The issue of rent burden is a pressing concern across the nation, affecting millions of households who spend a disproportionate amount of their income on housing. Defined as spending more than 30% of one's income on rent, being rent burdened can lead to financial instability, reduced savings, and limited access to other essential needs like healthcare and education. Nationwide, the number of rent-burdened individuals has been steadily rising due to factors such as stagnant wages, skyrocketing housing costs, and a shortage of affordable housing options. Understanding the scale of this problem is crucial for policymakers, advocates, and communities to develop effective solutions and alleviate the strain on families struggling to make ends meet.

Explore related products

What You'll Learn

![]()

Definition of Rent Burdened Households

A household is considered rent burdened when it spends more than 30% of its income on housing costs. This threshold, established by the U.S. Department of Housing and Urban Development (HUD), serves as a critical benchmark for assessing housing affordability. For example, a family earning $4,000 monthly would be rent burdened if their rent exceeds $1,200. This definition is not arbitrary; it reflects the balance between housing expenses and the ability to cover other necessities like food, healthcare, and transportation. When households surpass this limit, they often face financial strain, making them vulnerable to eviction, debt, or poverty.

The 30% rule, however, is not one-size-fits-all. It assumes a standardized budget where housing is the largest expense, but individual circumstances vary. For instance, low-income households may need to allocate more than 30% to secure even substandard housing, while higher-income households might comfortably spend above this threshold without financial distress. Critics argue that this definition fails to account for regional cost-of-living disparities, family size, or fluctuating incomes. Despite these limitations, the 30% metric remains the most widely used tool for identifying rent-burdened households nationwide.

To illustrate, consider a single parent earning $30,000 annually in a high-cost urban area. If their rent is $1,000 monthly, they are spending 40% of their income on housing, well above the 30% threshold. This leaves them with limited funds for childcare, groceries, and other essentials. In contrast, a dual-income household earning $100,000 annually might spend $2,500 on rent (30% of their income) without experiencing financial hardship. These examples highlight the need for a more nuanced approach to defining rent burden, one that considers income levels, geographic location, and household composition.

Policymakers and researchers are increasingly advocating for alternative metrics to complement the 30% rule. One such measure is the "residual income approach," which assesses how much income remains after housing costs are deducted, ensuring it is sufficient to cover other basic needs. Another is the "housing expense-to-income ratio," which adjusts the threshold based on local housing market conditions. For instance, in cities like San Francisco or New York, where housing costs are exorbitant, a higher threshold might be more realistic. Adopting such tailored definitions could provide a clearer picture of the true extent of rent burden nationwide.

Ultimately, understanding the definition of rent-burdened households is crucial for addressing the housing affordability crisis. While the 30% rule is a useful starting point, it must be applied with caution and supplemented with context-specific data. By refining our definition, we can better identify vulnerable populations, allocate resources effectively, and develop policies that ensure stable, affordable housing for all. This shift in perspective is not just academic—it has real-world implications for millions of households struggling to make ends meet.

Tropicana Palms NV Lot Rent: Costs and Community Insights

You may want to see also

Explore related products

![]()

National Rent Burden Statistics by Year

The number of rent-burdened households in the United States has fluctuated over the past decade, reflecting broader economic trends and housing market dynamics. According to the U.S. Department of Housing and Urban Development (HUD), a household is considered rent-burdened if it spends more than 30% of its income on rent and utilities. In 2010, approximately 46% of renter households nationwide were rent-burdened, a figure that climbed to 49.7% by 2016, despite economic recovery from the Great Recession. This increase highlights the growing disparity between wage growth and rising rental costs during that period.

Analyzing year-over-year trends reveals critical inflection points. For instance, between 2018 and 2019, the national rent burden rate dipped slightly from 47.4% to 47.1%, coinciding with a surge in multifamily housing construction in some metropolitan areas. However, this relief was short-lived. By 2021, the rate rebounded to 46.8%, driven by pandemic-related economic disruptions and a sharp increase in rental prices. Low-income households were disproportionately affected, with over 70% of renters earning below $30,000 annually facing rent burdens, compared to just 10% of those earning above $75,000.

