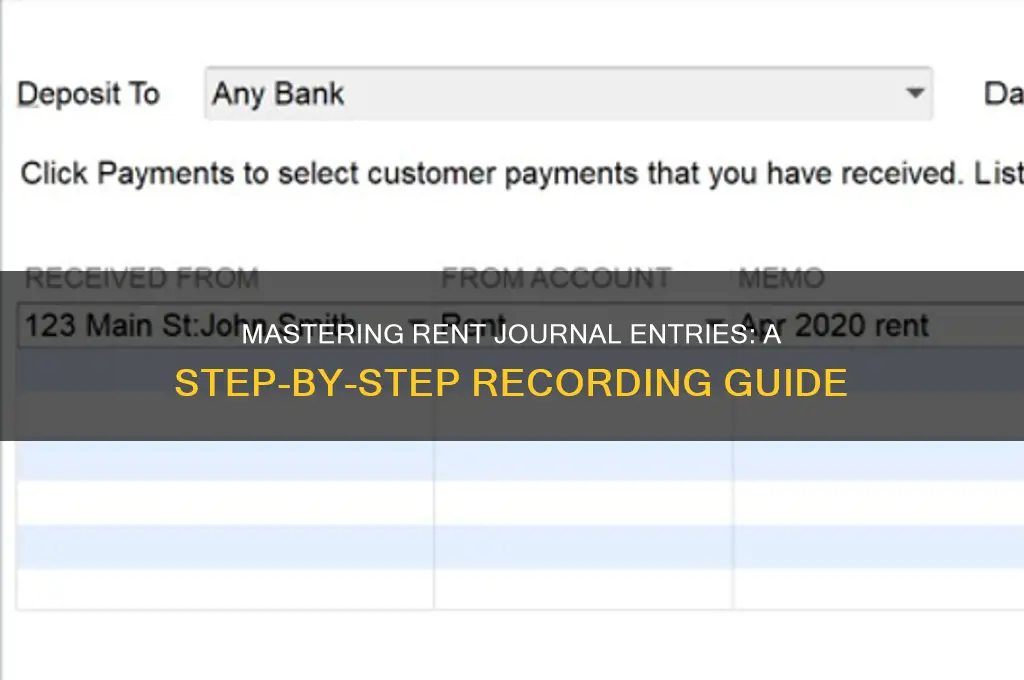

Recording a journal entry for rent is a fundamental aspect of accounting, ensuring accurate financial reporting and compliance with accounting principles. When a business pays rent for its premises, it must recognize the expense in the appropriate accounting period, typically the month in which the rent is due or paid. The journal entry involves debiting the Rent Expense account to reflect the cost incurred and crediting the Cash or Accounts Payable account, depending on whether the rent is paid immediately or deferred. For example, if a company pays $2,000 in rent for the month, the entry would debit Rent Expense for $2,000 and credit Cash for the same amount. Proper documentation, such as lease agreements and payment receipts, is essential to support the transaction and maintain transparency in financial records. Understanding this process is crucial for businesses to manage their expenses effectively and prepare accurate financial statements.

| Characteristics | Values |

|---|---|

| Account Type | Rent is typically an expense account. |

| Debit Account | Rent Expense (increases expense) |

| Credit Account | Cash, Bank Account, or Accounts Payable (decreases asset or increases liability) |

| Timing | Recorded when rent is incurred, typically at the beginning of the rental period or when paid. |

| Frequency | Monthly, quarterly, or annually, depending on the lease agreement. |

| Documentation | Lease agreement, rent invoice, or receipt. |

| Example Entry (Prepaid Rent) | Debit: Prepaid Rent (Asset), Credit: Cash |

| Example Entry (Monthly Rent Payment) | Debit: Rent Expense, Credit: Cash/Accounts Payable |

| Example Entry (Accrued Rent) | Debit: Rent Expense, Credit: Rent Payable (Liability) |

| GAAP/IFRS Compliance | Must follow matching principle, recognizing expenses in the period incurred. |

| Reversing Entry (Prepaid Rent) | Debit: Rent Expense, Credit: Prepaid Rent (at the start of the next period) |

| Tax Treatment | Rent expense is generally tax-deductible for businesses. |

| Adjusting Entry | Required for accrued rent at the end of an accounting period. |

| Journal Entry Type | Can be a simple, compound, or adjusting entry depending on the situation. |

| Supporting Documents | Lease contracts, payment receipts, or bank statements. |

