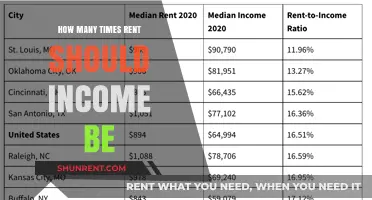

When considering the financial implications of housing, it’s essential to compare monthly rent to other significant expenses or investments to understand its relative scale. For instance, examining how many times larger monthly rent is compared to utilities, groceries, or savings can provide valuable insights into budgeting and financial planning. This comparison helps individuals gauge whether their rent is disproportionately high or if it aligns with their overall financial goals. By analyzing this ratio, one can make informed decisions about housing affordability, lifestyle adjustments, or potential relocation, ensuring a balanced and sustainable financial strategy.

Explore related products

What You'll Learn

![]()

Comparing annual rent to monthly rent

Annual rent is simply the total amount a tenant pays over 12 months, but understanding its relationship to monthly rent reveals critical financial insights. For instance, annual rent is exactly 12 times the monthly rent, assuming no changes in lease terms. However, this straightforward calculation often masks hidden costs or savings. For example, some landlords offer a discount for paying rent annually, effectively making the annual rent less than 12 times the monthly rate. Conversely, late fees or rent increases during the year can inflate the annual total. This basic comparison is the foundation for deeper financial planning and negotiation.

To accurately compare annual rent to monthly rent, tenants should account for variability in lease agreements. A fixed monthly rent of $1,500 would total $18,000 annually, but this ignores potential fluctuations. For instance, a lease might include a 3% annual increase, making the second year’s rent $1,545 per month, or $18,540 annually. Additionally, prorated rent for partial months or move-in specials can skew the comparison. Tenants should calculate the *effective annual rent* by summing all monthly payments, including adjustments, to understand the true cost. This method ensures a realistic budget and highlights opportunities to save.

From a budgeting perspective, comparing annual to monthly rent helps tenants align expenses with income. Monthly rent is often easier to manage within a paycheck cycle, but annual rent provides a long-term view of housing costs. For example, a tenant earning $60,000 annually might allocate 30% of their income to housing, or $18,000 per year. If monthly rent is $1,500, this fits neatly within the 30% rule. However, if annual rent includes additional fees or increases, it could exceed this threshold. By comparing both figures, tenants can adjust spending in other areas or negotiate terms to stay within budget.

Persuasively, understanding the annual rent-to-monthly rent ratio empowers tenants in lease negotiations. Landlords often emphasize monthly payments to make rent seem more affordable, but framing the conversation around annual costs can reveal room for discounts. For instance, offering to pay rent annually upfront might secure a 5% reduction, effectively lowering the monthly equivalent. Similarly, tenants can negotiate lower monthly rates by committing to a longer lease term, reducing the annual total. This strategic approach shifts the focus from short-term affordability to long-term savings, benefiting both parties.

Finally, comparing annual and monthly rent is essential for financial forecasting and decision-making. For renters considering buying a home, knowing their annual rent expenditure helps assess mortgage affordability. If annual rent is $18,000, a mortgage with similar monthly payments (e.g., $1,500) might seem comparable, but homeowners must also factor in property taxes, insurance, and maintenance. Conversely, renters might realize that their annual rent exceeds the cost of owning in their area, prompting a shift in priorities. This comparison bridges short-term renting with long-term financial goals, making it a vital tool for anyone managing housing expenses.

Oregon Rent Late Fees: Understanding Grace Periods and Deadlines

You may want to see also

Explore related products

![]()

Calculating rent size differences over time

Rent inflation often outpaces general consumer price increases, making historical comparisons essential for tenants and landlords alike. To calculate how many times larger current rent is compared to past figures, start by gathering monthly rent data for the same property or comparable units over specific periods—say, 10 or 20 years. Use inflation-adjusted values to ensure accuracy; for instance, a $1,000 rent in 2003 would be equivalent to roughly $1,600 in 2023 dollars. Divide the current rent by the adjusted historical rent to determine the multiplier. For example, if today’s rent is $2,000 and the 2003 equivalent is $1,200, the rent is 1.67 times larger. This method reveals the true growth rate, stripping away the distortion of general inflation.

Analyzing rent size differences over time requires more than raw numbers—it demands context. Consider external factors like neighborhood gentrification, local job market growth, or changes in zoning laws. For instance, a once-affordable area may now command rents three times higher due to a tech industry boom. Pairing rent multipliers with demographic shifts or economic trends provides a clearer picture of why disparities exist. A rent that’s four times larger than it was in 1990 might reflect not just inflation but also increased demand from a younger, higher-earning population moving into the area.

For practical application, tenants can use rent multipliers to negotiate leases or assess long-term affordability. If a property’s rent has grown 2.5 times faster than the regional average, question whether the increase is justified by improvements or market conditions. Landlords, meanwhile, can benchmark their properties against historical trends to set competitive yet profitable rates. Tools like rent-to-income ratios (ideally below 30%) can help both parties evaluate sustainability. For example, if rent has tripled over 15 years but median incomes have only doubled, affordability becomes a pressing concern.

