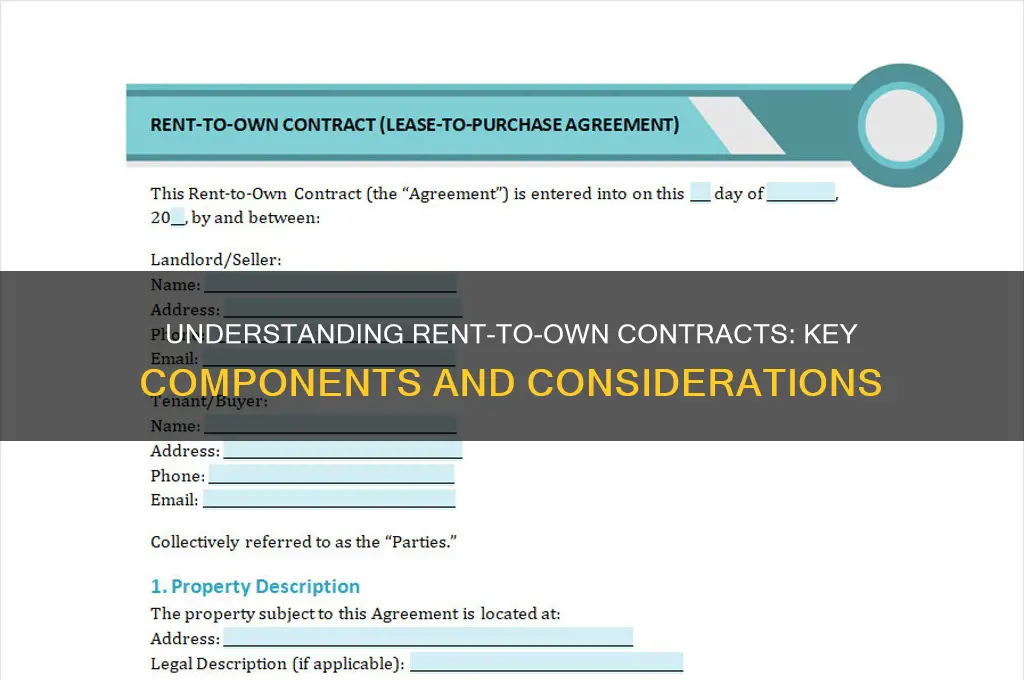

A rent-to-own contract is a unique agreement that combines elements of a lease and a purchase agreement, allowing tenants to rent a property with the option to buy it at a later date. Key components typically include the lease term, monthly rent payments, a predetermined purchase price, and an option fee—a non-refundable upfront payment that secures the right to purchase the property. The contract also outlines how a portion of the rent may be credited toward the down payment, the conditions under which the tenant can exercise the purchase option, and any maintenance responsibilities. Additionally, it specifies the timeline for the purchase, potential penalties for early termination, and the terms for financing the property. Understanding these details is crucial for both parties to ensure clarity and protect their interests throughout the agreement.

Explore related products

What You'll Learn

- Purchase Price & Down Payment: Total cost, initial payment, and how it’s applied to ownership

- Monthly Payments: Rent amount, due dates, and how payments contribute to purchase

- Lease Term: Duration of the rental period before ownership option activates

- Maintenance Responsibilities: Who handles repairs and upkeep during the lease term

- Option Fee & Terms: Non-refundable fee to secure the purchase option and conditions

![]()

Purchase Price & Down Payment: Total cost, initial payment, and how it’s applied to ownership

The purchase price in a rent-to-own contract is the agreed-upon amount the tenant-buyer will pay to own the property outright by the contract’s end. This figure is typically locked in at the start, shielding the buyer from market fluctuations. For instance, if a home’s current value is $250,000, the contract might set this as the purchase price, even if the market rises to $300,000 during the rental period. This predictability is a key advantage, but it also requires careful negotiation to ensure the price is fair and aligned with future market expectations.

The down payment in a rent-to-own agreement serves as a commitment fee, typically ranging from 3% to 20% of the purchase price. Unlike traditional rentals, this payment is non-refundable and applies toward the final purchase. For example, on a $250,000 home, a 5% down payment would be $12,500, reducing the remaining balance to $237,500. This initial investment demonstrates the buyer’s seriousness and reduces the total cost of ownership. However, tenants should ensure the contract explicitly states how this payment is applied to avoid disputes later.

