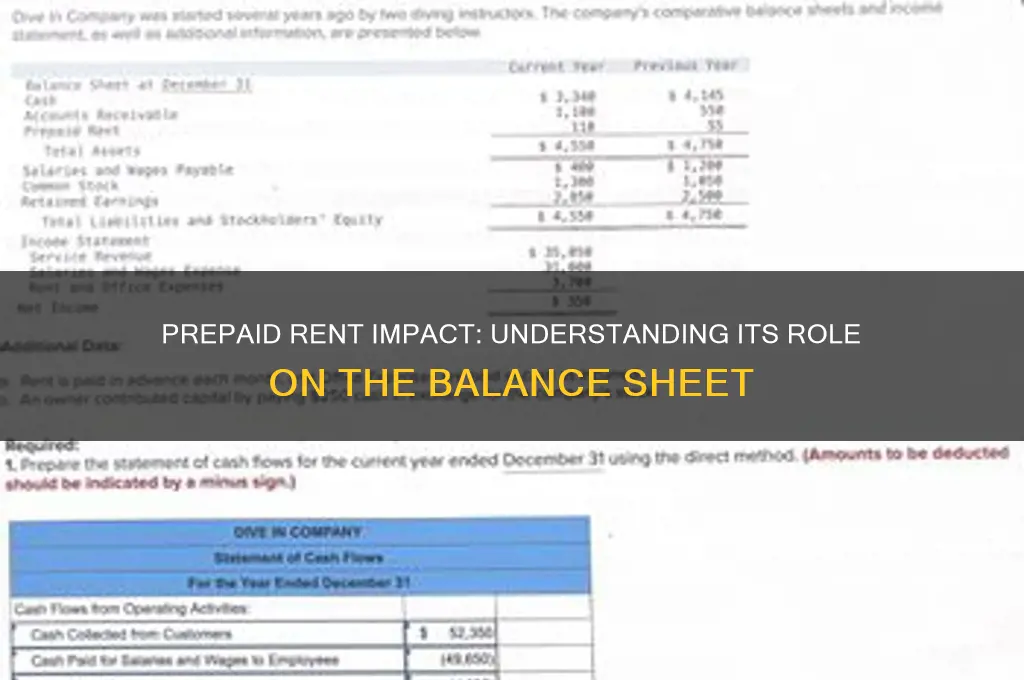

Prepaid rent significantly impacts a company's balance sheet by affecting both the asset and liability sections, albeit temporarily. When a business pays rent in advance, it records the payment as a prepaid expense, which is an asset, reflecting the value of rent paid but not yet consumed. This asset is gradually reduced over the rental period through periodic adjustments to the rent expense account, ensuring that expenses are matched with the appropriate accounting period. Simultaneously, the cash account decreases by the amount paid, reflecting the outflow of funds. As the prepaid rent is utilized, the asset account is reduced, and the corresponding expense is recognized, maintaining the balance sheet's accuracy and adherence to the matching principle in accounting.

| Characteristics | Values |

|---|---|

| Asset Recognition | Prepaid rent is recorded as a current asset on the balance sheet, representing the portion of rent paid in advance for future periods. |

| Initial Entry | Debit: Prepaid Rent (Asset), Credit: Cash (Asset) or Bank (Asset), reflecting the outflow of cash for future rent. |

| Amortization | Over time, the prepaid rent is amortized to recognize rent expense. Debit: Rent Expense (Expense), Credit: Prepaid Rent (Asset). |

| Balance Sheet Impact | Increases current assets initially, then gradually reduces as rent is recognized as an expense. |

| Classification | Classified as a current asset if it is expected to be consumed within one year or the operating cycle, whichever is longer. |

| Financial Statement Effect | Improves liquidity ratios initially but has no long-term impact on financial health. |

| Disclosure | Typically disclosed in the notes to the financial statements if material. |

| Reversal | Fully reversed once the prepaid period is over, with the asset balance reducing to zero. |

| Tax Treatment | Generally not deductible until the period to which the rent expense applies. |

| Example | If $12,000 is paid for 12 months of rent, $1,000 is recognized as rent expense monthly, reducing prepaid rent by $1,000 each month. |

Explore related products

What You'll Learn

![]()

Prepaid Rent as Asset

Prepaid rent is a crucial concept in accounting that directly impacts a company's balance sheet, specifically under the category of current assets. When a business makes a rental payment in advance for a period that extends beyond the current accounting period, this payment is recorded as prepaid rent. This accounting treatment is essential because it adheres to the matching principle, which ensures that expenses are recognized in the same period as the revenues they help generate. By recording prepaid rent as an asset, companies can accurately reflect their financial position and avoid distorting their income statement with expenses that pertain to future periods.