Explore related products

What You'll Learn

- Identify Rent Expense Account: Determine the correct ledger account for recording rent expenses in your chart of accounts

- Debit Rent Expense: Record the rent amount as a debit to the rent expense account

- Credit Cash/Payable: Credit either cash (if paid) or accounts payable (if unpaid) for the rent amount

- Document Supporting Details: Include invoice number, payment date, and lease agreement details in the journal entry

- Post to Ledger: Transfer the journal entry to the general ledger for accurate financial reporting

![]()

Identify Rent Expense Account: Determine the correct ledger account for recording rent expenses in your chart of accounts

Recording rent expenses begins with pinpointing the correct ledger account in your chart of accounts. This foundational step ensures accuracy in financial reporting and compliance with accounting standards. The rent expense account is typically categorized under operating expenses, reflecting the day-to-day costs of running a business. For most organizations, this account is straightforwardly labeled "Rent Expense," but variations like "Occupancy Costs" or "Lease Payments" may exist depending on industry or internal conventions. Identifying the right account is crucial because misclassification can distort financial statements, leading to incorrect analysis of profitability or cash flow.

To determine the correct ledger account, start by reviewing your chart of accounts structure. Look for a section dedicated to operating expenses, where rent-related accounts are usually housed. If your chart of accounts is well-organized, the rent expense account should be clearly labeled and distinct from other expense categories like utilities or maintenance. For businesses with multiple locations or complex lease agreements, consider creating sub-accounts (e.g., "Rent Expense – Office" or "Rent Expense – Warehouse") to track expenses more granularly. This level of detail aids in budgeting, forecasting, and identifying cost drivers.

A common pitfall is confusing the rent expense account with the prepaid rent account, which is a balance sheet item representing rent paid in advance. While both accounts are related to rent, they serve different purposes. The rent expense account records the portion of rent incurred during a specific accounting period, while prepaid rent reflects the unexpired portion of rent payments. For example, if a business pays $12,000 annually in January for a year-long lease, $1,000 is expensed monthly as rent expense, while the remaining balance is recorded as prepaid rent. Understanding this distinction is vital to avoid double-counting or misstating expenses.

In practice, identifying the correct rent expense account often involves collaboration with accounting software or ERP systems. Most platforms, like QuickBooks or Xero, come pre-configured with standard charts of accounts that include a rent expense account. However, customization may be necessary to align with your business’s specific needs. For instance, a retail business might rename the account to "Store Rent Expense" for clarity. When setting up or modifying accounts, ensure consistency with accounting principles (e.g., GAAP or IFRS) and internal reporting requirements. Regularly reviewing and reconciling the rent expense account can also help catch errors early and maintain data integrity.

Finally, consider the tax implications of rent expenses when selecting the appropriate account. In many jurisdictions, rent is a deductible business expense, reducing taxable income. Properly identifying and recording rent expenses in the correct ledger account ensures compliance with tax regulations and maximizes potential deductions. For businesses with international operations or complex lease structures, consulting a tax professional can provide additional clarity. By treating the identification of the rent expense account with care, businesses can streamline their financial processes and support informed decision-making.

Is Renting in New York City Worth the High Cost?

You may want to see also

Explore related products

![]()

Debit Rent Expense: Record the rent amount as a debit to the rent expense account

Recording a journal entry for rent begins with debiting the rent expense account, a fundamental step in accrual accounting. This action acknowledges that rent is a cost incurred during the accounting period, regardless of when payment is made. For instance, if a business occupies a space from January 1 to January 31 but pays rent on February 1, the expense is still recognized in January. Debit the rent expense account for the full amount due, ensuring the financial statements accurately reflect the period’s obligations. This practice aligns with the matching principle, pairing expenses with the revenues they help generate.

The debit to the rent expense account is straightforward but requires precision. For example, if monthly rent is $2,000, debit the rent expense account for $2,000. Avoid rounding or estimating, as this can distort financial reporting. Use the exact amount stated in the lease agreement or invoice. If rent includes additional charges like utilities or maintenance, allocate these to their respective accounts separately. This ensures clarity and compliance with accounting standards, preventing misclassification errors that could skew expense analysis.