How the down payment and rent payments contribute to ownership varies by contract. Some agreements allocate a portion of each rent payment (e.g., 20%) toward the purchase price, effectively building equity over time. For instance, if monthly rent is $1,500, $300 might go toward the purchase. This structure benefits buyers who want to gradually reduce their future payment burden. However, not all contracts include this feature, so tenants must clarify terms upfront. Without such provisions, the down payment remains the only contribution until the final purchase.

A critical caution: ambiguity in how payments are applied can lead to financial setbacks. Tenants should insist on clear, written terms specifying the exact allocation of down payments and rent credits. For example, a contract might state, “$12,500 down payment plus $300/month from rent applied to purchase price.” Additionally, buyers should verify whether these contributions are refundable if they opt not to purchase. While rare, some contracts allow partial refunds or credits, but most treat these payments as sunk costs if the buyer walks away.

In conclusion, the purchase price and down payment are foundational elements of a rent-to-own contract, requiring careful negotiation and clarity. Locking in a fair purchase price protects buyers from market volatility, while a substantial down payment reduces long-term costs. Tenants must scrutinize how payments contribute to ownership, ensuring every dollar paid moves them closer to their goal. By treating this section as a financial blueprint, buyers can maximize benefits and minimize risks in their path to homeownership.

How to Apply for Rent Relief: A Step-by-Step Guide

You may want to see also

Explore related products

![Adams Residential Lease, Forms and Instructions [Print and Downloadable] (LF310)](https://m.media-amazon.com/images/I/81uP3OCk9qL._AC_UY218_.jpg)

![]()

Monthly Payments: Rent amount, due dates, and how payments contribute to purchase

A rent-to-own contract hinges on clear, structured monthly payments that serve dual purposes: covering rent and building equity toward the eventual purchase. The rent amount is typically higher than market rate, as a portion of each payment contributes to the purchase price. For instance, if the monthly rent is $1,200, $300 might be allocated to the purchase fund, reducing the final amount owed when the tenant decides to buy. This structure requires precise calculation and agreement upfront to avoid disputes later.

Due dates are critical in rent-to-own agreements, as missed or late payments can jeopardize the tenant’s progress toward ownership. Most contracts specify a grace period (usually 3–5 days) before penalties apply, but consistent tardiness may void the purchase option. Tenants should align their payment schedule with their income cycle—whether weekly, bi-weekly, or monthly—to ensure timely payments. Setting up automatic transfers or reminders can mitigate the risk of oversight, especially when juggling multiple financial obligations.

The contribution of payments to the purchase price is where rent-to-own contracts differ from standard leases. For example, if a tenant pays $1,500 monthly for 36 months, with $400 allocated to the purchase fund, they’ll have accumulated $14,400 toward the down payment by the end of the term. This reduces the final purchase price proportionally, making the property more attainable. However, tenants must understand that this equity is often non-refundable if they choose not to buy, emphasizing the need for long-term commitment.

Practical tips for managing these payments include negotiating flexibility in the contract, such as allowing lump-sum contributions to accelerate equity buildup. Tenants should also request a detailed breakdown of each payment, showing how much goes toward rent versus the purchase fund. Keeping meticulous records of all transactions is essential, as discrepancies can arise during the final purchase phase. Finally, tenants should factor in additional costs like maintenance fees or property taxes, which may or may not be included in the monthly payment, to avoid financial surprises.

In summary, monthly payments in a rent-to-own contract are a delicate balance of rent and equity-building, requiring discipline, clarity, and foresight. By understanding the mechanics of these payments, tenants can maximize their investment while landlords ensure consistent cash flow and a motivated buyer. Both parties benefit from transparency and adherence to the agreed terms, turning a rental agreement into a pathway to homeownership.

Rent-to-Own Serum: Splice Not Always Needed

You may want to see also

Explore related products

![]()

Lease Term: Duration of the rental period before ownership option activates

The lease term in a rent-to-own contract is a critical component that defines the duration of the rental period before the tenant can exercise the option to purchase the property. Typically, this period ranges from 1 to 5 years, though some contracts may extend up to 7 years depending on the agreement between the parties. This timeframe is not arbitrary; it is carefully structured to allow tenants to build equity, improve credit, or save for a down payment while enjoying the benefits of living in the home. For instance, a 3-year lease term is common because it strikes a balance between giving tenants enough time to prepare financially and providing landlords with a reasonable period to assess the tenant’s commitment.

