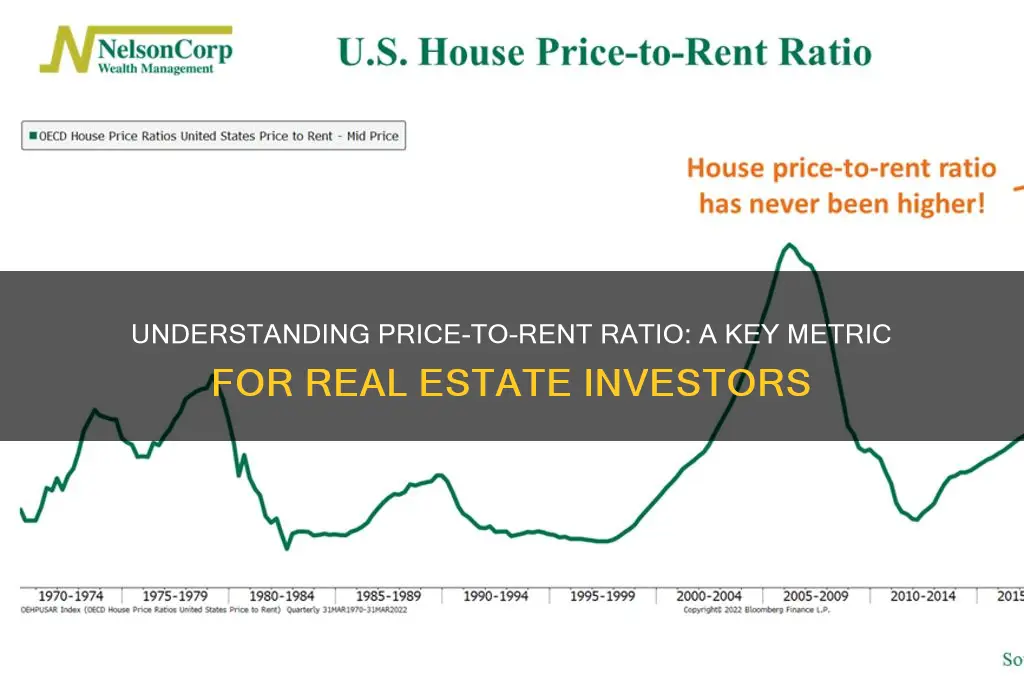

The price-to-rent ratio is a key metric used in real estate to compare the relative affordability of buying versus renting a property. It is calculated by dividing the median home price by the annual median rent in a given market. A lower ratio suggests that buying may be more cost-effective than renting, while a higher ratio indicates renting could be the better financial option. This ratio helps investors, homebuyers, and renters assess market conditions, identify potential investment opportunities, and make informed decisions about whether to enter the housing market as buyers or continue renting. Understanding the price-to-rent ratio is essential for navigating the complexities of real estate and aligning financial goals with market trends.

Explore related products

What You'll Learn

- Definition: Price to rent ratio compares property purchase cost to annual rental income

- Calculation: Divide property price by yearly rent to get the ratio

- Interpretation: Lower ratios suggest buying is better; higher favors renting

- Market Analysis: Indicates housing affordability and investment potential in a region

- Limitations: Doesn’t account for maintenance, taxes, or financing costs

![]()

Definition: Price to rent ratio compares property purchase cost to annual rental income

The price-to-rent ratio is a financial metric that distills the relationship between buying and renting a property into a single, digestible number. Calculated by dividing the property’s purchase price by its annual rental income, this ratio offers a snapshot of relative affordability. For instance, a ratio of 15 means the property’s price is 15 times its yearly rent. This figure is more than just a number—it’s a tool for comparing markets, assessing investment potential, and making informed decisions about whether to buy or rent.

Consider this scenario: In City A, a $300,000 home generates $20,000 in annual rent, yielding a price-to-rent ratio of 15. In City B, a $400,000 home rents for $25,000 annually, resulting in a ratio of 16. While City A appears more affordable on the surface, the ratio alone doesn’t tell the full story. Factors like property appreciation, maintenance costs, and local market trends must also be weighed. Still, the ratio serves as a starting point for deeper analysis, helping investors and homebuyers prioritize opportunities.

