The question of whether rent received from parents is considered taxable income is a common concern for many individuals, particularly those who own property and reside with their parents or have parents living in their property. In most jurisdictions, rental income is generally taxable, but the specifics can vary depending on the relationship between the landlord and tenant, as well as the terms of the rental agreement. When parents pay rent to their children, it may be viewed differently by tax authorities compared to traditional landlord-tenant relationships, potentially raising questions about the nature of the transaction and its tax implications. Understanding the rules and regulations surrounding this issue is crucial for accurately reporting income and avoiding potential penalties or audits.

| Characteristics | Values |

|---|---|

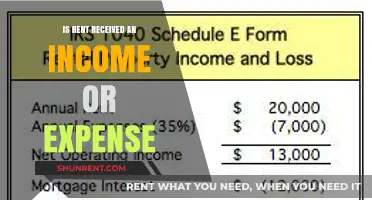

| Taxability of Rent from Parents | Generally taxable as rental income |

| Reporting Requirement | Must be reported on tax return (e.g., IRS Form 1040, Schedule E in the U.S.) |

| Fair Market Rent Rule | If rent is below fair market value, the IRS may impute fair market rent as taxable income |

| Gift Tax Consideration | If rent is significantly below market value, it may be considered a gift, subject to gift tax rules |

| Expenses Deduction | Eligible for deductions related to rental property (e.g., maintenance, mortgage interest, property taxes) |

| Depreciation | Can claim depreciation on the property if used as a rental |

| State Tax Rules | Varies by state; some states may have specific rules or exemptions |

| International Tax Implications | May be subject to tax in the recipient's country of residence, depending on tax treaties |

| Documentation Required | Lease agreement, rent receipts, and records of expenses are recommended |

| Audit Risk | Higher risk if rent is significantly below market value or not reported properly |

| Professional Advice | Consultation with a tax professional is advised for complex situations |

Explore related products

What You'll Learn

![]()

Rent from Parents: Gift or Income?

In the eyes of tax authorities, the line between a gift and taxable income can be razor-thin, especially when it involves transactions between family members. Consider this scenario: an adult child receives monthly rent from their parents for living in a property owned by the child. Is this rent a gift, a gesture of familial support, or does it qualify as taxable income? The answer hinges on the intent behind the payment and the structure of the arrangement. If the parents are paying fair market rent and the child is treating the property as a rental business—maintaining records, reporting expenses, and filing taxes accordingly—the IRS and similar bodies typically classify this as taxable income. However, if the payments are sporadic, below market value, or framed as a gift without formal documentation, the classification becomes murkier.

From a legal standpoint, the key to determining whether rent from parents is taxable lies in the arm’s length principle. This principle asks whether the transaction resembles one that would occur between unrelated parties. For instance, if a parent pays $1,000 monthly for a property that would rent for $1,500 on the open market, the arrangement may not meet this standard. Tax authorities often scrutinize such cases, particularly if the child claims deductions for rental expenses while treating the income as a gift. To avoid complications, it’s advisable to formalize the agreement with a written lease, set market-rate rent, and maintain consistent records of payments and expenses.

Persuasively, treating rent from parents as taxable income has long-term benefits, both financially and relationally. By reporting the income, the child establishes a clear separation between personal and business finances, which can protect familial relationships from misunderstandings. Additionally, declaring the income allows the child to claim legitimate deductions, such as mortgage interest, property taxes, and maintenance costs, potentially reducing their overall tax liability. Conversely, failing to report the income could result in penalties, audits, or strained family dynamics if the arrangement is questioned by tax authorities.

Comparatively, the treatment of rent from parents varies across jurisdictions. In the U.S., the IRS requires income from rental properties to be reported, regardless of the relationship between landlord and tenant. In contrast, some countries may offer exemptions or allowances for familial transactions, provided they meet specific criteria. For example, in the UK, rent from family members may be taxed under the “rent-a-room” scheme if the annual income is below a certain threshold. Understanding local tax laws is crucial, as misclassification can lead to unintended consequences.

Practically, here’s a step-by-step guide to navigating this issue: First, draft a formal lease agreement outlining rent, payment terms, and responsibilities. Second, ensure the rent aligns with local market rates—use online tools or consult real estate agents for accurate pricing. Third, maintain meticulous records of all transactions, including receipts for expenses and proof of payments. Fourth, consult a tax professional to determine the best way to report the income and claim deductions. Finally, communicate openly with family members about the arrangement’s financial implications to avoid misunderstandings. By taking these steps, you can ensure compliance while preserving the integrity of familial relationships.

