirements: Credit checks, income verification, and employment status needed for approval

- Payment Structure: Weekly/bi-weekly payments, including rent and ownership option fees

- Ownership Timeline: Total payments and duration to fully own the item

- Early Purchase Option: Discounted buyout options available before the contract ends

- Return Policy: No penalties for returning items, but payments are non-refundable

![]()

Eligibility Requirements: Credit checks, income verification, and employment status needed for approval

Before you can drive off in a rent-to-own vehicle from Enterprise, you'll need to meet specific eligibility requirements. These aren't just formalities; they're a way for the company to assess your ability to commit to the program. Let's break down what's involved.

Credit Checks: A Snapshot of Your Financial History

Enterprise will run a credit check to evaluate your financial responsibility. This doesn't necessarily mean a perfect credit score is required, but a history of consistent payments and responsible credit management will work in your favor. If your credit score is below 600, you might face higher down payment requirements or need a co-signer. Remember, rent-to-own programs often cater to individuals with less-than-ideal credit, so don't be discouraged if your score isn't stellar.

Income Verification: Proving Your Ability to Pay

Expect to provide proof of income, typically through recent pay stubs or bank statements. Enterprise needs to ensure you have a stable and sufficient income to cover the weekly or bi-weekly payments. As a general rule, your monthly vehicle payment shouldn't exceed 20% of your take-home pay. For example, if you take home $2,500 per month, aim for a payment of $500 or less.

Employment Status: Stability is Key

A steady job is crucial for rent-to-own approval. Enterprise will verify your employment status and may require a minimum employment duration, often six months to a year. If you're self-employed, be prepared to provide tax returns or profit and loss statements to demonstrate consistent income. Seasonal workers might need to show additional documentation to prove income stability during off-seasons.

Practical Tips for a Smooth Approval Process

Gather all necessary documents beforehand, including your driver's license, proof of insurance, and recent pay stubs. Be honest about your financial situation; transparency can strengthen your case. If you have a co-signer, ensure they meet the eligibility requirements as well. Finally, consider saving for a down payment, as this can improve your chances of approval and reduce your overall payment amount. By understanding and meeting these eligibility requirements, you'll be well on your way to driving off in a rent-to-own vehicle from Enterprise.

Rent the Runway's Size Inclusivity: Large Sizes Available?

You may want to see also

Explore related products

![]()

Payment Structure: Weekly/bi-weekly payments, including rent and ownership option fees

Enterprise rent-to-own programs often break down payments into manageable weekly or bi-weekly installments, blending rent with ownership option fees. This structure appeals to those seeking flexibility and gradual ownership without the immediate financial burden of a lump-sum purchase. For instance, a $1,200 appliance might require a $50 weekly payment over 24 weeks, with a portion allocated to rent and another toward the ownership option. This approach allows users to test the product’s fit in their lifestyle before committing fully.

Analyzing the payment structure reveals its dual purpose: it serves as a trial period while simultaneously building equity. Each payment reduces the remaining balance required to own the item outright. For example, if $20 of the $50 weekly payment goes toward the ownership option, the customer accumulates $480 toward ownership after 24 weeks. This transparency helps users track progress and plan financially, though it’s crucial to review contracts for hidden fees or penalties for early termination.

Persuasively, this payment model aligns with modern consumer preferences for subscription-based services and budget-friendly commitments. It’s particularly advantageous for individuals with fluctuating incomes or those rebuilding credit, as consistent payments can improve financial standing. However, critics argue that the total cost may exceed retail prices, making it essential to compare long-term expenses before signing. For optimal use, consider setting up automatic payments to avoid missed deadlines and leverage promotions or discounts offered by providers.

Comparatively, traditional financing often requires credit checks and down payments, whereas rent-to-own programs are more accessible but come with higher overall costs. For instance, a $500 laptop might cost $800 through rent-to-own versus $600 with a credit card. To maximize value, evaluate the item’s utility over time and assess whether the convenience of small payments outweighs the premium. Practical tip: negotiate terms or seek providers offering early buyout discounts to reduce total expenses.

Descriptively, the bi-weekly option further eases financial strain by aligning payments with pay periods, ideal for those with semi-monthly income. For example, a $100 bi-weekly payment for a $2,000 piece of furniture spreads the cost over 20 weeks, making it feel less daunting. This cadence also fosters discipline, as payments are less frequent but require larger individual commitments. Always ensure the contract clearly outlines payment distribution and ownership milestones to avoid confusion.

