The classification of rent received as either income or expense depends on the perspective of the party involved in the transaction. For the landlord or property owner, rent received is considered income because it represents revenue generated from leasing out their property. This income is typically reported on financial statements and is subject to taxation. Conversely, for the tenant or lessee, rent paid is classified as an expense since it represents a cost incurred for the use of the property. Understanding this distinction is crucial for accurate financial reporting and tax compliance, as it directly impacts the financial health and obligations of both parties.

| Characteristics | Values |

|---|---|

| Nature of Rent Received | Income |

| Accounting Classification | Revenue or Income |

| Impact on Financial Statements | Increases profit or surplus |

| Tax Treatment | Taxable income (subject to local tax laws) |

| Cash Flow Effect | Positive cash inflow |

| Recording in Books | Credited to income account (e.g., Rental Income) |

| Frequency | Periodic (e.g., monthly, quarterly) |

| Source | Tenants or lessees |

| Purpose | Compensation for use of property |

| Expense Counterpart | Rent paid is an expense for the tenant |

| Reporting | Reported in the income statement under operating income or other income |

| Economic Impact | Contributes to the owner's earnings |

| Legal Obligation | No legal obligation to pay (received by owner) |

| Adjustments | May be subject to deductions (e.g., property maintenance costs) |

| Example | A landlord receives $1,000 monthly rent, recorded as income. |

Explore related products

What You'll Learn

- Rent as Revenue: Classifying rent received as income in financial statements

- Expense vs. Income: Differentiating rent received from rent paid as expenses

- Tax Treatment: How rent income is taxed for individuals and businesses

- Accounting Principles: Recording rent received under GAAP or IFRS standards

- Cash Flow Impact: Rent received as a source of operating cash inflow

![]()

Rent as Revenue: Classifying rent received as income in financial statements

Rent received is unequivocally classified as income in financial statements, but its precise categorization depends on the entity’s role in the transaction. For landlords or property owners, rent is a primary revenue stream, reported under "Rental Income" in the income statement. This classification aligns with accounting principles like GAAP and IFRS, which define revenue as inflows from ordinary business activities. For example, a real estate company leasing commercial spaces would record monthly rent payments as operating revenue, directly impacting profitability metrics like net income.

However, the timing of rent recognition is critical. Under the accrual accounting method, rent is recorded when earned, not when received. For instance, if a tenant pays $12,000 annually in December for the entire year, the landlord recognizes $1,000 monthly as revenue. This ensures financial statements reflect the economic reality of the rental period. In contrast, cash accounting records rent only upon receipt, which is simpler but less accurate for long-term leases.

Tenants, on the other hand, treat rent as an expense, not income. For businesses leasing property, rent is recorded as "Rental Expense" in the income statement, reducing taxable income. This duality—income for the landlord, expense for the tenant—highlights the reciprocal nature of rent transactions. For example, a retail store leasing a storefront would deduct monthly rent payments from its revenue, directly affecting its operating profit.

Practical tips for accurate classification include maintaining clear lease agreements to determine rent periods and using accounting software to automate accrual adjustments. For landlords, segregating rental income from other revenue streams enhances financial transparency. Tenants should reconcile rent payments with lease terms to avoid overpayment or underpayment. Proper classification not only ensures compliance with accounting standards but also provides stakeholders with a clear view of financial health and operational efficiency.

In summary, rent received is income for the property owner, but its recognition and reporting require adherence to specific accounting principles. Whether accrual or cash-based, consistency in classification is key. For landlords, it’s a vital revenue source; for tenants, a necessary expense. Understanding this distinction ensures financial statements accurately reflect the economic substance of rental transactions.

Using ITIN for Renter Screening: Legal, Effective, or Risky?

You may want to see also

Explore related products

![]()

Expense vs. Income: Differentiating rent received from rent paid as expenses

Rent received and rent paid are two sides of the same coin, yet they are classified differently in financial accounting. For a landlord, rent received is a revenue stream, representing the income generated from leasing property. This inflow of cash is recorded as income on the profit and loss statement, contributing to the overall profitability of the business. For instance, if a landlord receives $1,200 monthly from a tenant, this amount is categorized as rental income, subject to taxation and reported as earnings.

Conversely, for a tenant, rent paid is an operating expense, a necessary outflow to secure a place of residence or business. This expense is deducted from the tenant’s income, reducing taxable earnings. For example, a small business paying $1,500 monthly for office space would record this as a business expense, lowering its taxable profit. The same transaction—rent—is thus income for one party and an expense for the other, highlighting the dual nature of this financial exchange.

To differentiate the two, consider the perspective of the transacting parties. From the landlord’s viewpoint, rent received is a core business income, often the primary revenue source for property owners. From the tenant’s viewpoint, rent paid is a cost of doing business or living, akin to utilities or supplies. This distinction is critical for accurate financial reporting and tax compliance, as misclassifying rent can lead to errors in profit calculation and tax liabilities.

