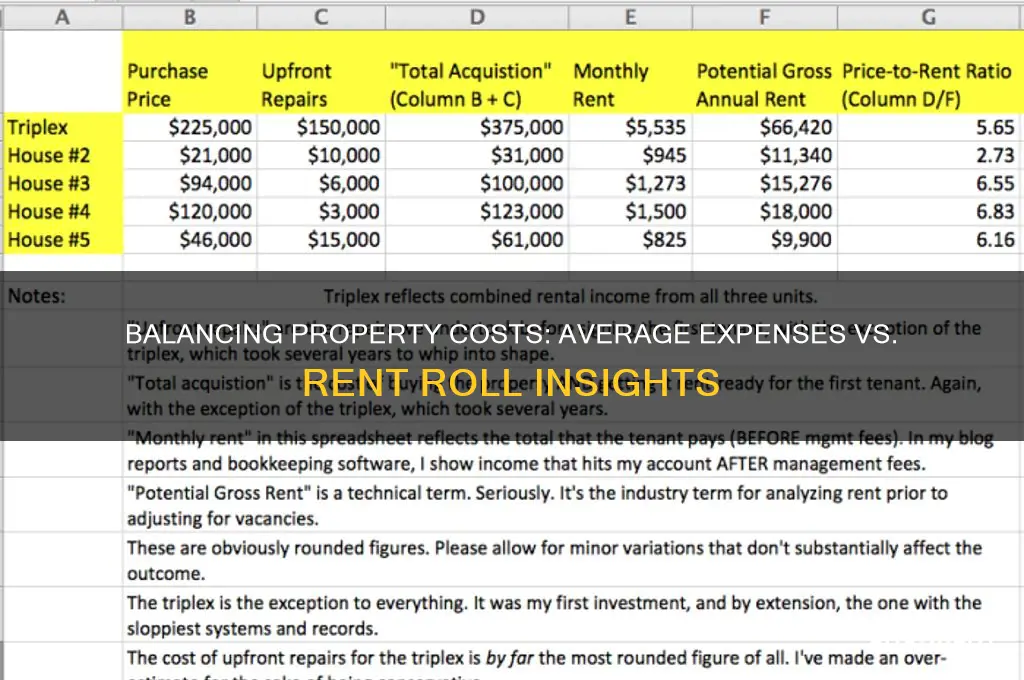

When analyzing property investments, understanding the relationship between average expenses and rent roll is crucial for assessing financial viability. The rent roll represents the total income generated from tenant leases, while average expenses encompass ongoing costs such as maintenance, property management, taxes, insurance, and utilities. Comparing these two metrics provides insight into the property's operational efficiency and profitability. A healthy balance occurs when rent roll significantly exceeds average expenses, ensuring sufficient cash flow for reinvestment and contingencies. Conversely, if expenses approach or surpass rental income, it may indicate financial strain or mismanagement. This analysis is essential for landlords, investors, and property managers to make informed decisions, optimize budgets, and maximize returns on their real estate assets.

Explore related products

What You'll Learn

- Rent-to-Income Ratios: Comparing tenant income to rent costs for affordability analysis

- Expense Ratios: Analyzing property operating expenses as a percentage of rental income

- Market Benchmarks: Comparing expenses and rent across similar properties in the same market

- Profit Margins: Calculating net income after expenses relative to total rent collected

- Cost Trends: Tracking changes in expenses and rent over time for financial planning

![]()

Rent-to-Income Ratios: Comparing tenant income to rent costs for affordability analysis

A common rule of thumb in rental affordability is the 30% rent-to-income ratio, suggesting tenants should spend no more than 30% of their gross monthly income on rent. This benchmark, however, often fails to account for regional variations in living costs, income disparities, and other financial obligations. For instance, in high-cost urban areas like San Francisco or New York, tenants frequently exceed this threshold, allocating closer to 40-50% of their income to housing. Conversely, in more affordable regions, such as the Midwest, tenants may comfortably stay below 25%. This disparity highlights the need for a more nuanced approach to affordability analysis.