Maine Hotel Rental Age: What You Need to Know

You may want to see also

Explore related products

![]()

Ownership Timeline: Total payments and duration to fully own the item

Understanding the ownership timeline in a rent-to-own agreement is crucial for anyone considering this financing option. Unlike traditional purchases, where ownership transfers immediately upon full payment, rent-to-own programs spread payments over an extended period, often with weekly or bi-weekly installments. The total duration to fully own the item varies widely, typically ranging from 12 to 24 months, depending on the retailer and the item’s value. For example, a $1,000 appliance might require 52 weekly payments of $25, totaling $1,300, while a $3,000 piece of furniture could extend to 91 payments, totaling $4,550. These timelines highlight the importance of calculating the total cost upfront to avoid surprises.

Analyzing the financial commitment reveals that rent-to-own agreements often result in higher total payments compared to outright purchases. This is due to added fees, interest, and service charges embedded in the payment structure. For instance, a $500 laptop might cost $800 by the end of a 12-month agreement, reflecting a 60% markup. While this may seem steep, the flexibility of smaller, frequent payments appeals to those with limited cash flow or poor credit. However, it’s essential to compare these costs with alternative financing options, such as credit cards or personal loans, to ensure the best financial decision.

To navigate the ownership timeline effectively, start by reviewing the contract’s terms carefully. Pay attention to the total number of payments, the amount per installment, and any additional fees. Some agreements offer early purchase options, allowing you to buy the item at a discounted price before the term ends. For example, paying 50% of the total cost within 90 days might waive remaining payments. Additionally, inquire about return policies, as canceling the agreement typically means forfeiting all payments made. Practical tip: Use a payment tracker to monitor progress and ensure you’re on course to meet your ownership goal.

Comparing rent-to-own timelines with traditional financing options underscores the trade-off between convenience and cost. While a 24-month rent-to-own plan for a $2,000 sofa might total $3,200, a personal loan at 10% interest could cost $2,200 over the same period. However, rent-to-own requires no credit check, making it accessible to those with poor or no credit history. For individuals prioritizing immediate access to items without large upfront costs, this timeline can be a viable solution. Yet, it’s critical to weigh the long-term financial impact against short-term needs.

In conclusion, the ownership timeline in rent-to-own agreements demands careful consideration of total payments and duration. By understanding the structure, comparing costs, and leveraging early purchase options, consumers can make informed decisions. While this financing method offers flexibility, it’s not without its drawbacks, particularly the higher overall cost. For those who proceed, staying organized and committed to the payment schedule ensures a smoother path to full ownership. Always remember: the key to success lies in clarity, comparison, and discipline.

Renting the Perfect Party Hall: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Early Purchase Option: Discounted buyout options available before the contract ends

One of the most appealing aspects of Enterprise Rent-to-Own programs is the Early Purchase Option, a feature that allows customers to buy the vehicle they’re renting at a discounted price before the contract ends. This option is not just a financial tool; it’s a strategic opportunity for those who find themselves ahead of schedule or simply in love with their current ride. Unlike traditional leasing, where early termination often comes with penalties, this option rewards commitment and foresight. For instance, if you’ve been renting a vehicle for 12 months out of a 24-month contract and decide you want to own it, the buyout price is typically reduced based on the payments already made and the remaining contract term.

To maximize the benefits of the Early Purchase Option, it’s crucial to understand the calculation behind the discount. Most programs apply a portion of your rental payments toward the purchase price, but the exact formula varies. Some providers deduct a fixed percentage of each payment, while others apply a sliding scale based on how early you decide to buy. For example, buying out after 50% of the contract might reduce the remaining balance by 30%, whereas waiting until 75% could reduce it by 50%. Always review the contract terms to know exactly how much you’ll save by acting early.

A comparative analysis of this option reveals its advantages over traditional financing or leasing. In a standard lease, early termination often incurs fees, and in a loan, prepayment penalties might apply. With the Early Purchase Option, not only do you avoid these costs, but you also gain equity in an asset you’ve already been using. This makes it particularly attractive for individuals with fluctuating financial situations or those who prefer flexibility. For instance, if you’re a contractor whose income varies seasonally, this option lets you align your purchase decision with your cash flow.