When drafting the lease term, it’s essential to consider both parties’ goals. For tenants, a longer lease term can provide stability and more time to secure financing, but it also means committing to a property without the flexibility of a standard rental agreement. For landlords, a shorter term may reduce risk if the tenant defaults, but it might not allow enough time for the tenant to qualify for a mortgage. A practical tip is to include a clause that allows for a mutual extension of the lease term if both parties agree, providing flexibility without compromising the contract’s structure.

Comparatively, the lease term in a rent-to-own contract differs significantly from traditional leases. In a standard rental agreement, the tenant has no obligation or right to purchase the property, and the lease term is often 12 months with the option to renew. In contrast, a rent-to-own contract’s lease term is a stepping stone toward ownership, often with a portion of the rent (typically 20-30%) allocated toward the down payment. This distinction underscores the importance of clearly defining the lease term’s length and its implications for both parties.

One cautionary note is to avoid overly long lease terms without built-in milestones. For example, a 5-year term might seem appealing for long-term planning, but without periodic reviews or options to adjust the agreement, it can lead to stagnation. Incorporating annual reviews or benchmarks, such as credit score improvements or savings targets, can keep the contract dynamic and aligned with the tenant’s progress. Additionally, specifying the consequences of early termination or default during the lease term is crucial to protect both parties’ interests.

In conclusion, the lease term is more than just a timeline—it’s a strategic element of the rent-to-own contract that shapes the path to homeownership. By carefully selecting the duration, incorporating flexibility, and setting clear expectations, both tenants and landlords can maximize the benefits of this arrangement. Whether opting for a 2-year term to expedite the process or a 5-year term for gradual preparation, the key is to ensure the lease term aligns with the financial and personal goals of all involved parties.

Measuring a Year in Rent: Life's Cost and Value Insights

You may want to see also

Explore related products

![]()

Maintenance Responsibilities: Who handles repairs and upkeep during the lease term

In a rent-to-own contract, maintenance responsibilities are a critical yet often overlooked detail that can significantly impact both the tenant-buyer and the landlord-seller. Typically, the tenant-buyer assumes responsibility for day-to-day upkeep, such as lawn care, changing air filters, and minor repairs under a certain cost threshold (e.g., $100). However, major repairs—like fixing a leaky roof or replacing an HVAC system—usually fall to the landlord-seller, as these are considered structural or essential to the property’s integrity. This division ensures the tenant-buyer isn’t burdened with unexpected expenses while incentivizing them to maintain the property they may eventually own.

Consider the example of a tenant-buyer who notices a dripping faucet. Under most agreements, they’d handle this minor repair themselves, as it’s part of routine maintenance. Conversely, if the water heater fails, the landlord-seller would likely be responsible, as this is a major system repair. Clarity in the contract is key: specify which repairs the tenant-buyer can handle independently and which require landlord approval. Including a clause that outlines a maximum repair cost the tenant-buyer can incur without reimbursement (e.g., $50) can prevent disputes and ensure both parties understand their obligations.

From a persuasive standpoint, landlords-sellers should view clear maintenance responsibilities as a protective measure. By retaining control over major repairs, they safeguard their investment while allowing tenant-buyers to build equity through minor upkeep. For tenant-buyers, accepting these responsibilities demonstrates commitment to the property, which can strengthen their case for eventual ownership. However, they should negotiate for a clause that allows them to deduct maintenance costs from the rent or purchase price, ensuring their efforts aren’t financially one-sided.

Comparatively, traditional rental agreements often place all maintenance burdens on landlords, while homeowner responsibilities are entirely on the owner. Rent-to-own contracts blend these models, requiring a hybrid approach. For instance, tenant-buyers might handle cosmetic repairs (e.g., painting, patching holes) while landlords address structural issues. This shared responsibility reflects the unique nature of rent-to-own agreements, where both parties have a vested interest in the property’s condition.

In practice, tenant-buyers should keep detailed records of all maintenance activities, including receipts and before-and-after photos, to document their contributions. Landlords-sellers, meanwhile, should conduct periodic inspections (e.g., every six months) to ensure the property is being maintained to standard. By fostering transparency and accountability, both parties can avoid misunderstandings and ensure the property remains in optimal condition throughout the lease term.

