1099-MISC forms are typically used by businesses to report payments made to independent contractors or vendors for services rendered, but they are not generally used for reporting rent paid to landlords. Instead, rent payments are usually handled differently for tax purposes. However, if a landlord receives payments totaling $600 or more from a business tenant during the tax year, the business may be required to issue a 1099-MISC form to the landlord, specifically reporting the rent paid in Box 1 (Rents). This is less common for individual renters and more applicable to commercial leases. It’s important for both landlords and tenants to understand these requirements to ensure compliance with IRS regulations and avoid potential penalties.

| Characteristics | Values |

|---|---|

| Purpose | Used to report miscellaneous income, including rent payments in certain cases. |

| Applicability to Rent | Generally not required for personal rent payments to landlords. |

| Exception for Rent | Required if rent is paid to a business or for business-related property. |

| Filing Requirement | Mandatory if payments exceed $600 in a tax year. |

| Form Name | 1099-MISC (Miscellaneous Income). |

| Box Used for Rent | Box 1 (Rents) for reporting rent payments. |

| Due Date (Recipient Copy) | January 31st of the year following the tax year. |

| Due Date (IRS Copy) | February 28th (paper filing) or March 31st (electronic filing). |

| Penalty for Non-Filing | Penalties vary based on tardiness and size of the business. |

| Recipient Information | Requires recipient's name, address, and Taxpayer Identification Number (TIN). |

| Landlord Responsibility | Landlords must issue 1099-MISC if they receive $600+ in business-related rent. |

| Tenant Responsibility | Tenants typically do not file 1099-MISC for personal rent payments. |

| IRS Reference | IRS Publication 1779 and Instructions for Form 1099-MISC. |

Explore related products

$9.99

![Adams Notice to Pay Rent or Vacate, Forms and Instructions [Print and Downloadable] (LF280), White](https://m.media-amazon.com/images/I/81FvibdeL4L._AC_UL320_.jpg)

What You'll Learn

- Reporting Rent Payments: When and how to report rent payments on a 1099-MISC form

- Landlord Requirements: Obligations of landlords to issue 1099-MISC forms for rent received

- Tenant Exemptions: Situations where tenants are exempt from receiving a 1099-MISC for rent

- IRS Filing Deadlines: Key deadlines for filing 1099-MISC forms related to rent payments

- Penalties for Non-Compliance: Consequences of failing to report rent payments on 1099-MISC forms

![]()

Reporting Rent Payments: When and how to report rent payments on a 1099-MISC form

Rent payments typically fall outside the scope of 1099-MISC reporting requirements. The IRS mandates this form for reporting miscellaneous income, primarily focusing on payments to independent contractors, freelancers, and other non-employee service providers. However, there’s a critical exception: if you’re a property manager or real estate agent collecting rent on behalf of a property owner, and the total payments to that owner exceed $600 in a tax year, you must issue a 1099-MISC. This distinction hinges on your role—whether you’re acting as an intermediary or directly receiving rent as the property owner. Misunderstanding this can lead to unnecessary filings or penalties for non-compliance.

To report rent payments correctly on a 1099-MISC, follow these steps: first, confirm your obligation by verifying your role as a property manager or agent. Next, ensure the total payments to the property owner surpass the $600 threshold. Use Box 1 (Rents) on the form to report the exact amount paid. Include the owner’s taxpayer identification number (TIN) and address. File Copy A with the IRS by January 31 and provide Copy B to the property owner by the same deadline. Failure to meet these requirements can result in fines ranging from $50 to $550 per late or incorrect form, depending on the delay.

A common pitfall is assuming all rent payments require a 1099-MISC. For instance, if you’re a landlord receiving rent directly from tenants, you’re not required to file this form. The obligation lies solely with intermediaries managing payments for others. Additionally, if the property owner is a corporation, reporting is unnecessary, as corporations are exempt from 1099-MISC requirements. Always cross-reference IRS guidelines or consult a tax professional to avoid errors, especially when dealing with multiple properties or complex ownership structures.