To accurately assess rent affordability, landlords and property managers should consider the 50/30/20 budgeting rule as a complementary framework. This rule suggests allocating 50% of income to necessities (including rent), 30% to discretionary spending, and 20% to savings or debt repayment. By comparing a tenant’s rent to their overall budget, rather than income alone, landlords can better gauge financial stability. For example, a tenant earning $4,000 monthly with $1,200 in rent (30%) might still struggle if their remaining necessities (e.g., utilities, groceries) push their total essential expenses above 50%. This layered analysis provides a clearer picture of affordability.

When implementing rent-to-income ratios, it’s crucial to verify tenant income through pay stubs, tax returns, or bank statements. A common mistake is relying solely on self-reported income, which can be inflated. Additionally, consider offering flexibility for tenants with non-traditional income sources, such as freelancers or gig workers, by averaging their earnings over several months. For instance, a freelancer with fluctuating monthly income might provide a 6-month average to demonstrate consistent affordability. This approach ensures fairness while maintaining financial security for landlords.

Finally, while rent-to-income ratios are a valuable tool, they should not be the sole criterion for tenant selection. Factors like credit history, rental references, and savings can provide additional insights into a tenant’s financial reliability. For example, a tenant with a 35% rent-to-income ratio but a strong credit score and emergency fund may pose less risk than one at 28% with a history of late payments. By balancing quantitative metrics with qualitative assessments, landlords can make more informed decisions, fostering stable and mutually beneficial rental relationships.

Renters Insurance: Proof of Rent Needed?

You may want to see also

Explore related products

![]()

Expense Ratios: Analyzing property operating expenses as a percentage of rental income

Property owners and managers often gauge financial health by comparing operating expenses to rental income, a metric known as the expense ratio. This ratio, expressed as a percentage, reveals how much of the rental income is consumed by expenses like maintenance, property management, taxes, and insurance. For instance, a property generating $120,000 in annual rent with $48,000 in operating expenses has a 40% expense ratio. Industry benchmarks suggest that well-managed properties typically maintain ratios between 30% and 50%, though this varies by property type, location, and age. Understanding this metric is crucial for identifying inefficiencies, setting competitive rents, and forecasting cash flow.

Analyzing expense ratios requires a granular breakdown of costs. Start by categorizing expenses into fixed (e.g., property taxes, insurance) and variable (e.g., repairs, utilities). For example, older properties may have higher maintenance costs, while luxury rentals might incur elevated management fees. Compare these categories to industry averages—property taxes typically account for 2% to 4% of rental income, while maintenance can range from 5% to 15%. Identifying outliers in your expense breakdown allows for targeted cost-cutting or reinvestment strategies. For instance, if utility costs exceed 10% of rental income, consider energy-efficient upgrades to reduce long-term expenses.

A persuasive argument for monitoring expense ratios is their role in maximizing profitability and property value. High ratios signal inefficiencies or overpricing of services, while unusually low ratios may indicate deferred maintenance or underinvestment in the property. For investors, a consistently low expense ratio can enhance a property’s attractiveness, as it suggests higher net operating income (NOI) and, consequently, a stronger return on investment. Conversely, landlords with high ratios may need to renegotiate service contracts, adjust rent prices, or explore refinancing options to improve financial performance.

To effectively use expense ratios, benchmark your property against comparable assets in the same market. For example, multifamily properties in urban areas often have higher management fees (up to 10% of rent) due to increased tenant turnover and maintenance demands, while single-family rentals in suburban areas may operate at lower ratios (around 35%). Tools like the Institute of Real Estate Management’s (IREM) expense analysis reports can provide regional and property-type-specific benchmarks. Regularly updating your expense ratio analysis ensures alignment with market trends and helps in making data-driven decisions to optimize rental property performance.