Florida Rent Control: Understanding Caps and Tenant Protections in 2023

You may want to see also

Explore related products

![Problems in Contract Law: Cases and Materials [Connected eBook with Study Center] (Aspen Casebook)](https://m.media-amazon.com/images/I/71KVwHbBZ1L._AC_UL320_.jpg)

$204.51 $359

![Contracts: Cases and Doctrine [Connected eBook with Study Center] (Aspen Casebook Series)](https://m.media-amazon.com/images/I/61O10YrdWFL._AC_UL320_.jpg)

![Contracts: A Modern Coursebook [Connected eBook with Study Center] (Aspen Casebook)](https://m.media-amazon.com/images/I/616HqNXJThL._AC_UL320_.jpg)

![]()

Option Fee & Terms: Non-refundable fee to secure the purchase option and conditions

A rent-to-own contract often begins with a critical component: the option fee. This fee is a non-refundable payment made by the tenant to the landlord, granting the tenant the exclusive right to purchase the property at a predetermined price within a specified timeframe. Think of it as a down payment on the opportunity to buy, not the property itself. Typically ranging from 1% to 5% of the property’s agreed-upon purchase price, this fee serves as a commitment from the tenant and a safeguard for the landlord. For example, if a home is valued at $200,000, an option fee of 3% would amount to $6,000, securing the tenant’s right to purchase the property under the agreed terms.

While the option fee is non-refundable, it’s important to understand its purpose and implications. Unlike a security deposit, which may be returned at the end of a lease, the option fee is retained by the landlord regardless of whether the tenant ultimately decides to buy. This fee compensates the landlord for taking the property off the market and locking in the sale price during the lease term. For tenants, it’s a calculated risk—a way to secure the option to buy while building equity through rent payments. However, tenants should carefully weigh their financial readiness and long-term plans before committing to this fee, as losing it could be costly if circumstances change.

Negotiating the terms of the option fee is a critical step in crafting a fair rent-to-own agreement. Tenants should seek clarity on how the fee is applied if they choose to purchase the property. In some cases, the fee may be credited toward the down payment or closing costs, effectively reducing the upfront burden at the time of purchase. For instance, if the $6,000 option fee is credited toward a 10% down payment on a $200,000 home, the tenant would only need to provide an additional $14,000 at closing. This arrangement can make the option fee feel less like a loss and more like an investment in the tenant’s future homeownership.

Finally, tenants must scrutinize the conditions tied to the option fee and purchase terms. These conditions often include maintaining timely rent payments, adhering to property maintenance requirements, and meeting specific credit or financial benchmarks by the end of the lease term. Failure to meet these conditions could void the purchase option, leaving the tenant with no path to ownership and no refund of the option fee. For example, if a tenant’s credit score fails to improve to the agreed-upon threshold, the landlord may terminate the purchase option, even if all other terms have been met. Thus, tenants should approach rent-to-own contracts with a clear understanding of their obligations and a realistic plan to fulfill them.

Goodwill's Rental Assistance: Down Payment Help for Renters

You may want to see also

Frequently asked questions

A rent-to-own contract is an agreement that allows a tenant to rent a property with the option to purchase it at a later date, typically at a predetermined price. The contract combines elements of a standard lease agreement with a purchase option.

Key components include the lease term, monthly rent amount, purchase price, option fee (a non-refundable fee for the right to purchase), rent credits (portion of rent applied toward the down payment), and the timeline for exercising the purchase option.

The purchase price is typically agreed upon at the start of the contract and may be based on the current market value of the property or a future agreed-upon price. It remains fixed for the duration of the contract, regardless of market fluctuations.

The option fee is usually non-refundable and retained by the landlord as compensation for granting the purchase option. Rent credits, if applicable, may also be forfeited unless otherwise specified in the contract.

Yes, the tenant can typically back out, but they may lose the option fee and any rent credits. The specific consequences depend on the terms outlined in the contract, so it’s important to review it carefully.

![Drafting Contracts: How and Why Lawyers Do What They Do [Connected Ebook] (Aspen Coursebook) (Aspen Coursebook Series)](https://m.media-amazon.com/images/I/81SL5EH9XdL._AC_UL320_.jpg)