When considering the financial burden of rent on individuals, it's essential to examine the percentage of one's paycheck that goes towards housing costs. This figure can vary significantly depending on factors such as location, income level, and personal financial management. In urban areas with high costs of living, such as New York City or San Francisco, it's not uncommon for individuals to allocate 30% or more of their income towards rent. On the other hand, in more affordable regions, this percentage may be closer to 20% or even 15%. Understanding this ratio is crucial for budgeting and financial planning, as it can impact an individual's ability to save, invest, and cover other essential expenses.

Explore related products

What You'll Learn

- Average Rent-to-Income Ratio: Explore the typical percentage of income spent on rent across various cities

- Factors Influencing Rent Costs: Analyze how location, property type, and amenities affect rental prices

- Budgeting for Rent: Discuss strategies for managing rent expenses within a monthly budget

- Rent Control and Subsidies: Examine policies and programs aimed at making housing more affordable

- Impact of Rent on Financial Health: Investigate how high rent can influence savings, debt, and overall financial stability

![]()

Average Rent-to-Income Ratio: Explore the typical percentage of income spent on rent across various cities

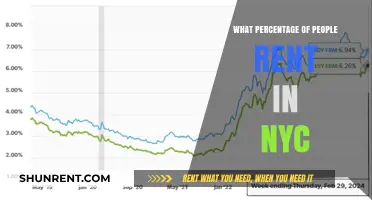

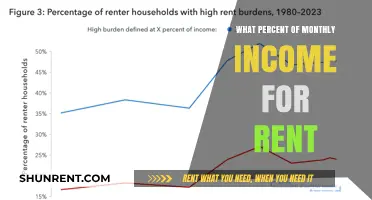

The average rent-to-income ratio is a critical metric for understanding the financial burden of housing on individuals and families. This ratio varies significantly across different cities, influenced by factors such as local economy, housing market conditions, and cost of living. For instance, in cities like San Francisco and New York, the rent-to-income ratio can exceed 30%, meaning that a significant portion of one's paycheck is allocated to rent. In contrast, cities like Detroit and Cleveland have much lower ratios, often below 20%.

Analyzing the rent-to-income ratio can provide insights into the affordability of housing in a particular area. A higher ratio indicates that housing is less affordable, potentially leading to financial strain for residents. This can have broader implications for the local economy, as individuals may have less disposable income to spend on other goods and services. Furthermore, a high rent-to-income ratio can contribute to increased homelessness and housing insecurity, as individuals struggle to make ends meet.

To calculate the rent-to-income ratio, one must divide the average monthly rent by the average monthly income in a given area. This calculation can be done for different income brackets to provide a more nuanced understanding of the housing affordability landscape. For example, a city may have a relatively low overall rent-to-income ratio, but this could mask the fact that low-income residents are spending a much higher percentage of their income on rent compared to higher-income residents.

When examining the rent-to-income ratio across various cities, it is essential to consider the broader context of each location. Factors such as public transportation availability, job opportunities, and access to amenities can all impact the desirability of a city, even if the rent-to-income ratio is high. Additionally, the ratio can fluctuate over time due to changes in the housing market, economic conditions, and demographic shifts.

In conclusion, the average rent-to-income ratio is a valuable tool for assessing the affordability of housing in different cities. By understanding this metric, policymakers, urban planners, and individuals can make more informed decisions about where to live, invest, and allocate resources to address housing affordability challenges.

Understanding Your Rights: 9-Year Carpet Replacement Laws for Renters

You may want to see also

Explore related products

![]()

Factors Influencing Rent Costs: Analyze how location, property type, and amenities affect rental prices

Location is a critical factor influencing rent costs. Urban areas, particularly those with high demand and limited supply, tend to have higher rental prices. For instance, cities like New York, San Francisco, and Los Angeles are known for their exorbitant rent costs due to their desirability and economic opportunities. Conversely, rural areas or less popular cities often have lower rental prices. Proximity to public transportation, schools, and employment centers also plays a significant role in determining rent costs, as convenience and accessibility are highly valued by renters.

Property type is another key determinant of rental prices. Single-family homes, apartments, condos, and townhouses each have their own market dynamics and price points. For example, single-family homes typically command higher rents due to their larger size and private amenities, while apartments may be more affordable but offer less space and shared facilities. The condition and age of the property also impact rent costs, with newer, well-maintained properties generally fetching higher prices.

