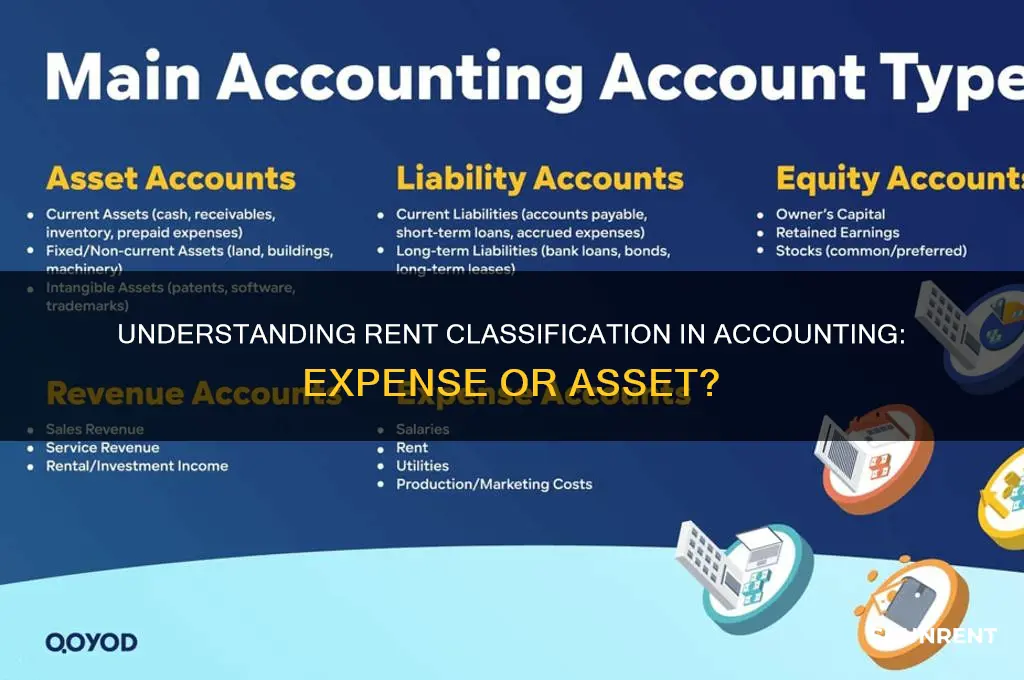

In accounting, rent typically falls under the category of operating expenses, specifically within the income statement. It is considered a day-to-day expense incurred by a business for the use of property, such as office space, retail locations, or equipment, and is essential for the ongoing operations of the company. Rent is usually recorded as a debit to the rent expense account and a credit to the accounts payable or cash account, depending on the payment method. Proper classification and recording of rent expenses are crucial for accurate financial reporting, as they directly impact a company's profitability, cash flow, and overall financial health. Understanding how rent is treated in accounting is vital for businesses to maintain compliance with accounting standards and make informed financial decisions.

| Characteristics | Values |

|---|---|

| Type of Expense | Operating Expense |

| Accounting Classification | Typically recorded as a Selling, General, and Administrative (SG&A) expense on the income statement. |

| Nature | A fixed cost (usually) that remains constant regardless of production or sales volume. |

| Payment Frequency | Usually paid periodically (monthly, quarterly, annually) as per the lease agreement. |

| Accounting Treatment | Recognized as an expense in the period incurred (accrual basis) or when paid (cash basis). |

| Prepaid Rent | If rent is paid in advance, it's recorded as a prepaid asset and amortized over the rental period. |

| Lease Accounting (ASC 842) | For leases meeting specific criteria, rent may be capitalized as a right-of-use asset and a lease liability on the balance sheet. |

| Tax Treatment | Generally tax-deductible as a business expense. |

Explore related products

What You'll Learn

- Expense Classification: Rent is categorized as an operating expense in the income statement

- Lease Accounting: Rent under leases follows ASC 842 or IFRS 16 standards

- Prepaid Rent: Advance payments are recorded as a current asset

- Tax Deductibility: Rent is often tax-deductible for businesses as an expense

- Cash Flow Impact: Rent payments are reported under operating activities in cash flow statements

![]()

Expense Classification: Rent is categorized as an operating expense in the income statement

Rent, a ubiquitous cost for businesses occupying physical spaces, is classified as an operating expense in the income statement. This categorization stems from its direct association with the day-to-day operations of a business. Unlike capital expenditures, which involve long-term investments in assets, rent represents a recurring cost necessary for maintaining a functional workspace. Whether it’s an office, retail store, or warehouse, the payment of rent is essential for the business to operate, making it a core component of operating expenses.

From an accounting perspective, the classification of rent as an operating expense is straightforward. It is recorded in the income statement under the "Operating Expenses" section, typically alongside other costs like utilities, salaries, and supplies. This grouping provides a clear picture of the expenses directly tied to generating revenue. For instance, a retail business’s rent for its storefront is directly linked to its ability to sell products, making it an operational necessity rather than a discretionary cost.

