The cost of rent is a significant expense for many, and it's essential to understand how much of your income should go towards it. The most common rule of thumb is the 30% rule, which suggests that 30% of your gross income should be spent on rent. However, this may not always be feasible, especially in high-cost cities like New York or San Francisco. In these cases, it might be necessary to spend a higher percentage of your income on rent, but it could also mean compromising on the location or size of the rental property. On the other hand, if you live in an affordable area, you might be able to spend less than 30% of your income on rent and save more or spend more on non-essential items. Other guidelines, like the 50/30/20 budget, suggest allocating 50% of your income to needs (including rent), 30% to wants, and 20% to savings and debt payments. Ultimately, the decision on how much to spend on rent depends on various factors, including income, cost of living, and other financial obligations.

| Characteristics | Values |

|---|---|

| Rule of thumb | 30% of gross income |

| Other rules | 25% of net income, 40% of gross income for higher earners, 50/30/20 rule |

| Other factors | Cost of living, other bills, location, lifestyle |

| Average rent | $1,749 according to RentCafe |

Explore related products

What You'll Learn

![]()

The 30% rule

For instance, in high-cost cities like New York City or San Francisco, where rents are significantly higher, sticking to the 30% rule may not be realistic. On the other hand, in more affordable areas, spending less than 30% of your income on rent may be achievable, allowing for more financial flexibility.

Additionally, the 30% rule has been criticised as an outdated concept, originating from public housing regulations in the 1960s and 1980s. Critics argue that it does not account for modern financial realities, such as student loan payments, retirement savings, and other essential expenses. As a result, some people may find that even with the 30% rule, their budget for other necessities is constrained.

Despite these criticisms, the 30% rule can serve as a starting point or a maximum threshold for individuals creating their budget. It can help people avoid overspending on housing and maintain financial stability by ensuring they have sufficient funds for other expenses and savings.

In conclusion, while the 30% rule provides a general guideline for rent affordability, it is essential to consider individual circumstances and create a budget tailored to specific needs and financial goals.

Best Places to Rent a Steam Cleaner for Your Couch

You may want to see also

Explore related products

![]()

Location

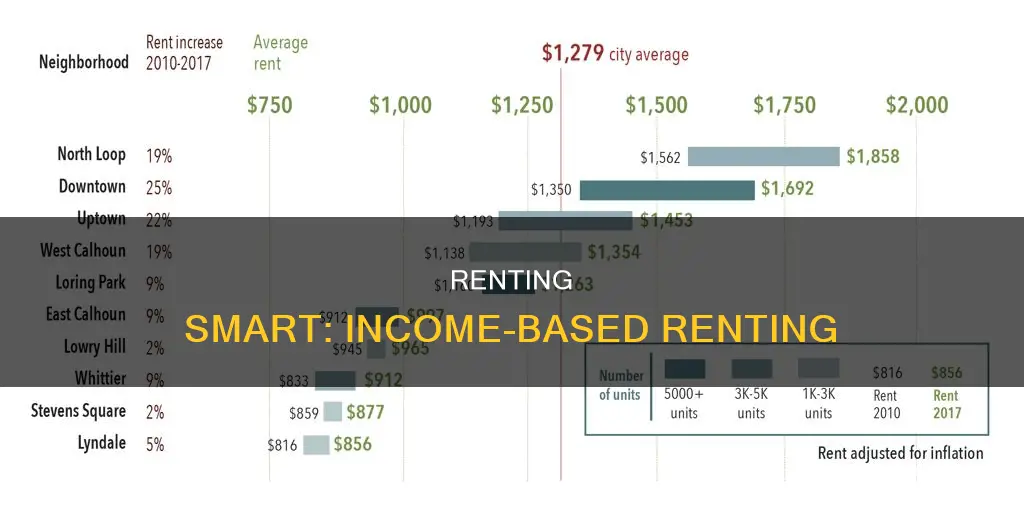

When determining how much rent you can afford, location is a key factor to consider. The cost of renting varies significantly depending on where you live, and this can greatly influence the amount of your income that you'll need to allocate to rent.

In major metropolitan areas, rentals can be scarce due to factors like population density or local policy. In such locations, the competition for vacant rentals is high, and renters may need to pay an agency to assist in their search. Once a desirable property is found, an application must be submitted promptly. In competitive markets, the renter normally pays the agent's fee, which is usually equivalent to one month's rent.

The location of a rental property relative to places that an individual frequents and their interests is also an important consideration. For example, an individual who enjoys hiking may want to consider a property close to hiking trails, while someone who enjoys a daily coffee may prefer to live near cafes. Additionally, most people prefer to live close to their workplace, family, and friends.

The affordability of a location is a crucial aspect of choosing a rental property. According to the 30% rule, a widely accepted guideline, individuals should spend around 30% of their gross income on rent. However, this rule may not always be feasible in high-cost cities like New York City or San Francisco, where median rents exceed $3,000 for a one-bedroom apartment. In such cases, individuals may need to consider allocating a higher percentage of their income to rent or opting for a less desirable location.

On the other hand, in affordable areas, individuals may find rentals that constitute a lower percentage of their income. For example, a rental that accounts for only 18% of one's income may be a good deal and should not be overlooked.

The income level of an individual plays a significant role in determining the location of their rental property. If an individual earns an above-average income, allocating 40% of it toward rent can secure a rental in a better location or provide more living space.