As an asset, prepaid rent represents a future economic benefit that the company has already paid for but has not yet consumed. It is classified as a current asset because it is typically expected to be used within one year or the operating cycle of the business, whichever is longer. This classification is important for stakeholders, such as investors and creditors, as it provides insight into the company's liquidity and short-term financial health. For example, if a company prepays $12,000 for a year’s rent in January, $10,000 of that amount would be recorded as prepaid rent on the balance sheet at the end of January, with the remaining $2,000 recognized as rent expense for the month.

The journal entry to record prepaid rent involves debiting the prepaid rent account (an asset account) and crediting the cash account. This entry increases the total assets on the balance sheet by the amount of the prepaid rent. As each period progresses, the company will then recognize a portion of the prepaid rent as rent expense, reducing the prepaid rent asset and transferring the amount to the income statement. This process ensures that the balance sheet remains accurate and that expenses are matched with the appropriate accounting periods.

Another key aspect of prepaid rent as an asset is its amortization over time. Amortization refers to the process of allocating the prepaid amount to the periods in which the benefit is consumed. For instance, if a company prepays rent for six months, it would amortize the prepaid rent by recognizing one-sixth of the total amount as rent expense each month. This systematic reduction of the prepaid rent asset ensures that the balance sheet reflects the remaining unexpired portion of the prepaid rent, providing a clear picture of the company's financial obligations and resources.

In summary, prepaid rent is recorded as an asset on the balance sheet because it represents a payment made in advance for future benefits. Its classification as a current asset highlights its short-term nature and its role in assessing a company's liquidity. By properly recording and amortizing prepaid rent, businesses can maintain accurate financial statements that comply with accounting principles and provide transparency to stakeholders. Understanding how prepaid rent affects the balance sheet is essential for effective financial management and reporting.

Renter's Insurance: Does It Cover My Rented Items?

You may want to see also

Explore related products

![]()

Current vs. Long-term Classification

Prepaid rent is a unique item on the balance sheet as it represents an advance payment for a future expense. Its classification as either a current or long-term asset depends on the duration of the rental period and the company’s accounting policies. Understanding this classification is crucial for accurately reflecting a company’s financial position. The primary distinction lies in whether the prepaid rent will be fully utilized within the next 12 months or extend beyond that period.

Current Asset Classification: Prepaid rent is typically classified as a current asset if the rental period covered by the payment falls entirely within the next 12 months. For example, if a company pays $12,000 in January for a year’s rent, the entire amount is recorded as a current asset because it will be fully expensed within the current fiscal year. This classification aligns with the definition of current assets, which are resources expected to be consumed or converted into cash within one year. On the balance sheet, prepaid rent is often listed under the "Prepaid Expenses" or "Other Current Assets" section, ensuring it is clearly identifiable as a short-term asset.

Long-term Asset Classification: Conversely, if the prepaid rent covers a period extending beyond 12 months, the portion of the payment applicable to the period beyond one year is classified as a long-term asset. For instance, if a company prepays $24,000 for two years of rent, $12,000 (the amount for the second year) would be classified as a long-term asset, while the remaining $12,000 (for the first year) would be a current asset. This bifurcation ensures that the balance sheet accurately reflects the timing of the expense. Long-term prepaid rent is typically reported under "Other Long-term Assets" or a similar category, distinguishing it from assets that will be utilized in the short term.

Impact on Financial Analysis: The classification of prepaid rent as current or long-term affects key financial ratios and analyses. For example, a higher current asset balance can improve the current ratio, a measure of short-term liquidity. Misclassification could lead to misleading interpretations of a company’s financial health. Therefore, accountants must carefully assess the rental period and allocate prepaid rent appropriately to maintain transparency and compliance with accounting standards.

Accounting Treatment: To record prepaid rent, the initial journal entry debits "Prepaid Rent" (an asset account) and credits "Cash." As rent is consumed, the entry shifts from the asset account to "Rent Expense," reducing the prepaid balance. For long-term portions, only the current year’s expense is recognized annually, while the remaining balance continues to be reported as a long-term asset. This method ensures that expenses are matched with the periods in which they are incurred, adhering to the matching principle of accounting.

