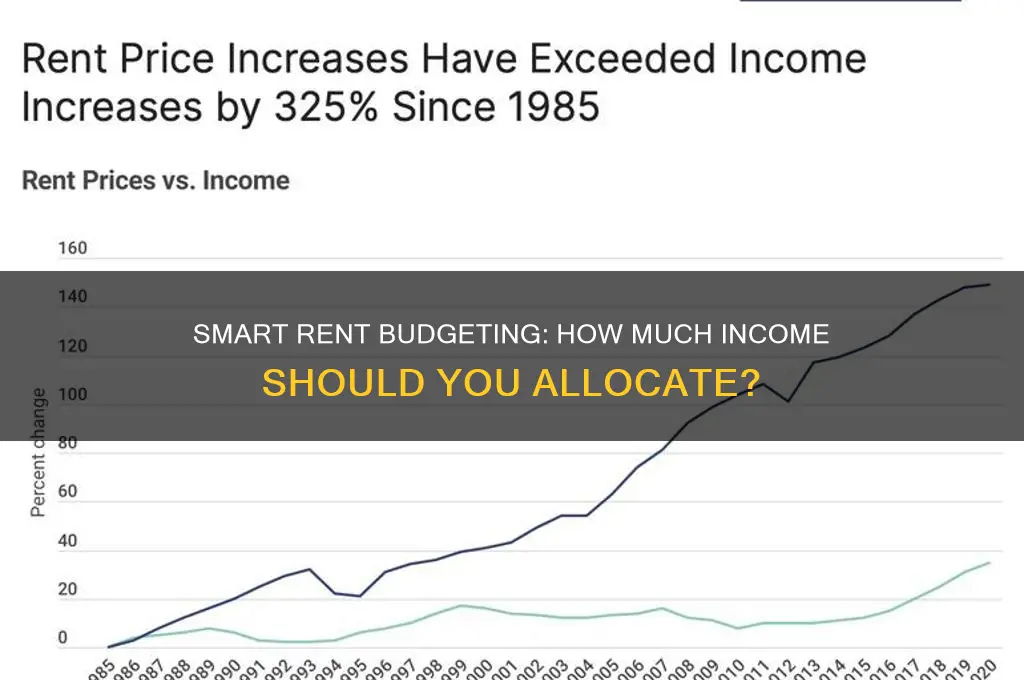

Determining the appropriate amount of income to spend on rent is a critical financial decision that balances affordability, lifestyle, and long-term financial health. A widely accepted rule of thumb is the 30% rule, which suggests allocating no more than 30% of your gross monthly income to housing costs. However, this guideline may vary based on individual circumstances, such as location, income level, and personal financial goals. High-cost urban areas often require a larger portion of income for rent, while those with lower incomes may need to prioritize essential expenses over housing. Additionally, factors like savings, debt repayment, and other living expenses must be considered to ensure financial stability and avoid overextending oneself. Ultimately, finding the right balance requires careful budgeting and a clear understanding of one’s financial priorities.

Explore related products

What You'll Learn

- Budgeting Basics: Allocate 30% of income for rent to maintain financial stability and cover other expenses

- Location Impact: Rent costs vary by city; adjust spending based on local housing market rates

- Income Fluctuations: Plan for variable income by saving extra during high-earning months for rent

- Shared Housing: Splitting rent with roommates reduces individual costs, freeing up income for savings

- Rent vs. Own: Compare renting costs to mortgage payments to determine the better financial choice

![]()

Budgeting Basics: Allocate 30% of income for rent to maintain financial stability and cover other expenses

A common rule of thumb in personal finance is the 30% rule, which suggests allocating no more than 30% of your gross income to housing costs, primarily rent. This guideline, often cited by financial advisors and housing experts, serves as a benchmark for maintaining financial stability. By capping rent at 30%, individuals can ensure they have sufficient funds for other essential expenses, such as utilities, groceries, transportation, and savings. For example, if your monthly income is $4,000, your rent should ideally not exceed $1,200. This simple calculation provides a clear starting point for budgeting, helping you avoid the pitfalls of overspending on housing.

However, the 30% rule is not one-size-fits-all. It’s a general guideline that may need adjustment based on individual circumstances. For instance, someone living in a high-cost urban area like New York City or San Francisco might find it impractical to adhere strictly to this rule due to skyrocketing rental prices. In such cases, it’s essential to prioritize needs over wants and consider alternatives like roommates or smaller living spaces. Conversely, individuals in lower-cost regions may allocate less than 30% to rent, freeing up funds for savings, investments, or debt repayment. The key is to use the 30% rule as a flexible framework rather than a rigid mandate.

To implement the 30% rule effectively, start by calculating your gross monthly income and multiplying it by 0.30. Compare this figure to your current or prospective rent. If your rent exceeds this amount, evaluate your budget to identify areas where you can cut back or explore more affordable housing options. Additionally, consider your financial goals. Are you saving for a home, paying off student loans, or building an emergency fund? Adjusting your rent allocation to align with these priorities can provide a more tailored approach to budgeting. For example, if you’re aggressively saving for a down payment, you might aim to spend 25% on rent instead of 30%.