Renting a U-Haul Online: A Step-by-Step Guide for Beginners

You may want to see also

Explore related products

![]()

Tax Rules for Family Rentals

Rent received from family members, including parents, is taxable income under most tax laws, but the rules can vary significantly depending on the jurisdiction and the specifics of the arrangement. In the United States, for instance, the IRS treats rental income from family members the same as income from unrelated tenants, provided the arrangement is structured as a legitimate rental agreement. This means that if you’re renting a property to your parents, the rent you receive must be reported on your tax return, typically on Schedule E of Form 1040. However, the IRS scrutinizes such arrangements to ensure they aren’t a disguised gift or support payment, which would have different tax implications.

To ensure compliance, the rental agreement between family members should mirror those used in arm’s-length transactions. This includes a written lease agreement outlining the terms of the tenancy, such as rent amount, due dates, and responsibilities for maintenance. The rent charged should also be at fair market value, not a discounted rate, as this could raise red flags with tax authorities. For example, if the market rent for a similar property in your area is $1,200 per month, charging your parents $500 could be seen as a gift rather than legitimate rent, potentially disqualifying it from being treated as rental income.

One critical aspect often overlooked is the impact of family rentals on deductions and depreciation. If the property is considered a rental for tax purposes, you can deduct expenses such as mortgage interest, property taxes, insurance, and maintenance costs. Additionally, you can claim depreciation on the property’s value, which can offset the taxable rental income. However, if the property is also used personally (e.g., if you occasionally stay there), the IRS imposes strict rules on how expenses are allocated between personal and rental use. For instance, if you use the property for personal purposes more than 14 days per year, special limitations apply to deducting rental losses.

Internationally, tax rules for family rentals differ widely. In the UK, for example, rental income from family members is taxable, but if the rent is below market value, the tax liability is calculated based on the market rent, not the actual rent received. In Canada, the Canada Revenue Agency (CRA) requires that the rental arrangement be at fair market value and documented properly to avoid recharacterization as a gift. In Australia, the Australian Taxation Office (ATO) allows deductions for expenses only if the rental income is declared at market rates and the arrangement is commercial in nature.

Practical tips for navigating family rentals include maintaining clear records of all transactions, including rent payments and expenses, and consulting a tax professional to ensure compliance with local laws. If the rent is below market value, consider whether the difference is intended as a gift, as gifts may have separate tax implications, such as gift tax in the U.S. if the amount exceeds the annual exclusion limit ($17,000 per recipient in 2023). Finally, if the property is part of an estate plan, structuring the rental agreement carefully can help avoid unintended tax consequences for both you and your parents.

Rent the Runway: Shuttle Service to Secaucus?

You may want to see also

Explore related products

![]()

Fair Market Value Considerations

Rent received from parents is taxable if it exceeds the fair market value of the property. This distinction is crucial because the Internal Revenue Service (IRS) considers any amount above fair market rent as a gift, which may have separate tax implications. For instance, if a parent pays $1,500 monthly for a room that typically rents for $1,000 in the area, the $500 difference could be classified as a gift rather than taxable income. Understanding fair market value is the first step in determining your tax liability accurately.

To establish fair market value, compare your rental arrangement to similar properties in your area. Use online tools like Zillow, Craigslist, or local real estate listings to gauge average rents for comparable spaces. Consider factors such as location, property size, amenities, and condition. For example, a two-bedroom apartment in a suburban area might rent for $1,200, while a similar unit in a city center could command $1,800. Documenting these comparisons provides a defensible basis for your rental rate if questioned by the IRS.

If the rent from your parents is below fair market value, the IRS may still consider the full amount as taxable income if it views the arrangement as a rental agreement rather than a gift. To avoid this, ensure the rental agreement is structured like any other tenancy. Draft a formal lease agreement, require regular payments, and maintain records of all transactions. For example, if you charge $800 for a room worth $1,200, the IRS might argue the full $1,200 is taxable unless you can prove the lower rate is part of a legitimate familial arrangement.

Finally, consult a tax professional if your rental arrangement with parents involves complexities like property ownership or shared living spaces. They can help navigate IRS rules, such as the "personal use" exception, which may apply if you and your parents share the property. For example, if you rent out a portion of your home while living there, the tax treatment differs from renting out a separate property. Proactive planning and accurate valuation ensure compliance while minimizing tax liabilities.

