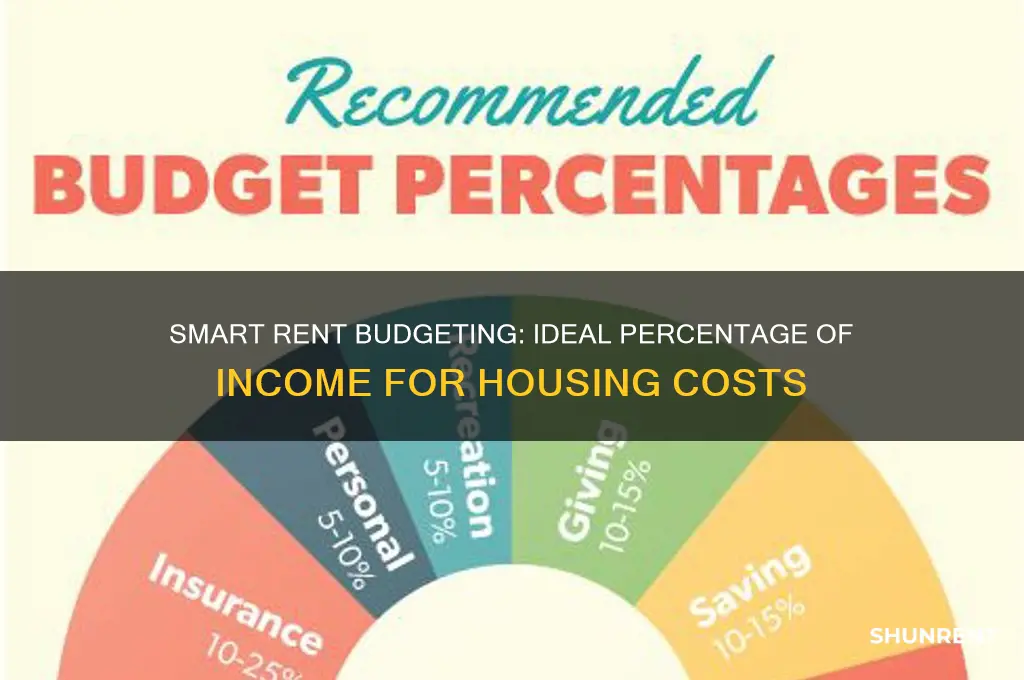

Determining the ideal percentage of income that should go toward rent is a crucial financial decision that varies based on individual circumstances, location, and lifestyle. A widely accepted rule of thumb is the 30% rule, which suggests allocating no more than 30% of your gross monthly income to housing costs. This guideline helps ensure that rent remains manageable without compromising other financial obligations, such as savings, utilities, groceries, and debt repayment. However, factors like high cost-of-living areas, fluctuating income, or personal financial goals may necessitate adjusting this percentage. For instance, in expensive cities like New York or San Francisco, renters might exceed 30% to secure adequate housing, while those prioritizing savings or debt reduction may aim for a lower percentage. Ultimately, striking a balance between affordability and quality of life is key when deciding how much to spend on rent.

| Characteristics | Values |

|---|---|

| Recommended Percentage of Income for Rent | 30% or less |

| Source of Recommendation | U.S. Department of Housing and Urban Development (HUD) |

| Reason for 30% Rule | Ensures affordability and prevents financial strain |

| Average Rent-to-Income Ratio in the U.S. (2023) | ~32% (varies by city and region) |

| High-Cost Urban Areas (e.g., NYC, SF) | Often exceeds 50% of income |

| Low-Income Households | May spend 50% or more on rent |

| Factors Influencing Rent Percentage | Location, income level, household size, lifestyle |

| Alternative Budgeting Methods | 50/30/20 rule (50% needs, 30% wants, 20% savings) |

| Impact of High Rent-to-Income Ratio | Reduced savings, increased debt, financial instability |

| Adjustments for High Rent Areas | Roommates, smaller living spaces, or relocating |

| Latest Trend (2023) | Rising rents outpacing wage growth in many areas |

Explore related products

What You'll Learn

- Affordability Rules: 30% rule, 50/30/20 budget, and other guidelines for rent affordability

- Location Impact: How city costs affect rent percentage allocation in household budgets

- Income Variability: Adjusting rent percentage based on salary, debt, and savings goals

