The Net Present Value (NPV) of rent is a critical financial metric used to evaluate the profitability of a rental property by discounting all future rental income streams to their present value. This calculation accounts for the time value of money, recognizing that cash received in the future is worth less than the same amount today due to factors like inflation and opportunity costs. To compute the NPV of rent, one must estimate the expected rental income over the property’s holding period, determine an appropriate discount rate (often based on the investor’s required rate of return or market interest rates), and then sum the present values of each future cash flow. Additionally, expenses such as maintenance, property taxes, and vacancies are subtracted from the rental income to derive the net cash flows. The resulting NPV provides a clear indication of whether the investment in the rental property is financially viable, with a positive NPV suggesting a profitable venture and a negative NPV indicating a potential loss.

| Characteristics | Values |

|---|---|

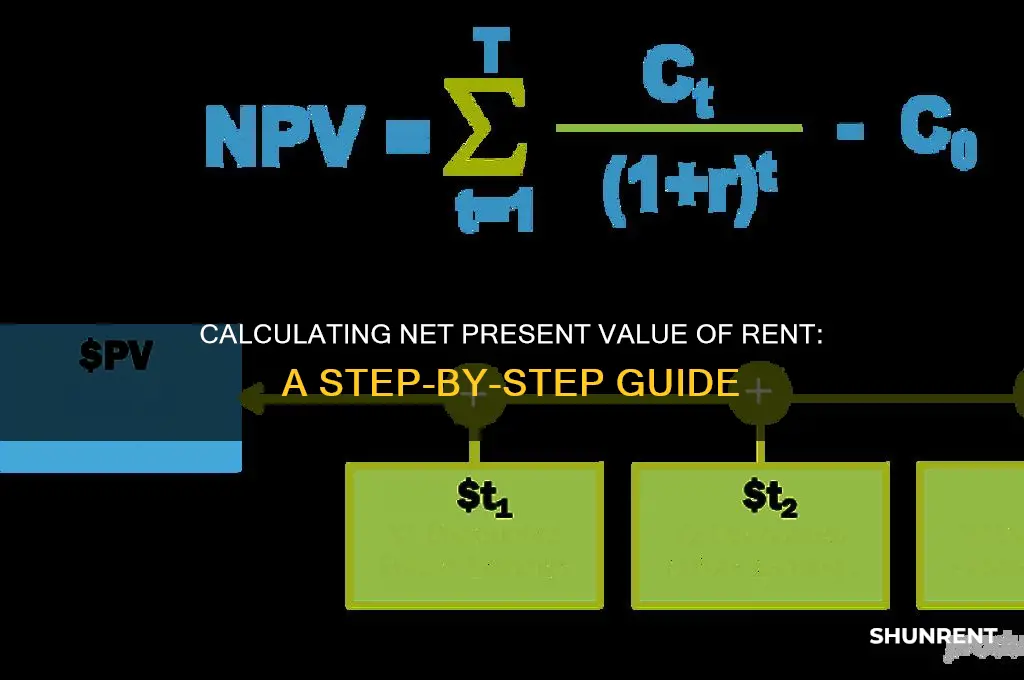

| Definition | Net Present Value (NPV) of rent calculates the current value of future rental payments, discounted to the present using a specific discount rate. |

| Formula | NPV = ∑ (Cash Flow / (1 + Discount Rate)^t) where t is the period number. |

| Discount Rate | Typically based on the weighted average cost of capital (WACC) or a risk-free rate plus a risk premium. As of 2023, the risk-free rate (e.g., 10-year Treasury yield) is around 3.5-4.5%, and WACC ranges from 6-12% depending on industry and risk. |

| Cash Flow | Includes all rental income and associated expenses (e.g., maintenance, property taxes, insurance). |

| Time Period | Usually calculated over the lease term or a specified investment horizon (e.g., 5-10 years). |

| Inflation Adjustment | Rental cash flows may be adjusted for inflation, typically 2-3% annually based on recent U.S. inflation rates (2023). |

| Terminal Value | For long-term leases, a terminal value may be added to account for the property's value at the end of the period, discounted back to the present. |

| Tax Considerations | After-tax cash flows are used, with tax rates varying by jurisdiction (e.g., U.S. corporate tax rate is 21% as of 2023). |

| Sensitivity Analysis | NPV is often tested with varying discount rates and cash flow assumptions to assess risk. |

| Application | Commonly used in real estate investment decisions, lease vs. buy analyses, and property valuation. |

| Limitations | Assumes constant cash flows and discount rates, which may not reflect real-world volatility. |

Explore related products

What You'll Learn

- Discount Rate Selection: Choosing appropriate rate for present value calculation

