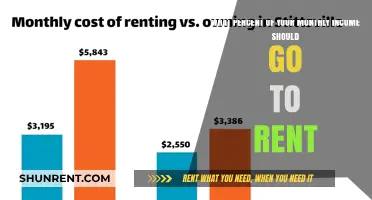

Deciding how much of your income to allocate to rent and utilities is a crucial aspect of financial planning. While the 30% rule, which recommends that no more than 30% of your gross income should be spent on rent and utilities, is a popular guideline, it may not be suitable for everyone. The 50/30/20 budget rule is an alternative, suggesting 50% for needs, 30% for wants, and 20% for savings and debt repayment. However, the ideal rent-to-income ratio depends on individual circumstances, including location, cost of living, income level, and financial goals.

| Characteristics | Values |

|---|---|

| Common rule of thumb | No more than 30% of income should go to rent and utility payments each month |

| Origin of the 30% rule | Housing initiatives introduced by the federal government in the 1960s |

| Alternative budgeting rule | 50/30/20 rule: 50% for needs, 30% for wants, 20% for savings and debt repayment |

| Average monthly expenses | Vary depending on location's cost of living, optional costs like renter's insurance, and income level |

| Rent-to-income ratio | Divide monthly rent payment by gross monthly income |

Explore related products

What You'll Learn

![]()

The 30% rule

The rule is not set in stone and may not work for everyone. It is important to consider individual circumstances, such as location, cost of living, debt payments, and financial goals. For example, in high-cost-of-living areas like New York City or San Francisco, sticking to the 30% rule may not be feasible due to high rent prices.

To determine how much you can afford to spend on rent, you can use the 50/30/20 budget rule. This rule recommends allocating 50% of your income to needs (including rent, utilities, and groceries), 30% to wants (such as clothing and entertainment), and 20% to savings and debt repayment. This approach provides a more nuanced way to budget and ensures you can build savings into your monthly expenses.

Additionally, there are other ways to reduce rental costs, such as finding a roommate to split the cost, taking advantage of move-in deals or resident referral programs, and shopping around for cheaper insurance options.

Rent Payment: Behind or Ahead?

You may want to see also

Explore related products

![]()

The 50/30/20 rule

A common rule of thumb for renters is that no more than 30% of their income should be spent on rent and utilities. This guideline, known as the 30% rule, dates back to housing initiatives introduced by the US federal government in the 1960s. However, this rule may not work for everyone, and there are alternative budgeting methods, such as the 50/30/20 rule.

- 50% for needs

- 30% for wants

- 20% for savings or paying off debt

The first 50% of your income should be allocated to needs, such as rent, utilities, groceries, insurance, transportation, and minimum debt payments. These are critical costs that are necessary for daily living and are incurred on a monthly basis.

The second 30% of your income is for 'wants' or discretionary items. These are non-essential expenses that you spend money on by choice, such as clothing, dining out, entertainment, and travel.

The final 20% of your income is for savings and additional debt payments. This includes retirement savings and non-retirement investments. It is important to prioritize creating an emergency fund for unforeseen monetary costs, such as job loss or unexpected medical expenses.

To apply the 50/30/20 rule, it is recommended to first calculate your monthly after-tax income. Then, track your expenses for a month to identify which category (needs, wants, or savings) they belong to. This will help you allocate your budget accordingly and make any necessary adjustments.

Hotel Renting Age: Understanding the Legal Requirements

You may want to see also

Explore related products

![]()

Location and cost of living

The location and cost of living play a significant role in determining how much of your income should go towards rent and utilities. The general rule of thumb is that no more than 30% of your income should be spent on rent and utilities, but this may not always be feasible depending on where you live. For example, in high-cost cities like New York City or San Francisco, the median rent for a one-bedroom apartment is well over $3,000, which may exceed the 30% guideline.

Cost of living indices and calculators can be useful tools to compare the expenses associated with different locations. These tools consider various factors, including housing affordability, transportation costs, food prices, taxes, healthcare costs, entertainment, and education expenses. For instance, the cost of living in California is 38% higher than the national average, with San Francisco being 71% higher. In contrast, Texas has a cost of living that is 7% lower than the national average, and Florida is 2% lower.

When considering your location and budget, it's essential to factor in additional costs or savings associated with your rental choice. For example, living farther from the city center is often more affordable in terms of rent but may result in higher transportation costs. On the other hand, choosing a rental with amenities like an on-site gym or in-unit laundry can save you money on gym memberships or trips to the laundromat.