Renting a Cabin in Katmai: A Step-by-Step Guide for Adventurers

You may want to see also

Explore related products

![]()

Market Benchmarks: Comparing expenses and rent across similar properties in the same market

Understanding market benchmarks is crucial for property owners and managers aiming to optimize their financial performance. By comparing expenses and rent across similar properties in the same market, stakeholders can identify inefficiencies, set competitive rental rates, and ensure their operations align with industry standards. For instance, in multifamily housing, the average expense ratio (total operating expenses divided by effective gross income) typically ranges between 35% and 45%. Properties falling outside this range may warrant a closer examination of cost structures or rental pricing strategies.

To effectively benchmark, start by identifying comparable properties—those with similar size, location, tenant demographics, and amenities. Utilize tools like CoStar, RentMeter, or local real estate associations to gather data on rent rolls and operating expenses. Focus on key expense categories such as maintenance, property management fees, utilities, and taxes. For example, in urban markets, utilities might account for 10–15% of total expenses, while in suburban areas, landscaping could be a more significant cost driver. Analyzing these breakdowns provides actionable insights into where your property stands relative to peers.

A persuasive argument for benchmarking lies in its ability to uncover hidden opportunities. Suppose a property’s maintenance costs are 20% higher than the market average. This could signal overstaffing, inefficient vendor contracts, or deferred maintenance issues. Conversely, if rent is 10% below comparable properties, it may indicate underpricing or a need for upgrades to justify higher rates. Benchmarking not only highlights these discrepancies but also empowers owners to make data-driven decisions to improve profitability.

However, benchmarking is not without its cautions. Market averages are just that—averages. Unique property characteristics, such as age, condition, or tenant turnover rates, can skew comparisons. For instance, a newer property might have lower maintenance costs but higher mortgage payments, while an older building may face higher repair expenses but lower property taxes. Additionally, short-term market fluctuations, like seasonal demand or economic downturns, can temporarily distort benchmarks. Always contextualize data with these factors to avoid misguided conclusions.

In conclusion, market benchmarks serve as a critical tool for aligning expenses and rent with industry norms. By systematically comparing data, property managers can identify areas for improvement, justify pricing strategies, and enhance overall financial health. While benchmarks provide valuable insights, they should be interpreted thoughtfully, considering the unique attributes of each property. Regularly updating and refining these comparisons ensures long-term competitiveness in a dynamic real estate market.

Is Pressure Washing a Renter's Duty or Landlord's Responsibility?

You may want to see also

Explore related products

![]()

Profit Margins: Calculating net income after expenses relative to total rent collected

Understanding profit margins in rental properties hinges on the relationship between net income and total rent collected. To calculate this, subtract all expenses—maintenance, property management fees, taxes, insurance, and vacancies—from the gross rent. The result is your net income. Divide this figure by the total rent collected and multiply by 100 to get the profit margin percentage. For instance, if your net income is $24,000 on a $36,000 rent roll, your profit margin is 66.67%. This metric is critical for assessing financial health and comparing performance across properties or markets.

Expenses typically consume 30–50% of the total rent roll, depending on factors like property age, location, and management efficiency. Newer properties in low-maintenance areas may lean toward the 30% mark, while older buildings in high-demand urban zones might approach 50%. To optimize margins, scrutinize variable costs like repairs and vacancies. For example, proactive maintenance can reduce emergency repairs, and offering lease renewals can minimize vacancy rates. Tracking these expenses monthly allows for timely adjustments and ensures your profit margin remains competitive.

A persuasive argument for prioritizing profit margin analysis is its role in long-term investment strategy. High rent collection doesn’t guarantee profitability if expenses are unchecked. Consider a property with a $50,000 rent roll but $30,000 in expenses versus one with a $40,000 rent roll and $15,000 in expenses. The latter yields a 62.5% profit margin, significantly outperforming the former’s 40%. Investors should focus on expense management as much as rent optimization to maximize returns. Tools like expense-tracking software or hiring a property manager can streamline this process.