Consider this scenario: a property management company collects $800 in monthly rent for a client, totaling $9,600 annually. Since the payments exceed $600, the company must issue a 1099-MISC to the property owner. However, if the same company manages a property owned by an LLC, no reporting is needed. This example underscores the importance of understanding the nuances of 1099-MISC rules. By staying informed and organized, you can ensure compliance while avoiding unnecessary administrative burdens.

Renting Camera Gear for Out-of-State Shoots: A Complete Guide

You may want to see also

Explore related products

![]()

Landlord Requirements: Obligations of landlords to issue 1099-MISC forms for rent received

Landlords who receive rent payments totaling $600 or more from a single tenant during the tax year are legally obligated to issue a 1099-MISC form to that tenant. This requirement stems from IRS regulations, which mandate reporting miscellaneous income, including rent, when it meets or exceeds this threshold. Failure to comply can result in penalties, making it crucial for landlords to understand and fulfill this obligation.

To issue a 1099-MISC, landlords must first collect the tenant’s taxpayer identification number (TIN) or Social Security number (SSN) using Form W-9. This step is non-negotiable, as the IRS requires accurate taxpayer information for proper reporting. Landlords should request this form at the start of the lease agreement to avoid last-minute scrambling during tax season. Once collected, the information must be retained for record-keeping purposes.

The 1099-MISC form must be filed with the IRS by January 31st of the following tax year, with a copy provided to the tenant by the same deadline. Landlords can file electronically through the IRS Filing Information Returns Electronically (FIRE) system or submit paper forms, though electronic filing is encouraged for efficiency. Missing these deadlines can result in fines ranging from $50 to $280 per form, depending on the delay.

While the obligation to issue 1099-MISC forms applies primarily to rent received from individuals, landlords should note exceptions. For instance, rent paid by corporations or LLCs classified as C corporations does not require a 1099-MISC, as these entities are not considered individuals under IRS rules. However, rent from LLCs classified as partnerships or sole proprietorships still falls under the reporting requirement.

Practical tips for landlords include maintaining detailed records of all rent payments throughout the year, using accounting software to track payments, and setting calendar reminders for January deadlines. Additionally, landlords should consult a tax professional if they are unsure about their reporting obligations, especially in complex scenarios involving multiple properties or tenants. Compliance not only avoids penalties but also fosters transparency and trust with tenants.

Rent in Stratford-upon-Avon: Is It Affordable or Overpriced?

You may want to see also

Explore related products

![]()

Tenant Exemptions: Situations where tenants are exempt from receiving a 1099-MISC for rent

Tenants generally do not receive 1099-MISC forms for rent payments because the IRS considers rent a personal expense, not taxable income. However, exceptions exist, particularly when tenants provide services to landlords in exchange for reduced rent. In such cases, the value of the services may be considered taxable income, requiring a 1099-MISC if it exceeds $600 annually. Yet, even within these exceptions, certain situations exempt tenants from receiving this form. Understanding these exemptions is crucial for both landlords and tenants to ensure compliance with tax regulations.

One key exemption arises when tenants perform minimal or incidental services for landlords. For example, if a tenant agrees to mow the lawn or shovel snow as part of their lease agreement, these tasks are typically considered part of maintaining the property rather than taxable services. The IRS does not require a 1099-MISC in such cases, as the services are deemed insignificant in relation to the overall rental arrangement. Landlords should carefully evaluate whether the services provided by tenants are truly incidental or if they cross the threshold into taxable territory.

Another exemption occurs when tenants live in rent-controlled or subsidized housing. In these scenarios, the rent paid is often below market value due to government assistance or regulations. Since the tenant’s payment is not considered full market rent, any services provided in exchange for reduced rent are generally not subject to 1099-MISC reporting. This exemption ensures that low-income tenants are not burdened with unexpected tax liabilities for minor services performed as part of their housing agreement.

Additionally, tenants who barter services for rent in informal, non-commercial arrangements are often exempt from receiving a 1099-MISC. For instance, if a tenant offers to paint a room in exchange for a rent reduction without a formal agreement, the IRS typically does not require reporting. However, landlords should exercise caution, as the lack of formal documentation does not automatically exempt the arrangement from scrutiny. Clear communication and adherence to IRS guidelines are essential to avoid potential tax issues.

