Rent income in accounting is classified as a type of operating revenue, specifically under the category of non-operating income if it is not the primary business activity of the entity. For companies whose main operations involve leasing properties, such as real estate companies, rent income is considered operating income, as it directly relates to their core business. However, for businesses that generate rent income from peripheral assets like unused office space or equipment, it is typically recorded as non-operating income on the income statement. This classification ensures that financial statements accurately reflect the source and nature of the revenue, providing stakeholders with a clear understanding of the company’s financial performance and income streams.

Explore related products

What You'll Learn

- Revenue Recognition: Rent income is recognized over the lease term, not upfront

- Operating vs. Non-Operating: Classified as operating income if core to business, else non-operating

- Accrual Accounting: Recorded when earned, not when received, following accrual principles

- Lease Classification: Depends on lease type (operating or finance lease) in accounting

- Tax Treatment: Taxable as ordinary income, subject to specific regulations and deductions

![]()

Revenue Recognition: Rent income is recognized over the lease term, not upfront

Rent income, a cornerstone of many businesses, is not a windfall to be recognized in a single swoop. This is a critical distinction in accounting, where the principle of revenue recognition demands a more nuanced approach. The concept is straightforward: rent income is recognized over the lease term, not upfront. This means that the revenue from a lease agreement is spread out over the period during which the tenant occupies the property, rather than being recorded all at once when the lease is signed.

Consider a commercial property leased for a 12-month period at a monthly rent of $5,000. Under the principle of revenue recognition, the landlord would not record $60,000 in revenue immediately upon signing the lease. Instead, they would recognize $5,000 in revenue each month as the tenant occupies the space. This approach aligns with the matching principle in accounting, which requires that revenues and expenses be matched in the period in which they are incurred. By recognizing rent income over the lease term, businesses can provide a more accurate representation of their financial performance, avoiding distortions that could arise from upfront recognition.

The rationale behind this method is both practical and theoretical. From a practical standpoint, it reflects the economic reality of the transaction. The landlord is providing a service – the use of the property – over a specific period, and the revenue should be recognized as that service is delivered. Theoretically, this approach adheres to the accrual basis of accounting, which records transactions when they are earned, not when payment is received. For instance, if a tenant pays the entire year’s rent upfront, the landlord would still recognize the income monthly, ensuring that the financial statements reflect the true financial position of the business.

However, implementing this principle requires careful consideration. Businesses must establish clear policies for lease agreements, ensuring that the terms are well-defined and that the rent income is systematically recognized. This may involve setting up accounting systems that automatically allocate revenue over the lease term or training staff to manually record income on a monthly basis. For example, accounting software like QuickBooks allows users to set up recurring journal entries, making it easier to recognize rent income over time. Additionally, businesses should be aware of the specific accounting standards that apply to their jurisdiction, such as ASC 842 in the United States or IFRS 16 internationally, which provide detailed guidance on lease accounting.

In conclusion, recognizing rent income over the lease term is not just a matter of compliance with accounting standards; it is a fundamental practice that ensures financial statements accurately reflect a business’s operations. By avoiding the temptation to record revenue upfront, businesses can maintain transparency, improve financial reporting, and make more informed decisions. Whether you’re a landlord, property manager, or accountant, understanding and applying this principle is essential for maintaining the integrity of your financial records.

Understanding Renter's Insurance: Factors Influencing Your Policy Premium Calculation

You may want to see also

Explore related products

$15.95 $15.95

![]()

Operating vs. Non-Operating: Classified as operating income if core to business, else non-operating

Rent income, a common revenue stream for many businesses, often sparks debate in accounting circles: where does it truly belong on the income statement? The classification hinges on a critical distinction: is rent collection central to the business's core operations? This question separates operating income from non-operating income, a distinction with significant implications for financial analysis.

Operating income reflects revenue generated from a company's primary activities, those essential to its raison d'être. For a real estate company, rent income is undoubtedly operating income; leasing properties is their core business. Conversely, consider a manufacturing company that owns a vacant warehouse and leases it out. The rent received is incidental to their primary function of producing goods, thus classified as non-operating income.

This classification isn't merely semantic. Investors and analysts scrutinize operating income to gauge a company's core profitability and operational efficiency. Non-operating income, while valuable, provides a separate lens, highlighting income streams unrelated to the company's primary focus. Think of it as separating the wheat from the chaff – operating income reveals the true strength of the core business, while non-operating income offers insights into ancillary activities.

For instance, a tech company generating substantial rent income from subletting office space might appear highly profitable on the surface. However, if this rent income is classified as non-operating, it signals that the company's core tech operations may not be as robust as initially perceived.

The key takeaway is this: the classification of rent income as operating or non-operating depends entirely on its relationship to the company's core business activities. This distinction is crucial for accurate financial analysis, allowing stakeholders to understand the true drivers of a company's profitability and make informed decisions.

