Renting out a condo can be a lucrative investment, but its viability depends on several factors such as location, market demand, and property management costs. In high-demand areas, condos often attract steady rental income and can appreciate in value over time, making them a solid long-term investment. However, investors must consider expenses like maintenance fees, property taxes, and potential vacancies, which can impact profitability. Additionally, the condo’s condition, local rental regulations, and the investor’s financial readiness play crucial roles in determining whether it’s a wise decision. For those willing to navigate these challenges, renting out a condo can offer both passive income and equity growth, but thorough research and planning are essential to ensure success.

Explore related products

What You'll Learn

- Potential rental income vs. mortgage and maintenance costs analysis

- Market demand and location impact on condo rental profitability

- Tax benefits and deductions for condo rental property owners

- Risks of tenant turnover, property damage, and legal issues

- Long-term appreciation potential versus immediate cash flow returns

![]()

Potential rental income vs. mortgage and maintenance costs analysis

When considering whether renting out a condo is a good investment, a critical analysis of potential rental income versus mortgage and maintenance costs is essential. This analysis helps determine the property’s cash flow potential and long-term profitability. Start by researching the local rental market to estimate the monthly rental income you can expect. Compare this figure to your monthly mortgage payment, including principal, interest, taxes, and insurance (PITI). If the rental income exceeds the mortgage cost, the property is cash flow positive, which is a strong indicator of a good investment. However, if the mortgage costs are higher, you may need to reassess the property’s viability or consider ways to increase rent or reduce expenses.

Beyond the mortgage, maintenance and operational costs play a significant role in the financial equation. Condos often come with homeowners’ association (HOA) fees, which cover shared amenities and maintenance but can be substantial. Additionally, factor in potential repairs, property management fees (if hiring a manager), utilities, and vacancy periods when the unit is unoccupied. These expenses can quickly erode rental income if not carefully managed. A thorough analysis should include setting aside a reserve fund for unexpected repairs and accounting for periodic updates to keep the property competitive in the rental market.

To conduct a detailed rental income vs. costs analysis, create a spreadsheet outlining all projected monthly expenses and income. Include fixed costs like the mortgage and HOA fees, as well as variable costs like maintenance and vacancies. Subtract these total expenses from the expected rental income to calculate the net cash flow. For a more conservative estimate, consider using a vacancy rate of 5-10% and budgeting for higher maintenance costs in the first few years. This approach ensures a realistic assessment of the property’s financial performance.

Another aspect to consider is the potential for rental income growth versus the fixed or predictable increase in mortgage and maintenance costs. In high-demand rental markets, rents may rise over time, improving cash flow and overall returns. However, mortgage payments (if fixed) and HOA fees may remain stable or increase minimally, providing a hedge against inflation. Conversely, in stagnant or declining markets, rental income may not keep pace with rising expenses, making the investment less attractive. Analyzing local market trends and economic indicators can help forecast these dynamics.

Finally, evaluate the long-term return on investment (ROI) by considering both cash flow and property appreciation. While positive cash flow is crucial for short-term sustainability, the condo’s appreciation over time can significantly impact overall profitability. Compare the potential ROI of renting out the condo to other investment opportunities, such as stocks or real estate investment trusts (REITs). If the condo offers competitive returns after accounting for all costs and risks, it may be a worthwhile investment. However, if the analysis reveals marginal returns or high financial strain, it might be prudent to explore alternative investment options.

Applying for Rental Assistance: A Step-by-Step Guide to Getting Help

You may want to see also

Explore related products

![]()

Market demand and location impact on condo rental profitability

When considering whether renting out a condo is a good investment, market demand plays a pivotal role in determining profitability. High demand for rental properties in a particular area can drive up rental prices and reduce vacancy rates, ensuring a steady income stream. Factors influencing demand include population growth, employment opportunities, and lifestyle trends. For instance, condos located in urban centers or near major employers tend to attract young professionals and commuters, creating a robust rental market. Conversely, areas with stagnant or declining populations may struggle to fill rental units, leading to lower returns. Analyzing local market trends and demographic data is essential to gauge the potential demand for condo rentals.

Location is equally critical in maximizing condo rental profitability. Proximity to amenities such as public transportation, schools, shopping centers, and recreational facilities can significantly enhance a property’s appeal to tenants. For example, condos in walkable neighborhoods or near transit hubs often command higher rents due to their convenience. Additionally, areas with low crime rates and high-quality schools are particularly attractive to families, a demographic that often seeks long-term rentals. Coastal or scenic locations may also appeal to tourists or seasonal renters, offering opportunities for short-term rental income. However, prime locations often come with higher purchase prices, so investors must balance the potential for higher rents against the initial investment cost.

The interplay between market demand and location can create unique opportunities or challenges for condo investors. In high-demand areas, even less-than-ideal locations can yield profitable rentals due to the sheer number of prospective tenants. Conversely, a poorly located condo in a low-demand market is unlikely to generate significant returns, regardless of its condition or amenities. Investors should also consider future developments in the area, such as new infrastructure projects or zoning changes, which can impact both demand and property values. For instance, a planned transit expansion could increase the desirability of a currently underserved neighborhood, boosting rental potential.