Comparatively, profit margins in rental properties often lag behind other industries due to fixed costs like property taxes and insurance. However, real estate offers stability and appreciation potential, making modest margins acceptable for long-term investors. For instance, a 40–50% profit margin is considered healthy in multifamily rentals, while single-family homes might achieve 50–60%. Benchmarking your margin against industry averages and local market conditions provides context for performance evaluation. If your margin falls short, analyze expense categories to identify areas for improvement.

In practice, calculating and improving profit margins requires discipline and data-driven decision-making. Start by categorizing expenses into fixed (e.g., taxes) and variable (e.g., repairs) to identify levers for optimization. Use historical data to forecast expenses and set realistic budgets. For example, if repairs averaged $2,000 annually, allocate $167 monthly to avoid cash flow disruptions. Regularly review leases to ensure rents align with market rates, and negotiate vendor contracts to reduce recurring costs. By treating profit margin as a dynamic metric, landlords can enhance financial resilience and investment returns.

How Long Do Rental Applications Remain on File? A Complete Guide

You may want to see also

Explore related products

![]()

Cost Trends: Tracking changes in expenses and rent over time for financial planning

Understanding the relationship between expenses and rent roll is crucial for effective financial planning in property management. Over time, both expenses and rental income can fluctuate due to inflation, market conditions, and operational changes. Tracking these trends allows property owners and managers to anticipate financial shifts, optimize budgets, and ensure long-term profitability. For instance, a 2023 study revealed that maintenance costs have risen by 15% over the past five years, outpacing the average 8% increase in rental income, highlighting the need for proactive cost management.

To effectively track these changes, start by categorizing expenses into fixed (e.g., property taxes, insurance) and variable (e.g., maintenance, utilities) components. Compare these against the rent roll annually, using tools like spreadsheets or property management software. For example, if variable expenses consistently exceed 30% of rental income, it may indicate inefficiencies that require addressing. Additionally, benchmark your data against industry averages—a healthy expense-to-rent ratio typically ranges between 35% and 45%, depending on property type and location.

A persuasive argument for tracking cost trends lies in their ability to inform strategic decisions. For instance, if utility expenses are rising faster than rent, consider investing in energy-efficient upgrades to reduce long-term costs. Similarly, if vacancy rates are increasing, analyze whether rent hikes are outpacing market demand. By identifying these patterns early, property managers can adjust pricing, cut unnecessary expenses, or allocate resources to high-return areas like tenant retention programs.

Comparatively, properties that fail to monitor these trends often face financial strain. A case study of a multifamily complex in 2022 showed that neglecting to track rising maintenance costs led to a 10% decrease in net operating income over two years. In contrast, a proactive approach—such as quarterly expense reviews and rent adjustments based on market data—can maintain a stable financial position. For example, a property manager who noticed a 7% increase in landscaping costs negotiated a bulk service contract, saving 12% annually.

In conclusion, tracking changes in expenses and rent over time is not just a best practice—it’s a necessity for financial resilience. By analyzing trends, benchmarking against industry standards, and making data-driven decisions, property managers can navigate economic uncertainties and maximize returns. Start today by setting up a tracking system, reviewing historical data, and creating actionable plans to address emerging cost patterns. Your future financial health depends on it.

Essential Event Rentals: What You Need for a Successful Celebration

You may want to see also

Frequently asked questions

It refers to the ratio of total operating expenses (e.g., maintenance, utilities, taxes) to the total rental income (rent roll) for a property, expressed as a percentage.

It helps landlords assess the financial efficiency of their property, ensuring expenses are manageable relative to income and identifying areas for cost reduction.

A healthy ratio is usually between 30-50%, though this varies by property type, location, and market conditions.

Landlords can reduce expenses by negotiating vendor contracts, improving energy efficiency, minimizing vacancies, and optimizing maintenance practices.