Converting Rent-Stabilized Residential Units into Condos: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

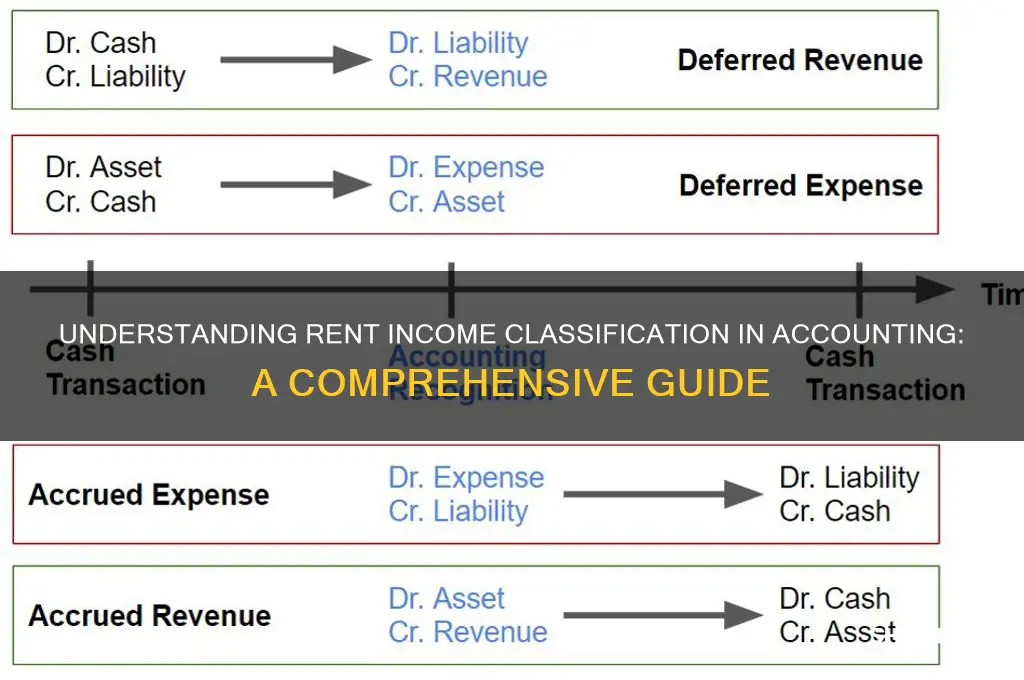

Accrual Accounting: Recorded when earned, not when received, following accrual principles

In accrual accounting, rent income is recognized when it is earned, not when the payment is received. This principle aligns with the matching concept, ensuring that revenues and expenses are recorded in the same accounting period they are incurred. For instance, if a tenant signs a lease agreement on January 1 for a year-long rental, the landlord records the entire year’s rent income in January, even if payments are made monthly. This approach provides a more accurate financial snapshot by reflecting the economic reality of the transaction, rather than the timing of cash flows.

Consider a practical example: a commercial property owner leases a space for $12,000 annually, payable in $1,000 monthly installments. Under accrual accounting, the full $12,000 is recorded as income in January, the month the lease begins. This contrasts with cash-basis accounting, where income is recorded only when payments are received. The accrual method ensures that the financial statements reflect the landlord’s right to the income as soon as the tenant occupies the property, regardless of payment timing.

However, applying accrual principles to rent income requires careful judgment. Accountants must assess the collectibility of the rent to avoid overstating income. For example, if there is significant doubt about a tenant’s ability to pay, the income should not be fully accrued. Instead, a provision for doubtful debts may be necessary. This ensures compliance with the conservatism principle, which prioritizes understating rather than overstating financial performance.

A key takeaway is that accrual accounting for rent income enhances financial transparency but demands precision. Businesses must maintain detailed records of lease agreements, payment schedules, and tenant creditworthiness. Software tools like QuickBooks or Xero can automate accrual entries, reducing the risk of errors. Additionally, regular reviews of outstanding rent receivables help identify potential collection issues early, allowing for timely adjustments to financial statements.

In summary, accrual accounting classifies rent income as earned when the tenant’s right to use the property begins, not when payment is received. This method aligns revenues with the period in which they are incurred, offering a clearer picture of financial health. While it requires meticulous record-keeping and judgment, the benefits of accuracy and compliance with accounting standards make it the preferred approach for most businesses.

Finding the Perfect Warehouse Rental: A Comprehensive Guide for Businesses

You may want to see also

Explore related products

$28.74 $38.99

![]()

Lease Classification: Depends on lease type (operating or finance lease) in accounting

In accounting, the classification of lease agreements as either operating or finance leases significantly impacts how rent income is recognized and reported. This distinction is not merely semantic but carries profound implications for financial statements, affecting metrics such as assets, liabilities, and income. For lessors, understanding this classification is crucial for accurate reporting, while lessees must recognize how it influences their balance sheets and income statements.