Practical record-keeping tips can help clarify this distinction. Landlords should maintain separate accounts for rental income and property-related expenses (e.g., maintenance, mortgage interest). Tenants, especially businesses, should track rent payments as part of their operating expenses, ensuring they are deducted appropriately on tax returns. For individuals, rent paid is typically not tax-deductible unless it’s for a home office or other qualified purpose, underscoring the importance of understanding these classifications.

In summary, while rent is a single transaction, its classification as income or expense depends entirely on the role of the party involved. Landlords treat it as income, tenants as an expense, and this differentiation is fundamental for financial accuracy and compliance. By understanding this dynamic, both parties can manage their finances more effectively, ensuring proper reporting and maximizing tax benefits where applicable.

Rent the Splash Derryl Hanna Mermaid Tail: Top Locations Guide

You may want to see also

Explore related products

![]()

Tax Treatment: How rent income is taxed for individuals and businesses

Rent received is unequivocally classified as income, not an expense, for both individuals and businesses. This fundamental distinction is critical for tax purposes, as it determines how the funds are reported, taxed, and utilized. For individuals, rental income typically falls under the category of passive income, while for businesses, it is often considered part of operational revenue. However, the tax treatment of this income varies significantly depending on the taxpayer’s status, location, and specific circumstances.

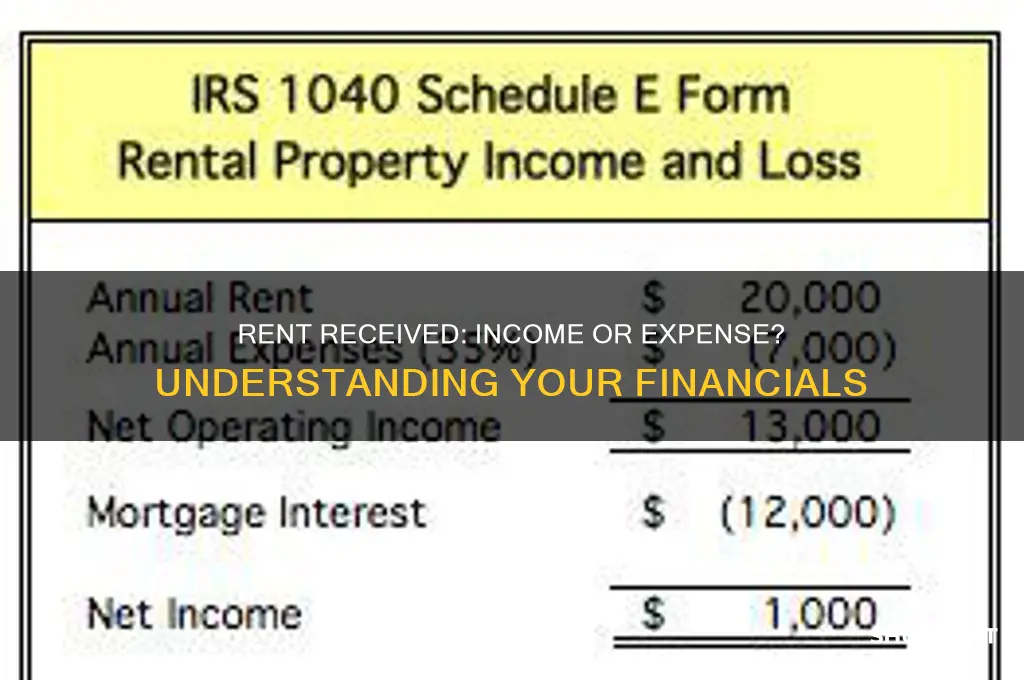

For individuals, rental income is generally taxed as ordinary income, subject to federal and state income tax rates. The IRS requires landlords to report rental income on Schedule E of Form 1040, where expenses directly related to the rental property—such as maintenance, property management fees, and mortgage interest—can be deducted. These deductions reduce the taxable rental income, potentially lowering the overall tax liability. For example, if a landlord earns $20,000 in rent annually and incurs $8,000 in deductible expenses, only $12,000 is subject to taxation. It’s crucial to maintain detailed records of all income and expenses to ensure compliance and maximize deductions.

Businesses, on the other hand, treat rental income as part of their gross revenue, which is reported on their tax returns (e.g., Form 1120 for corporations or Schedule C for sole proprietorships). Unlike individuals, businesses may also be eligible for additional deductions, such as depreciation of the rental property, which allows them to recover the cost of the asset over time. For instance, a commercial property owner can depreciate the building (not the land) over 39 years using the straight-line method, reducing taxable income annually. However, businesses must also consider self-employment taxes if the rental activity is part of a trade or business, adding another layer of complexity.

One critical distinction in tax treatment arises from how the rental activity is classified. If an individual’s rental activity is considered a passive activity, losses from the property may be limited in their ability to offset other income. However, real estate professionals—those who spend more than 750 hours per year in real estate activities—may be exempt from these restrictions. For businesses, the classification of rental income as active or passive depends on the nature of the business and the taxpayer’s involvement in the rental activity.