A cautionary note: relying solely on multipliers can oversimplify complex dynamics. Rent control policies, housing supply shortages, or speculative investments can skew data. Always cross-reference with local housing reports and consider outliers. For instance, a post-recession dip in rents might artificially inflate the multiplier for the recovery period. Pair quantitative analysis with qualitative insights—such as tenant turnover rates or vacancy trends—to avoid misinterpretation. By combining historical data with current realities, both renters and landlords can make informed decisions about pricing, budgeting, and long-term planning.

Bohemian Rhapsody Rental: Is It Available on Service Electric?

You may want to see also

Explore related products

![]()

Rent vs. other monthly expenses

Rent often dwarfs other monthly expenses, consuming 30-50% of a household's income, according to the U.S. Department of Housing and Urban Development. This disproportionate allocation forces a reevaluation of budgeting priorities. For instance, while groceries might average $400 monthly for a family of four, rent could easily surpass $1,500 in urban areas. This stark contrast highlights the necessity of strategic financial planning to balance housing costs with essentials like food, transportation, and healthcare.

Consider the comparative impact of rent versus utilities. A typical monthly utility bill ranges from $100 to $200, a fraction of rent yet still critical. However, rent’s fixed nature leaves little room for negotiation, unlike utilities, which can be optimized through energy-efficient practices. For renters, this means prioritizing housing stability while seeking ways to reduce variable expenses. For example, switching to LED bulbs or using programmable thermostats can trim utility costs, freeing up funds for rent without compromising lifestyle.

Persuasively, rent’s dominance in monthly budgets underscores the need for proactive measures. Renters should explore cost-saving strategies like roommate arrangements or relocating to more affordable neighborhoods. For instance, sharing a two-bedroom apartment can halve rent, making it comparable to combined grocery and utility expenses. Alternatively, negotiating lease terms or seeking rent-controlled units can provide long-term savings. These steps empower individuals to reclaim financial flexibility in the face of escalating housing costs.

Descriptively, the rent-to-expense ratio varies by demographic and location. A young professional in San Francisco might spend 60% of their income on rent, leaving minimal funds for savings or leisure. In contrast, a retiree in a rural area may allocate only 20%, allowing for greater discretionary spending. This disparity emphasizes the importance of tailoring budgets to individual circumstances. For instance, a high-rent tenant could adopt a minimalist lifestyle, cutting entertainment and dining out to offset housing costs, while a low-rent tenant might invest in experiences without financial strain.

Instructively, balancing rent with other expenses requires a three-step approach: assess, adjust, and automate. First, calculate your rent-to-income ratio; if it exceeds 30%, reassess housing options. Second, trim non-essential expenses like subscriptions or dining out to allocate more funds to rent or savings. Finally, automate savings and bill payments to ensure financial stability. For example, setting up a monthly transfer of 10% of income to savings can build an emergency fund, providing a safety net for unexpected rent increases or other expenses. This structured approach ensures rent remains manageable without overshadowing other financial obligations.

Exploring St. George, Utah: Average Rent Costs Revealed

You may want to see also

Explore related products

![]()