Regional disparities further complicate the national picture. In 2022, states like California, Florida, and New York reported rent burden rates exceeding 50%, while more affordable markets like Iowa and West Virginia remained below 35%. These variations underscore the need for localized solutions, such as expanding housing vouchers or incentivizing affordable housing development in high-cost areas. Policymakers must also address systemic issues like zoning restrictions and construction costs, which limit housing supply and exacerbate affordability crises.

To mitigate rent burdens effectively, individuals and families can take proactive steps. First, explore federal and state rental assistance programs, such as HUD’s Housing Choice Voucher Program. Second, consider shared housing arrangements or relocating to areas with lower living costs, though this may involve trade-offs in employment opportunities or proximity to family. Finally, advocate for policy changes that promote equitable housing access, such as rent control measures or increased funding for public housing initiatives. Without concerted action, the number of rent-burdened households will likely continue to rise, perpetuating cycles of financial instability and inequality.

Renting Your Own CDs: Legal or Not? A Comprehensive Guide

You may want to see also

Explore related products

![]()

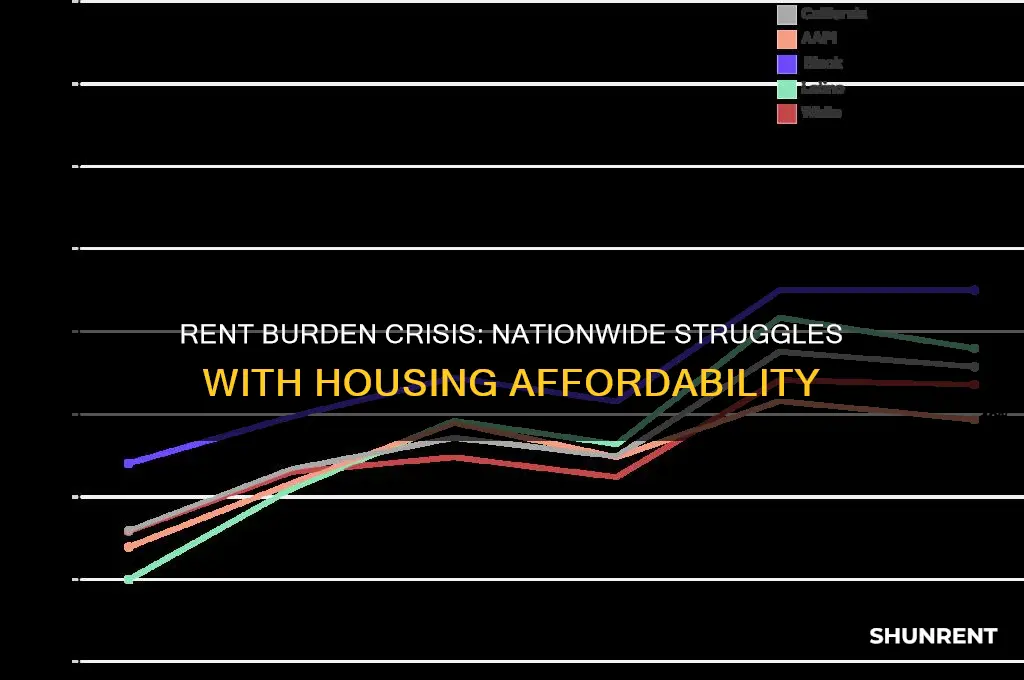

Demographics Most Affected by Rent Burden

Rent burden, defined as spending more than 30% of income on housing, disproportionately affects specific demographic groups, exacerbating economic inequality. Among these, low-income households stand out as the most vulnerable. According to the National Low Income Housing Coalition, nearly half of renters earning below $30,000 annually are severely rent-burdened, spending over 50% of their income on housing. This financial strain leaves little room for other essentials like healthcare, education, or savings, trapping individuals in a cycle of poverty. For context, a family earning $25,000 annually and paying $1,000 in monthly rent allocates 48% of their income to housing alone, far exceeding the recommended threshold.

Another demographic acutely impacted by rent burden is single-parent households, particularly those headed by women. Data from the U.S. Census Bureau reveals that 43% of female-headed households with children are rent-burdened, compared to 30% of male-headed households. This disparity is compounded by the gender wage gap and limited access to affordable childcare, forcing many single mothers to prioritize housing over other critical needs. For instance, a single mother earning $35,000 annually and paying $1,200 in rent spends 41% of her income on housing, leaving minimal funds for childcare or unexpected expenses.