- Cash Flow Projection: Estimating future rental income and expenses

- Time Period Consideration: Defining the analysis period for rent calculation

- Inflation Adjustment: Accounting for inflation in future cash flows

- Terminal Value Calculation: Estimating property value at the end of the period

![]()

Discount Rate Selection: Choosing appropriate rate for present value calculation

When calculating the net present value (NPV) of rent, selecting an appropriate discount rate is crucial, as it directly impacts the accuracy and reliability of the valuation. The discount rate represents the required rate of return or the cost of capital, reflecting the time value of money and the risk associated with the cash flows. For rental property investments, the discount rate should align with the investor’s expectations and the market conditions. A common starting point is to use the weighted average cost of capital (WACC) of the investor or the market rate for similar investments. However, this rate must be adjusted to account for the specific risks of the rental property, such as vacancy rates, maintenance costs, and market volatility.

One method to determine the discount rate is to benchmark it against comparable investments. For instance, if similar rental properties in the area yield a certain return, that rate can serve as a reference point. Additionally, the risk-free rate, typically represented by government bond yields, can be used as a baseline and adjusted upward to account for additional risks. For example, if the risk-free rate is 3%, and the investor expects an additional 5% return to compensate for property-specific risks, the discount rate would be 8%. This approach ensures that the discount rate reflects both the time value of money and the inherent risks of the investment.

Another factor to consider is the investor’s opportunity cost. The discount rate should be at least equal to the return the investor could earn from alternative investments of similar risk. For instance, if an investor could achieve a 7% return in a real estate investment trust (REIT), the discount rate for the rental property NPV calculation should not be lower than 7%. This ensures that the investment is competitive relative to other options available in the market. Failing to account for opportunity cost can lead to overvaluation of the rental property.

Inflation and future market expectations also play a role in discount rate selection. If inflation is expected to rise, the discount rate should be adjusted upward to maintain the real value of future cash flows. Similarly, if the rental market is projected to grow or decline, the discount rate should incorporate these expectations. For example, in a growing market, a higher discount rate may be justified to account for increased competition and potential rent increases, while in a declining market, a lower rate might be appropriate due to reduced demand.

Finally, sensitivity analysis can be a valuable tool in discount rate selection. By calculating the NPV of rent using different discount rates, investors can assess how sensitive the investment’s value is to changes in the rate. This analysis helps in understanding the range of potential outcomes and ensures that the chosen discount rate is robust. For instance, if the NPV remains positive across a range of discount rates, the investment is likely more resilient to changes in market conditions. In conclusion, selecting the appropriate discount rate requires a careful consideration of market benchmarks, risk factors, opportunity costs, and future expectations, ensuring a realistic and reliable NPV calculation for rental property investments.

JFK Airport: Are Lockers Available for Rent?

You may want to see also

Explore related products

![]()

Cash Flow Projection: Estimating future rental income and expenses

To accurately calculate the Net Present Value (NPV) of rental income, a robust Cash Flow Projection is essential. This involves estimating future rental income and expenses to determine the property’s profitability over time. The first step is to forecast rental income, which depends on factors like market rent trends, lease agreements, and potential vacancy rates. For instance, if the current market rent is $1,500 per month, and you expect a 2% annual increase, the projection would reflect this growth over the investment period. Additionally, account for vacancy periods by estimating a realistic vacancy rate, say 5%, and adjust the income accordingly.

Next, operating expenses must be projected to complete the cash flow picture. These include property taxes, insurance, maintenance, property management fees, and utilities (if not covered by the tenant). For example, if property taxes are $2,400 annually and insurance costs $600, these should be factored in monthly. Maintenance costs can be estimated as a percentage of rental income, typically 10-15%, depending on the property’s age and condition. Summing these expenses provides a clear view of annual outlays, which are then subtracted from the rental income to calculate the net operating income (NOI).

A critical component of cash flow projection is accounting for capital expenditures (CapEx) and replacement reserves. CapEx includes major repairs or upgrades, such as replacing a roof or HVAC system. Setting aside a monthly reserve, say $100, ensures funds are available when needed. These reserves are treated as an expense, reducing the net cash flow but providing a more accurate financial model. Similarly, financing costs, such as mortgage payments, must be included if the property is not owned outright.

Once income and expenses are projected, the discount rate is applied to calculate the NPV. The discount rate reflects the investor’s required rate of return and accounts for the time value of money. For example, if the discount rate is 8%, future cash flows are adjusted to their present value using this rate. The formula for NPV sums the present value of all future cash flows and subtracts the initial investment. A positive NPV indicates a profitable investment, while a negative NPV suggests otherwise.

