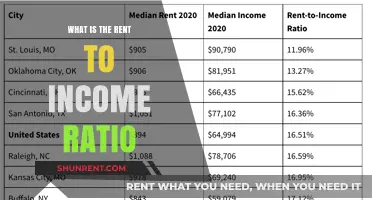

The question of whether 3x the rent refers to gross or net income is a common point of confusion for both landlords and tenants. This metric is often used as a rule of thumb to assess a tenant's ability to afford rent, but its interpretation can vary depending on the context. Gross income typically includes all earnings before deductions, such as taxes and other withholdings, while net income reflects the amount a tenant actually takes home after these deductions. Clarifying whether 3x the rent is based on gross or net income is crucial, as it directly impacts affordability assessments and rental approval processes, ensuring both parties have a clear understanding of financial expectations.

Explore related products

What You'll Learn

- Gross Rent Definition: Includes all income before expenses, encompassing base rent and additional charges

- Net Rent Explained: Rent after deducting expenses like maintenance, taxes, and utilities

- x Rent Rule: Landlords often require tenants' income to be three times the gross rent

- Gross vs. Net Impact: Using gross rent increases tenant qualification chances compared to net rent

- Income Calculation: Whether to use pre-tax (gross) or post-tax (net) income for the 3x rule

![]()

Gross Rent Definition: Includes all income before expenses, encompassing base rent and additional charges

Gross rent is a term that often sparks confusion, especially when tenants and landlords discuss affordability. At its core, gross rent includes all income a landlord receives before any expenses are deducted. This means it’s not just the base rent but also encompasses additional charges like utilities, parking fees, or maintenance costs rolled into the monthly payment. For instance, if a tenant pays $1,500 monthly, including $100 for water and $50 for parking, the gross rent is $1,500, not the $1,350 base rent. This distinction is critical when evaluating affordability ratios like the "3x rent rule," which typically refers to gross rent, not net.

To apply this concept practically, consider a tenant earning $4,500 monthly. If the 3x rent rule is based on gross rent, their maximum affordable rent would be $1,500, inclusive of all additional charges. This calculation ensures the tenant’s housing costs don’t exceed 33% of their income, a common affordability benchmark. However, if the rule were misinterpreted as net rent, the tenant might mistakenly believe they could afford $1,350 in base rent plus additional fees, potentially overshooting their budget. Clarity on gross rent prevents such miscalculations.

From a landlord’s perspective, understanding gross rent is equally vital for financial planning. It represents the total revenue stream from a property, which can then be used to cover expenses like mortgage payments, property taxes, and repairs. For example, a landlord collecting $2,000 in gross rent might allocate $1,200 to the mortgage, $300 to maintenance, and retain $500 as profit. This breakdown highlights why gross rent is a more comprehensive metric than net rent, which only reflects income after expenses.

A comparative analysis further underscores the importance of gross rent. While net rent might seem more appealing to tenants because it appears lower, it doesn’t provide a full picture of housing costs. Gross rent, on the other hand, offers transparency and aligns with affordability standards used by lenders and housing authorities. For instance, when a tenant applies for a rental, landlords often require proof of income at least three times the gross rent, not the net. This practice ensures tenants can comfortably cover all housing-related expenses.

In conclusion, gross rent is a foundational concept for both tenants and landlords, serving as the basis for affordability calculations and financial planning. By including all income before expenses, it provides a clear, holistic view of rental costs. Whether you’re a tenant budgeting for housing or a landlord managing property finances, understanding gross rent ensures informed decision-making and avoids costly misunderstandings. Always verify whether affordability ratios like the 3x rent rule refer to gross or net rent to stay on solid financial ground.

Smart Strategies to Cut Costs on Renting Office Space

You may want to see also

Explore related products

![]()

Net Rent Explained: Rent after deducting expenses like maintenance, taxes, and utilities

Net rent is the amount a tenant actually pays after subtracting specific expenses from the gross rent. This concept is crucial for both landlords and tenants to understand, as it directly impacts cash flow and budgeting. For instance, if a tenant is told the rent is $1,500 per month, they need to clarify whether this is gross rent (the total before deductions) or net rent (the final amount after expenses). Misunderstanding this distinction can lead to unexpected financial burdens.

Consider a commercial lease where the landlord charges $3,000 per month as gross rent. However, the lease agreement stipulates that the tenant is responsible for property taxes, insurance, and common area maintenance (CAM) fees. If these expenses total $800 monthly, the net rent the tenant pays is $2,200. This example highlights why tenants must scrutinize lease terms to determine which expenses are included in the quoted rent and which are their responsibility.

