Determining how much to spend on rent is a critical financial decision that depends on several factors, including your income, lifestyle, and long-term goals. A common rule of thumb is the 30% rule, which suggests allocating no more than 30% of your gross monthly income to housing costs. However, this guideline may vary based on your location, as rent prices can differ significantly between cities and regions. It’s essential to consider your overall budget, including savings, debt repayment, and other expenses, to ensure that your rent doesn’t strain your finances. Additionally, prioritizing affordability over luxury can help you maintain financial stability and avoid unnecessary stress. Ultimately, striking a balance between your housing needs and financial health is key to making a sustainable decision.

| Characteristics | Values |

|---|---|

| General Rule (50/30/20 Budget) | Spend no more than 30% of your gross monthly income on rent. |

| 3x Rent Rule | Monthly rent should not exceed 1/3 of your monthly gross income. |

| 40x Rent Rule | Annual rent should not exceed 40 times your monthly rent budget. |

| Affordability by Income | Varies; e.g., for $50,000 annual income, max rent is ~$1,250/month. |

| Location Impact | Higher in urban areas (e.g., NYC, SF); lower in rural areas. |

| Additional Costs | Include utilities, parking, and renters insurance in budget. |

| Savings Priority | Ensure rent allows for savings, emergencies, and other expenses. |

| Debt Considerations | Factor in student loans, car payments, or credit card debt. |

| Lifestyle Adjustments | Consider roommates or smaller spaces to reduce rent burden. |

| Market Trends (2023) | Average U.S. rent: ~$1,700/month (varies by city). |

| Government Guidelines | HUD recommends <30% of income for housing (U.S.). |

| Personal Circumstances | Adjust based on family size, job stability, and financial goals. |

Explore related products

What You'll Learn

- Affordable Rent Percentage: 30% of income rule for manageable housing costs

- Location Impact: Higher rents in urban areas vs. rural savings

- Budgeting Tips: Prioritize essentials, limit extras to balance rent expenses

- Roommate Benefits: Shared rent reduces individual financial burden significantly

- Long-Term Savings: Lower rent allows more savings for future goals

![]()

Affordable Rent Percentage: 30% of income rule for manageable housing costs

A widely accepted guideline for determining how much to spend on rent is the 30% rule, which suggests allocating no more than 30% of your gross monthly income to housing costs. This rule emerged as a practical benchmark to ensure that individuals and families maintain financial stability while covering essential living expenses. For example, if your monthly income is $4,000, your rent should ideally not exceed $1,200. This approach helps prevent overextension and leaves room for savings, utilities, groceries, and other necessities.

Analyzing the 30% rule reveals its strengths and limitations. On one hand, it provides a clear, actionable threshold for budgeting, making it easier to plan and avoid financial strain. On the other hand, it may not account for regional variations in living costs or individual financial obligations, such as student loans or childcare. For instance, in high-cost cities like New York or San Francisco, adhering strictly to this rule might be impractical, forcing renters to seek housing farther from city centers or consider roommates. Thus, while the 30% rule is a useful starting point, it should be adjusted based on personal circumstances and local market conditions.

To apply the 30% rule effectively, begin by calculating your gross monthly income and multiplying it by 0.30. Next, compare this figure to the average rent in your desired area. If the rent exceeds this amount, consider alternatives such as finding a less expensive neighborhood, downsizing, or splitting costs with a roommate. Additionally, factor in other housing-related expenses like utilities, internet, and maintenance, which are often not included in rent but can significantly impact your budget. Tools like rent calculators or budgeting apps can streamline this process, providing a clearer picture of affordability.

A persuasive argument for adhering to the 30% rule is its role in long-term financial health. Overspending on rent can limit your ability to save for emergencies, invest in retirement, or achieve other financial goals. For young professionals or families, staying within this threshold allows for greater flexibility in managing debt, building wealth, and adapting to unexpected expenses. Conversely, consistently exceeding this limit can lead to financial stress and instability, making it harder to recover from setbacks. By prioritizing affordability, you create a foundation for sustained economic well-being.

In conclusion, the 30% rule serves as a valuable framework for determining manageable rent expenses, but it is not one-size-fits-all. Its simplicity makes it accessible, yet its effectiveness depends on individual and regional factors. By combining this guideline with careful planning, research, and flexibility, you can make informed decisions that align with your financial goals and lifestyle. Whether you’re a first-time renter or a seasoned tenant, this rule offers a practical starting point for navigating the complexities of housing costs.

Rent Hike and Last Month's Deposit: What Are Your Options?

