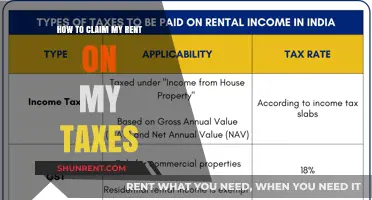

Claiming rent on taxes, specifically under the H&R Block platform, involves understanding the deductions and credits available to renters. Renters can potentially claim certain expenses related to their rental property, such as a portion of their rent if they use a part of their home for business purposes or if they are eligible for specific tax credits like the Renters’ Credit. To navigate this process, individuals should gather necessary documentation, including rental agreements and proof of payments, and utilize H&R Block’s tools or consult a tax professional to ensure accurate filing and maximize potential savings.

| Characteristics | Values |

|---|---|

| Eligibility | You must be a renter and not a homeowner. |

| Form to Use | Schedule A (Form 1040) - Itemized Deductions |

| Deduction Type | Itemized deduction, not available if you take the standard deduction |

| Qualifying Expenses | Rent payments for your primary residence or a second home used for personal purposes |

| Limitations | No specific dollar limit, but total itemized deductions must exceed the standard deduction amount for your filing status |

| Documentation Required | Rent receipts, lease agreements, or canceled checks showing rent payments |

| State Tax Considerations | Some states may allow a separate deduction or credit for rent payments; check your state's tax laws |

| IRS Publication | IRS Publication 530 (Tax Information for Homeowners) and IRS Publication 17 (Your Federal Income Tax) |

| Tax Year | 2022 and later (as of latest data) |

| Standard Deduction Amounts (2022) | - Single or Married Filing Separately: $12,950 - Married Filing Jointly or Qualifying Widow(er): $25,900 - Head of Household: $19,400 |

| Note | Rent paid for business or investment purposes may be deductible as a business expense, not as a personal itemized deduction |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand who qualifies to claim rent on taxes under H&R Block guidelines

- Documentation Needed: Gather lease agreements, payment receipts, and other essential proof for filing

- Deduction Limits: Learn maximum allowable deductions for rental expenses as per tax regulations

- Filing Process: Step-by-step guide to claim rent on taxes using H&R Block tools

- Common Mistakes: Avoid errors like incorrect categorization or missing deadlines when claiming rent

![]()

Eligibility Criteria: Understand who qualifies to claim rent on taxes under H&R Block guidelines

To claim rent on taxes under H&R Block guidelines, it’s essential to understand the eligibility criteria set by the IRS and how H&R Block interprets these rules. Generally, individuals who rent out residential or commercial property may qualify for tax deductions related to their rental activities. However, not all rental income situations are eligible. The primary requirement is that the property must be rented for profit, meaning there is an intention to generate income rather than personal use. H&R Block emphasizes that occasional rentals or properties used primarily for personal purposes may not meet this criterion. Additionally, the property must be available for rent during the tax year, even if it remains unoccupied for periods.

Another key eligibility factor is the taxpayer’s level of involvement in the rental activity. According to H&R Block, individuals who actively participate in managing their rental property—such as handling repairs, finding tenants, or collecting rent—may qualify for more deductions. Passive investors, who rely on a property manager, may still claim deductions but could face limitations under IRS passive activity rules. H&R Block advises taxpayers to document their involvement to support their claims during tax preparation.

The type of property being rented also plays a role in eligibility. Residential properties, including single-family homes, apartments, and vacation homes rented for more than 14 days per year, typically qualify. Commercial properties, such as office spaces or retail units, are also eligible. However, H&R Block notes that properties used for both personal and rental purposes require careful allocation of expenses. For example, if a vacation home is rented for part of the year, only the expenses related to the rental period can be claimed.

Taxpayers must also meet specific IRS requirements to claim rental deductions. For instance, the rental activity must be reported on Schedule E of Form 1040, and income must be declared accordingly. H&R Block highlights that individuals who rent property to family members or friends at below-market rates may face additional scrutiny. The IRS requires that such arrangements be structured as legitimate rentals to qualify for deductions.

Lastly, H&R Block stresses the importance of maintaining accurate records to establish eligibility. This includes lease agreements, rental income statements, expense receipts, and documentation of property use. Taxpayers should ensure their records clearly demonstrate that the rental activity is conducted in a businesslike manner. By meeting these eligibility criteria and following H&R Block’s guidance, taxpayers can confidently claim rent-related deductions while remaining compliant with IRS regulations.

Understanding Section 8 Rent Calculations: How Your Payment is Determined

You may want to see also

Explore related products

![]()

Documentation Needed: Gather lease agreements, payment receipts, and other essential proof for filing

When preparing to claim rent on your taxes, the first step is to gather all lease agreements related to the property. This document is crucial as it outlines the terms of the rental, including the duration of the lease, the amount of rent, and any additional clauses that may affect your tax claim. Ensure that the lease agreement is signed by both you and the tenant, as this provides legal proof of the rental arrangement. If you have multiple properties or tenants, organize each lease agreement separately to avoid confusion during the filing process.