Another aspect to consider is the competition within the local rental market. In areas saturated with rental properties, landlords may need to offer competitive pricing or additional perks to attract tenants. This can erode profitability, especially if the condo’s location or condition does not stand out. Conducting a comparative market analysis (CMA) to assess local rental rates and vacancy levels is crucial for setting realistic expectations. Investors should also evaluate the condition and features of their condo relative to competitors, as upgrades or unique amenities can justify higher rents even in a crowded market.

Finally, seasonality and target demographics can further influence the profitability of renting out a condo based on location and demand. In tourist-heavy areas, short-term rentals may yield higher returns during peak seasons but could face vacancies in off-peak months. Conversely, condos in areas dominated by students or young professionals may experience consistent demand year-round but require frequent tenant turnover. Tailoring the rental strategy to the specific demands of the local market—whether through long-term leases, short-term rentals, or targeted marketing—can optimize profitability. Ultimately, a thorough understanding of market demand and location-specific factors is indispensable for determining whether renting out a condo is a sound investment.

Nonpayment of Rent: Understanding Breach of Contract Implications

You may want to see also

Explore related products

![]()

Tax benefits and deductions for condo rental property owners

Renting out a condo can be a lucrative investment, and one of the significant advantages lies in the various tax benefits and deductions available to property owners. These incentives can substantially reduce the overall tax burden, making condo rentals an even more attractive financial venture. Here's an in-depth look at some of the key tax advantages:

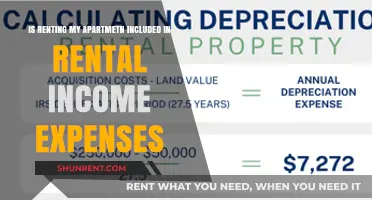

Depreciation Deduction: One of the most valuable tax benefits for condo rental property owners is the ability to claim depreciation. Depreciation allows you to deduct a portion of the property's value as an expense each year, recognizing the wear and tear and obsolescence of the building and its assets. This deduction is unique to investment properties and can result in substantial tax savings. The IRS has specific guidelines for depreciation, typically allowing a recovery period of 27.5 years for residential properties. This means you can deduct a percentage of the property's value annually, reducing your taxable rental income.

Operating Expenses: Condo rental owners can deduct a wide range of operating expenses, which are the day-to-day costs of running the rental business. These expenses may include property management fees, maintenance and repair costs, insurance premiums, property taxes, advertising for tenants, legal fees, and even travel expenses related to managing the property. For instance, if you need to visit the condo for repairs or to meet with tenants, the travel costs can be tax-deductible. Keeping detailed records of these expenses is essential to maximize your deductions and ensure compliance with tax regulations.

Mortgage Interest and Property Taxes: If you have a mortgage on the rental condo, the interest paid on that mortgage is generally tax-deductible. This can be a significant benefit, especially in the early years of the mortgage when a large portion of the payment goes towards interest. Additionally, property taxes paid on the rental property are also deductible. These deductions can substantially lower your taxable income, especially in areas with high property tax rates. It's important to note that these deductions are typically claimed on Schedule E of your tax return, which is used to report income and expenses from rental real estate.

Capital Improvements: While repairs and maintenance are deductible as operating expenses, capital improvements deserve special attention. These are substantial upgrades or restorations that increase the property's value, prolong its life, or adapt it to new uses. Examples include renovating a kitchen, adding a new roof, or installing a security system. The cost of capital improvements cannot be deducted in the year they are incurred but can be depreciated over several years, providing long-term tax benefits. Properly identifying and documenting these improvements is crucial for accurate tax reporting.

Passive Activity Losses: For many condo rental owners, the property may not generate positive cash flow immediately, especially if there are periods of vacancy or high initial investment costs. The IRS allows taxpayers to deduct passive activity losses, which include rental real estate activities, against passive activity income. This means that if your rental property incurs a loss, you may be able to use it to offset income from other passive investments. However, there are specific rules and limitations to this deduction, and it's essential to consult a tax professional to ensure compliance. Understanding these tax benefits and deductions is crucial for condo rental property owners to optimize their investment strategy and maximize their returns. It is always advisable to seek professional tax advice to ensure you take full advantage of these incentives while remaining compliant with the ever-evolving tax laws.

Exploring Rental Options: A Practical Guide

You may want to see also

Explore related products

![]()

Risks of tenant turnover, property damage, and legal issues

Renting out a condo can be a lucrative investment, but it’s not without its risks, particularly when it comes to tenant turnover, property damage, and legal issues. Tenant turnover is one of the most significant challenges landlords face. Every time a tenant moves out, there’s a vacancy period where the property generates no income. Marketing the unit, screening new tenants, and preparing the condo for occupancy all require time and money. High turnover rates can erode profitability, especially if the rental market is slow or if the property is in a less desirable location. To mitigate this risk, landlords must focus on tenant retention strategies, such as maintaining the property well, addressing concerns promptly, and offering competitive lease terms.