Classification Criteria: The Foundation of Lease Accounting

The classification of a lease hinges on specific criteria outlined in accounting standards, such as ASC 842 in the U.S. or IFRS 16 internationally. A lease is classified as a finance lease if it transfers substantially all the risks and rewards of ownership to the lessee. Indicators include lease terms covering a major part of the asset’s life, the presence of a bargain purchase option, or lease payments totaling the asset’s fair value. If these conditions are not met, the lease is classified as an operating lease. For example, a 10-year lease on a building with a 20-year useful life might be classified as an operating lease, while a 15-year lease on the same building could be a finance lease.

Impact on Rent Income Recognition: A Comparative Analysis

For lessors, the classification determines how rent income is recognized. Under a finance lease, income is recognized as a combination of interest income (using the effective interest method) and reduction of the lease receivable. This mirrors the amortization of a loan. In contrast, operating leases result in rent income being recognized on a straight-line basis over the lease term. For instance, if a lessor leases a property for $120,000 over 12 months under an operating lease, $10,000 is recognized monthly. Under a finance lease, the income would be split between interest and principal, depending on the interest rate implicit in the lease.

Practical Implications for Financial Reporting

Misclassification of leases can lead to material misstatements in financial statements. For lessors, incorrectly classifying a finance lease as an operating lease could understate interest income and overstate rental income. Lessee accounting also differs significantly: finance leases capitalize the lease asset and liability on the balance sheet, while operating leases are expensed as incurred. This distinction affects leverage ratios, profitability metrics, and cash flow presentations. For example, a retailer with multiple store leases must carefully classify each lease to ensure compliance and accurate financial reporting.

Strategic Considerations and Best Practices

To navigate lease classification effectively, lessors and lessees should adopt a structured approach. Lessors should review lease agreements for the presence of ownership transfer indicators and document their rationale for classification. Lessees should assess the impact of lease classification on their financial ratios and disclosures. Tools such as lease accounting software can automate calculations and ensure consistency. Additionally, periodic reviews of lease portfolios are essential, especially when lease terms are modified or renewed. By mastering lease classification, stakeholders can enhance the transparency and reliability of their financial reporting.

Renting Smart: Income-Based Renting Guide

You may want to see also

Explore related products

![]()

Tax Treatment: Taxable as ordinary income, subject to specific regulations and deductions

Rent income, a staple for many property owners, is classified as ordinary income for tax purposes. This means it’s taxed at the same rates as wages, salaries, or business profits. Unlike capital gains, which often benefit from lower tax rates, rental income doesn’t get special treatment. For instance, if you earn $30,000 annually from renting out a property, that amount is added to your taxable income and taxed according to your marginal tax bracket. This straightforward classification simplifies reporting but requires careful attention to deductions and regulations to optimize your tax liability.

The IRS allows landlords to offset rental income with specific deductions, effectively reducing the taxable amount. Common deductions include mortgage interest, property taxes, insurance premiums, maintenance costs, and depreciation. For example, if your rental property generates $40,000 in income but incurs $20,000 in allowable expenses, only $20,000 is subject to taxation. However, these deductions must be directly tied to the rental activity and properly documented. Misclassifying personal expenses as rental deductions can trigger audits or penalties, so meticulous record-keeping is essential.

One critical regulation to note is the passive activity loss rules. If your rental activity is considered passive—meaning you’re not actively involved in managing the property—losses from the rental may be limited. For example, if your rental property generates a $10,000 loss, you can’t use it to offset other types of income unless you meet specific material participation tests. However, real estate professionals may be exempt from these rules, allowing them to deduct losses more freely. Understanding these nuances can significantly impact your tax strategy.

To navigate the tax treatment of rental income effectively, consider these practical steps: first, maintain separate bank accounts and financial records for your rental property to streamline expense tracking. Second, consult a tax professional to ensure compliance with IRS regulations and maximize deductions. Third, stay informed about changes in tax laws, such as updates to depreciation schedules or deductions for energy-efficient property improvements. By proactively managing your rental income and expenses, you can minimize tax obligations while staying within legal boundaries.

Step-by-Step Guide to Applying for Rent Relief Grant Assistance

You may want to see also

Frequently asked questions

Rent income is classified as operating revenue if it is generated from a company’s primary business activities, such as leasing property. If it is from non-core activities, it may be classified as non-operating income or other income.

Rent income is not typically classified as earned income, which usually refers to income from employment or business operations. Instead, it is categorized as passive income or rental income in accounting.

Rent income is reported on the income statement under the appropriate category, such as operating revenue or other income, depending on its source. It is also disclosed in the notes to the financial statements for clarity.