Next, collect all payment receipts from your tenants. These receipts serve as direct evidence of the rent payments you received throughout the tax year. Acceptable forms of receipts include canceled checks, bank statements showing deposits, or digital payment confirmations from platforms like PayPal or Venmo. It’s essential to ensure that these receipts are dated and clearly indicate the amount paid, the payer’s name, and the property address. If any payments were made in cash, create a detailed receipt for each transaction and have the tenant sign it to validate the payment.

In addition to lease agreements and payment receipts, gather any other essential proof that supports your rental income and expenses. This includes property tax records, insurance documents, and receipts for maintenance or repairs. If you hired a property manager, obtain statements or invoices from them detailing their services and fees. For those who use a portion of their home as a rental property, gather documentation that clearly separates personal and rental expenses, such as utility bills with prorated amounts for the rental space.

Another critical piece of documentation is records of any security deposits held or refunded during the tax year. Keep detailed notes on how these deposits were handled, including any amounts applied to unpaid rent or damages. If you retained part of a security deposit, this amount may need to be reported as income. Conversely, if you refunded the deposit, ensure you have proof of the refund to avoid discrepancies.

Finally, organize all gathered documents in a systematic manner to streamline the filing process. Create digital or physical folders for each category of documentation, such as lease agreements, receipts, and additional proof. Label each document clearly with the tenant’s name, property address, and date range it covers. This organization not only makes it easier to file your taxes but also ensures you’re prepared in case of an audit. By meticulously gathering and organizing these documents, you’ll be well-equipped to accurately claim your rental income and deductions on your tax return.

Renting a U-Haul: License Requirements and More

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Deduction Limits: Learn maximum allowable deductions for rental expenses as per tax regulations

When claiming rental expenses on your taxes, it’s crucial to understand the deduction limits set by tax regulations to maximize your benefits while staying compliant. The IRS allows landlords to deduct ordinary and necessary expenses for managing, maintaining, and operating rental properties, but these deductions are subject to specific rules and caps. For instance, while there’s no single maximum limit for total rental expense deductions, certain expenses may be restricted based on the property’s income or usage. Understanding these limits ensures you don’t overstep boundaries and risk audits or penalties.

One key area to consider is the distinction between repairs and improvements. Repairs, such as fixing a leaky roof or replacing broken fixtures, are fully deductible in the year they are incurred. However, improvements—like adding a new room or upgrading a kitchen—must be capitalized and depreciated over time, typically 27.5 years for residential properties. This distinction is critical because improperly categorizing expenses can lead to disallowed deductions or incorrect tax reporting. Always ensure you document the nature of the expense to justify its classification.

Another important limit pertains to personal use of the rental property. If you use the property for personal purposes for more than 14 days per year or more than 10% of the total rental days, your deductions become partially limited. In such cases, you must allocate expenses between rental and personal use, deducting only the rental portion. For example, if you stay in your rental property for two weeks annually, you can only deduct expenses for the days it was rented out, prorating costs like utilities, maintenance, and property taxes accordingly.

Depreciation is another area with strict deduction limits. While you can depreciate the cost of the building (not the land) over 27.5 years, special rules apply if the property was placed in service after specific dates or if it qualifies for bonus depreciation. Additionally, the IRS requires landlords to use the Modified Accelerated Cost Recovery System (MACRS) for depreciation, which has set recovery periods and methods. Failure to adhere to these rules can result in incorrect deductions and potential adjustments during an audit.

Lastly, passive activity loss rules can limit your ability to deduct rental expenses against other income. Generally, rental activities are considered passive, and losses can only be deducted against passive income (like income from other rentals). However, there are exceptions, such as the $25,000 special allowance for active participants in rental activities with adjusted gross incomes below certain thresholds. If your income exceeds these limits, the disallowed losses carry forward to future years. Understanding these rules is essential to avoid overclaiming deductions and ensuring compliance with tax laws.

Asheville Cabin Resort Getaways: Your Private Mountain Escape

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

$114.99

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![]()

Filing Process: Step-by-step guide to claim rent on taxes using H&R Block tools

To claim rent on your taxes using H&R Block tools, start by gathering all necessary documentation. This includes your lease agreement, rent payment receipts, and any records of rental expenses if you’re a landlord. If you’re a tenant, ensure you have proof of rent payments, especially if you’re eligible for deductions under specific state or local tax laws. H&R Block’s software will guide you through the process, but having these documents ready will streamline your filing. Log into your H&R Block account or create one if you’re a new user, and select the tax filing option for the current year.