In conclusion, while rent received is clearly income, its tax treatment differs markedly between individuals and businesses. Individuals benefit from straightforward deductions but face limitations on passive losses, while businesses enjoy additional deductions like depreciation but must navigate self-employment taxes and activity classifications. Understanding these nuances is essential for accurate reporting and optimizing tax outcomes. Always consult a tax professional to tailor strategies to your specific situation.

Top Grease Trap Rental Options in Las Vegas: Your Ultimate Guide

You may want to see also

Explore related products

![]()

Accounting Principles: Recording rent received under GAAP or IFRS standards

Rent received is unequivocally classified as income under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). However, the specific treatment and recognition of this income depend on the nature of the lease agreement and the accounting framework applied. For entities operating under GAAP, ASC 842 (Leases) provides the guidelines, while IFRS users refer to IFRS 16. Both standards emphasize the importance of recognizing income systematically over the lease term, reflecting the economic substance of the transaction.

Under GAAP, rent received from operating leases is recognized as revenue on a straight-line basis over the lease term, regardless of whether payments are received evenly. For example, if a tenant pays $1,200 monthly for 12 months but the lease agreement stipulates a total payment of $15,000, the landlord records $1,250 ($15,000 / 12) as income each month. This approach smooths out fluctuations in cash receipts and aligns with the matching principle. IFRS 16 adopts a similar stance, requiring lessors to recognize lease income systematically, though it distinguishes between operating and finance leases, with the latter treated as a receivable generating interest income.

A critical distinction arises in the treatment of lease incentives. Under GAAP, lease incentives (e.g., rent-free periods or tenant improvements) are amortized over the lease term, reducing rental income proportionally. IFRS 16, however, allows lessors to allocate incentives as a reduction in the lease receivable, impacting the interest income generated. For instance, a $10,000 incentive under a 10-year lease would reduce annual rental income by $1,000 under GAAP, whereas IFRS 16 would adjust the lease receivable, affecting the interest calculation.

Practical application requires meticulous documentation of lease terms, including payment schedules, incentives, and lease classification. Entities must also consider the impact of variable lease payments, which are recognized as income when the variability is resolved. For example, a lease with rent tied to a percentage of sales would record income only when the sales figures are finalized. Both frameworks demand transparency, with disclosures detailing lease portfolios, income recognition policies, and any remeasurements of lease receivables.

In conclusion, while rent received is universally treated as income, the nuances of GAAP and IFRS standards dictate specific recognition and measurement practices. Entities must navigate these requirements carefully, ensuring compliance while accurately reflecting the economic reality of lease transactions. Regular reviews of lease agreements and accounting treatments are essential to avoid misstatements and maintain financial integrity.

Connect to Your Nitrado Xbox One Rented Server: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Cash Flow Impact: Rent received as a source of operating cash inflow

Rent received is unequivocally classified as income, specifically operating income, for entities that own and lease property. This classification stems from the fact that rent is a primary revenue stream generated from the core business activity of property management or ownership. When analyzing cash flow, understanding the role of rent as an operating cash inflow is critical for assessing financial health and liquidity.

Consider a commercial real estate company with 10 properties, each generating $5,000 in monthly rent. Annually, this equates to $600,000 in operating cash inflow from rent alone. This predictable, recurring revenue stream directly enhances the company’s ability to meet short-term obligations, reinvest in property maintenance, or expand its portfolio. Unlike non-operating income (e.g., interest or dividends), rent is tied to the entity’s primary operations, making it a cornerstone of cash flow stability.

However, the impact of rent on cash flow isn’t static. For instance, a 10% vacancy rate in the aforementioned portfolio would reduce annual rent inflows by $60,000, highlighting the importance of occupancy rates in maintaining cash flow. Additionally, rent escalations or lease renewals can increase inflows, while tenant defaults or market downturns pose risks. Thus, prudent cash flow management requires monitoring these variables to ensure rent remains a reliable operating cash source.

To maximize the cash flow impact of rent received, property owners should implement strategies such as offering incentives for long-term leases, maintaining competitive rental rates, and diversifying property types to mitigate vacancy risks. For example, a landlord might offer a 5% discount for a 3-year lease, securing consistent cash inflow while reducing turnover costs. Conversely, failing to address maintenance issues could lead to tenant churn, disrupting this critical cash flow source.

In conclusion, rent received is not merely income—it is a vital operating cash inflow that underpins financial stability for property owners. By understanding its dynamics and implementing proactive management strategies, entities can optimize this cash flow source, ensuring resilience in the face of market fluctuations and operational challenges.

Strategic Timing: When and How to Adjust Rental Rates Fairly

You may want to see also

Frequently asked questions

Rent received is considered an income because it represents money earned from leasing property to a tenant.

Rent received is classified as income because it increases the recipient’s financial resources, whereas expenses reduce them.

No, rent received is always treated as income for the landlord or property owner. However, the expenses associated with maintaining the property (e.g., repairs, taxes) are separate and classified as expenses.

Rent received is reported as revenue or income on the income statement, contributing to the total earnings of the property owner.

Yes, rent received is typically taxable income and must be reported on tax returns, subject to applicable deductions for related expenses.