For residential leases, net rent is less common but still relevant in certain scenarios. For example, some landlords may include utilities like water or electricity in the rent but deduct a fixed amount for maintenance or administrative fees. A tenant renting an apartment for $1,200 per month might see a $50 deduction for maintenance, resulting in a net rent of $1,150. Understanding these deductions ensures tenants can accurately assess affordability and avoid surprises.

To navigate net rent effectively, tenants should follow these steps: First, request a detailed breakdown of all expenses included in the gross rent. Second, clarify which costs are deductible and whether they are fixed or variable. Third, calculate the net rent by subtracting these expenses from the gross amount. Finally, compare the net rent to their budget to ensure it aligns with their financial capabilities. This proactive approach empowers tenants to make informed decisions and avoid overcommitting financially.

In the context of "is 3x the rent gross or net," understanding net rent becomes even more critical. If a landlord or lender requires tenants to earn three times the rent, knowing whether this refers to gross or net rent significantly impacts eligibility. For example, if the gross rent is $2,000 but the net rent is $1,800 after deductions, a tenant earning $5,400 monthly would meet the 3x gross requirement but not the 3x net requirement. This distinction underscores the importance of clarity in financial agreements.

Rent 'Hitman's Wife's Bodyguard' Now: Top Streaming & Rental Options

You may want to see also

Explore related products

![]()

3x Rent Rule: Landlords often require tenants' income to be three times the gross rent

The 3x rent rule is a widely adopted benchmark in the rental market, where landlords typically require a tenant’s monthly income to be at least three times the gross rent. This standard serves as a quick financial viability check, ensuring tenants can afford rent while covering other living expenses. For example, if a studio apartment rents for $1,500 per month, a tenant would need to demonstrate a monthly income of at least $4,500 to meet this requirement. The rule is straightforward, but its application varies depending on whether "income" is interpreted as gross or net, which can significantly impact a tenant’s eligibility.

Analyzing the rule’s practicality reveals its strengths and limitations. Landlords favor the 3x gross rent metric because it simplifies the screening process and minimizes risk of non-payment. Gross income, being pre-tax and pre-deduction, provides a clearer picture of a tenant’s earning potential. However, this approach may unfairly exclude individuals with high fixed expenses, such as student loans or childcare costs, whose net income is substantially lower. For instance, a tenant earning $6,000 gross monthly but with $2,000 in deductions might struggle to meet the rule for a $2,000 rental, despite having sufficient net income for affordability.

To navigate this rule effectively, tenants should proactively clarify with landlords whether gross or net income is being assessed. If gross income is the criterion, tenants can strengthen their applications by providing additional financial documentation, such as savings accounts or secondary income sources, to demonstrate stability. Conversely, if net income is considered, tenants should be prepared to share detailed expense breakdowns to show how they manage their finances. For example, a tenant with a high gross income but significant deductions could highlight consistent savings or low debt-to-income ratios to reassure landlords.

Comparing the 3x rule to other affordability metrics underscores its simplicity but also its rigidity. Alternative methods, such as the 50/30/20 budget rule (50% of income on needs, 30% on wants, 20% on savings), offer a more holistic view of financial health but are time-consuming to assess. The 3x rule, while less nuanced, remains a practical tool for landlords managing multiple applications. Tenants in competitive markets may need to exceed this threshold or offer larger security deposits to stand out, especially in high-cost urban areas where rents consume a larger portion of income.

In conclusion, the 3x rent rule is a double-edged sword—efficient for landlords but potentially restrictive for tenants. Understanding whether the rule applies to gross or net income is crucial for both parties. Tenants should prepare accordingly by organizing financial records and being ready to negotiate, while landlords might consider flexibility in high-demand markets to avoid vacancies. Ultimately, the rule’s effectiveness lies in its clarity and widespread acceptance, but its fairness depends on how it’s applied and interpreted.

Rent AWD Cargo Vans in LA: Top Locations & Tips

You may want to see also

Explore related products

![]()

Gross vs. Net Impact: Using gross rent increases tenant qualification chances compared to net rent

The debate over whether the 3x rent rule applies to gross or net income significantly impacts tenant qualification. Landlords who use gross income as the benchmark inherently widen their pool of eligible renters. Gross income, before deductions like taxes and insurance, typically appears higher than net income. For instance, a tenant earning $6,000 monthly gross might only take home $4,500 net. By applying the 3x rule to gross income, a $2,000 rent becomes feasible, whereas net income would disqualify them. This approach benefits landlords by reducing vacancy rates and tenants by increasing their housing options.