One practical tip for businesses is to ensure rent payments are accurately recorded on an accrual basis, especially if rent is paid in advance or in arrears. This means recognizing the expense in the period it is incurred, not when it is paid. For example, if a business pays $12,000 in annual rent upfront in January, it should allocate $1,000 per month as an operating expense throughout the year. This approach aligns with accounting principles like matching revenue with expenses, providing a more accurate financial snapshot.

Comparatively, rent differs from other expenses like depreciation or interest, which are often classified separately. Depreciation, for instance, reflects the wear and tear of owned assets, while interest pertains to financing costs. Rent, however, is purely operational and does not involve ownership or financing. This distinction is crucial for financial analysis, as it helps stakeholders understand the true cost of running the business versus investing in long-term assets or managing debt.

In conclusion, categorizing rent as an operating expense is both logical and practical. It reflects the expense’s direct role in supporting business operations and ensures consistency in financial reporting. By adhering to this classification, businesses can maintain transparency, facilitate accurate analysis, and make informed decisions based on a clear understanding of their operational costs.

PP&E: Should You Include Rented Buildings?

You may want to see also

Explore related products

![]()

Lease Accounting: Rent under leases follows ASC 842 or IFRS 16 standards

Rent, when structured as a lease, falls under specific accounting standards that dictate how it should be recognized, measured, and disclosed. In the United States, ASC 842 (Accounting Standards Codification 842) governs lease accounting, while globally, IFRS 16 (International Financial Reporting Standard 16) sets the framework. These standards eliminate the distinction between operating and capital leases for lessees, requiring virtually all leases to be capitalized on the balance sheet. This shift ensures greater transparency and comparability across financial statements.

Under ASC 842 and IFRS 16, lessees recognize a right-of-use (ROU) asset and a lease liability for most leases. The ROU asset represents the lessee’s right to use the leased asset over the lease term, while the lease liability reflects the obligation to make lease payments. Rent payments are bifurcated into principal and interest components, with the principal reducing the liability and the interest recognized as an expense over time. This approach aligns lease accounting with the principles of accrual accounting, providing a more accurate depiction of a company’s financial position and obligations.

For example, consider a company leasing office space for 10 years with annual rent of $100,000. At inception, the lessee records an ROU asset and a lease liability equal to the present value of the lease payments, discounted using the incremental borrowing rate. As rent is paid, the lease liability decreases, and the ROU asset is depreciated over the lease term. This treatment contrasts with pre-ASC 842 and IFRS 16 practices, where operating leases were often expensed as incurred, leaving significant liabilities off the balance sheet.

One critical aspect of these standards is the lease term determination, which includes both the non-cancellable period and options to extend or terminate the lease if they are reasonably certain to be exercised. This assessment requires judgment and can significantly impact the magnitude of the ROU asset and lease liability. Additionally, lessees must reassess lease terms and discount rates periodically, adjusting the ROU asset and liability accordingly.

In practice, implementing ASC 842 or IFRS 16 requires careful planning and robust systems. Companies should conduct a comprehensive lease inventory, analyze lease contracts for embedded terms, and calculate present values accurately. Tools like lease accounting software can streamline these processes, ensuring compliance and reducing the risk of errors. By adhering to these standards, businesses not only meet regulatory requirements but also enhance the reliability and comparability of their financial reporting.

Renting and Discovering Mold: Essential Steps to Protect Your Health

You may want to see also

Explore related products

![]()

Prepaid Rent: Advance payments are recorded as a current asset

Rent, in accounting, is typically classified as an expense when it is incurred. However, when rent is paid in advance, it takes on a different character. Prepaid rent occurs when a tenant pays for occupancy rights before the rental period begins. Instead of immediately expensing this payment, it is recorded as a current asset on the balance sheet. This treatment aligns with the accounting principle of matching expenses with the period in which they are incurred. For example, if a company pays $12,000 for a year’s rent in January, only $1,000 is expensed each month, while the remaining balance is held as prepaid rent.

Recording prepaid rent as a current asset serves a practical purpose in financial reporting. It ensures that the company’s financial statements accurately reflect its financial position and operational efficiency. By deferring the expense, the asset account gradually decreases as the rental period progresses, with the corresponding expense recognized monthly. This method prevents distortion in the income statement, where a lump-sum payment might otherwise create an artificial spike in expenses. For instance, a small business paying quarterly rent in advance can maintain consistent expense reporting by amortizing the prepaid rent over the relevant months.

From a compliance perspective, treating prepaid rent as a current asset adheres to Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). These frameworks require assets to be recognized when there is a future economic benefit and control over the resource. Prepaid rent meets this criterion, as it represents a right to use property in the future. Auditors and stakeholders scrutinize such entries, making proper classification critical. Misclassification could lead to misstated financial statements, potentially triggering regulatory penalties or eroding investor confidence.