In summary, when deciding on a rental property, it is essential to consider the location relative to one's preferences and interests, the affordability of the area, and the income level that can be allocated toward rent. These factors will help determine the ideal location that aligns with an individual's budget and lifestyle choices.

Renting Smart: How Much of Your Income?

You may want to see also

Explore related products

![]()

Cost of living

The cost of living is a significant factor in determining how much rent you should budget for. The general rule of thumb is to spend no more than 30% of your gross income on rent, but this is not always feasible, especially in high-cost cities like New York or San Francisco.

Your rent budget should be considered in the context of your other expenses and financial goals. The 50/30/20 budget rule suggests that 50% of your after-tax income goes towards needs, 30% towards non-essential or 'want' expenses, and 20% towards savings. However, this rule may not be suitable for everyone, and some sources suggest a 60/30/10 budget to accommodate higher needs costs.

If you are a high earner, spending 30% of your income on rent may be irresponsible, as it could hinder other financial goals, such as saving for retirement or investing in property. In this case, keeping your rent budget to 20% or 25% of your income may be more prudent.

The location of your rental property is a crucial factor in determining cost. Living in the heart of a city tends to be more expensive, but you may save on transportation costs. Conversely, living farther out may reduce your rent costs but increase transportation expenses.

Other factors to consider when budgeting for rent include utilities, additional amenities, and any debts or living expenses, such as insurance or pet costs. It is essential to calculate all your costs before signing a lease to ensure you can afford the rent without financial strain.

Rent-to-Own Homes: California's Guide

You may want to see also

Explore related products

$39.25 $48.99

![]()

Other bills

When considering how much rent you can afford, it's important to take into account your other bills and expenses. A popular guideline is the 30% rule, which recommends spending around 30% of your gross income on rent. However, this may vary depending on your city's cost of living and other financial obligations. Here are some other bills and factors to consider when determining how much rent you can afford:

Utility Bills: These include electricity, gas, and water bills. Some landlords may include these utilities in the monthly rent, so it's essential to clarify which utilities are included and which ones you need to pay separately. The cost of utility bills can vary depending on factors such as your location, the number of people in your household, and the efficiency of your appliances.

Internet and Cable: Internet and cable services can add to your monthly expenses. The cost of these services depends on factors such as location, market competition, and standalone versus bundled options. If you're looking to cut costs, you can consider eliminating your home internet and cable services by relying on mobile data or accessing the internet from work or school.

Transportation Costs: If you choose to rent farther from the city centre, you may save on rent but incur higher transportation costs for commuting to work and social engagements. On the other hand, living in a well-connected area with good public transportation or bicycle infrastructure may reduce your need for a car, lowering your transportation expenses.

Insurance and Indemnification: Rental insurance may be required, and bundling it with other insurance policies such as car or life insurance can help you save money.

Application and Processing Fees: When applying for a rental property, you may need to pay application and processing fees to cover the costs of credit checks, rental history checks, and background checks.

Moving Expenses: Don't forget to factor in the costs associated with moving, such as packing materials, transportation, and any deposits or fees associated with setting up new utilities at your new residence.

It's important to create a budget that takes into account your income, fixed costs, variable costs, and incidentals. This will help you determine how much rent you can comfortably afford while staying on top of your other financial obligations and maintaining your desired lifestyle.

Renting Your RV on Airbnb: A Guide to Success

You may want to see also

Explore related products

![]()

The 50/30/20 rule

When deciding how much of your income should go towards rent, one popular guideline is the 30% rule, which says to spend about 30% of your gross income on rent. However, this is not a one-size-fits-all solution. For example, if you live in an affordable area, you could get a good deal on rent that is only 18% of your income. On the other hand, sticking to the 30% rule might not always be feasible in places like New York City or San Francisco, where median rents are well over $3,000 for a one-bedroom apartment.

Another guideline is the 50/30/20 rule, a simple and effective plan for personal money management and wealth creation. This rule allocates your take-home pay (after taxes) into three categories: 50% for needs, 30% for wants, and 20% for savings and additional debt payments.

Using the 50/30/20 rule, someone with a monthly income of $4,000 would aim to keep the cost of their needs, such as rent, utilities, groceries, insurance, and minimum debt payments, below $2,000. However, with other expenses, this could leave only $880 for rent and utilities, which might not be enough unless you're planning to split rent payments with someone else.

While the 50/30/20 rule can be a helpful guideline, it's important to remember that budgets are flexible and should be adjusted to fit your specific needs and goals.

Arch Rentals for Your Dream Wedding

You may want to see also

Frequently asked questions

The 30% rule, also known as the One-Third Rule, is a guideline that suggests that 30% of your gross income or pre-tax income should be spent on rent. However, this rule is flexible and depends on your income, the cost of living in your city, and your other expenses.

The 50/30/20 rule is a budget guideline that allocates 50% of your take-home pay (after taxes) to essential needs, 30% to wants, and 20% to savings and additional debt payments. This rule provides a balance between financial obligations, lifestyle, and wealth accumulation.

To determine how much rent you can afford, consider your income, location, lifestyle, and additional housing costs. Online rent calculators can assist in estimating affordable rent based on your income and expenses.

To manage rent expenses, consider sharing rent payments with roommates. Additionally, look for areas with lower rents, such as the suburbs, to find more affordable options. Creating a budget and tracking expenses can also help manage rent costs in relation to your income and other financial obligations.