Consider the practical implications for a landlord screening applicants. A tenant with a gross income of $75,000 annually but a net income of $55,000 might struggle to meet a 3x net requirement for a $1,800 rent. However, using gross income, their $75,000 qualifies them for up to $2,500 monthly rent. This flexibility not only secures a tenant faster but also minimizes the risk of losing qualified individuals due to arbitrary income thresholds. For landlords, this means fewer days on the market and a broader selection of financially stable tenants.

From a tenant’s perspective, understanding this distinction can be a game-changer. If a landlord uses gross income, tenants can strategically highlight their pre-tax earnings to meet qualification criteria. For example, a freelancer with irregular income might present their gross earnings, including untaxed amounts, to satisfy the 3x rule. Conversely, if a landlord insists on net income, tenants must meticulously document deductions to prove their eligibility. This knowledge empowers tenants to navigate rental applications more effectively, increasing their chances of approval.

However, landlords must exercise caution when opting for gross income calculations. While it expands the tenant pool, it may introduce higher financial risk if tenants struggle with post-deduction affordability. To mitigate this, landlords can implement additional screening measures, such as requiring proof of consistent income or requesting a higher security deposit. Balancing flexibility with financial security ensures that the gross income approach remains a win-win for both parties.

In conclusion, using gross income in the 3x rent rule enhances tenant qualification chances while offering landlords a larger, more diverse applicant pool. This method simplifies the screening process and reduces vacancy periods, benefiting both parties. Tenants, armed with this knowledge, can better position themselves during applications, while landlords can refine their screening practices to maintain financial stability. Ultimately, the choice between gross and net income hinges on striking the right balance between accessibility and risk management.

RV Rentals: Can You Use RCI Points?

You may want to see also

Explore related products

![]()

Income Calculation: Whether to use pre-tax (gross) or post-tax (net) income for the 3x rule

The 3x rent rule is a widely used benchmark for determining affordability, but its application hinges on a critical distinction: whether to use gross or net income. Gross income, the total earnings before deductions, provides a broader picture of financial capacity. Net income, however, reflects the actual take-home pay after taxes and other withholdings, offering a more realistic view of disposable income. This distinction is not merely semantic; it directly impacts the accuracy of the 3x rule in assessing rental affordability.

Consider a hypothetical scenario: a tenant earns $60,000 annually. Using the gross income, the 3x rule suggests they can afford rent up to $1,500 per month ($60,000 / 12 / 3). However, if their net income after taxes and deductions is $45,000, the calculation drops to $1,125 per month ($45,000 / 12 / 3). This $375 difference highlights the potential for overestimation when using gross income, which could lead to financial strain for the tenant. Landlords and tenants alike must weigh the practicality of each approach, considering factors like tax bracket, deductions, and regional tax rates.

From a persuasive standpoint, using net income aligns better with the principle of financial responsibility. Rent is paid with take-home pay, not pre-tax earnings. A tenant’s ability to meet other financial obligations—utilities, groceries, savings—is equally important. By focusing on net income, the 3x rule becomes a more reliable tool for ensuring long-term affordability rather than a superficial metric that ignores real-world financial constraints. This approach also reduces the risk of eviction or late payments, benefiting both parties in the rental agreement.

For those seeking a practical middle ground, a comparative analysis suggests a hybrid approach. Start with gross income to gauge overall earning potential, then adjust downward based on estimated tax deductions and other mandatory withholdings. For instance, if a tenant’s gross income is $72,000, but they anticipate $20,000 in deductions, use an adjusted gross income of $52,000 for the calculation. This method balances optimism with realism, providing a more nuanced assessment of affordability. Tools like tax calculators or financial advisors can aid in refining these estimates.

In conclusion, the choice between gross and net income for the 3x rule depends on the desired level of precision and the specific financial context. While gross income offers a broader view, net income ensures a more accurate reflection of disposable funds. Tenants should advocate for net income calculations to avoid overextension, while landlords might consider gross income as a starting point, tempered by an understanding of typical deductions. Ultimately, transparency and flexibility in income assessment foster fairer, more sustainable rental agreements.

Top Winnipeg Spots for Renting Cross-Country Skis This Winter

You may want to see also

Frequently asked questions

Typically, the 3x rent rule is based on gross income, which is your total earnings before taxes and deductions.

Most landlords and property managers use monthly gross income when applying the 3x rent rule to assess affordability.

No, the 3x rent rule is generally applied to gross income, not net income, regardless of deductions or expenses.