Racial disparities also play a significant role in rent burden, with Black and Hispanic households disproportionately affected. The Urban Institute reports that 47% of Black renters and 44% of Hispanic renters are cost-burdened, compared to 38% of white renters. Historical redlining practices, systemic discrimination in lending, and wage inequities contribute to this gap. For example, a Black family earning $40,000 annually and paying $1,300 in rent allocates 39% of their income to housing, while a white family with the same income and rent spends 39% as well, but benefits from greater generational wealth and financial stability.

Young adults, particularly those aged 25–34, face increasing rent burdens as they navigate early careers and student loan debt. The Joint Center for Housing Studies notes that 45% of renters in this age group are cost-burdened, often delaying milestones like homeownership or starting a family. For instance, a recent college graduate earning $45,000 annually and paying $1,500 in rent spends 40% of their income on housing, while also managing $300 monthly student loan payments. This dual financial pressure underscores the need for targeted policies, such as rent control or expanded housing vouchers, to alleviate the strain on these demographics.

Finally, seniors on fixed incomes are increasingly vulnerable to rent burden as housing costs outpace Social Security adjustments. The AARP reports that 48% of renters aged 65 and older are cost-burdened, with many forced to choose between housing and medical care. For example, a retiree receiving $18,000 annually in Social Security and paying $900 in rent spends 60% of their income on housing, leaving just $300 per month for all other expenses. Addressing this crisis requires innovative solutions, such as incentivizing affordable senior housing development and expanding rental assistance programs tailored to elderly populations.

Renting DVC Points: Your Ultimate Guide to Disney World Vacations

You may want to see also

Explore related products

![]()

Regional Variations in Rent Burden Rates

Rent burden rates, defined as households spending over 30% of their income on housing, vary dramatically across regions, reflecting disparities in local economies, housing markets, and demographic profiles. For instance, coastal cities like Los Angeles and New York consistently report rent burden rates exceeding 50%, driven by high housing demand and limited supply. In contrast, Midwestern cities such as Indianapolis and Cleveland see rates closer to 30%, thanks to lower living costs and more affordable housing stock. These regional differences highlight the need for localized solutions to address housing affordability.

Analyzing the data reveals that metropolitan areas with thriving tech or finance industries often experience higher rent burden rates due to influxes of high-earning professionals driving up housing costs. For example, San Francisco’s median rent-to-income ratio is nearly 45%, making it one of the least affordable cities nationwide. Conversely, rural areas and smaller towns typically have lower rates, as incomes and housing prices remain relatively stable. However, even in these regions, low-income households can still face significant rent burdens, as wages often fail to keep pace with rising costs.

To address regional disparities, policymakers must consider tailored interventions. In high-burden cities, increasing housing supply through zoning reforms and incentivizing affordable development can alleviate pressure on renters. For example, Minneapolis’s 2040 Plan, which eliminates single-family zoning, aims to create more housing options and reduce costs. In contrast, rural areas may benefit from initiatives like rent subsidies or workforce housing programs to ensure residents can afford to live where they work. Balancing these approaches requires understanding each region’s unique challenges and resources.

A comparative look at Sun Belt cities like Phoenix and Atlanta shows how rapid population growth can exacerbate rent burdens. Both cities have seen rents spike by over 20% in recent years, outpacing wage growth and pushing more households into rent-burdened status. Meanwhile, older industrial cities like Detroit and Pittsburgh have experienced slower growth but still face challenges due to stagnant wages and aging housing stock. This comparison underscores the importance of proactive planning to manage growth and preserve affordability, whether in booming or declining markets.

Finally, demographic factors play a critical role in regional rent burden rates. In the Southeast, for example, a higher proportion of elderly and minority households face rent burdens due to fixed incomes and systemic inequalities. Programs targeting these groups, such as expanded housing vouchers or senior housing initiatives, can make a significant impact. By focusing on the specific needs of each region’s population, policymakers can create more equitable solutions to the nationwide rent burden crisis.