Amenities can significantly affect rental prices as well. Properties with desirable features such as swimming pools, gyms, on-site laundry, and pet-friendly policies often have higher rents. Additionally, the inclusion of utilities like water, electricity, and internet can also increase the rental cost. Landlords may also charge premiums for properties with scenic views, private outdoor spaces, or high-end finishes.

To analyze how these factors affect rental prices, one can conduct a comparative study of properties in different locations, with varying property types and amenities. This analysis can help renters and landlords understand the market dynamics and make informed decisions. For renters, it's essential to consider their budget and prioritize the factors that matter most to them, such as location, property type, and amenities. Landlords, on the other hand, can use this information to set competitive rental prices and attract quality tenants.

In conclusion, location, property type, and amenities are the primary factors influencing rent costs. Understanding these factors can help renters and landlords navigate the rental market more effectively. Renters should carefully consider their needs and budget when choosing a property, while landlords should ensure that their rental prices are competitive and reflective of the property's value.

Renting a U-Haul in Brooklyn: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Budgeting for Rent: Discuss strategies for managing rent expenses within a monthly budget

To effectively manage rent expenses within a monthly budget, it's crucial to adopt a strategic approach that aligns with your financial goals and lifestyle. One key strategy is to prioritize rent as a fixed expense and allocate a specific percentage of your paycheck towards it. Financial experts often recommend the 30% rule, where no more than 30% of your gross income should go towards housing costs. This guideline helps ensure that you have enough funds left for other essential expenses, savings, and discretionary spending.

Another effective strategy is to create a detailed budget that categorizes all your monthly expenses. Start by listing your fixed expenses, such as rent, utilities, and insurance, followed by variable expenses like groceries, transportation, and entertainment. This comprehensive overview will help you identify areas where you can cut costs and reallocate funds to cover your rent more comfortably. Consider using budgeting apps or spreadsheets to track your spending and make adjustments as needed.

Negotiating with your landlord can also be a valuable tactic in managing rent expenses. If you're a reliable tenant with a good rental history, you may be able to secure a lower rent or more favorable lease terms. It's essential to approach the negotiation process professionally, highlighting your positive attributes as a tenant and demonstrating your willingness to commit to a longer lease if necessary.

Additionally, consider exploring alternative housing options that may be more affordable. This could include downsizing to a smaller apartment, moving to a less expensive neighborhood, or even considering a roommate situation. While these changes may require some adjustments to your lifestyle, they can significantly reduce your rent burden and free up more funds for other financial priorities.

Lastly, building an emergency fund is crucial for managing unexpected expenses and avoiding financial stress. Aim to save at least three to six months' worth of living expenses in a readily accessible savings account. This financial cushion will provide peace of mind and help you cover rent and other essential costs in case of job loss or unforeseen emergencies.

By implementing these strategies and maintaining a proactive approach to budgeting, you can effectively manage your rent expenses and achieve greater financial stability. Remember to regularly review and adjust your budget to accommodate changes in your income, expenses, and financial goals.

Comcast TV Tuner Rentals: Are They Necessary?

You may want to see also

Explore related products

![Quicken Classic Deluxe for New Subscribers| 1 Year [PC/Mac Online Code]](https://m.media-amazon.com/images/I/61ypcFpjCuL._AC_UY218_.jpg)

![QUICKEN CLASSIC BUSINESS & PERSONAL FOR NEW SUBSCRIBERS| 1 Year [PC/Mac Online code]](https://m.media-amazon.com/images/I/51sQsom78CL._AC_UY218_.jpg)

![Quicken Simplifi Personal Finance Software for NEW Simplifi Subscribers | 1 Year Subscription| Cloud [Online Code]](https://m.media-amazon.com/images/I/71f4PqikPzL._AC_UY218_.jpg)

![]()

Rent Control and Subsidies: Examine policies and programs aimed at making housing more affordable

Rent control policies are regulatory measures that limit the amount by which rent can increase over a given period. These policies are designed to protect tenants from steep rent hikes and to maintain a stable housing market. By capping rent increases, rent control can help ensure that housing remains affordable for low- and middle-income households. However, critics argue that rent control can lead to a decrease in the supply of rental housing, as landlords may be less incentivized to invest in rental properties if their potential returns are limited.