Maximize Your Yoga Studio: Tips for Renting Additional Space Effectively

You may want to see also

Explore related products

![The Parent Trap [ NON-USA FORMAT, PAL, Reg.2 Import - United Kingdom ]](https://m.media-amazon.com/images/I/81obEM2Y-sL._AC_UY218_.jpg)

![The Parent Trap [VHS]](https://m.media-amazon.com/images/I/819y6A-veOL._AC_UY218_.jpg)

![]()

Reporting Rental Income to IRS

Rent received from parents, whether it’s for a room in your home or a separate property, is taxable income in the eyes of the IRS. This means you must report it on your federal tax return, regardless of the familial relationship. The IRS considers rental income as any payment received for the use or occupancy of property, and it doesn’t exempt transactions between family members. Failing to report this income could result in penalties, audits, or back taxes owed, so compliance is critical.

To report rental income from parents, use Schedule E (Form 1040) to declare the total amount received. This includes not only cash payments but also any services or property provided in lieu of rent. For example, if your parents pay your utilities or property taxes as part of the rental agreement, those amounts must be included as income. Keep detailed records of all transactions, including dates, amounts, and any agreements in writing, to substantiate your reporting in case of an audit.

One common misconception is that rent from family members is exempt from taxes if it’s below a certain threshold. However, the IRS does not impose a minimum income requirement for reporting rental income. Even if the amount is small, it must be declared. Additionally, if you’re renting out a portion of your primary residence, you may need to allocate expenses like mortgage interest and property taxes between the rental and personal-use portions of the property, which can complicate your reporting.

A practical tip is to treat the rental arrangement with your parents as you would with any other tenant. Draft a formal lease agreement outlining the terms, including rent amount, due dates, and responsibilities. This not only ensures clarity but also provides documentation to support your tax reporting. If you’re unsure about how to allocate expenses or report the income, consult a tax professional to avoid errors that could trigger IRS scrutiny.

Finally, consider the tax deductions available to offset rental income. Expenses such as repairs, maintenance, property management fees, and depreciation can reduce your taxable rental income. However, these deductions must be directly related to the rental activity and properly documented. By accurately reporting rental income and claiming eligible deductions, you can fulfill your tax obligations while minimizing your liability.

Average Rent for 3-Bedroom, 2-Bathroom Townhouses: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Exemptions and Deductions for Family Rent

Rent received from family members, including parents, often blurs the lines between personal and taxable income. However, specific exemptions and deductions can alleviate tax burdens under certain conditions. For instance, if the property rented to parents is a primary residence and the rent charged is below the fair market value, the IRS may consider it a personal arrangement rather than a taxable transaction. This distinction hinges on whether the agreement is deemed arm’s length or a familial gesture. Understanding these nuances is crucial for accurate tax reporting and compliance.

One key exemption arises when the rental income is offset by allowable deductions. Expenses such as mortgage interest, property taxes, maintenance, and depreciation can be deducted against the rent received, potentially reducing or eliminating taxable income. For example, if a homeowner receives $1,000 monthly from their parents but incurs $800 in deductible expenses, only $200 would be taxable. Proper documentation of these expenses is essential, as the IRS scrutinizes family transactions for fairness and legitimacy.

Another critical factor is the property’s classification. If the rented space is part of the taxpayer’s primary residence, the rental income may qualify for partial exclusion under the *renting part of your home* rules. For instance, if parents occupy a self-contained unit within the homeowner’s house, and the space is used exclusively by them, up to 14 days of rental income per year can be tax-free. This exemption is particularly useful for short-term or informal arrangements.

For long-term rentals, the *fair rental value* test becomes pivotal. If the rent charged to parents is significantly below market rates, the IRS may impute the fair market value as taxable income. However, if the rent is at or above market value, standard rental income rules apply, allowing for full deductions. Taxpayers should research local rental rates and maintain records to substantiate their charges.

Lastly, state-specific laws can further influence tax treatment. Some states align with federal guidelines, while others impose additional restrictions or benefits. For example, California allows deductions for property expenses but requires detailed documentation for family rentals. Consulting a tax professional or using tax software tailored to state regulations can ensure compliance and maximize deductions. By leveraging these exemptions and deductions, taxpayers can navigate the complexities of family rent transactions with confidence.

Top Minneapolis Trampoline Parks: Where to Bounce and Rent Time

You may want to see also

Frequently asked questions

Yes, rent received from parents is generally considered taxable income, even if you live with them, as it is treated as rental income by tax authorities.

Yes, regardless of the amount, rent received from parents must be reported as taxable income, though tax implications may vary based on local tax laws.

Yes, you may be able to claim deductions for expenses related to the rental property, such as maintenance, repairs, or mortgage interest, depending on tax regulations.

If the payment is structured as rent (even informally), it is typically taxable. However, if it’s clearly a gift and not rent, it may not be taxable, though rules vary by jurisdiction.