Practical implementation involves creating a prepaid rent account under current assets and systematically adjusting it through journal entries. At the end of each accounting period, an adjusting entry is made to transfer a portion of the prepaid rent to the rent expense account. For example, if $6,000 is prepaid for six months, $1,000 is expensed monthly. This process requires meticulous record-keeping and a clear understanding of lease terms. Accounting software can automate these entries, reducing the risk of errors and ensuring consistency.

In conclusion, prepaid rent is a nuanced aspect of accounting that demands careful handling. By recording advance payments as a current asset, businesses maintain accuracy in financial reporting, comply with accounting standards, and provide a clear picture of their financial health. Whether for a startup or a multinational corporation, mastering this concept is essential for effective financial management. Proper treatment of prepaid rent not only ensures compliance but also supports informed decision-making by reflecting the true economic reality of the business.

What Renter's Insurance Covers: Essential Protection for Your Belongings

You may want to see also

Explore related products

![]()

Tax Deductibility: Rent is often tax-deductible for businesses as an expense

Rent, a significant expense for many businesses, often qualifies as a tax-deductible item, providing a crucial financial benefit. This deduction allows businesses to reduce their taxable income, thereby lowering their overall tax liability. For instance, if a small business pays $2,000 monthly in rent for its office space, this $24,000 annual expense can be deducted from its taxable income, potentially saving thousands in taxes depending on the tax bracket. Understanding the specifics of this deduction is essential for maximizing its benefits.

To claim rent as a tax-deductible expense, businesses must ensure the rental agreement is for a legitimate business purpose. This includes office spaces, retail locations, warehouses, or any property used primarily for business operations. Personal use properties, such as a home office used occasionally, may only qualify for a partial deduction based on the percentage of space and time dedicated to business activities. For example, if 20% of a home is exclusively used for business, only that portion of the rent or mortgage interest may be deductible.

The process of claiming rent as a deduction involves meticulous record-keeping. Businesses should maintain copies of lease agreements, rent receipts, and any other documentation that verifies the rental expense. Additionally, it’s important to distinguish between rent and other property-related expenses. While rent itself is deductible, costs like utilities, insurance, or property taxes may fall under different categories, though they can also be deductible if business-related. Consulting a tax professional can help clarify these distinctions and ensure compliance with tax laws.

One common misconception is that rent deductions are universally applicable. However, eligibility varies by jurisdiction and business structure. For example, in the U.S., sole proprietors report rent deductions on Schedule C of Form 1040, while corporations include it in their income tax returns. Internationally, tax laws differ significantly; in the UK, rent is deductible under “business expenses” for self-assessment tax returns, but specific rules apply to partnerships and limited companies. Always verify local tax regulations to avoid errors or audits.

Finally, while rent deductions offer substantial savings, businesses should avoid overstating expenses or misclassifying personal use as business use. Tax authorities scrutinize large deductions, and inaccuracies can lead to penalties or audits. A proactive approach includes regularly reviewing rental agreements, tracking usage percentages for shared spaces, and staying informed about tax law updates. By leveraging rent deductions wisely, businesses can optimize their financial health while maintaining compliance.

COVID-19 Rent Relief Program: Updates, Challenges, and What's Next

You may want to see also

Explore related products

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![]()

Cash Flow Impact: Rent payments are reported under operating activities in cash flow statements

Rent payments, a ubiquitous expense for businesses, are classified under operating activities in the cash flow statement. This categorization stems from the fundamental nature of rent as a core operational cost, essential for maintaining a business's day-to-day functions. Unlike capital expenditures, which involve acquiring long-term assets, rent represents a recurring expense directly tied to the ongoing operations of a company.

Understanding the Rationale

The rationale behind this classification lies in the matching principle of accounting. This principle dictates that expenses should be recognized in the same period as the revenues they help generate. Rent, being a necessary expense for occupying premises where business activities occur, directly contributes to revenue generation. Therefore, reporting it under operating activities provides a more accurate representation of a company's operational cash flow.

Implications for Financial Analysis

This classification has significant implications for financial analysis. Investors and analysts scrutinize operating cash flow as a key indicator of a company's ability to generate cash from its core business operations. Including rent payments in this section provides a clearer picture of the company's operational efficiency and sustainability. A consistent and manageable rent expense reflects a well-managed business, while excessive rent burdens can signal potential financial strain.

Practical Considerations

For businesses, understanding this classification is crucial for accurate financial reporting and analysis. When preparing cash flow statements, ensure rent payments are consistently categorized under operating activities. This consistency allows for meaningful comparisons across periods and with industry peers. Additionally, analyzing rent expenses in relation to revenue can help identify areas for cost optimization or negotiate more favorable lease terms.

Renting a Billboard in Florida: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Rent typically falls under operating expenses in accounting, as it is a regular, ongoing cost associated with running a business.

Rent is considered an expense, not an asset, because it represents a cost incurred for the use of a property or asset, not ownership.

Rent is recorded on the income statement as part of the operating expenses, reducing the business's net income.

Yes, if rent is paid in advance, it is initially recorded as a prepaid expense (an asset) and then expensed over the rental period through amortization.

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)