In summary, the classification of prepaid rent as current or long-term hinges on the timing of its utilization. Proper classification is essential for an accurate balance sheet and meaningful financial analysis. Companies must carefully evaluate the rental period and apply consistent accounting practices to ensure compliance and transparency in financial reporting.

Cutting Cable Box Rental Costs: What Are My Options?

You may want to see also

Explore related products

![]()

Impact on Total Assets

Prepaid rent significantly impacts the total assets section of a balance sheet by representing a future economic benefit that the company has already paid for. When a business makes a prepaid rent payment, it is essentially exchanging cash for the right to use a property over a specified period. This transaction does not reduce total assets immediately; instead, it transforms the asset from cash to a prepaid expense, which is classified as a current asset on the balance sheet. This reclassification ensures that the total asset value remains unchanged, as the reduction in cash is offset by the increase in prepaid rent.

The impact on total assets becomes more apparent when analyzing the timing of the payment. Prepaid rent reflects an advance payment for a service that will be consumed in the future. As such, it is recorded as an asset until the rental period begins, at which point it is gradually expensed over time. For example, if a company prepays $12,000 for a year’s rent, the entire $12,000 is initially recorded as a prepaid rent asset. Each month, $1,000 is expensed as rent expense, and the prepaid rent asset is reduced by the same amount. This process ensures that the total assets remain balanced, as the decrease in prepaid rent is matched by an increase in expenses and a corresponding decrease in retained earnings.

Importantly, prepaid rent does not alter the total asset figure but redistributes it within the current asset category. This redistribution is crucial for accurately reflecting the company’s financial position. By maintaining the total asset value, prepaid rent ensures that the balance sheet adheres to the fundamental accounting equation: Assets = Liabilities + Equity. This consistency is essential for stakeholders, such as investors and creditors, who rely on the balance sheet to assess the company’s liquidity and solvency.

Another aspect of prepaid rent’s impact on total assets is its role in financial statement analysis. Analysts often scrutinize the composition of current assets to gauge a company’s short-term liquidity. A significant prepaid rent balance may indicate that the company has committed a portion of its cash to future obligations, which could affect its ability to meet immediate financial needs. However, since prepaid rent is a current asset, it is still considered a liquid resource, albeit one that is earmarked for a specific purpose. This distinction highlights the importance of understanding the nature of prepaid rent when evaluating total assets.

In summary, prepaid rent affects the balance sheet by reclassifying cash into a prepaid expense, which is recorded as a current asset. This reclassification ensures that the total assets remain unchanged, as the reduction in cash is offset by the increase in prepaid rent. As the prepaid rent is expensed over time, the asset is gradually reduced, maintaining the balance sheet’s equilibrium. This process underscores the principle that prepaid rent does not diminish total assets but rather shifts their composition, providing a clear and accurate representation of the company’s financial position.

Rent Pricing: Strategies for Landlords

You may want to see also

Explore related products

![]()

Effect on Working Capital

Prepaid rent, a common accounting concept, represents rent paid in advance for a future period. When a company makes a prepaid rent payment, it initially records the transaction as a current asset on the balance sheet. This is because the payment provides a future economic benefit that will be realized within the next 12 months. The asset account is typically labeled "Prepaid Rent" or "Prepaid Expenses." This initial recording increases the company's total assets, which, in turn, affects its working capital.

Working capital is calculated as current assets minus current liabilities. Since prepaid rent is classified as a current asset, it directly contributes to the increase in the company's working capital at the time of payment. This might seem like an improvement in liquidity, but it's essential to understand that this increase is temporary. As the rented period progresses, the prepaid rent is gradually recognized as an expense, reducing the asset account and, consequently, the working capital.

The effect on working capital is twofold: an initial boost when the payment is made, followed by a gradual decrease as the rent is expensed over time.

As the prepaid rent is amortized, it moves from the asset section to the expense section of the income statement. This process is typically done on a straight-line basis, meaning an equal amount is expensed each month. For example, if a company pays $12,000 for a year's rent in advance, it would recognize $1,000 as rent expense each month. This monthly expense reduces the prepaid rent asset account and, in turn, decreases the company's working capital. This reduction is a normal part of the accounting cycle and reflects the consumption of the prepaid asset.