To calculate the price-to-rent ratio, follow these steps: First, determine the property’s purchase price. Next, find its annual rental income—either through market research or existing lease agreements. Divide the purchase price by the annual rent. For example, a $250,000 property with $15,000 in yearly rent has a ratio of 16.67. Experts often consider ratios below 15 to favor buying, while ratios above 20 may indicate renting is more cost-effective. However, these thresholds aren’t universal—they vary by location, property type, and economic conditions.

A persuasive argument for using the price-to-rent ratio lies in its ability to demystify housing markets. In high-ratio cities like San Francisco or New York, where ratios often exceed 25, renting may be more financially prudent. Conversely, in markets with ratios closer to 12, such as parts of the Midwest, buying could offer better long-term value. This metric empowers individuals to align their housing decisions with their financial goals, whether they’re seeking stability, equity, or flexibility.

Finally, while the price-to-rent ratio is a valuable tool, it’s not without limitations. It doesn’t account for variables like property taxes, insurance, or potential rent increases. Additionally, it assumes consistent rental income, which may fluctuate in volatile markets. To maximize its utility, pair the ratio with other analyses, such as cash flow projections or comparable market studies. By doing so, you’ll gain a more holistic understanding of whether buying or renting aligns with your financial strategy.

Escape to Nature: Top Spots to Rent a Cozy Woodland Cabin

You may want to see also

Explore related products

![]()

Calculation: Divide property price by yearly rent to get the ratio

The price-to-rent ratio is a straightforward yet powerful metric for assessing whether buying or renting a property is more financially prudent. At its core, the calculation involves dividing the property’s purchase price by its annual rental income. For instance, if a home costs $300,000 and rents for $18,000 per year, the ratio is 16.67. This figure provides a snapshot of the relative affordability of buying versus renting in a given market. A lower ratio suggests buying might be more attractive, while a higher ratio leans toward renting as the better option.

To perform this calculation accurately, ensure you’re using consistent data. For the property price, rely on recent sales data or a professional appraisal, not inflated list prices. For annual rent, use the gross rental income—the total expected rent over 12 months—excluding any additional costs like maintenance or property management fees. Precision in these inputs is critical, as even small discrepancies can skew the ratio and mislead your decision-making.

While the calculation itself is simple, interpreting the result requires context. A common benchmark is a ratio of 15 to 20, often cited as the threshold where buying becomes more favorable than renting. However, this varies by location, market conditions, and personal financial goals. For example, in high-demand urban areas like San Francisco or New York, ratios frequently exceed 30, making renting the more economical choice for many. Conversely, in suburban or rural markets, ratios below 15 are common, tipping the scales toward buying.

One practical tip for using this ratio is to compare it across multiple properties or neighborhoods to identify trends. For instance, if you’re considering two homes with similar prices but vastly different rent potential, the one with the lower price-to-rent ratio may offer better long-term value. Additionally, factor in other costs like property taxes, insurance, and maintenance when making your decision, as these can significantly impact the financial viability of buying.

Finally, remember that the price-to-rent ratio is just one tool in your real estate analysis toolkit. It doesn’t account for factors like mortgage interest rates, property appreciation, or personal lifestyle preferences. Use it as a starting point, not the sole determinant. For example, if you plan to stay in a home for decades, buying might still be worthwhile even with a higher ratio, as long-term equity gains could outweigh short-term rental savings. Always pair this calculation with broader financial planning and market research.

Hollywood CA Rent Prices: Average Costs for Living in Tinseltown

You may want to see also

Explore related products

![]()

Interpretation: Lower ratios suggest buying is better; higher favors renting

The price-to-rent ratio, a key metric in real estate, compares the cost of buying a home to the cost of renting a similar property. This ratio is calculated by dividing the average home price by the average annual rent in a given area. A lower ratio indicates that buying a home is more financially advantageous compared to renting, while a higher ratio suggests the opposite. For instance, a ratio of 15 means that buying a home is equivalent to paying 15 years of rent upfront. Understanding this ratio is crucial for making informed decisions in the housing market.