Critics of the 30% rule argue that it doesn’t account for variations in income levels or regional cost of living. For low-income earners, even 30% may be unsustainable, leaving little room for other necessities. In contrast, high-income individuals might comfortably spend more than 30% without compromising financial stability. To address these limitations, supplement the rule with a holistic budget that includes all expenses and savings goals. Tools like budgeting apps or spreadsheets can help track spending and ensure you’re staying within your means. The 30% rule is a starting point, not the final word, in crafting a budget that works for your unique situation.

Ultimately, the 30% rule is a practical tool for achieving financial balance, but its success depends on how you adapt it to your life. Regularly review your budget to ensure your rent allocation aligns with your income, expenses, and goals. If circumstances change—such as a job loss, raise, or relocation—reassess your housing costs accordingly. By treating the 30% rule as a dynamic guideline rather than a fixed law, you can maintain financial stability while still pursuing your long-term aspirations. Remember, the goal isn’t just to afford rent but to build a sustainable financial future.

Calculating Rent per Square Foot in Lima, Ohio: A Practical Guide

You may want to see also

Explore related products

![]()

Location Impact: Rent costs vary by city; adjust spending based on local housing market rates

Rent in San Francisco consumes nearly 45% of the average income, while in Detroit, it’s closer to 25%. This stark disparity underscores the critical role location plays in determining how much of your paycheck goes toward housing. Before committing to a rent amount, research local market rates using tools like Zillow, RentJungle, or city-specific housing reports. Understanding the median rent for your desired neighborhood ensures you’re not overpaying or underestimating costs.

A common rule of thumb is the 30% rule—spending no more than 30% of your gross income on rent. However, this guideline often falls flat in high-cost cities like New York or Los Angeles, where rents routinely exceed 40% of income. In such markets, consider adjusting your expectations by prioritizing affordability over amenities or exploring roommate situations to split costs. Conversely, in lower-cost areas, aim to stay below 25% to free up funds for savings or investments.

For instance, a $60,000 annual income translates to $1,500 monthly (30% rule). In Austin, Texas, this comfortably covers a one-bedroom apartment, but in Boston, it may only secure a studio. To bridge this gap, factor in local cost-of-living indices, which account for housing, groceries, and transportation. Websites like Numbeo or the Economic Policy Institute’s Family Budget Calculator provide city-specific data to refine your budget.

If relocating for work, negotiate relocation packages or housing stipends, especially if moving to a high-cost area. Employers in competitive markets often offer such benefits to offset living expenses. Additionally, consider government housing assistance programs or rent-controlled units in cities like San Francisco or New York, which can significantly reduce financial strain.

Ultimately, location isn’t just a factor—it’s the deciding factor in how much rent you can afford. Tailor your budget to the local market, not a one-size-fits-all rule. By aligning your spending with regional realities, you’ll avoid financial overextension and maintain a sustainable lifestyle, regardless of where you call home.

Master Port Forwarding on Your Rented Router: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Income Fluctuations: Plan for variable income by saving extra during high-earning months for rent

Income variability can turn budgeting into a high-wire act, especially when rent demands a fixed chunk of your earnings. For freelancers, gig workers, or anyone with seasonal income, the 30% rent-to-income rule feels like a luxury. Instead of chasing a static percentage, adopt a dynamic approach: treat high-earning months as opportunities to fund future housing costs. During peak periods, allocate 50% of your surplus income (after essentials and savings) to a dedicated "rent reserve." This buffer ensures stability during lean months, when your rent-to-income ratio might temporarily spike to 40% or higher.

Consider a scenario: A graphic designer earns $6,000 in December but only $2,000 in July. By saving $1,500 from December’s surplus, they cover July’s $1,200 rent without dipping into emergency funds or accruing debt. This method decouples rent anxiety from income unpredictability, turning variability into a strategic advantage.

However, this strategy requires discipline and foresight. First, calculate your annual average income and total rent costs. Divide the latter by 12 to determine your monthly rent obligation. Next, during high-earning months, automate transfers to a separate rent savings account. Avoid treating this fund as discretionary; it’s not for vacations or impulse buys. Finally, resist the temptation to overspend during prosperous periods. Maintain a baseline lifestyle to maximize savings for future obligations.

Critics might argue this approach prioritizes rent over other financial goals, like investing or debt repayment. While valid, housing instability undermines progress in other areas. A missed rent payment can trigger late fees, credit damage, or eviction, derailing long-term plans. By securing housing first, you create a foundation for pursuing other objectives.

In practice, pair this strategy with a zero-based budget to track every dollar. Use apps like YNAB or spreadsheets to visualize income fluctuations and allocate funds efficiently. For those with extreme variability, consider setting aside 6–8 months’ worth of rent during peak earning periods. This extended buffer accommodates prolonged downturns, ensuring peace of mind regardless of income swings.