In conclusion, while 1099-MISC forms are rarely issued to tenants for rent payments, understanding the exemptions is vital for both parties. Minimal services, rent-controlled housing, and informal barter arrangements are common scenarios where tenants are exempt from receiving this form. By staying informed and maintaining clear records, landlords and tenants can navigate these exceptions confidently, ensuring compliance without unnecessary complications.

Renting with a Husky: What You Need to Know

You may want to see also

Explore related products

![]()

IRS Filing Deadlines: Key deadlines for filing 1099-MISC forms related to rent payments

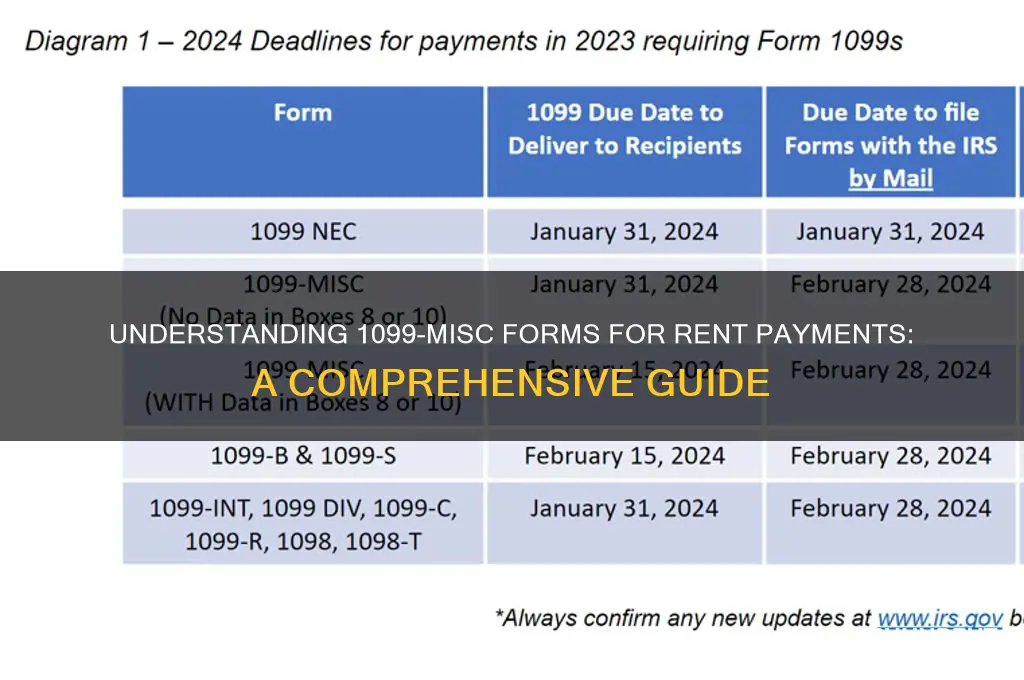

Landlords and property managers must adhere to strict IRS deadlines when filing 1099-MISC forms for rent payments made to vendors or service providers. Missing these deadlines can result in penalties ranging from $50 to $580 per form, depending on the delay. For rent-related payments, the key deadline is January 31st, when both the recipient and the IRS must receive Copy B of the 1099-MISC. This date is non-negotiable, even if it falls on a weekend or holiday, as the IRS expects timely compliance.

To avoid penalties, it’s crucial to understand the distinction between rent paid to a property owner (which typically doesn’t require a 1099-MISC) and payments made to independent contractors or service providers involved in rental operations. For example, if you paid a plumber $600 or more for repairs, a 1099-MISC is required. However, if you paid rent directly to a landlord, no form is necessary unless the landlord provided additional services beyond leasing the property.

Filing extensions are rarely granted for 1099-MISC forms, so proactive planning is essential. Gather recipient information (name, address, and Taxpayer Identification Number) by January 1st to ensure accuracy and allow time for corrections. Electronic filing through the IRS’s FIRE system can expedite processing and reduce errors, but it requires registration at least 5 business days in advance. Paper filers must submit forms to the IRS by February 28th, though the recipient deadline remains January 31st.