You may want to see also

Explore related products

![]()

Location Impact: Higher rents in urban areas vs. rural savings

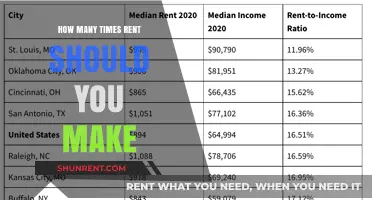

Urban areas consistently demand higher rents due to concentrated job opportunities, cultural amenities, and convenience. In cities like New York or San Francisco, renters often allocate 40–50% of their income to housing, far exceeding the recommended 30% rule. This financial strain is a trade-off for proximity to high-paying jobs, public transit, and entertainment hubs. For instance, a one-bedroom apartment in Manhattan averages $3,500 monthly, while a similar unit in a rural area like Iowa might cost $600. The urban premium reflects the economic principle of supply and demand: limited space meets high desirability.

Rural living offers significant rent savings but requires careful consideration of trade-offs. In small towns or countryside locations, rents can be 50–70% lower than urban counterparts, freeing up income for savings or other expenses. However, this often means longer commutes, fewer job opportunities, and limited access to services like healthcare or specialty stores. For example, a family saving $1,500 monthly on rent in a rural area might spend $300 extra on gas for commuting. This financial shift demands budgeting for hidden costs, such as increased transportation or home maintenance in less serviced areas.

For those weighing urban convenience against rural savings, a hybrid approach can balance costs and lifestyle. Suburban areas or smaller cities often offer rents 20–30% lower than major metros while maintaining access to jobs and amenities. For instance, moving from downtown Chicago to a nearby suburb like Naperville could reduce rent from $2,000 to $1,400 monthly. This strategy requires researching local job markets and transportation options to ensure the move doesn’t negate savings. Tools like rent-to-income calculators and cost-of-living indexes can help quantify the impact of location shifts.

Persuasively, the choice of location should align with long-term financial and personal goals. Urban living accelerates career growth and networking but strains budgets, while rural living fosters savings and simplicity but may limit opportunities. For young professionals prioritizing career advancement, higher urban rents may be a necessary investment. Conversely, families or remote workers might find rural savings more valuable for building wealth or improving quality of life. Ultimately, the decision hinges on prioritizing income potential, lifestyle preferences, and tolerance for financial risk.

Columbus North Side: Who's Renting the Vacant Thirty-One Gifts Building?

You may want to see also

Explore related products

![]()

Budgeting Tips: Prioritize essentials, limit extras to balance rent expenses

Rent often consumes a significant portion of income, leaving many to wonder how to balance housing costs with other financial obligations. A widely accepted rule of thumb is the 30% threshold: aim to spend no more than 30% of your gross monthly income on rent. For instance, if you earn $4,000 monthly, your rent should ideally stay under $1,200. However, this guideline isn’t one-size-fits-all. High-cost urban areas may require exceeding this limit, while lower-cost regions allow for more flexibility. The key is to assess your unique financial landscape before committing to a lease.

Prioritizing essentials is the cornerstone of effective budgeting. Start by listing non-negotiable expenses like groceries, utilities, transportation, and insurance. These should take precedence over discretionary spending. For example, if your monthly essentials total $1,500 and your income is $4,000, you’re left with $2,500. Subtracting the recommended $1,200 for rent leaves $1,300 for savings, debt repayment, and extras. This structured approach ensures rent doesn’t overshadow critical financial responsibilities.

Limiting extras is equally crucial to maintaining balance. Extras include dining out, entertainment, and non-essential shopping. A practical strategy is the 50/30/20 rule: allocate 50% of income to needs (including rent), 30% to wants, and 20% to savings and debt. If rent exceeds 30%, trim discretionary spending to compensate. For instance, reducing weekly restaurant visits from four to two can free up $100–$200 monthly. Small adjustments in spending habits can create significant breathing room in your budget.

Comparing housing options can also help align rent with your budget. Consider roommates to split costs, or opt for a smaller unit in a less central location. For example, a studio apartment in a suburban area might cost $900, compared to a one-bedroom downtown for $1,500. Weigh the trade-offs between convenience and affordability. Additionally, negotiate lease terms or ask for move-in specials to lower initial costs. These proactive steps ensure rent remains manageable without sacrificing financial stability.

Finally, build an emergency fund to safeguard against unexpected rent increases or income disruptions. Aim to save three to six months’ worth of living expenses, including rent. For someone spending $1,200 on rent, this translates to $7,200–$14,400. Start with small, consistent contributions, such as $100 weekly, and gradually increase as income allows. This buffer not only provides peace of mind but also ensures rent remains a sustainable expense, even in uncertain times. Balancing rent with other financial priorities requires discipline, but the payoff is long-term financial health.