- Lifestyle Trade-offs: Balancing rent costs with spending on leisure, food, and travel

- Emergency Funds: Ensuring rent percentage allows for financial stability during unexpected crises

![]()

Affordability Rules: 30% rule, 50/30/20 budget, and other guidelines for rent affordability

Determining how much of your income should go toward rent is a cornerstone of financial stability. The 30% rule is the most widely cited guideline, suggesting that no more than 30% of your gross monthly income should be allocated to housing costs. For example, if you earn $4,000 per month, your rent should ideally not exceed $1,200. This rule originated from federal affordability standards for subsidized housing but has since become a general benchmark for renters. While it’s a simple and widely accepted principle, its applicability varies based on location, income level, and personal financial goals.

The 50/30/20 budget offers a broader framework for managing expenses, including rent. Under this rule, 50% of your income covers necessities (like housing, utilities, and groceries), 30% goes to discretionary spending (entertainment, travel, etc.), and 20% is allocated to savings and debt repayment. Within the 50% for necessities, rent typically consumes the largest share, often aligning with the 30% rule. However, this model assumes a balanced income distribution, which may not work for low-income earners or those in high-cost-of-living areas. For instance, someone earning $3,000 monthly might struggle to keep rent under $900 while covering other essentials.

Beyond these rules, local affordability guidelines provide more context-specific advice. In cities like New York or San Francisco, where rent often exceeds 30% of income, experts recommend adjusting expectations or seeking roommates to share costs. Conversely, in more affordable regions, aiming for a lower percentage, such as 25%, can free up funds for savings or investments. Tools like rent-to-income calculators can help tailor these guidelines to individual circumstances, factoring in local median rents and personal financial obligations.

For young professionals or students, flexibility is key. If you’re starting your career, consider prioritizing lower rent to build an emergency fund or pay off student loans. For instance, allocating 20–25% of your income to rent might allow you to save more aggressively. Conversely, families or established earners may opt to spend closer to 30% on rent to secure larger or more convenient housing. The key is aligning your rent percentage with your long-term financial goals, not just adhering to a one-size-fits-all rule.

Ultimately, affordability rules are starting points, not rigid laws. They provide a framework for decision-making but should be adjusted based on personal priorities and local realities. For example, if you value living in a vibrant urban area, you might accept a higher rent percentage in exchange for reduced transportation costs or greater career opportunities. Conversely, if financial independence is your goal, aim for a lower rent-to-income ratio to accelerate savings. By understanding these guidelines and adapting them to your unique situation, you can make informed choices that balance housing needs with overall financial health.

Why Rent a Cabin in Sylva or Bryson City?

You may want to see also

Explore related products

![]()

Location Impact: How city costs affect rent percentage allocation in household budgets

The 30% rule, a widely accepted guideline suggesting that households should allocate no more than 30% of their income to rent, often falls short in high-cost urban centers. In cities like New York, San Francisco, or London, where median rents can exceed $3,000 per month, adhering to this rule would require a household income of at least $120,000 annually. For many residents, this disparity forces a reevaluation of budgeting priorities, with rent often consuming 40% to 50% of income. This imbalance highlights how location-specific costs can render traditional financial advice impractical, necessitating a more nuanced approach to rent allocation.

Consider the comparative impact of city costs on household budgets. In smaller cities or rural areas, where rent might account for 20% to 25% of income, families can allocate more resources to savings, investments, or leisure. Conversely, urban dwellers often face a trade-off: higher rent in exchange for job opportunities, cultural amenities, or convenience. For instance, a family in Austin, Texas, might spend 28% of their income on rent, while a similarly sized household in San Francisco could allocate 45% for comparable living space. This disparity underscores the need to adjust rent percentages based on local economic realities rather than adhering rigidly to one-size-fits-all guidelines.

To navigate these challenges, households in expensive cities should adopt a flexible budgeting strategy. Start by calculating your post-tax income and subtracting essential expenses like groceries, transportation, and healthcare. If rent exceeds 40% of your remaining budget, consider downsizing, moving to a less expensive neighborhood, or exploring shared housing arrangements. For example, a single professional in Seattle earning $70,000 annually might opt for a studio apartment priced at $1,600 (27% of income) instead of a one-bedroom at $2,200 (38%). Such adjustments can help maintain financial stability without sacrificing urban living.