While debiting rent expense is routine, it’s crucial to consider timing and frequency. For monthly rentals, record the entry at the end of each month or when the expense is incurred. For prepaid rent, debit the rent expense account only for the portion applicable to the current period. For example, if $6,000 is paid for six months upfront, debit $1,000 to rent expense each month. This approach avoids overstating expenses in a single period and maintains consistency in financial reporting.

One common mistake is confusing the rent expense account with a prepaid rent asset account. While both are related to rent, they serve different purposes. The debit to rent expense reflects the current period’s usage, while prepaid rent represents future obligations. For instance, if $12,000 is paid annually in December for the upcoming year, debit prepaid rent for $12,000. Then, debit rent expense for $1,000 monthly, reducing the prepaid balance. This distinction ensures accurate cash flow and expense tracking.

Finally, documenting the journal entry with supporting details enhances transparency and auditability. Include the lease agreement, invoice, or payment receipt as backup. For example, if rent is $2,500 per month, the journal entry would be: *Debit Rent Expense $2,500, Credit Cash/Accounts Payable $2,500*. This clear linkage between the entry and source documents facilitates verification and reduces the risk of errors. By mastering this step, businesses ensure their financial records are both accurate and reliable.

Does Advance Auto Rent Ball Joint Press Tools? A Quick Guide

You may want to see also

Explore related products

![]()

Credit Cash/Payable: Credit either cash (if paid) or accounts payable (if unpaid) for the rent amount

Recording a journal entry for rent involves a critical decision: crediting either Cash or Accounts Payable. This choice hinges on one question: Has the rent been paid? If the rent is settled immediately, the transaction affects your cash balance. Conversely, if payment is deferred, it becomes a liability. This distinction is fundamental in maintaining accurate financial records and ensuring compliance with accounting principles.

Consider the mechanics of crediting Cash. When rent is paid upfront, the journal entry debits Rent Expense (an expense account) and credits Cash (an asset account). For instance, if monthly rent is $2,000 and paid in full, the entry would be: *Debit Rent Expense $2,000, Credit Cash $2,000*. This reduces your cash balance while recognizing the expense in the same period. It’s a straightforward transaction, ideal for businesses with immediate payment terms or those prioritizing liquidity management.

In contrast, crediting Accounts Payable applies when rent is unpaid but incurred. Here, the journal entry debits Rent Expense and credits Accounts Payable (a liability account). Using the same $2,000 rent example, the entry would be: *Debit Rent Expense $2,000, Credit Accounts Payable $2,000*. This approach acknowledges the expense while deferring the cash outflow, aligning with the accrual accounting principle of matching expenses to their respective periods. It’s particularly useful for businesses operating on credit terms or managing cash flow strategically.

The choice between crediting Cash or Accounts Payable also impacts financial statements. Crediting Cash immediately reduces liquidity on the balance sheet, while crediting Accounts Payable increases short-term liabilities. Both methods are valid, but the decision should reflect the actual payment status and the business’s accounting framework. For instance, a small business with tight cash flow might prefer deferring payments to preserve liquidity, while a larger entity might prioritize immediate settlements for simplicity.

In practice, consistency is key. Whichever method you choose, apply it uniformly across all rent transactions to avoid discrepancies. Additionally, ensure supporting documentation, such as lease agreements or payment receipts, is readily available for audit purposes. By mastering this aspect of rent journal entries, you not only maintain financial accuracy but also gain insights into your business’s cash flow and liability management.

Anaheim's Income-Based Rent: Affordable Housing Options Explained

You may want to see also

Explore related products

![]()

Document Supporting Details: Include invoice number, payment date, and lease agreement details in the journal entry

Recording a journal entry for rent requires more than just debiting an expense account and crediting cash. To ensure accuracy, compliance, and auditability, supporting details must be meticulously documented. Among these, the invoice number, payment date, and lease agreement details are non-negotiable. These elements serve as the backbone of your entry, providing traceability and context that can withstand scrutiny. Without them, your records risk being incomplete, misleading, or even non-compliant with accounting standards.

Consider the invoice number as the unique identifier for the transaction. It ties the journal entry directly to the source document, eliminating ambiguity. For instance, if you’re paying rent for multiple properties or units, the invoice number ensures each payment is allocated correctly. In QuickBooks or similar software, this number can be entered in the memo field or a dedicated reference field. For manual entries, include it in the description line of the journal entry. This small detail can save hours during reconciliations or audits, as it allows for quick verification against the original invoice.