A common pitfall is assuming all rent-related payments are exempt from 1099-MISC reporting. For instance, payments to corporations (other than medical or legal services) are generally excluded, but payments to LLCs or sole proprietors often require reporting. Additionally, if you withheld federal income tax under backup withholding rules, you must file regardless of the payment amount. Cross-referencing IRS Publication 1220 and consulting a tax professional can clarify gray areas and ensure compliance.

Finally, maintaining detailed records is your best defense against audits or disputes. Retain invoices, contracts, and payment receipts for at least four years. If a recipient disputes the reported amount, promptly issue a corrected 1099-MISC using Form 1099-MISC with the “Corrected” box checked. Staying organized and informed not only meets IRS requirements but also streamlines your tax process, reducing stress during filing season.

Rent-to-Own Equipment: Cash Flow Impact?

You may want to see also

Explore related products

![]()

Penalties for Non-Compliance: Consequences of failing to report rent payments on 1099-MISC forms

Failing to report rent payments on 1099-MISC forms can trigger a cascade of penalties, each escalating in severity based on the IRS’s perception of intent and timing. For individuals or businesses paying rent to a property owner or manager, the requirement to file a 1099-MISC arises when payments exceed $600 in a tax year. Non-compliance isn’t merely an oversight—it’s a violation of tax regulations that can result in financial penalties, legal repercussions, and long-term damage to your financial reputation.

The IRS imposes penalties for late or missing 1099-MISC filings on a per-form basis. As of 2023, penalties range from $60 to $630 per form, depending on how late the filing is and whether the delay is deemed intentional. For example, filing within 30 days of the deadline incurs a $60 penalty per form, while waiting more than August 1 increases the penalty to $630 per form. Small landlords or businesses with multiple tenants could face staggering fines if they neglect this requirement. Additionally, if the IRS determines the failure to file was intentional, penalties can soar to $630 per form with no maximum limit, plus potential criminal charges for tax evasion.

Beyond immediate financial penalties, non-compliance can trigger IRS audits, which are time-consuming and costly. During an audit, the IRS scrutinizes not only the missing 1099-MISC forms but also other aspects of your financial records. This can lead to additional penalties for discrepancies unrelated to rent payments. For businesses, audits can disrupt operations and strain relationships with vendors or tenants. For individuals, audits can result in personal liability, especially if the IRS suspects fraud or negligence.

A lesser-known consequence of non-compliance is the impact on the recipient’s tax situation. When a landlord or property manager fails to receive a 1099-MISC, they may underreport income, leading to penalties of their own. This creates a ripple effect, as the IRS may pursue both parties involved in the transaction. To avoid this, proactive communication with recipients is essential. For instance, ensure you have accurate taxpayer identification numbers (TINs) for all payees and file corrections promptly if errors occur.

Practical steps to mitigate risks include maintaining detailed records of all rent payments, using tax software to automate 1099-MISC filings, and consulting a tax professional if unsure about requirements. For those managing multiple properties, consider setting calendar reminders for January deadlines and allocating funds for potential penalties in your budget. While compliance may seem burdensome, the consequences of non-compliance far outweigh the effort required to file accurately and on time.

Cut the Cord: How to Watch Cable Without Renting a Cable Box

You may want to see also

Frequently asked questions

A 1099-MISC form for rent paid is a tax document used to report payments made to a landlord or property manager if the total rent paid during the year exceeds $600. It is filed with the IRS to ensure proper reporting of income.

Individuals or businesses that pay $600 or more in rent to a landlord or property manager during the tax year are required to file a 1099-MISC form. This typically applies to tenants or property managers acting on behalf of tenants.

Yes, if you paid $600 or more in rent to a real estate company or property management firm, you must issue a 1099-MISC form, as these entities are considered independent contractors for tax purposes.

The form requires the landlord’s name, address, and taxpayer identification number (TIN or SSN), along with the total amount of rent paid during the year. The payer’s information is also needed.

The deadline to provide a copy of the 1099-MISC to the landlord is January 31st, and the form must be filed with the IRS by the end of February (paper filing) or March 31st (electronic filing).