Property damage is another major risk associated with renting out a condo. Even the most responsible tenants can cause accidental damage, while others may neglect the property or intentionally cause harm. Common issues include stains, broken fixtures, or structural damage from unauthorized modifications. While security deposits can cover minor repairs, extensive damage may exceed the deposit amount, leaving landlords to bear the cost. Regular inspections and clear lease agreements outlining tenant responsibilities can help minimize this risk. Additionally, landlords should consider investing in property insurance that covers rental-specific damages, though this adds to ongoing expenses.

Legal issues pose a third significant risk for condo landlords. Rental laws vary by location, and non-compliance can result in costly fines, lawsuits, or even the loss of rental income. For example, improper handling of security deposits, failure to provide habitable living conditions, or discriminatory tenant screening practices can lead to legal disputes. Eviction processes, in particular, are highly regulated and can be time-consuming and expensive if not executed correctly. Landlords must stay informed about local tenant-landlord laws, maintain detailed records, and consider consulting legal professionals to ensure compliance.

The intersection of these risks—tenant turnover, property damage, and legal issues—can compound the challenges of renting out a condo. For instance, a problematic tenant who causes damage may also require eviction, leading to legal fees, repair costs, and vacancy losses. Similarly, frequent turnover increases the likelihood of wear and tear, as well as the potential for disputes over security deposit deductions. Landlords must weigh these risks against the potential returns and decide whether they have the time, resources, and risk tolerance to manage them effectively.

To navigate these risks, proactive management is essential. Screening tenants thoroughly, including background and credit checks, can reduce the likelihood of problematic renters. Clear, comprehensive lease agreements that outline expectations and consequences can deter misconduct and provide legal protection. Building a relationship with reliable contractors for maintenance and repairs can also minimize downtime and costs. While renting out a condo can be a good investment, it requires careful planning, ongoing effort, and a willingness to address these risks head-on.

Understanding Rent-to-Own Homes in Georgia: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Long-term appreciation potential versus immediate cash flow returns

When considering whether renting out a condo is a good investment, one of the most critical decisions is balancing long-term appreciation potential against immediate cash flow returns. Both aspects are essential, but they serve different financial goals and come with distinct risks and rewards. Understanding this trade-off is key to determining if condo rental aligns with your investment strategy.

Long-term appreciation potential refers to the increase in the property's value over time. Condos in prime locations or growing markets often appreciate significantly, providing substantial equity gains when sold. This strategy is ideal for investors with a long-term horizon who can withstand market fluctuations and hold the property for 10–20 years or more. For example, urban condos in areas with rising demand, infrastructure development, or limited housing supply tend to appreciate faster. However, appreciation is not guaranteed and depends on factors like market conditions, local economy, and property maintenance. Investors focusing on appreciation may prioritize capital gains over monthly cash flow, sometimes even accepting break-even or slightly negative cash flow if the property’s value is expected to rise substantially.

On the other hand, immediate cash flow returns focus on generating consistent monthly income from rent after covering expenses like mortgage, property taxes, maintenance, and vacancies. This approach appeals to investors seeking steady, passive income to supplement their earnings or reinvest in other opportunities. To maximize cash flow, investors often target condos in high-demand rental markets with lower purchase prices and strong tenant pools, such as college towns or affordable urban neighborhoods. However, properties with high cash flow potential may have slower appreciation rates, especially if they are in less desirable or oversaturated areas. Additionally, relying on cash flow requires careful management to avoid vacancies and unexpected expenses, which can erode profitability.

The choice between long-term appreciation and immediate cash flow depends on your financial goals, risk tolerance, and market conditions. Investors seeking wealth accumulation over decades may prioritize appreciation, viewing the condo as a vehicle for building equity. Conversely, those needing regular income or preferring a more hands-on approach may favor cash flow. Some investors strike a balance by selecting properties with moderate appreciation potential and positive cash flow, ensuring both short-term stability and long-term growth.

Ultimately, renting out a condo can be a good investment if it aligns with your objectives. If you’re willing to wait for the property’s value to increase, long-term appreciation may yield higher returns. If immediate income is more important, focusing on cash flow could be the better strategy. Conduct thorough market research, analyze local trends, and consider consulting with real estate professionals to make an informed decision tailored to your circumstances.

Renting in NYC: A Foreigner's Guide to Navigating the Big Apple

You may want to see also

Frequently asked questions

Renting out a condo can be a good investment if it generates positive cash flow, appreciates in value, and aligns with your financial goals. However, it depends on factors like location, market demand, and maintenance costs.

Calculate the potential rental income and subtract all expenses (mortgage, HOA fees, taxes, maintenance, etc.). If the net income is positive and meets your ROI expectations, it’s likely a profitable investment.

Yes, risks include tenant turnover, property damage, legal issues, and market downturns. Proper screening, insurance, and a financial buffer can mitigate these risks.

Location is critical. Condos in high-demand areas (e.g., near jobs, schools, or amenities) tend to attract more tenants and command higher rents, making them better investments.

Hiring a property manager can save time and reduce stress, especially if you’re not local or don’t want to handle tenant issues. However, it adds to expenses, so weigh the cost against the convenience.