Ultimately, saving extra during high-earning months transforms rent from a liability into a manageable expense. It’s not about spending a fixed percentage of income but about leveraging variability to build resilience. By planning ahead, you turn unpredictability into a tool for financial security.

Sailing on a Budget: Is Renting a Sailboat Costly?

You may want to see also

Explore related products

![]()

Shared Housing: Splitting rent with roommates reduces individual costs, freeing up income for savings

Rent should ideally consume no more than 30% of your monthly income, a guideline echoed by financial experts and housing authorities alike. However, in high-cost urban areas, this threshold can be difficult to maintain, often forcing individuals to allocate closer to 50% of their earnings to housing. Shared housing emerges as a practical solution, allowing roommates to split rent and utilities, effectively reducing each person’s financial burden. For example, a $2,000 monthly rent divided among four roommates lowers the individual cost to $500, freeing up income for savings, investments, or other expenses.

Consider the math: if you earn $4,000 per month, the 30% rule suggests capping rent at $1,200. In a shared housing scenario, even a $1,600 apartment split with one roommate keeps your share at $800, well within the recommended limit. This not only eases financial stress but also creates room for building an emergency fund or paying off debt. For younger adults or those in entry-level positions, shared housing can be particularly transformative, enabling them to live in desirable locations without sacrificing financial stability.

However, successful shared housing requires more than just splitting costs. Clear communication and boundaries are essential. Draft a roommate agreement outlining responsibilities for rent, utilities, and chores. Apps like Splitwise can simplify expense tracking, ensuring fairness and transparency. Additionally, choose roommates whose lifestyles align with yours to minimize conflicts. For instance, if you prioritize quiet evenings, avoid pairing with someone who frequently hosts late-night gatherings.

Critics argue that shared housing sacrifices privacy and independence, but the financial benefits often outweigh these drawbacks. For those prioritizing savings or debt repayment, the trade-off is worthwhile. Moreover, shared housing fosters community and shared resources, such as communal groceries or streaming services, further stretching your budget. A 2022 study found that individuals in shared housing saved an average of 20% more per month compared to solo renters, highlighting its effectiveness as a financial strategy.

In conclusion, shared housing isn’t just a temporary fix for high rent—it’s a strategic approach to managing income allocation. By splitting costs with roommates, you can adhere to the 30% rent rule, even in expensive markets, while freeing up funds for long-term financial goals. With careful planning and the right roommates, shared housing becomes more than cost-sharing; it’s a pathway to greater financial freedom.

Is This Neighborhood Right for Renters? Key Signs to Look For

You may want to see also

Explore related products

$15.99 $15.99

![]()

Rent vs. Own: Compare renting costs to mortgage payments to determine the better financial choice

A common rule of thumb suggests spending no more than 30% of your gross income on housing, whether renting or owning. However, this guideline often oversimplifies a complex decision. Renting typically offers flexibility and lower upfront costs, while owning a home builds equity and provides long-term financial benefits. To determine the better financial choice, compare not just monthly payments but also hidden costs, tax advantages, and long-term wealth accumulation.

Step 1: Calculate Total Monthly Costs

For renters, this includes rent, utilities, and renter’s insurance. For homeowners, factor in the mortgage payment, property taxes, homeowners insurance, maintenance (1–4% of the home’s value annually), and HOA fees if applicable. Example: A $2,000 monthly rent vs. a $2,200 mortgage payment might seem comparable, but adding $300 in maintenance and taxes tilts the scale.

Step 2: Assess Hidden Financial Impacts

Renting often means predictable costs and no repair surprises, but rent increases over time erode affordability. Owning locks in a fixed-rate mortgage payment, and mortgage interest and property taxes are tax-deductible (up to certain limits). Over 10 years, a homeowner might save $15,000 in taxes while a renter pays full price.

Step 3: Evaluate Long-Term Wealth Building

Renting offers no equity, but owning builds wealth through property appreciation and principal payments. Historically, home values rise 3–4% annually, turning a $300,000 home into $400,000 in 15 years. However, this assumes staying put; frequent moves negate these gains.

Caution: Avoid Overlooking Opportunity Costs

A large down payment ties up cash that could earn returns elsewhere. For instance, $60,000 invested in a 7% index fund grows to $100,000 in 10 years, while the same amount in a home’s equity depends on market conditions. Renting allows flexibility to invest in higher-yield assets.

If stability, tax benefits, and long-term wealth align with your priorities, owning may outweigh renting’s flexibility. Conversely, if mobility, simplicity, and investing in markets appeal more, renting remains financially prudent. Use a rent vs. buy calculator to model scenarios specific to your income, location, and timeline.

Rent Expenses: Taxable Income for C Corporations?

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent. This helps ensure you have enough left for other expenses and savings.

While the 30% rule is a guideline, it may be necessary to exceed it in high-cost areas. However, aim to keep rent as close to 30% as possible to avoid financial strain. Consider budgeting carefully or finding a roommate to share costs.

If your rent is already above 30%, prioritize reducing other discretionary expenses, increasing your income, or finding more affordable housing. Long-term, exceeding this threshold can limit your ability to save and cover unexpected costs.