Once logged in, navigate to the income or deductions section of the H&R Block platform. If you’re a landlord, report rental income under the “Rental Income and Expenses” category. The software will prompt you to enter details such as total rent received, property-related expenses (e.g., maintenance, repairs, property taxes), and mortgage interest. For tenants, H&R Block will ask if you qualify for any rent-related deductions, such as those available in certain states or for specific professions (e.g., military personnel). Follow the on-screen instructions to input your information accurately.

After entering your rental income or expenses, H&R Block’s tools will automatically calculate your taxable rental income or applicable deductions. Review the summary page to ensure all details are correct. If you’re unsure about any step, use the platform’s built-in help feature or consult the H&R Block knowledge center for clarification. The software also offers the option to connect with a tax professional for personalized advice, which can be particularly useful for complex rental situations.

Once you’ve confirmed all details, proceed to finalize your tax return. H&R Block will guide you through the payment or refund process, depending on your tax liability. If you’re claiming deductions as a tenant, ensure the software has correctly applied them to your return. Double-check all forms, especially Schedule E (for landlords) or state-specific forms for tenants, before submitting. H&R Block’s error-checking feature will flag any potential issues, ensuring your return is accurate and complete.

Finally, submit your tax return electronically through the H&R Block platform. You’ll receive a confirmation once your return is accepted by the IRS or state tax agency. Keep a copy of your filed return and all supporting documents for your records. H&R Block’s tools make claiming rent on taxes straightforward, but staying organized and following each step carefully will ensure a smooth filing process.

Rent-a-Girlfriend: Kazuya's Final Choice

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![]()

Common Mistakes: Avoid errors like incorrect categorization or missing deadlines when claiming rent

When claiming rent on your taxes, it’s crucial to avoid common mistakes that can lead to errors, delays, or even audits. One of the most frequent errors is incorrect categorization of rental income and expenses. Many taxpayers mistakenly lump all rental-related costs under a single category, such as "repairs," when they should be itemized based on their nature. For example, routine maintenance should be separated from capital improvements, as the latter are depreciated over time rather than deducted in full immediately. Misclassifying these expenses can result in overpaying or underpaying taxes, so it’s essential to understand the IRS guidelines for rental property deductions.

Another critical mistake is missing deadlines for filing taxes or making estimated tax payments. Rental income is considered taxable, and if you’re not having taxes withheld from another source, you may need to pay quarterly estimated taxes to avoid penalties. Failing to meet these deadlines can result in fines and interest charges. Additionally, some taxpayers overlook the due dates for reporting rental income on Schedule E of Form 1040, leading to incomplete filings. Always mark your calendar for tax deadlines and consult the IRS website or a tax professional to stay on track.

A common oversight is failing to keep detailed records of rental income and expenses. Without proper documentation, it’s easy to miss deductible expenses or inaccurately report income. Keep receipts, leases, repair invoices, and other relevant documents organized throughout the year. Digital tools or spreadsheets can help track expenses, ensuring you have everything ready when it’s time to file. Inadequate record-keeping not only increases the risk of errors but also makes it difficult to defend your deductions in case of an audit.

Some taxpayers also make the mistake of claiming personal expenses as rental deductions. For instance, if you use a rental property personally for part of the year, you can only deduct expenses for the time it was rented out. Mixing personal and rental expenses, such as utilities or property taxes, can trigger IRS scrutiny. Similarly, deducting non-essential upgrades or improvements as repairs is a red flag. Always ensure that expenses are directly related to the rental activity and proportionally allocated if the property has dual use.

Lastly, overlooking depreciation is a costly error many landlords make. Depreciation allows you to recover the cost of the property over time, reducing taxable rental income. However, it’s often forgotten or miscalculated due to its complexity. The IRS has specific rules for depreciating residential rental properties, typically over 27.5 years. Failing to claim depreciation means missing out on a significant tax benefit. If you’re unsure how to calculate it, consult a tax professional to ensure accuracy and maximize your deductions.

By avoiding these common mistakes—incorrect categorization, missing deadlines, poor record-keeping, mixing personal and rental expenses, and overlooking depreciation—you can confidently claim rent on your taxes while staying compliant with IRS regulations. Taking a proactive and organized approach will not only simplify the filing process but also help you optimize your tax savings.

Rosamond Gifford Zoo: Wagon Rentals Available?

You may want to see also

Frequently asked questions

Yes, you can claim certain rent-related expenses on your taxes using H&R Block, but only if you qualify as a self-employed individual or use the property for business purposes. Personal rent payments are generally not deductible.

You’re eligible to claim rent if you use part of your rented property for business or self-employment activities. H&R Block will guide you through eligibility questions to determine if you qualify.

You’ll need rental agreements, receipts for rent payments, and proof of business use (e.g., home office calculations or business expense records) to claim rent on your taxes with H&R Block.

Yes, if you use part of your rented home exclusively for business, you can claim a portion of your rent as a home office deduction using H&R Block’s software.

H&R Block calculates the deductible rent amount based on the percentage of your home used for business. For example, if 20% of your home is used for business, 20% of your rent may be deductible.

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)