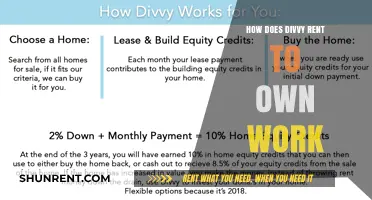

Kmart's rent-to-own program, often referred to as lease-to-own, allows customers to acquire products without paying the full price upfront. This flexible payment option is ideal for those who need essential items like appliances, electronics, or furniture but prefer to spread the cost over time. Customers select their desired items, sign a lease agreement, and make regular payments, typically weekly or bi-weekly, until the item is fully paid off. The program often includes the option to return the item at any time without further obligation, providing a low-risk way to access products. While it can be a convenient solution for immediate needs, it’s important to understand the total cost, as rent-to-own agreements may include higher overall payments compared to traditional purchases.

| Characteristics | Values |

|---|---|

| Program Name | Kmart Rent-to-Own (operated by WhyNot Lease It) |

| Eligibility | - Must be 18+ years old - Valid photo ID - Social Security Number - Active debit card/checking account - Minimum monthly income requirement (varies) |

| Application Process | - In-store application - Quick approval decision (often within minutes) - No credit check required |

| Payment Terms | - Weekly, bi-weekly, or monthly payments - Early purchase option available - 90-day purchase option (pay full cash price + tax within 90 days to avoid additional fees) |

| Ownership | - Ownership transfers after all payments are completed - Early buyout options available |

| Product Categories | - Furniture - Appliances - Electronics - Jewelry - Tools - Other select items |

| Fees | - Lease-to-own fees (included in total cost) - Late payment fees (if applicable) - No hidden fees (all costs disclosed upfront) |

| Return Policy | - Early termination option (return item with no further obligation) - No penalties for early returns |

| Delivery/Pickup | - In-store pickup or delivery options available - Delivery fees may apply |

| Partner | Operated by WhyNot Lease It, not directly by Kmart |

| Availability | Select Kmart stores (check local store for participation) |

| Website | WhyNot Lease It for more details |

Explore related products

What You'll Learn

- Eligibility Requirements: Credit checks, income verification, and identification needed for Kmart rent-to-own approval

- Payment Terms: Weekly/bi-weekly payments, total cost, and ownership duration explained clearly

- Product Selection: Available items, brands, and categories for rent-to-own at Kmart

- Early Purchase Option: Save money by buying out the contract early with discounts

- Return Policy: Terms for returning items, fees, and impact on payments

![]()

Eligibility Requirements: Credit checks, income verification, and identification needed for Kmart rent-to-own approval

Kmart's rent-to-own program, like many similar offerings, has specific eligibility criteria to ensure both parties—the retailer and the customer—are protected. One of the first hurdles applicants face is the credit check. Unlike traditional financing, rent-to-own programs often cater to individuals with less-than-perfect credit. However, Kmart still conducts a credit check to assess the applicant’s financial history. This doesn’t necessarily mean a high credit score is required, but it does mean the company evaluates the risk of non-payment. For those with poor credit, this step can feel daunting, but it’s less stringent than a bank loan, making it a viable option for those rebuilding their credit.

Next in line is income verification, a critical component of the approval process. Kmart needs to confirm that the applicant has a steady and sufficient income to cover the rental payments. Typically, this involves providing recent pay stubs, bank statements, or other proof of income. The rule of thumb here is that the monthly rental payment should not exceed a certain percentage of the applicant’s income—often around 15-20%. For example, if the monthly payment is $100, the applicant should ideally earn at least $500-$600 per month. This ensures the payment is manageable and reduces the risk of default.

Identification is another non-negotiable requirement. Applicants must provide valid government-issued ID, such as a driver’s license or passport, to verify their identity. This step is straightforward but essential for fraud prevention and legal compliance. Without proper identification, the application process cannot proceed. It’s a simple yet critical step that ties into the broader framework of financial responsibility and accountability.

While these requirements might seem rigorous, they serve a practical purpose. Credit checks, income verification, and identification collectively minimize risk for Kmart while providing an accessible financing option for customers. For applicants, understanding these requirements upfront can streamline the process and increase the likelihood of approval. Practical tips include gathering all necessary documents before applying, ensuring income stability, and being honest about credit history. By meeting these eligibility criteria, customers can take advantage of Kmart’s rent-to-own program to acquire goods they need without the burden of traditional financing barriers.