Practical tips for leveraging this feature include monitoring your contract milestones and planning ahead. If you anticipate wanting to buy the vehicle early, set aside a portion of your savings each month to cover the discounted buyout amount. Additionally, keep an eye on the vehicle’s condition, as excessive wear and tear might affect the final price. Finally, communicate with your provider regularly to ensure you’re aware of any promotions or additional discounts they might offer for early buyouts.

In conclusion, the Early Purchase Option is a powerful tool within Enterprise Rent-to-Own programs, offering both financial savings and ownership flexibility. By understanding its mechanics, comparing it to other financing methods, and implementing practical strategies, you can turn a rental agreement into a smart investment. Whether you’re a long-term planner or someone who values adaptability, this option ensures you’re always in the driver’s seat.

Rent a Range Rover in Michigan: Top Locations & Tips

You may want to see also

Explore related products

![Adams Residential Lease, Forms and Instructions [Print and Downloadable] (LF310)](https://m.media-amazon.com/images/I/81uP3OCk9qL._AC_UL320_.jpg)

![]()

Return Policy: No penalties for returning items, but payments are non-refundable

One of the most critical aspects of any rent-to-own agreement is understanding the return policy, particularly when it comes to financial implications. Enterprise Rent-to-Own programs typically offer a unique approach: no penalties for returning items, but payments made up to that point are non-refundable. This policy is designed to provide flexibility while maintaining a clear financial boundary. For instance, if you’ve rented a refrigerator for six months and decide it’s not the right fit, you can return it without facing additional fees. However, the $1,200 you’ve paid over those months will not be returned, as it covers the usage and depreciation of the item during that period.

Analyzing this policy reveals a balance between consumer protection and business sustainability. On one hand, the absence of return penalties reduces the risk for customers who may need to exit the agreement prematurely due to financial hardship or changing circumstances. On the other hand, non-refundable payments ensure that the rent-to-own company recoups some value for the item’s use and wear. This structure contrasts with traditional retail return policies, where refunds are often issued for unused or lightly used items. In rent-to-own scenarios, the item’s value diminishes with use, making full refunds impractical.

For consumers, navigating this policy requires careful consideration. If you’re unsure about committing to a long-term rental, treat the initial payments as a trial period. For example, if you’re renting a laptop for $50 per week, consider the first month’s payments ($200) as a testing phase. If the item doesn’t meet your needs, returning it within this timeframe minimizes financial loss. However, if you’ve made payments for six months or more, returning the item means forfeiting a significant amount, so assess your long-term commitment before proceeding.

A practical tip for maximizing this policy is to align your rental period with your financial goals. If you’re renting furniture for a temporary living situation, opt for shorter-term agreements or be prepared to return items early. Conversely, if you’re renting appliances with the intent to own, focus on completing the agreement rather than viewing it as a flexible rental. Always review the contract terms to understand the exact point at which returning an item becomes financially disadvantageous.

In conclusion, the "no penalties, non-refundable payments" return policy in rent-to-own agreements offers both freedom and financial responsibility. It allows customers to exit agreements without additional fees but requires them to accept the sunk cost of payments made. By understanding this policy and planning accordingly, consumers can make informed decisions that align with their needs and financial capabilities. Treat each payment as an investment in the item’s use, not as a refundable deposit, and you’ll navigate rent-to-own agreements more effectively.

How Much Rent Does Section 8 Cover?

You may want to see also

Frequently asked questions

Enterprise Rent-to-Own is a program that allows customers to rent vehicles with the option to purchase them later. It combines the flexibility of renting with the potential to own the vehicle after meeting certain terms and conditions.

Customers select a vehicle, pay a weekly or monthly rental fee, and use the vehicle as if it were their own. A portion of the rental payments may go toward the purchase price if the customer decides to buy the vehicle at the end of the rental period.

Enterprise typically requires a credit check for rent-to-own programs, but they may offer more flexible options compared to traditional financing. Approval depends on credit history, income, and other factors.

Yes, customers can usually return the vehicle without penalty, though specific terms may vary by location. However, any payments made will not be refunded, and the option to purchase the vehicle will be forfeited.

If you choose to buy the vehicle, the remaining balance (after deducting eligible rental payments, if applicable) must be paid. The exact terms, including the purchase price and payment options, will be outlined in your agreement.