Persuasively, it’s worth noting that prioritizing rent over other expenses in high-cost cities isn’t just a financial decision—it’s a lifestyle choice. Urban residents often accept higher rent percentages in exchange for proximity to work, cultural hubs, or social networks. However, this trade-off can lead to long-term financial strain if not managed carefully. For instance, allocating 50% of income to rent leaves limited funds for retirement savings or emergency funds, increasing vulnerability to economic shocks. Balancing the desire for urban living with long-term financial health requires intentional planning and, occasionally, difficult compromises.

In conclusion, the impact of location on rent allocation demands a tailored approach to household budgeting. While the 30% rule serves as a useful starting point, it must be adapted to reflect local cost-of-living realities. By analyzing income, expenses, and lifestyle priorities, households can determine a sustainable rent percentage that aligns with their unique circumstances. Whether in a bustling metropolis or a quiet suburb, understanding the interplay between location and rent is essential for achieving financial equilibrium.

Affordable Renting on $60K: Smart Budgeting Tips for Your Salary

You may want to see also

Explore related products

![]()

Income Variability: Adjusting rent percentage based on salary, debt, and savings goals

A common rule of thumb suggests allocating 30% of your income to rent, but this one-size-fits-all approach ignores the complexities of individual financial situations. Income variability demands a more nuanced strategy, one that considers not just your salary but also your debt obligations and savings goals.

A young professional with a high salary and minimal debt can comfortably allocate a larger percentage to rent in a desirable neighborhood, leveraging their earning potential to build a fulfilling lifestyle. Conversely, someone burdened by student loans and credit card debt must prioritize debt repayment, potentially necessitating a smaller, more affordable living space and a lower rent percentage, even if it means sacrificing some convenience.

Imagine two individuals earning $60,000 annually. One, free from debt, could allocate 35% to rent, allowing them to live in a vibrant urban area close to work. The other, burdened by $30,000 in student loans, should aim for a 25% rent allocation, freeing up funds for aggressive debt repayment and potentially choosing a more affordable neighborhood. This example highlights the importance of tailoring rent percentage to individual circumstances.

Steps to Adjust Rent Percentage:

- Calculate Your Discretionary Income: Subtract essential expenses like taxes, insurance, and minimum debt payments from your net income. This reveals your disposable income, the pool from which rent should be drawn.

- Prioritize Debt Repayment: Aim to allocate at least 20% of your discretionary income towards debt repayment. High-interest debt, like credit cards, should be prioritized.

- Define Your Savings Goals: Whether it's an emergency fund, retirement savings, or a down payment on a house, allocate a realistic percentage of your discretionary income towards these goals.

- Determine Your Rent Comfort Zone: Based on steps 1-3, calculate the maximum rent percentage that allows you to meet your debt obligations and savings targets while maintaining a comfortable lifestyle.

Cautions:

- Avoid Overcommitting: Don't stretch yourself too thin by allocating an unsustainable percentage to rent. Factor in unexpected expenses and leave room for flexibility.

- Consider Lifestyle Choices: Your desired lifestyle plays a role. If you prioritize travel or dining out, you may need to adjust your rent allocation accordingly.

The 30% rule is a starting point, not a rigid mandate. By considering income variability, debt obligations, and savings goals, you can determine a rent percentage that aligns with your unique financial reality. This personalized approach ensures that your housing costs support your overall financial well-being, allowing you to build a secure and fulfilling future.

Bouncy Castle Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Lifestyle Trade-offs: Balancing rent costs with spending on leisure, food, and travel

Rent consumes a staggering 30-50% of income for many, leaving a tightrope walk between shelter and the experiences that make life rich. This reality forces a constant negotiation: a cozy apartment near the city center versus weekend getaways, a spacious living room versus dining out with friends, a shorter commute versus saving for that dream vacation.

Consider the 50/30/20 rule, a popular budgeting framework. It suggests allocating 50% of income to needs (including rent), 30% to wants (leisure, dining, travel), and 20% to savings and debt repayment. However, this is a starting point, not a rigid mandate. For those in high-rent areas, 50% for needs might be unrealistic, necessitating a reallocation. Perhaps rent stretches to 60%, squeezing leisure to 20% and demanding creative solutions like potluck dinners instead of restaurants or exploring free local attractions.