Renting: A Strategic Short-Term Step or Long-Term Lifestyle Choice?

You may want to see also

Explore related products

![]()

Payment Terms: Weekly/bi-weekly payments, total cost, and ownership duration explained clearly

Kmart's rent-to-own program, often facilitated through partnerships with third-party providers like Acima or Progressive Leasing, structures payments to fit tight budgets. Customers typically choose between weekly or bi-weekly payments, with weekly being the most common due to its smaller, more manageable increments. For instance, a $500 appliance might break down to $25 weekly payments, easing the financial burden compared to lump-sum purchases. This flexibility is particularly appealing for those with irregular income streams or limited savings.

The total cost of rent-to-own agreements at Kmart often exceeds the retail price due to added fees and interest. While the program advertises "no credit needed," the convenience comes at a premium. For example, a $300 item could total $600 or more over the payment term, depending on the duration and provider. Customers should carefully review the agreement to understand the markup, as it varies based on the item and payment schedule. Early payoff options can mitigate some of this cost, but they require discipline and foresight.

Ownership duration is another critical factor in Kmart’s rent-to-own model. Most agreements span 12 to 18 months, though shorter terms are available for those who pay early. Ownership transfers only after the final payment, meaning the item remains the property of the leasing company until then. Missed payments can reset the clock, delaying ownership and increasing the total cost. Customers should treat the agreement like a loan, prioritizing timely payments to avoid complications.

Practical tips can help maximize the value of a rent-to-own agreement. First, compare total costs across providers to find the best deal. Second, budget for early payoff if possible—many programs reduce fees for early completion. Third, read the fine print regarding late fees, ownership timelines, and return policies. Finally, consider the item’s longevity—rent-to-own works best for durable goods like appliances or furniture, not quickly depreciating items.

In summary, Kmart’s rent-to-own program offers accessibility but demands careful planning. Weekly or bi-weekly payments provide flexibility, but the total cost can be steep. Ownership hinges on consistent payments, and early payoff options offer a pathway to savings. By understanding these terms and strategizing accordingly, customers can navigate the program effectively, turning a rental into a valuable asset.

How Rent-A-Center Rentals Work: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Product Selection: Available items, brands, and categories for rent-to-own at Kmart

Kmart's rent-to-own program offers a diverse array of products, ensuring customers can find items that fit their lifestyle and budget. From essential home appliances to the latest electronics, the selection is designed to cater to a wide range of needs. For instance, families looking to upgrade their living space can choose from top brands like Samsung, LG, and Whirlpool, ensuring both quality and reliability. This variety not only makes the program accessible but also appealing to a broad audience.

When considering product categories, Kmart’s rent-to-own options span furniture, electronics, appliances, and even fitness equipment. For those in need of a new refrigerator or washing machine, the appliance section features energy-efficient models that can help reduce utility bills over time. Similarly, the electronics category includes smart TVs, gaming consoles, and laptops, perfect for entertainment or remote work setups. Each category is carefully curated to balance affordability with functionality, making it easier for customers to make informed choices.

Brands play a crucial role in the rent-to-own experience, and Kmart partners with trusted names to ensure customer satisfaction. In the furniture category, brands like Ashley Furniture offer stylish and durable pieces, from sofas to bedroom sets. For tech enthusiasts, brands like Sony and HP provide cutting-edge electronics that align with current trends. This focus on reputable brands not only enhances the value proposition but also builds trust with customers who prioritize quality.

Selecting the right item involves understanding both personal needs and the terms of the rent-to-own agreement. For example, a family might opt for a larger refrigerator if they frequently host gatherings, while a student might prioritize a lightweight laptop for portability. Practical tips include assessing the item’s long-term utility, comparing it with similar products, and ensuring it fits within your budget. By taking these factors into account, customers can maximize the benefits of the program.

In conclusion, Kmart’s rent-to-own product selection is a strategic blend of variety, quality, and affordability. Whether you’re furnishing a new home, upgrading your tech, or investing in appliances, the program offers something for everyone. By focusing on trusted brands and essential categories, Kmart ensures that customers can access high-value items without the upfront financial burden. This approach not only meets immediate needs but also provides a pathway to ownership, making it a practical choice for budget-conscious shoppers.

AutoZone Double Flare Tool Rental: Availability and Usage Guide

You may want to see also

Explore related products

![]()

Early Purchase Option: Save money by buying out the contract early with discounts

Kmart's rent-to-own program offers flexibility for those who prefer not to pay the full price of an item upfront. Among its features, the Early Purchase Option stands out as a strategic way to save money. This option allows you to buy out your contract before the term ends, often with significant discounts applied to the remaining balance. By taking advantage of this feature, you can reduce the total cost compared to completing the full rental term.