Finally, sensitivity analysis can enhance the reliability of the cash flow projection. This involves testing how changes in key assumptions—such as rental income growth, vacancy rates, or operating expenses—impact the NPV. For instance, if rental income growth slows to 1% instead of 2%, how does this affect the overall NPV? Such analysis provides a buffer against uncertainty and helps investors make informed decisions. By meticulously estimating future rental income and expenses, investors can create a comprehensive cash flow projection that accurately reflects the property’s financial potential.

Renting vs. Buying: What's Your Home Choice?

You may want to see also

Explore related products

![]()

Time Period Consideration: Defining the analysis period for rent calculation

When calculating the Net Present Value (NPV) of rent, one of the critical initial steps is defining the appropriate time period for the analysis. The time period consideration is essential because it determines the duration over which future rent payments are evaluated and discounted to their present value. This period should align with the lease term, investment horizon, or the specific goals of the financial analysis. For instance, if a lease agreement spans 10 years, the analysis period should ideally cover this entire duration to capture all relevant cash flows. However, if the investor’s focus is on a shorter-term assessment, the period can be adjusted accordingly, though this may limit the comprehensiveness of the analysis.

The choice of the analysis period also depends on the stability and predictability of rent payments. For long-term leases with fixed rent, a longer analysis period is feasible because future cash flows can be projected with reasonable accuracy. Conversely, if rent is subject to frequent adjustments (e.g., market-based rent reviews), the analysis period may need to be shorter to avoid over-relying on uncertain projections. In such cases, sensitivity analysis can be employed to test different rent scenarios over varying time frames, ensuring the NPV calculation remains robust.

Another factor to consider is the discount rate used in the NPV calculation, which is closely tied to the time period. A longer analysis period typically requires a more conservative discount rate to account for increased uncertainty and risk over time. For example, a 10-year analysis might use a higher discount rate than a 5-year analysis to reflect the greater unpredictability of long-term cash flows. Thus, the time period and discount rate must be carefully aligned to ensure the NPV calculation accurately reflects the investment’s risk-adjusted returns.

Additionally, the analysis period should account for any significant events or milestones within the lease term that could impact rent payments. For instance, if a lease includes a rent-free period or a step-up in rent after a certain number of years, these events must be incorporated into the time period to ensure the NPV calculation captures all relevant cash flow changes. Ignoring such milestones could lead to an inaccurate assessment of the investment’s value.

Finally, the time period should be consistent with the broader financial objectives of the analysis. If the goal is to compare the NPV of renting versus purchasing a property, the analysis period should match the expected holding period of the property. Similarly, if the analysis is part of a larger investment portfolio evaluation, the time period should align with the portfolio’s overall investment horizon. By carefully defining the analysis period, the NPV calculation of rent becomes a more reliable tool for informed decision-making.

Renting Smart: Income-Based Renting

You may want to see also

Explore related products

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61gNC08X3PL._AC_UY218_.jpg)

![]()

Inflation Adjustment: Accounting for inflation in future cash flows

When calculating the Net Present Value (NPV) of rent, accounting for inflation is crucial because it ensures that future cash flows are accurately discounted to their present value. Inflation erodes the purchasing power of money over time, meaning that a dollar received in the future is worth less than a dollar today. To incorporate inflation into the NPV calculation, you must adjust both the future rent payments and the discount rate to reflect the expected inflation rate. This ensures that the analysis remains realistic and aligned with economic conditions.

One common method to account for inflation is to use real cash flows and a real discount rate. Real cash flows are nominal cash flows adjusted for inflation, while the real discount rate is the nominal discount rate minus the expected inflation rate. For example, if the nominal rent payment is expected to increase by 3% annually due to inflation, you would adjust the cash flows to reflect their real value. Similarly, if the nominal discount rate is 7% and the expected inflation rate is 2%, the real discount rate would be 5%. This approach ensures that both the cash flows and the discount rate are on the same basis, avoiding double-counting of inflation.

Alternatively, you can use nominal cash flows and a nominal discount rate, but this requires careful consideration of inflation in both components. Nominal cash flows include the effects of inflation, so rent payments would increase over time to reflect rising costs. The nominal discount rate, which includes both the real rate of return and the inflation premium, must be used to discount these cash flows. For instance, if rent is expected to increase by 3% annually due to inflation, and the nominal discount rate is 7%, the calculation would already account for inflation in both the cash flows and the discount rate.

Another important aspect of inflation adjustment is indexing rent to inflation. In many rental agreements, rent is tied to an inflation index, such as the Consumer Price Index (CPI), to ensure that the landlord receives a consistent real return. When calculating the NPV of such rent payments, you must project the future rent based on the expected inflation rate and discount these nominal cash flows using the nominal discount rate. This approach accurately reflects the contractual terms and economic reality of the rental agreement.