The impact on working capital becomes more apparent when analyzing the cash conversion cycle. Prepaid rent can temporarily distort this cycle, as it increases current assets without a corresponding increase in current liabilities. However, as the rent is expensed, the working capital position adjusts to reflect the true liquidity of the business. It's crucial for financial analysts and investors to consider the nature of prepaid rent when evaluating a company's short-term financial health, as it can provide a misleading picture of liquidity if not properly understood.

In summary, prepaid rent affects working capital by initially increasing it when the payment is made and then gradually decreasing it as the rent is recognized as an expense. This dynamic process highlights the importance of understanding the timing and classification of prepaid expenses in financial analysis. By recognizing how prepaid rent moves through the balance sheet and income statement, stakeholders can more accurately assess a company's working capital and overall financial position. This knowledge is particularly valuable for businesses with significant prepaid expenses, as it enables better cash flow management and financial planning.

Rogers Modem Rental: Is It Necessary?

You may want to see also

Explore related products

![]()

Adjustment in Financial Statements

Prepaid rent is a common accounting concept that requires adjustment in financial statements to accurately reflect a company's financial position. When a business pays rent in advance for a period that extends beyond the current accounting period, it creates a prepaid asset. This asset represents the portion of the rent payment that pertains to future periods and has not yet been consumed. In the context of Adjustment in Financial Statements, prepaid rent must be properly recorded to ensure compliance with the matching principle, which dictates that expenses should be recognized in the same period as the revenues they help generate.

To adjust for prepaid rent in the financial statements, the initial step is to record the entire rent payment as a prepaid asset on the balance sheet. For example, if a company pays $12,000 for a year’s rent in advance, the journal entry would debit Prepaid Rent (an asset account) and credit Cash for $12,000. At this stage, the balance sheet reflects the full prepaid amount as a current asset. However, as time progresses, a portion of this prepaid rent becomes an expense for the current period. This necessitates an adjusting entry to reclassify the consumed portion from the asset account to an expense account.

The adjusting entry for prepaid rent involves debiting Rent Expense (an income statement account) and crediting Prepaid Rent (a balance sheet account) for the amount of rent applicable to the current period. For instance, if one month has passed in the above example, $1,000 ($12,000 / 12 months) would be expensed. This adjustment reduces the Prepaid Rent asset on the balance sheet by $1,000 while increasing Rent Expense on the income statement by the same amount. This ensures that the financial statements accurately reflect the economic reality of the rent consumption over time.

On the balance sheet, the adjustment for prepaid rent directly impacts the asset section. Initially, the prepaid rent is reported as a current asset, but as adjustments are made, the balance decreases as the rent is expensed. By the end of the prepaid period, the Prepaid Rent account should be zero, assuming all the rent has been consumed. This adjustment is crucial for maintaining the integrity of the balance sheet, as it prevents overstatement of assets and ensures that expenses are appropriately matched with revenues.

In summary, Adjustment in Financial Statements for prepaid rent involves a systematic process of initially recording the prepaid amount as an asset and then periodically adjusting it to recognize the expense over time. This process ensures that the income statement reflects the correct rent expense for the period, while the balance sheet accurately represents the remaining prepaid rent as an asset. Proper handling of prepaid rent adjustments is essential for financial reporting accuracy and adherence to accounting principles.

Finding Rental Rates: A Guide to Your New Home

You may want to see also

Frequently asked questions

Prepaid rent is recorded as a current asset on the balance sheet under the "Prepaid Expenses" or "Other Current Assets" section. It represents the portion of rent paid in advance that has not yet been used or expired.

Yes, prepaid rent increases the total assets on the balance sheet by the amount paid in advance. It is offset by a decrease in cash or bank balances, but the total assets remain unchanged as one asset account increases while another decreases.

Prepaid rent is adjusted monthly through amortization. As the rental period progresses, the prepaid rent asset is reduced, and an equal amount is recognized as rent expense on the income statement. This adjustment ensures the balance sheet reflects the remaining prepaid amount.

No, prepaid rent does not directly impact liabilities or equity. It is purely an asset account and does not affect the liabilities or shareholders’ equity sections of the balance sheet. However, the amortization of prepaid rent indirectly affects net income, which can impact retained earnings in the equity section over time.