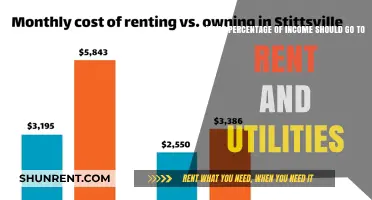

Determining how much of your monthly income should go towards rent is a critical aspect of financial planning. While the 30% rule, which suggests allocating 30% of your gross income to rent, is a widely accepted guideline, it may not be suitable for everyone. Various factors, such as income level, location, and personal financial goals, influence the ideal rent-to-income ratio. Creating a budget tailored to your needs and considering alternative housing options can help you make informed decisions about your rental expenses.

| Characteristics | Values |

|---|---|

| Popular guideline | 30% rule |

| Other guidelines | 20%, 40% |

| 50/30/20 budget | 50% for needs, 30% for non-essentials, 20% for savings or debt repayment |

| 60/30/10 budget | 60% for needs, 30% for non-essentials, 10% for savings |

| Severe rent burden | 50% or higher |

| Ideal rent-to-income ratio | Depends on unique situation and factors like other expenses and goals |

| Average for non-privileged renters | 50% |

Explore related products

![]()

The 30% rule

However, critics argue that the 30% rule is outdated and irrelevant in today's economic landscape. It does not account for modern expenses beyond basic living costs, such as student loan payments, retirement savings, childcare, and other substantial expenses. Additionally, the rule may not be practical in expensive rental markets like New York City or San Francisco, where rents are well over $3000 for a one-bedroom apartment.

While the 30% rule provides a general guideline, it may not be suitable for everyone. It is important to consider individual circumstances, such as income level, cost of living in the desired location, and other financial goals and expenses. Creating a personalised budget that takes into account all expenses, not just rent, can be a more effective approach to determining an appropriate rental budget.

In conclusion, while the 30% rule offers a starting point for budgeting, it should be adjusted based on individual needs and financial responsibilities.

Rent Covered: Making Triple the Rent Money

You may want to see also

Explore related products

![]()

Rent-to-income ratio

The rent-to-income ratio is a popular guideline used by renters and landlords to determine how much of your monthly income should go towards rent payments. This ratio is calculated by dividing your monthly rent payment by your gross monthly income, which is your income before taxes and other deductions.

One of the most well-known guidelines is the 30% rule, which suggests that individuals should spend around 30% of their gross income on rent. This rule aims to strike a balance between comfort and affordability, allowing individuals to cover housing costs while saving for financial goals. However, it is not a one-size-fits-all solution, and factors such as income level, location, and personal financial goals play a significant role in determining the ideal rent-to-income ratio for an individual.

For example, in expensive markets like New York City or San Francisco, where median rents are high, adhering to the 30% rule may not be feasible. In such cases, individuals may consider alternative budgets like the 50/30/20 or 60/30/10 rule. The 50/30/20 budget allocates 50% of your income to needs (rent, utilities, groceries, etc.), 30% to non-essentials (entertainment, dining out), and 20% to savings or debt repayment. The 60/30/10 budget is similar but allocates 60% to needs, which may be more realistic for those with higher costs of living.

Additionally, it's important to consider other factors that can impact your financial stability, such as debt, expenses, and savings. A rent-to-income ratio of 50% or higher is considered a severe rent burden and may indicate financial instability. Conversely, a low rent-to-income ratio is a positive indicator of financial stability, allowing for more savings and investments.

Ultimately, the ideal rent-to-income ratio depends on your unique circumstances, including income level, location, and financial goals. While the 30% rule is a widely accepted guideline, it may not apply to everyone, and individuals should assess their situation to determine the appropriate ratio that aligns with their needs and budget.

Understanding First and Last Month's Rent Requirements

You may want to see also

Explore related products

![]()

50/30/20 budget

A popular guideline is the 30% rent rule, which states that no more than 30% of your gross monthly income should be spent on rent. However, this may not always be feasible depending on where you live, and other factors such as your income level.

If the 30% rule doesn't work for your situation, the 50/30/20 budget rule could be a good alternative. This rule was popularized by US Sen. Elizabeth Warren in her book, "All Your Worth: The Ultimate Lifetime Money Plan." It is a simple and straightforward rule that can help you draw up a reasonable budget that you can stick to over time to meet your financial goals.

The 50/30/20 rule involves splitting your after-tax income into three categories of spending:

- 50% for needs: This includes essential expenses like rent, utilities, groceries, transportation, and student loan payments.

- 30% for wants: This is for discretionary items, entertainment, and dining out.

- 20% for savings and debt repayment: This is for your future, including emergency funds, retirement accounts, or saving for a down payment on a home.

The 50/30/20 rule is flexible and can be adjusted to fit your financial circumstances. For example, if saving or paying down debt is a priority, you can reduce the 'wants' bucket and increase the 'savings' bucket. It is a useful guideline to help you prioritize your expenses and ensure your essential needs are met, while still allowing for some discretionary spending.