Regional rent size variations analysis

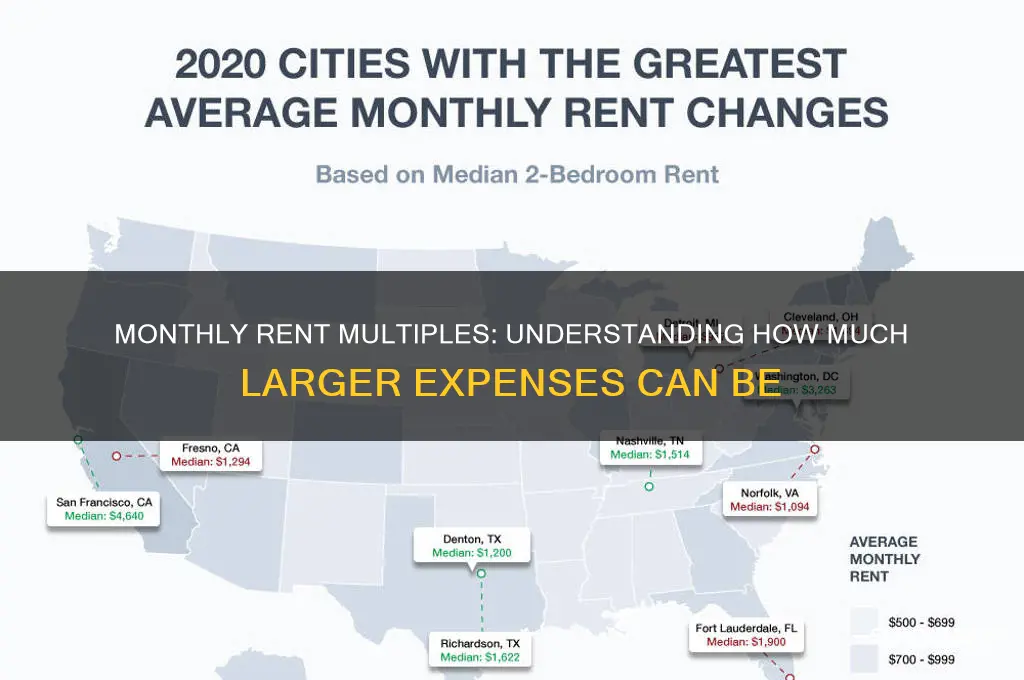

Rent disparities across regions often reveal startling contrasts, with some areas demanding monthly payments that dwarf those in others. For instance, in San Francisco, the median rent hovers around $4,500, while in Tulsa, Oklahoma, it’s roughly $850. This means a San Francisco tenant pays over five times more than their Tulsa counterpart. Such variations aren’t just numbers—they dictate lifestyle choices, savings potential, and even career paths. Understanding these regional differences is crucial for anyone considering relocation or investment in real estate.

Analyzing these disparities requires examining local economies, housing supply, and population density. High-rent cities like New York or Los Angeles often boast robust job markets but suffer from limited housing inventory, driving prices skyward. Conversely, smaller cities with lower rents typically have fewer high-paying jobs but greater housing availability. For example, in Austin, Texas, the tech boom has pushed rents up by 40% in the past five years, narrowing the gap with historically expensive cities. This dynamic underscores how regional rent sizes are tied to economic growth and urban planning.

To navigate these variations, consider a practical strategy: compare rent-to-income ratios across regions. Financial advisors recommend spending no more than 30% of your income on housing. In high-rent areas, this might mean seeking roommates or opting for smaller spaces. For instance, a tenant in Seattle earning $60,000 annually should aim for rent under $1,500, while someone in Indianapolis with the same income could comfortably afford up to $1,200. This approach ensures financial stability regardless of regional rent size.

Persuasively, it’s worth noting that regional rent variations also influence long-term wealth accumulation. In low-rent areas, tenants can save or invest a larger portion of their income, potentially building equity faster. For example, a tenant in Memphis saving $500 monthly on rent compared to a Chicago counterpart could accumulate $6,000 annually—enough for a substantial emergency fund or down payment. Thus, choosing a region with rent aligned to your financial goals can significantly impact your economic future.

Finally, a descriptive lens reveals how these variations shape local cultures. High-rent cities often foster transient populations, as residents move frequently in search of affordability. In contrast, low-rent regions may encourage deeper community roots, as residents can afford to stay longer. For instance, Portland, Oregon’s rising rents have displaced long-time residents, altering its cultural fabric, while cities like Columbus, Ohio, maintain a stable, close-knit community. This cultural dimension adds another layer to the analysis of regional rent size variations.

Exploring Philadelphia's Left Bank: Understanding Rent Costs and Trends

You may want to see also

Explore related products

![]()

Impact of rent increases on affordability

Rent increases often outpace wage growth, creating a widening gap between what tenants earn and what they must pay to keep a roof over their heads. For instance, in cities like San Francisco and New York, rents have surged by 20-30% over the past five years, while median incomes have risen by only 10-15%. This disparity forces households to allocate a larger share of their income to housing, leaving less for essentials like food, healthcare, and education. When rent consumes more than 30% of monthly income—a threshold widely considered the maximum for affordability—tenants face financial instability and increased risk of eviction.

Consider a practical example: a family earning $4,000 monthly could comfortably afford $1,200 in rent, adhering to the 30% rule. However, if rent increases by $400 (a common scenario in high-demand markets), their housing expense jumps to 40% of income. To compensate, they might cut back on groceries, delay medical care, or accumulate debt. Over time, this strain erodes savings and financial resilience, making it harder to recover from unexpected expenses or economic downturns.

The impact of rent increases isn’t uniform; it disproportionately affects low-income households and marginalized communities. For renters earning minimum wage, a $200 rent hike can equate to an additional 10-15 hours of work per month, assuming they can secure extra shifts. Seniors on fixed incomes and families with children are particularly vulnerable, as they often lack the flexibility to increase earnings or downsize without significant hardship. This inequity deepens socioeconomic divides, as wealthier tenants absorb increases more easily while others face displacement.

To mitigate the affordability crisis, tenants can take proactive steps. First, negotiate with landlords by offering longer lease terms or prepayment in exchange for stable rent. Second, explore local rent control policies or tenant unions for collective bargaining power. Third, allocate 5-10% of monthly income to an emergency fund to buffer against sudden increases. Policymakers must also act by expanding housing vouchers, incentivizing affordable development, and enforcing anti-gouging laws to prevent predatory rent hikes. Without such measures, the affordability gap will continue to widen, leaving millions struggling to balance housing costs with basic needs.

Essential Experience Requirements for Renting a Small Excavator Safely

You may want to see also

Frequently asked questions

A typical security deposit is usually 1 to 2 times the monthly rent, depending on local laws and landlord policies.

The average annual rent expense is 12 times the monthly rent, as there are 12 months in a year.

Common move-in costs are typically 2 to 3 times the monthly rent, as they often include the first month’s rent and a security deposit.