Analyzing the price-to-rent ratio requires context. In cities like New York or San Francisco, where ratios often exceed 25, renting is typically more cost-effective. Conversely, in smaller towns or regions with ratios below 15, buying becomes a more attractive option. For example, if a city has an average home price of $300,000 and annual rent of $20,000, the ratio is 15, signaling a balanced market. However, if the same city’s home prices rise to $450,000, pushing the ratio to 22.5, renting becomes the better financial choice. This shift highlights how market dynamics directly impact the ratio’s interpretation.

To leverage the price-to-rent ratio effectively, consider your long-term plans. If you plan to stay in an area for less than five years, renting is often more practical, especially in high-ratio markets. For instance, in a city with a ratio of 20, buying a $400,000 home would equate to paying $20,000 in rent annually. If you move within three years, you risk losing money on closing costs, maintenance, and potential property depreciation. Conversely, in a low-ratio market (e.g., ratio of 12), buying the same priced home aligns with paying $33,333 in rent annually, making it a smarter investment for long-term residents.

A persuasive argument for using the price-to-rent ratio is its ability to reveal hidden costs. Renting in a high-ratio market may seem expensive, but it often includes flexibility and lower upfront costs. For example, a $2,500 monthly rent in a ratio-25 market is more affordable than buying a $600,000 home, which requires a $120,000 down payment, closing costs, and ongoing maintenance. Conversely, in a low-ratio market, buying locks in housing costs, protecting against rent increases. For instance, a $200,000 home in a ratio-10 market offers stability, while renting at $1,666 monthly leaves you vulnerable to rising rents.

Finally, a comparative approach underscores the ratio’s limitations. While it’s a valuable tool, it doesn’t account for personal circumstances like credit scores, job stability, or lifestyle preferences. For example, a young professional in a high-ratio city might prioritize renting for flexibility, even if buying seems cheaper on paper. Conversely, a family in a low-ratio suburb may prioritize homeownership for stability, despite higher upfront costs. Pairing the price-to-rent ratio with personal financial goals ensures a well-rounded decision, turning this metric from a mere number into a strategic guide.

Who Killed Benny's Dog? Analyzing Angel's Motives in Rent

You may want to see also

Explore related products

![]()

Market Analysis: Indicates housing affordability and investment potential in a region

The price-to-rent ratio, a key metric in real estate analysis, offers a snapshot of housing affordability and investment potential within a specific market. This ratio compares the cost of purchasing a property to the annual cost of renting a similar one, providing valuable insights for both homebuyers and investors. A low ratio suggests that buying might be more financially attractive than renting, indicating a potentially affordable market for purchasers. Conversely, a high ratio implies that renting could be the more economical choice, signaling a market where investment opportunities may be less favorable.

Analyzing Affordability: In regions with a price-to-rent ratio below 15, housing is generally considered affordable for buyers. For instance, in the Midwest, cities like Cleveland and Detroit often exhibit ratios around 10, making homeownership an accessible option for many residents. This affordability can stimulate local economies as homeowners tend to invest in their properties and communities. However, it's crucial to consider other factors like local income levels and employment rates to fully understand the market dynamics.

Investment Strategies: Investors can utilize the price-to-rent ratio to identify markets with strong rental demand and potential for property value appreciation. A ratio above 20 might indicate a market where renting is prevalent, and buying for investment purposes could be risky. For example, in popular urban centers like New York or San Francisco, high ratios often correlate with a robust rental market but may also signify a challenging environment for investors due to intense competition and high entry costs.

Regional Variations and Trends: Market analysis reveals that price-to-rent ratios vary significantly across regions, influenced by local economic conditions, population growth, and housing supply. In rapidly growing cities, the ratio may increase over time as demand outpaces supply, making it a critical indicator for both short-term and long-term investment strategies. For instance, a comparison between Austin, Texas, and Seattle, Washington, shows how different growth patterns can lead to distinct price-to-rent trajectories, affecting investment decisions.