Subsidies, on the other hand, are financial assistance programs that help tenants pay their rent. These programs can take various forms, such as direct cash assistance, vouchers, or tax credits. Subsidies are typically targeted at low-income households and can help make housing more affordable by reducing the portion of a tenant's income that goes towards rent. For example, the Housing Choice Voucher Program, also known as Section 8, provides eligible low-income families with a voucher that covers a portion of their rent, allowing them to afford housing in the private market.

One unique approach to making housing more affordable is the concept of inclusionary zoning. This policy requires developers to set aside a certain percentage of units in new housing developments for affordable housing. By mandating the creation of affordable housing units, inclusionary zoning can help increase the supply of affordable housing and reduce the pressure on existing affordable housing stock.

Another innovative strategy is the use of community land trusts (CLTs). CLTs are nonprofit organizations that acquire and hold land for the benefit of a community. By removing land from the speculative market, CLTs can help stabilize housing prices and ensure that housing remains affordable for community members. CLTs often work in partnership with local governments and community organizations to develop affordable housing projects that meet the specific needs of the community.

In conclusion, rent control and subsidies are important tools for making housing more affordable, but they are not the only solutions. Innovative policies and programs, such as inclusionary zoning and community land trusts, can also play a critical role in addressing the housing affordability crisis. By examining these various approaches, policymakers and community leaders can develop comprehensive strategies that ensure everyone has access to safe, stable, and affordable housing.

Right to Rent: Company Lets and Compliance

You may want to see also

Explore related products

![Quicken Classic Premier for New Subscribers| 1 Year [PC/Mac Online Code]](https://m.media-amazon.com/images/I/614+auQosjL._AC_UY218_.jpg)

![]()

Impact of Rent on Financial Health: Investigate how high rent can influence savings, debt, and overall financial stability

High rent can significantly impact an individual's financial health, often leading to a vicious cycle of debt and limited savings. When a large portion of one's paycheck is allocated to rent, it reduces the available funds for other essential expenses, savings, and discretionary spending. This can result in individuals resorting to high-interest debt, such as credit cards or payday loans, to cover unexpected costs or emergencies. Over time, this accumulation of debt can lead to financial instability and hinder long-term wealth accumulation.

Furthermore, the burden of high rent can limit an individual's ability to invest in their future. For instance, saving for retirement, education, or a down payment on a home becomes increasingly challenging when rent consumes a substantial portion of one's income. This can lead to delayed milestones and a less secure financial future. Additionally, high rent can force individuals to cut back on other important expenses, such as healthcare, insurance, or quality food, which can have negative consequences on their overall well-being.

To mitigate the impact of high rent on financial health, individuals can explore various strategies. One approach is to create a detailed budget and prioritize expenses, ensuring that essential costs are covered before discretionary spending. Another strategy is to seek out additional sources of income, such as a side job or freelance work, to supplement the main paycheck. Additionally, individuals can consider downsizing their living space, moving to a more affordable location, or negotiating rent reductions with their landlord. By taking proactive steps to manage their finances and reduce the burden of high rent, individuals can work towards achieving greater financial stability and security.

Is Parckside Village Branford Rent Income-Based? What to Know

You may want to see also

Frequently asked questions

Financial advisors generally recommend that no more than 30% of your gross income should go towards housing costs, including rent. This guideline helps ensure that you have enough money left for other essential expenses, savings, and discretionary spending.

To calculate the percentage of your paycheck that goes to rent, divide your monthly rent by your gross monthly income and then multiply by 100. For example, if your rent is $1,000 and your gross income is $4,000, then 25% of your paycheck goes to rent.

Several factors can influence the percentage of your paycheck that goes to rent, including your income level, the cost of living in your area, the size and type of rental property, and your personal financial goals and priorities. In high-cost-of-living areas, it may be necessary to allocate a larger portion of your income to rent.

To reduce the percentage of your paycheck that goes to rent, you might consider downsizing to a smaller or less expensive rental property, moving to a more affordable area, negotiating a lower rent with your landlord, or increasing your income through additional work or side hustles. Additionally, budgeting carefully and reducing other expenses can help you allocate more of your income to savings and investments.