Conversely, those in more affordable areas might dedicate only 30% to rent, freeing up funds for spontaneous trips or indulging in culinary adventures. The key lies in understanding your priorities and making conscious choices.

The trade-offs are deeply personal. A young professional might prioritize a vibrant neighborhood with easy access to nightlife, accepting a smaller space and higher rent. A family might opt for a larger home in a quieter area, sacrificing proximity to cultural events. A digital nomad might choose a co-living space with built-in community, trading privacy for affordability and travel flexibility.

Ultimately, there's no one-size-fits-all answer. It's about finding your equilibrium, where rent doesn't suffocate your desire for experiences, and experiences don't jeopardize your financial stability. Track your spending, identify areas for adjustment, and remember: a fulfilling life isn't defined by square footage, but by the memories you create within those walls and beyond.

Understanding Quota Rent for Alaskan King Crab Fishing Rights

You may want to see also

Explore related products

![]()

Emergency Funds: Ensuring rent percentage allows for financial stability during unexpected crises

A common rule of thumb suggests allocating 30% of your income to rent, but this guideline often overlooks the critical need for emergency funds. Unexpected crises—job loss, medical emergencies, or sudden repairs—can destabilize your finances, making rent payments a burden rather than a routine expense. To ensure financial stability, consider how your rent percentage fits into a broader safety net. For instance, if you allocate 30% to rent, aim to save at least 20% of your income for emergencies, ensuring you have 3–6 months’ worth of living expenses set aside. This dual approach balances housing costs with preparedness, reducing the risk of eviction or debt during unforeseen events.

Analyzing the interplay between rent and emergency funds reveals a trade-off: higher rent payments leave less room for savings, while lower rent may compromise living standards. For example, if you spend 40% of your income on rent, you’ll likely struggle to build an emergency fund, leaving you vulnerable to financial shocks. Conversely, capping rent at 25% allows more flexibility to save and invest. A practical strategy is to prioritize affordable housing, even if it means downsizing or sharing space, to free up funds for emergencies. This approach ensures that your rent percentage doesn’t hinder your ability to weather crises.

Persuasively, consider this: an emergency fund isn’t just a savings account—it’s insurance for your financial independence. By keeping your rent percentage in check, you create breathing room in your budget to build this safety net. For young professionals or those in volatile industries, this is especially crucial. Start by automating savings into a high-yield account, even if it’s just 5–10% of your income initially. Over time, adjust your rent allocation downward if possible, redirecting those funds into emergency savings. This proactive mindset transforms rent from a potential liability into a manageable expense within a resilient financial plan.

Comparatively, countries with robust social safety nets often see lower personal savings rates, as citizens rely on government support during crises. In the U.S., however, where such systems are limited, individuals must take responsibility for their financial stability. For instance, someone earning $50,000 annually might allocate $15,000 (30%) to rent, leaving $35,000 for other expenses. By saving $10,000 (20%) annually, they could build a $30,000 emergency fund in 3 years, ensuring rent remains affordable even during job loss or illness. This contrasts with someone spending 40% on rent, who might save only $5,000 annually, delaying financial security.

Descriptively, imagine a scenario where your car breaks down, requiring a $2,000 repair. If your rent consumes 35% of your income, you might struggle to cover the cost without dipping into credit card debt. Now, picture having a $10,000 emergency fund, built by capping rent at 25% and saving the difference. The repair becomes a minor setback, not a financial crisis. This illustrates how a balanced rent percentage, paired with disciplined saving, creates a buffer against life’s unpredictability. It’s not just about affording rent today—it’s about securing peace of mind for tomorrow.

Renting Bank Space: A Guide to Maximizing Your Financial Institution's Potential

You may want to see also

Frequently asked questions

A common rule of thumb is the 30% rule, which suggests spending no more than 30% of your gross monthly income on rent. This helps ensure you have enough for other expenses and savings.

Not necessarily. The 30% rule is a general guideline, but it may vary based on your location, income level, and other financial obligations. In high-cost areas, you might need to spend more, while in lower-cost areas, you could spend less.

If 30% is unaffordable, consider finding a more budget-friendly housing option, getting a roommate, or increasing your income. Prioritize keeping housing costs as low as possible to avoid financial strain.

Yes, it’s best to include all housing-related costs, such as utilities, renters insurance, and maintenance, in your total rent percentage to get a more accurate picture of your housing expenses.