Practical Application: To effectively use the price-to-rent ratio, investors and homebuyers should track this metric over time, noting trends and anomalies. Combining this data with other market indicators, such as vacancy rates and local economic forecasts, provides a comprehensive view of a region's housing market. For instance, a sudden spike in the ratio could signal a bubble or a shift in market dynamics, prompting further investigation before making significant financial commitments. This approach ensures a more informed decision-making process, whether for personal homeownership or real estate investment.

Scuba Certification Requirements: Do You Need It to Rent Gear?

You may want to see also

Explore related products

![]()

Limitations: Doesn’t account for maintenance, taxes, or financing costs

The price-to-rent ratio, a popular metric for comparing the affordability of buying versus renting a home, simplifies complex decisions into a single number. However, its simplicity comes at a cost: it ignores critical expenses that significantly impact the true cost of homeownership. Maintenance, taxes, and financing costs are not factored into this ratio, which can lead to misleading conclusions about the financial viability of buying a property.

Consider maintenance costs, which can vary widely depending on the age and condition of a property. A newer home might require minimal upkeep, but an older one could demand thousands of dollars annually for repairs, renovations, or replacements. For instance, a 30-year-old roof might need replacement within the next decade, costing upwards of $10,000. Similarly, HVAC systems, plumbing, and electrical systems degrade over time, necessitating repairs or upgrades. The price-to-rent ratio fails to account for these unpredictable but substantial expenses, painting an incomplete picture of homeownership costs.

Taxes are another significant omission. Property taxes vary by location and can add thousands of dollars to annual expenses. For example, in high-tax states like New Jersey or Illinois, property taxes can exceed 2% of a home’s value annually. A $300,000 home in such areas could incur $6,000 or more in taxes each year—an expense entirely absent from the price-to-rent calculation. This oversight can make buying appear more attractive than it truly is, especially when compared to renting, where taxes are typically included in the rent.

Financing costs further complicate the equation. Mortgage interest, closing costs, and private mortgage insurance (PMI) are substantial expenses that the price-to-rent ratio ignores. For a $300,000 home with a 20% down payment, a 30-year mortgage at 6% interest would result in over $370,000 in interest payments alone. Add closing costs, which average 2-5% of the home’s price, and PMI for down payments under 20%, and the financial burden grows significantly. These costs are absent from the ratio, making renting seem less competitive than it might be when all expenses are considered.

To use the price-to-rent ratio effectively, it’s essential to supplement it with a detailed analysis of these omitted costs. Prospective buyers should estimate annual maintenance expenses based on the property’s condition, research local property tax rates, and calculate total financing costs over the life of the mortgage. For example, creating a spreadsheet that includes these expenses alongside the ratio can provide a more accurate comparison. While the price-to-rent ratio is a useful starting point, it should not be the sole determinant of whether to buy or rent. By accounting for maintenance, taxes, and financing costs, individuals can make more informed decisions that reflect the true financial realities of homeownership.

Verify Your Landlord: Essential Tips to Rent Safely and Securely

You may want to see also

Frequently asked questions

The Price to Rent Ratio compares the cost of purchasing a home to the cost of renting a similar property in the same area. It helps determine whether buying or renting is more financially advantageous.

The ratio is calculated by dividing the median home price by the annual rent for a similar property. For example, if the median home price is $300,000 and the annual rent is $18,000, the ratio is 16.67.

A ratio below 15 is generally considered favorable for buying, while a ratio above 20 suggests renting may be more cost-effective. However, this can vary by location and market conditions.

Investors use the ratio to assess the relative value of buying versus renting in a market. A lower ratio indicates better affordability for buyers, while a higher ratio may signal an overpriced housing market.

Yes, the ratio can differ significantly by city, region, or country due to factors like housing demand, rental market conditions, and local economic trends. It’s important to analyze the ratio within the specific context of the area.