It is important to note that this rule is just a guideline, and budgets should be adaptable to your unique situation and goals.

Boat Rentals in Florida: What You Need to Know

You may want to see also

Explore related products

![]()

Location

The location of your rental property is a crucial factor in determining how much of your monthly income should go towards rent. Here are some key considerations regarding location:

- Cost of living in the area: The cost of living varies significantly across different locations. For example, renting in high-cost cities like New York or San Francisco will likely require a larger portion of your income compared to more affordable areas. The 30% rule, a popular guideline, may not be feasible in expensive cities, and you may need to allocate a higher percentage of your income to rent.

- Distance from the city centre: Living farther from the city centre is usually more affordable in terms of rent. However, consider the potential increase in transportation costs for commuting to work or social engagements. Calculate whether the savings in rent outweigh the additional transportation expenses.

- Inclusion of utilities and amenities: In some locations, rentals may include utilities such as gas and water, or amenities like an on-site gym or in-unit laundry facilities. These inclusions can save you money on utility bills and additional costs such as gym memberships or trips to the laundromat. Therefore, the overall savings might justify a higher rent in these locations.

- Local rental market: Understand the rental market in your desired location. In competitive real estate markets, you may need to be more flexible with your budget and consider alternatives to the 30% rule. Research the average rent prices in the area and be prepared to adjust your budget accordingly.

- Neighbourhood preferences: Your preferred neighbourhood can impact the rent you pay. For example, a young family might be willing to pay a premium to live in an area with good schools, while city-dwelling professionals might opt for a conveniently located small apartment, potentially sharing with roommates.

Remember, while the 30% rule is a widely accepted guideline, it may not apply to all locations and situations. It's important to consider your unique financial circumstances, income level, and the specific location you're targeting to determine an appropriate budget for rent.

Late Rent Fees: Understanding Typical Charges

You may want to see also

Explore related products

$9.99 $24.99

![]()

Additional costs

When deciding on a rental property, it's essential to consider additional costs beyond the monthly rent instalments. These extra expenses can significantly impact your finances, and it's advisable to create a realistic budget that accounts for these costs. Here are some crucial additional costs to consider:

Utilities

Some rentals include utilities such as gas and water in the rent, while others do not. When budgeting, be sure to factor in these costs, as they can add up quickly. In addition to utilities, don't forget to include the cost of internet and cable services, which are essential for many people.

Insurance

Renters' insurance is another crucial expense to include in your budget. This type of insurance protects your personal belongings and provides liability coverage if someone is injured on the rental property. While it may not be mandatory, it is highly recommended to safeguard yourself financially.

Transportation

The location of your rental property can impact your transportation costs. If you choose to live farther from the city centre, you may face higher commuting expenses. On the other hand, living closer to work and social engagements can reduce transportation costs, but rent prices in these areas tend to be higher. Consider your lifestyle and transportation needs when deciding on a rental property.

Amenities and Services

On-site amenities like a gym or laundry facilities can save you money on a gym membership or trips to the laundromat. When comparing rental options, factor in the value of these perks. Additionally, consider the cost of parking, as some rentals may charge extra for a parking space or garage.

Pet Fees

If you have pets, be prepared for additional costs. Many landlords charge pet fees or deposits to cover potential damage or cleaning expenses. These fees can vary, so be sure to inquire about them before signing a lease.

Security Deposits and Move-in Expenses

When moving into a new rental, you may need to pay a security deposit, which is typically equivalent to one month's rent. Additionally, there may be broker's fees or the cost of new furniture to consider. These move-in expenses can add up, so it's essential to plan for them in your budget.

While the 30% rule is a popular guideline for determining how much to spend on rent, it may not fit every situation. Creating a budget tailored to your needs and considering the additional costs mentioned above will help you make an informed decision about your rental choices.

Best Android Rental Apps: Your Ultimate Guide

You may want to see also

Frequently asked questions

While the general rule is that no more than 30% of your gross monthly income should go towards rent, this is not a one-size-fits-all solution. The ideal rent-to-income ratio depends on your unique situation and factors like your other expenses and goals.

The 50/30/20 budget is a guideline that suggests you allocate 50% of your monthly income toward needs, such as rent, utilities, and groceries, 30% on non-essentials like entertainment and dining out, and 20% for savings or debt repayment.

The 60/30/10 budget is similar to the 50/30/20 budget but may be a better fit if 50% doesn't seem like enough. In this case, 60% of your after-tax income is allocated to needs.

To calculate your rent-to-income ratio, divide your monthly rent payment by your gross monthly income (income before taxes and other expenses). For example, if your rent is $2,000 per month and your gross monthly income is $4,000 per month, your rent-to-income ratio is 50%.

Spending more than 30% of your income on rent may not be the best option, as it could impact your ability to afford other essential expenses. However, it depends on your financial situation and goals. If you live in an expensive market, it may be difficult to stick to the 30% rule, and you may need to compromise with a higher rent-to-income ratio.