Top Rental Locations Near Canary Wharf for Professionals: A Guide

You may want to see also

Explore related products

![]()

Roommate Benefits: Shared rent reduces individual financial burden significantly

Sharing rent with a roommate can dramatically lower your housing costs, often cutting your monthly expense in half or more. For instance, if a two-bedroom apartment costs $2,000 per month, splitting it with a roommate reduces your share to $1,000—a savings that can free up funds for other financial goals, such as building an emergency fund or paying off debt. This simple division of costs is one of the most straightforward ways to align your rent spending with the widely recommended 30% rule, which suggests allocating no more than 30% of your income to housing.

Consider the practical implications of this arrangement. By sharing rent, you’re not just saving on housing; you’re also splitting utility bills, internet costs, and sometimes even groceries. For example, a $150 monthly electricity bill becomes $75 per person, and a $60 internet subscription drops to $30. Over time, these shared expenses add up, creating a financial cushion that can make the difference between living paycheck to paycheck and achieving financial stability. This model is particularly beneficial for young professionals, students, or anyone in the early stages of their career when income is often limited.

However, the success of this arrangement depends on clear communication and compatibility with your roommate. Establish ground rules early, such as how bills will be divided, who’s responsible for cleaning, and how to handle late payments. For instance, using a shared spreadsheet or apps like Venmo or Splitwise can streamline expense tracking and prevent misunderstandings. Additionally, ensure both parties are committed to the financial agreement to avoid one person bearing the brunt of the costs.

From a long-term perspective, sharing rent can accelerate your financial progress. The money saved can be redirected toward investments, retirement accounts, or high-interest debt repayment. For example, if you save $600 monthly by splitting rent, investing that amount in a retirement account with a 7% annual return could grow to over $100,000 in 20 years. This highlights how a seemingly small monthly saving can compound into significant financial gains over time.

In conclusion, sharing rent with a roommate is a powerful strategy to reduce your financial burden and create room for other priorities. By halving your housing costs and splitting ancillary expenses, you can stay within budget while building a stronger financial foundation. The key lies in choosing a compatible roommate and maintaining open communication to ensure the arrangement benefits both parties equally.

Understanding Pro Rata Rent Calculation: A Step-by-Step Guide for Tenants

You may want to see also

Explore related products

![]()

Long-Term Savings: Lower rent allows more savings for future goals

Spending less on rent isn’t just about having extra cash in your pocket today—it’s a strategic move to secure your financial future. By allocating a smaller portion of your income to housing, you free up resources that can be redirected toward long-term savings goals, such as retirement, a home down payment, or an emergency fund. For instance, if you reduce your rent by $300 per month, that’s $3,600 annually—enough to make a meaningful contribution to a 401(k) or an investment account. Over decades, this compounding effect can turn modest savings into substantial wealth.

Consider the 30% rule, a common guideline suggesting that rent should not exceed 30% of your gross income. While this rule is widely cited, it’s worth questioning whether it aligns with your long-term aspirations. For someone earning $60,000 annually, 30% equates to $1,500 per month. However, if you aim to retire early or save aggressively for a child’s education, capping rent at 25% or even 20% of your income could accelerate your progress. For example, reducing rent to $1,200 monthly from $1,500 frees up $3,600 yearly—funds that could grow to over $100,000 in 30 years with a 7% annual return.

Lower rent doesn’t mean sacrificing quality of life; it’s about prioritizing what matters most. For young professionals or families, this might mean choosing a smaller apartment in a less trendy neighborhood or opting for a roommate. These trade-offs can feel temporary but yield permanent benefits. For instance, a 25-year-old who saves $200 monthly by living frugally could amass over $400,000 by age 65, assuming consistent contributions and average market returns. Such decisions require discipline but pay dividends in financial security.

Critics might argue that low rent often comes with compromises, such as longer commutes or fewer amenities. However, these trade-offs can be mitigated with thoughtful planning. For example, living farther from the city center might save $500 monthly, but if it adds $100 in transportation costs, you still net $400 in savings. Additionally, remote work opportunities increasingly allow individuals to live in lower-cost areas without sacrificing career growth. By reframing priorities, you can align your housing choices with your financial goals rather than societal expectations.

Ultimately, the decision to spend less on rent is a commitment to your future self. It requires a shift in mindset—viewing housing not as a status symbol but as a tool for financial freedom. Start by calculating your current rent-to-income ratio and identifying areas to cut back. Then, automate your savings by directing the difference into retirement accounts or investment portfolios. Over time, these small adjustments will compound into significant gains, proving that lower rent today can unlock a wealthier tomorrow.

Where Can 18-Year-Olds Rent: Top Places to Consider

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent. This helps ensure you have enough left for other expenses and savings.

While the 30% rule is a guideline, it may be necessary to exceed it in high-cost areas. However, aim to keep your total housing expenses (rent, utilities, etc.) below 50% of your income to maintain financial stability.

Balancing rent and savings is key. If spending less on rent allows you to save more or avoid debt, it’s worth considering. However, ensure your living situation meets your needs and doesn’t compromise your quality of life.