To make an informed decision, you should also consider your income, financial goals, and personal preferences. Do you prefer the convenience of living in the city centre or the quieter surroundings of the countryside? Are you willing to compromise on certain amenities or commute longer distances? By using cost-of-living calculators, comparing rental options, and considering your priorities, you can determine the ideal location that aligns with your budget and lifestyle choices.

Commercial Rent Sales Tax: Which States Charge?

You may want to see also

Explore related products

![]()

Financial goals and expenses

When it comes to financial goals and expenses, the percentage of income spent on rent and utilities is a key consideration. While guidelines such as the 30% rule and the 50/30/20 budget can provide a starting point, the ideal percentage may vary depending on individual circumstances and financial goals.

The 30% rule, with roots in public housing regulations from the 1960s, suggests that no more than 30% of gross monthly income should be spent on rent and utilities. This rule has been used by landlords to assess tenants' affordability and provides a standard guideline for housing costs. However, it may not be suitable for everyone, especially in high-cost cities or with varying income levels.

The 50/30/20 budget is an alternative framework. It recommends allocating 50% of net income to essential needs, including rent, utilities, groceries, insurance, and debt payments; 30% to discretionary spending, such as dining out and entertainment; and 20% to savings and additional debt payments. This approach offers a more nuanced view of finances, allowing for savings and debt repayment while covering essential expenses.

Other factors to consider when determining the percentage of income for rent and utilities include location, cost of living, financial goals, and additional expenses. Location plays a significant role, as living further from city centres may reduce rent but increase transportation costs. Financial goals, such as saving for retirement or paying off student loans, can influence the preferred allocation of funds. Additionally, expenses like moving costs, renter's insurance, and parking fees should be factored in when budgeting for rent and utilities.

To make informed decisions, individuals should calculate their rent-to-income ratio and use budgeting tools. Examining spending habits and cutting back on non-essential expenses can help free up income for rent and utilities, while also contributing to financial goals.

In summary, while guidelines provide a starting point, determining the percentage of income for rent and utilities depends on individual circumstances. Considering location, expenses, and financial goals is crucial for effective financial planning.

How Much Does It Cost to Rent a Salon Booth?

You may want to see also

Explore related products

![]()

Additional housing costs

When it comes to additional housing costs, there are several factors to consider that can significantly impact your overall expenses. Here are some key points to keep in mind:

- Location and Commute: The location of your rental property can affect various additional costs. Living farther from city centres is often more affordable in terms of rent, but transportation costs to commute to work or social engagements can add up quickly. Consider the trade-off between rent prices and transportation expenses when deciding on a location.

- Utilities and Amenities: Some rentals include utilities such as gas, water, electricity, and internet in the rent, while others leave these as separate bills. Additionally, look for properties with amenities like an on-site gym or in-unit laundry, as these can save you money on a gym membership or trips to the laundromat.

- Homeowners' Expenses: If you're a homeowner, there are additional costs to consider beyond your mortgage payment. These include homeowners' insurance, property taxes, homeowners association dues or fees, and maintenance or repair expenses. Don't forget to factor in these ongoing costs when budgeting for homeownership.

- Rental Insurance and Deposits: As a renter, you may need to budget for rental insurance, which can protect your personal property and provide liability coverage. Additionally, be prepared for security deposits when signing a new lease. While you usually get these back if you leave the property in good condition, they can be a significant upfront cost.

- Room Additions and Renovations: If you're considering adding space or renovating your home, be aware that these projects can be costly. The cost will depend on factors such as location, size, complexity, and the type of room. Financing options like home equity loans or lines of credit can help, but be sure to get multiple quotes from contractors to understand the full financial commitment.

- Cost of Living Adjustments: Keep in mind that the cost of living varies significantly across different locations. For example, rent in cities like New York or San Francisco tends to be much higher than in smaller towns or rural areas. Adjust your budget accordingly if you're moving to an area with a higher or lower cost of living.

Late Rent Fees: Charging Tenants Fairly

You may want to see also

Frequently asked questions

The 30% rule states that no more than 30% of your gross monthly income should be spent on rent and utilities. This rule is based on 1969 public housing regulations, which capped public housing rent at 25% of a tenant's annual income. However, this rule may not be suitable for everyone, as it does not account for individual variations and modern financial obligations.

One alternative is the 50/30/20 rule, which divides your monthly net income into three spending categories: 50% for needs (rent, utilities, groceries, insurance, debt payments, etc.), 30% for wants (clothing, dining out, entertainment, etc.), and 20% for savings and debt repayment.

To calculate your rent-to-income ratio, divide your monthly rent payment by your gross monthly income (income before taxes and other expenses). For example, if your rent is $2,000 per month and your gross monthly income is $4,000 per month, your rent-to-income ratio would be 50%.