To illustrate, consider a $500 appliance with a 12-month rental agreement. If the total cost after 12 months is $700, the Early Purchase Option might allow you to pay just $550 if you buy it out after 6 months. This not only saves you $150 but also eliminates the remaining monthly payments. The discount varies depending on the timing of the buyout, with larger savings typically available earlier in the contract.

Analyzing the benefits, this option is particularly advantageous for those who anticipate having extra funds sooner than expected or for items that quickly become essential. For instance, a family renting a washer and dryer might find it more cost-effective to buy out the contract early if they receive a tax refund or bonus. However, it’s crucial to review the specific terms of your agreement, as some contracts may have minimum rental periods before the buyout option becomes available.

From a practical standpoint, here’s how to maximize this feature: first, track your payments and monitor when the Early Purchase Option becomes available. Second, compare the discounted buyout price to the remaining rental balance to ensure you’re saving money. Finally, plan your finances to take advantage of the option as early as possible, as delays reduce potential savings. By doing so, you can turn a rent-to-own agreement into a more affordable purchase.

In comparison to traditional financing or credit purchases, the Early Purchase Option offers a unique blend of flexibility and savings. Unlike fixed-term loans, it allows you to adapt to your financial situation, paying less if you’re able to settle early. This makes it an appealing choice for budget-conscious consumers who value both affordability and ownership. By understanding and leveraging this feature, you can transform a rent-to-own agreement from a temporary solution into a smart financial decision.

Renting a Horse in Monterey, CA: Your Ultimate Guide

You may want to see also

Explore related products

![]()

Return Policy: Terms for returning items, fees, and impact on payments

Understanding Kmart's rent-to-own return policy is crucial for anyone considering this payment option. Unlike traditional purchases, rent-to-own agreements come with specific terms for returning items, which can significantly impact your financial obligations. Here’s a breakdown of what you need to know.

Terms for Returning Items: Kmart’s rent-to-own program typically allows customers to return items without penalty within a specified grace period, often the first few weeks or months of the agreement. After this period, returns may still be possible, but they are subject to stricter conditions. For instance, you may need to pay a fee or forfeit a portion of the payments already made. It’s essential to review your contract carefully, as terms can vary based on the item and location. Always keep your agreement documents handy for reference.

Fees Associated with Returns: Returning an item after the grace period often incurs fees, which can include a restocking charge or a percentage of the remaining balance. These fees are designed to cover administrative costs and potential depreciation of the item. For example, if you’ve made six months of payments on a $500 appliance and decide to return it, you might be charged a fee equivalent to 10% of the remaining balance. Understanding these fees upfront can help you make informed decisions about whether to continue the agreement or return the item.

Impact on Payments: Returning an item does not necessarily cancel your financial obligation. Depending on the terms, you may still owe a portion of the remaining balance or fees. Additionally, returning an item early can affect your credit score if the agreement is reported to credit bureaus. On the flip side, if you’ve made significant payments and decide to keep the item, those payments contribute toward the total cost. Always calculate the total cost of returning versus keeping the item to determine the best course of action.

Practical Tips for Smooth Returns: To avoid unnecessary fees or complications, follow these steps: 1) Return the item in its original condition with all accessories and packaging. 2) Contact Kmart’s customer service to initiate the return process and confirm any fees. 3) Keep a record of all communications and receipts related to the return. 4) If possible, return the item during the grace period to minimize financial impact. By staying organized and informed, you can navigate the return process with confidence.

In summary, Kmart’s rent-to-own return policy is structured to balance flexibility with financial responsibility. By understanding the terms, fees, and potential impacts on payments, you can make decisions that align with your needs and budget. Always read the fine print and plan ahead to avoid unexpected costs.

Renting Farm Land to Whole Foods: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Kmart Rent-to-Own allows customers to take home products immediately and pay for them over time through regular rental payments. If all payments are made, the customer owns the item.

Kmart Rent-to-Own typically offers a range of products, including electronics, furniture, appliances, and home goods, depending on availability and store location.

Generally, Kmart Rent-to-Own does not require a credit check, making it accessible to customers with varying credit histories.

Missing a payment may result in late fees or other penalties. If payments are consistently missed, the item may be repossessed, and any payments made up to that point are non-refundable.