Maximize Your Savings: A Guide to Rent-A-Center Benefits Plus

You may want to see also

Explore related products

$15.69 $35

$170.62 $249.99

![]()

Policy Impacts on Rent Burden Trends

Rent burden, defined as spending more than 30% of household income on housing, affects millions of Americans, with recent data indicating that over 40% of renters nationwide are cost-burdened. This crisis is not merely a product of market forces but is significantly shaped by policy decisions at local, state, and federal levels. Understanding how policies influence rent burden trends is critical for crafting effective solutions.

Analytical Perspective:

Policies like rent control, while intended to stabilize housing costs, often have unintended consequences. For instance, rent-controlled units in cities like San Francisco and New York may benefit existing tenants but can reduce the overall housing supply as landlords opt to convert rentals into condos or Airbnb listings. This scarcity drives up rents in uncontrolled units, exacerbating rent burden for new entrants to the market. Conversely, inclusionary zoning policies, which require developers to allocate a percentage of units as affordable housing, can mitigate rent burden by increasing supply for low- and moderate-income households. However, these policies must be paired with subsidies or tax incentives to ensure developers remain financially viable.

Instructive Approach:

To address rent burden effectively, policymakers should focus on three key strategies. First, expand housing vouchers to cover more eligible households; currently, only one in four eligible families receive assistance due to funding limitations. Second, incentivize the construction of affordable housing through tax credits, density bonuses, and streamlined permitting processes. Third, invest in public housing maintenance and development to provide stable, low-cost options for vulnerable populations. For example, the Low-Income Housing Tax Credit (LIHTC) program has financed over 3 million affordable units since 1986, demonstrating the impact of targeted policy interventions.

Persuasive Argument:

The federal government must take a more proactive role in addressing rent burden. While local policies like just-cause eviction laws and rent stabilization measures provide temporary relief, they are insufficient without federal funding for large-scale affordable housing initiatives. Increasing the national Housing Trust Fund, which supports the development and preservation of affordable homes, could significantly reduce rent burden nationwide. Additionally, tying federal grants to localities that eliminate exclusionary zoning practices would encourage the construction of multi-family housing in high-opportunity areas, breaking down barriers to affordability.

Comparative Analysis:

Comparing rent burden trends in cities with and without strong tenant protections reveals the limitations of policy-driven solutions. For example, Portland, Oregon, implemented a rent control policy in 2017, capping annual rent increases at 7% plus inflation. While this slowed rent growth initially, it also led to a 15% reduction in new rental listings, as landlords chose to sell properties rather than operate under stricter regulations. In contrast, Minneapolis eliminated single-family zoning in 2018, allowing for denser, more affordable housing development. This policy has increased housing supply without directly controlling rents, offering a more sustainable model for reducing rent burden.

Descriptive Insight:

The impact of policy on rent burden is often felt most acutely in marginalized communities. For instance, the Section 8 Housing Choice Voucher program, while effective in reducing rent burden for participants, faces chronic underfunding and administrative barriers that limit its reach. In cities like Los Angeles, where the waitlist for vouchers can exceed 10 years, low-income families are forced to spend upwards of 50% of their income on rent, perpetuating cycles of poverty. Policies that prioritize equitable access to housing assistance, such as source-of-income protections and expanded funding for voucher programs, are essential to addressing these disparities.

In conclusion, policy plays a pivotal role in shaping rent burden trends, with both intended and unintended consequences. By adopting a multi-faceted approach that combines supply-side incentives, demand-side subsidies, and equitable access measures, policymakers can create a housing market that works for everyone. The challenge lies in balancing immediate relief with long-term sustainability, ensuring that no one is left behind in the fight against rent burden.

Renting Wheelchairs in Charleston, SC: Top Locations and Tips

You may want to see also

Frequently asked questions

A household is considered rent burdened if it spends more than 30% of its income on rent and utilities, as defined by the U.S. Department of Housing and Urban Development (HUD).

As of recent data, approximately 40-50% of renters in the United States are considered rent burdened, which translates to around 20-25 million households.

Low-income households, minorities, and young adults are disproportionately affected by rent burden. Additionally, single-parent households and seniors on fixed incomes often struggle with high rental costs.

The number of rent-burdened households has increased significantly over the past decade due to rising rents, stagnant wages, and a shortage of affordable housing. In 2010, approximately 38% of renters were rent burdened, compared to the current estimate of 40-50%.