Finally, it’s essential to forecast inflation accurately when adjusting future cash flows. Historical inflation rates, economic trends, and government policies can provide insights into expected inflation. However, inflation forecasts are inherently uncertain, so sensitivity analysis can be useful. By testing different inflation scenarios, you can assess how changes in inflation affect the NPV of rent, providing a more robust analysis. Properly accounting for inflation ensures that the NPV calculation is both accurate and reliable, enabling informed decision-making in rental investments.

Understanding Rent-to-Own Homes in Saskatchewan: A Comprehensive Guide

You may want to see also

Explore related products

![Rent: Filmed Live on Broadway [Blu-ray]](https://m.media-amazon.com/images/I/51SDxJNQfVL._AC_UY218_.jpg)

![Rent (Blu-ray) Starring Rosario Dawson, Taye Diggs, Jesse L. Martin, Idina Menzel [Spanish Artwork]](https://m.media-amazon.com/images/I/81wUIoGBEcL._AC_UY218_.jpg)

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)

![]()

Terminal Value Calculation: Estimating property value at the end of the period

When calculating the Net Present Value (NPV) of rent, understanding the Terminal Value (TV) is crucial, as it represents the estimated value of the property at the end of the analysis period. The Terminal Value is a key component in NPV calculations, particularly for long-term investments like real estate, where cash flows extend beyond the explicit forecast period. To estimate the Terminal Value, analysts typically use one of two methods: the Perpetuity Growth Model (Gordon Growth Model) or the Exit Multiple Approach. Both methods aim to capture the property's value at the end of the period, assuming it will continue to generate cash flows indefinitely or be sold at a future date.

The Perpetuity Growth Model is widely used for its simplicity and theoretical foundation. It assumes that the property's cash flows (e.g., net operating income) will grow at a constant rate indefinitely. The formula for Terminal Value using this method is: *TV = (Net Operating Income in the final year × (1 + Growth Rate)) / (Discount Rate – Growth Rate)*. Here, the Net Operating Income (NOI) is the income generated by the property after operating expenses but before financing and taxes. The Growth Rate is the assumed long-term growth rate of the NOI, typically conservative (e.g., 2-3%), and the Discount Rate is the required rate of return for the investment. This method is ideal for stable, income-generating properties with predictable cash flows.

Alternatively, the Exit Multiple Approach estimates Terminal Value by applying a multiple to a metric like NOI or gross rent in the final year of the forecast period. The formula is: *TV = Final Year NOI × Exit Multiple*. The Exit Multiple is derived from comparable sales or market data, reflecting how much an investor would pay for a property relative to its income. For example, if similar properties trade at a 10x NOI multiple, the Terminal Value would be the final year's NOI multiplied by 10. This method is more market-driven and is often used when comparable transactions are available.

Choosing between these methods depends on the availability of data and the nature of the property. For instance, the Perpetuity Growth Model is more theoretical and relies on assumptions about long-term growth, while the Exit Multiple Approach is grounded in market comparables. Regardless of the method, the Terminal Value is then discounted back to the present using the Discount Rate to determine its contribution to the overall NPV of the rental property.

Finally, it's essential to validate the Terminal Value calculation by performing sensitivity analyses. Varying key inputs such as the Growth Rate, Discount Rate, or Exit Multiple helps assess how robust the NPV is to changes in assumptions. Accurately estimating the Terminal Value ensures that the NPV calculation reflects the property's long-term potential, providing a comprehensive view of the investment's viability. By carefully considering these factors, investors can make informed decisions about the present value of future rental income.

Renting with a Criminal Record: Strategies for Finding Housing

You may want to see also

Frequently asked questions

Net Present Value (NPV) of rent is the calculation of the current value of future rental payments, discounted to reflect the time value of money. It is important because it helps landlords, investors, and tenants evaluate the profitability of a rental agreement by considering the present worth of future cash flows.

The NPV of rent is calculated by summing the present values of all future rental payments, discounted at a chosen discount rate. The formula is:

NPV = ∑ [Rent Payment / (1 + Discount Rate)^t], where t is the period number.

The discount rate used should reflect the opportunity cost of capital or the required rate of return for the investment. Common choices include the risk-free rate, the weighted average cost of capital (WACC), or a rate adjusted for inflation and risk.

Inflation can be factored into the NPV calculation by either adjusting the rental payments for inflation before discounting or by using a real discount rate (adjusted for inflation). Ignoring inflation can lead to an overestimation of the NPV if future rental payments are not inflation-adjusted.