The payment date is equally critical, as it determines the period in which the expense is recognized. Rent payments often straddle accounting periods, especially if paid in advance or arrears. For example, a December 31 payment for January rent must be recorded in the correct period to avoid misstating financial statements. The payment date also aligns with bank statements, ensuring consistency between your books and external records. In accrual accounting, this date is pivotal for matching expenses to the period in which they are incurred, rather than when they are paid.

Lease agreement details, such as the lease term, rent amount, and escalation clauses, provide the framework for your journal entry. These details ensure the recorded amount is accurate and justified. For instance, if the lease includes a $500 base rent plus a 5% annual increase, the journal entry should reflect the current agreed-upon amount, not a static figure. Additionally, referencing the lease agreement in the journal entry (e.g., "Lease Agreement #12345") creates a direct link to the contractual obligation, which is invaluable during audits or disputes.

In practice, combining these elements into a single journal entry might look like this: *"Rent expense – Office Space (Lease Agreement #12345, Invoice #45678, Payment Date: 12/31/2023) $1,500 | Cash $1,500."* This format is concise yet comprehensive, providing all necessary details for transparency and accountability. By consistently including invoice numbers, payment dates, and lease agreement references, you not only adhere to best practices but also streamline future financial analysis and reporting.

Amazon's Textbook Rental Refund Policy: What You Need to Know

You may want to see also

Explore related products

![]()

Post to Ledger: Transfer the journal entry to the general ledger for accurate financial reporting

Recording a journal entry for rent is just the first step in ensuring accurate financial reporting. The next critical phase is transferring this entry to the general ledger, a process known as posting to the ledger. This step transforms raw data into organized financial information, providing a clear snapshot of a company’s financial health. Without proper posting, even the most meticulously recorded journal entries become isolated transactions, lacking context and utility.

To post a rent journal entry to the general ledger, follow these steps: first, identify the accounts affected by the transaction, typically "Rent Expense" (debit) and "Cash" or "Accounts Payable" (credit). Next, locate these accounts in the general ledger. For each account, record the corresponding amount from the journal entry, ensuring the debit and credit totals balance. For example, if rent paid is $2,000, debit the Rent Expense account by $2,000 and credit the Cash account by the same amount. Consistency is key—use the same account names and numbering systems as established in your chart of accounts to avoid discrepancies.

A common pitfall in this process is overlooking the need for precision. Small errors, such as posting to the wrong account or transposing numbers, can lead to significant financial misstatements. To mitigate this, double-check each entry against the original journal entry and ensure the ledger balances after posting. Additionally, consider using accounting software that automates this process, reducing the risk of human error. For instance, QuickBooks and Xero offer features that sync journal entries directly to the general ledger, streamlining the workflow.

The importance of posting to the ledger cannot be overstated, especially in the context of rent transactions. Rent is often a substantial expense for businesses, and its accurate reflection in the ledger is vital for budgeting, tax reporting, and financial analysis. For example, a retail business paying $5,000 monthly in rent needs this expense to be correctly recorded to assess profitability and cash flow. Failure to post this entry accurately could lead to overstated profits or underestimated expenses, distorting financial decision-making.

In conclusion, posting journal entries to the general ledger is a foundational practice in accounting that bridges the gap between raw data and actionable financial insights. By systematically transferring rent transactions to the ledger, businesses ensure their financial records are complete, accurate, and reliable. This process, though seemingly routine, is a cornerstone of effective financial management, enabling stakeholders to make informed decisions based on a clear and accurate financial picture.

San Francisco Rent Trends: Rising or Falling in 2023?

You may want to see also

Frequently asked questions

The basic journal entry for recording rent expense is to debit Rent Expense (an expense account) and credit Cash or Accounts Payable, depending on whether the rent is paid immediately or owed.

To record prepaid rent, debit Prepaid Rent (an asset account) and credit Cash or Accounts Payable. This reflects the payment made in advance for future rent periods.

Debit Prepaid Rent for the full amount paid and credit Cash or Accounts Payable. Then, each month, debit Rent Expense and credit Prepaid Rent for the portion of rent applicable to that period.

If rent is paid after the rental period, debit Rent Expense and credit Accounts Payable when the obligation is incurred. When payment is made, debit Accounts Payable and credit Cash.

The security deposit is recorded separately. Debit Security Deposit (an asset account) and credit Cash. Rent payments are recorded as usual, debiting Rent Expense and crediting Cash or Accounts Payable.